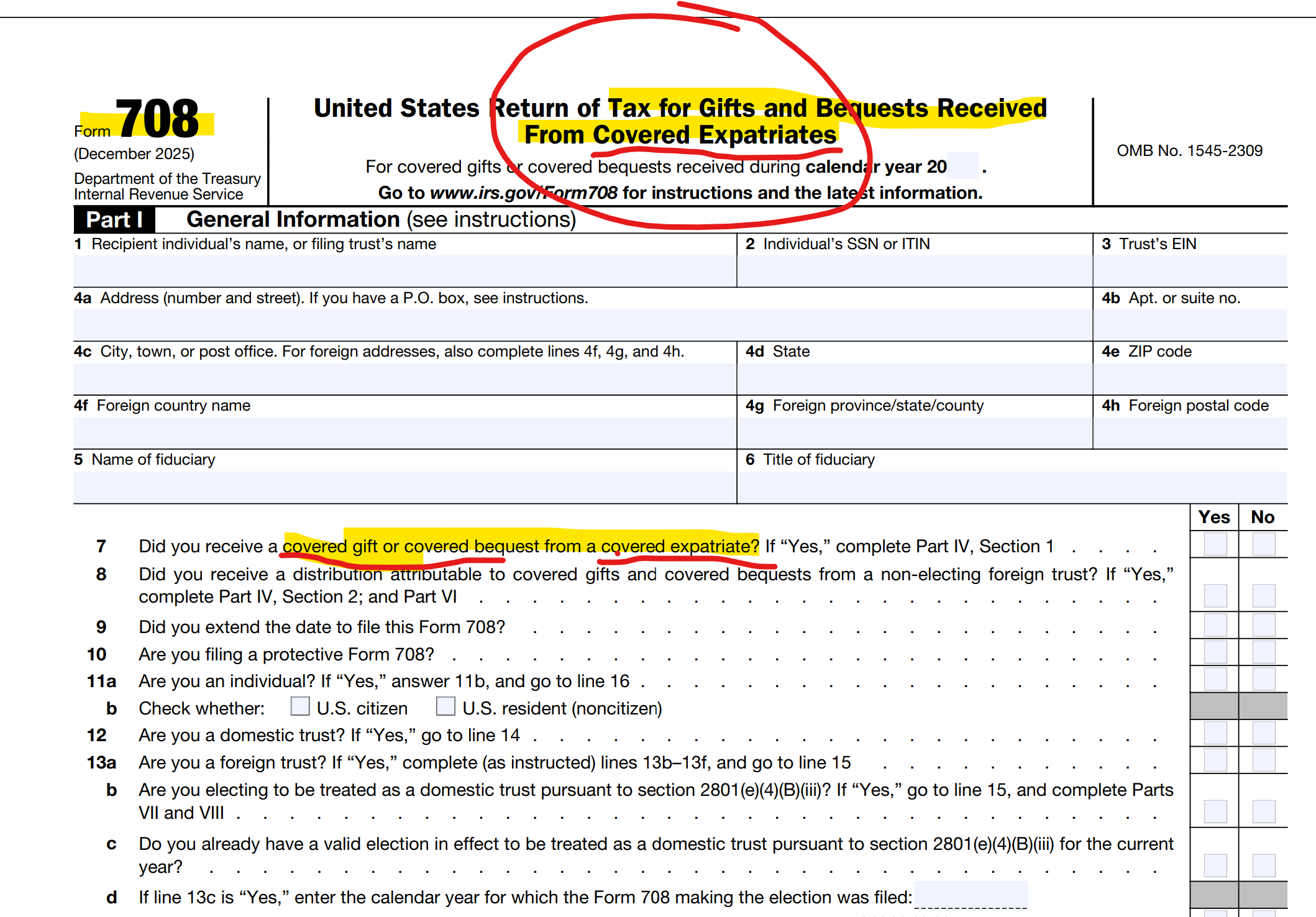

What is the certification requirement under Section 877(a)(2)(C)?

A former U.S. citizen or long-term green card holder (a lawful permanent resident, or LPR) becomes a “covered expatriate” under Section 877(a)(2)(C) if they fail to certify, under penalty of perjury, that they have met their federal tax requirements for the 5 preceding taxable years. The statute treats a person as covered if “(C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.” A “covered expatriate” is a person who triggers the U.S. exit tax rules on giving up citizenship or LPR status.

What makes someone a “covered expatriate”?

If you expatriated after June 16, 2008, the expatriation rules apply if any one of these statements is true:

Your average annual net income tax liability for the 5 tax years ending before the date of your expatriation is more than the listed amount.

Your net worth is $2 million or more on the date of your expatriation.

You fail to certify on Form 8854 that you have complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.

The third test is the certification requirement, and it is the one tied to the timing question below.

Does an IRS form or its instructions carry the “force of law”?

An IRS form and its conditions may not carry the “force of law.” Treasury and the IRS cannot create law by publishing a substantive rule in a form. The statute is what binds. This matters because a form instruction can state a condition that the statute itself does not, and anyone citing a form will want to keep that distinction in mind.

Do the Form 8854 instructions require tax compliance before the expatriation date?

The instructions read that way. The Form 8854 instructions state that the certification must reflect that you have “complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.” Taken literally, that language points to compliance completed before the expatriation or renunciation date. The statute, Section 877(a)(2)(C), does not specify whether the certification has to be made before or after the date of loss of nationality.

Can you come into compliance after renouncing and still avoid covered expatriate status?

This is the open question the form instructions raise. If the instructions are correct, a person could not satisfy the rule by attempting to comply with all federal tax obligations after renouncing. Under that reading, coming into compliance for 5 years and then filing Form 8854, all after taking the oath of renunciation, would not let the person avoid “covered expatriate” status. The statute itself does not say the certification must come before the date of loss of nationality, so whether the instructions can impose that timing is unsettled.

Are there Treasury regulations that settle this question?

No. Treasury has issued no regulations on this point to date. There are only a few notices. One of them is IRS Notice 2009-85 on expatriation, and its own “force of law” is itself open to question. Without regulations, a form instruction is not the same as binding law.

Could the IRS still challenge someone who complies after renouncing?

Yes. Even where a form instruction may not carry the force of law, the IRS may still challenge a former U.S. citizen or LPR who does not also meet the condition set out in the IRS’s own instructions. The agency could argue that the person failed the certification requirement of Section 877(a)(2)(C) by not satisfying tax compliance before the expatriation date.

Why does this matter before taking the oath of renunciation?

The timing of tax compliance is a detail a former U.S. citizen or green card holder may want to weigh carefully before renouncing. The statute is silent on whether the certification must come before the date of loss of nationality, while the form instructions point to compliance before that date, so the literal-statute reading and the form-instruction reading can diverge. Consult an experienced attorney before rushing off to take the oath of renunciation.

Why Long-Term Green Card Holders Cannot Escape the Exit Tax Rules

When long-term green card holders give up their green card, they face the same exit tax rules as US citizens who renounce citizenship. There is one exception in the law that allows certain dual citizens by birth to avoid covered expatriate status even if they meet the income or asset tests. Long-term green card holders cannot use it. Here is why.

When you give up your green card (or renounce US citizenship), the law determines whether you are a covered expatriate. You are a covered expatriate if you meet any one of three tests: an average annual income tax liability above an inflation-adjusted threshold, a net worth of $2 million or more on the date of expatriation, or a failure to certify 5 years of US tax compliance – where it is commonly certified on IRS Form 8854.

Meeting even one of these three tests makes you a covered expatriate. All three tests apply equally to US citizens who renounce and to long-term lawful permanent residents (LPRs) who give up their green card.

Is there an exception to the income and asset tests?

Yes, for some people. Under IRC Section 877A(g)(1)(B), certain individuals are exempt from the income and asset tests. If this exception applies to you, you can avoid covered expatriate status even if your net worth exceeds $2 million or your income exceeds the threshold. The certification requirement under Section 877(a)(2)(C) still applies to everyone, including those who qualify for this exception.

Who can use this exception?

The exception is narrow. Under the statute, it applies only to an individual who: became a citizen of the United States and a citizen of another country at birth; as of the date of expatriation, continues to be a citizen of and is taxed as a resident of that other country; and has been a US resident for no more than 10 taxable years during the 15-year period ending with the taxable year of expatriation. Only someone who acquired US citizenship automatically at birth, while also holding citizenship of another country from birth, can potentially qualify.

Why green card holders cannot use it

Lawful permanent residents are not US citizens. They hold a green card, which is a grant of permanent resident status, not citizenship. Because the exception in Section 877A(g)(1)(B) applies only to individuals who became US citizens at birth, long-term LPRs cannot satisfy this requirement by definition. The exception is simply not available to them.

What this means if you are a long-term green card holder

A long-term LPR who meets either the $2 million asset test or the income tax liability test will become a covered expatriate, even if they fully satisfy the 5-year certification requirement. Satisfying the certification requirement is necessary for everyone, but for long-term LPRs it is not sufficient on its own. If you also meet the income or asset test, you are a covered expatriate regardless.

The consequences include the mark-to-market exit tax on unrealized gains and the Section 2801 tax on covered gifts and bequests to US persons. These consequences can affect your US family members for decades. Understanding them well before you give up your green card, not after, is the only way to plan for them.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

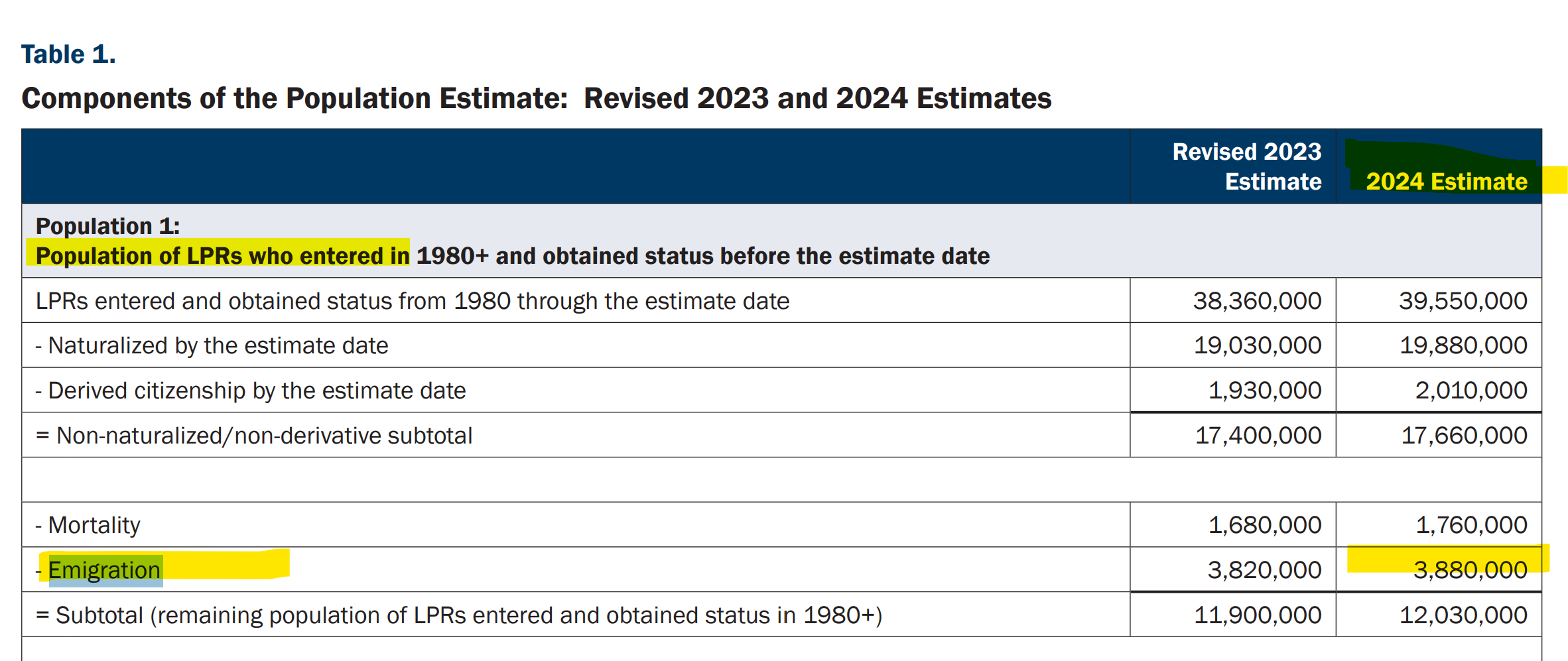

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Understanding State Income Taxes and Global Tax Planning for Expatriates (Part I of II)

Assets and income earned in high tax states such as California and New York, are taxed very differently compared to low-tax states such as Texas, Nevada, Florida or Tennessee. Focusing on “expatriation” (e.g., renouncing USC or abandoning LPR status) of the individual might be misplaced if the person wants to live mostly in the United States. See earlier post, Form 8854 Filing: TIGTA Report Reveals Compliance Gap

Does TIGTA have the Answer: to the Question – How many former U.S. citizens and long-term lawful permanent residents have filed and should have filed IRS Form 8854?

The short answer to the question above – is NO!

The government does not know how many IRS Forms 8854 should have been filed.

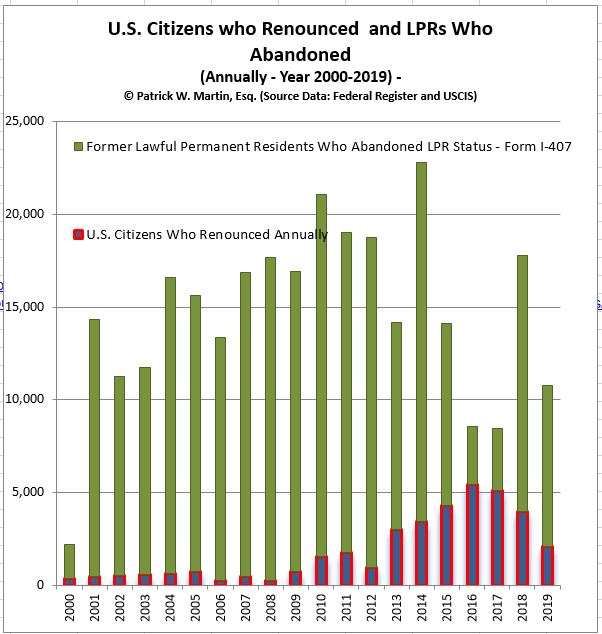

Note the total numbers of 8854 returns filed as reported in Figure 2 of the TIGTA Report were less than 25,000 during a ten year period. This report focuses really only on former U.S. citizens (“USC”) who have renounced their citizenship. Not on lawful permanent residents (“LPRs), which during that same ten year period there were around 200,000 who filed USCIS Form I-407.

* How Many Individuals Should have Filed Form 8854?

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

Immigration Forms, I-407; I-485, Application to Register Permanent Residence or Adjust Status & Tax Forms, 1040, 1040NR, 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114, etc. etc. (Part I of III)

The U.S. tax law is complex, including when an individual (i) becomes and (ii) ceases to be, a U.S. income tax resident (USITR). USITR is not a technical term used under the tax law. The U.S. tax and information reporting requirements are very different depending the status of an individual. Anyone who is not a United States citizen, is either a –

“Resident alien“, or a

“Nonresident alien” as the tax law defines both of these categories.

You can’t be both.

“Resident aliens” are generally also “United States persons” (both technical terms in the federal tax law).

“Non-resident aliens” as defined are necessarily not “United States persons.”

Being one versus the other has huge U.S. tax and reporting consequences.

An individual who is a “lawful permanent resident” as referenced in the tax law (Section 7701(b)(6)) cross-references the U.S. immigration law. The first requirement of that statutory tax rule in § 7701(b)(6)(A)) is that “(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws [such status not having changed]. . .[emphasis added]” This means the tax definition is dependent upon the immigration laws, which are found in Title 8, Immigration and Nationality Act. Importantly, the last part of that sentence (i.e., [such status not having changed] is a requirement in the immigration law (Title 8), but does not appear in the tax definition.

The term “lawful permanent resident” cannot be found in Title 8 as a noun or object (i.e., the individual). Instead, the immigration law defines the status of a person in 8 U.S. Code § 1101(a) as follows:- “. . . (20) The term “lawfully admitted for permanent residence” means the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed.“

This analysis is fundamental to be able to determine whether an individual who holds a “green card” in their pocket even has the status of being “lawfully admitted for permanent residence. . . such status not having changed.” It’s a fundamental legal question under immigration law that must be answered first, to then be able to answer the tax question.

Each form an individual files or does not file (e.g., IRS tax form 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114; and immigration forms, e.g., I-485, I-407, etc.) can have a potential impact on the tax residency status of an individual.

The immigration law and when forms, such as Form I-485, Application to Register Permanent Residence or Adjust Status are submitted to the U.S. federal government can have an impact on this determination. The government can use it against the individual as they did unsuccessfully in Aroeste (see below – Pages 9 and 11 of 17); asserting that Mr. Aroeste waived the treaty by not submitting certain forms.

The entire case from the Federal District Court can be read here: Aroeste v. United States, 22-cv-00682-AJB-KSC (20 Nov. 2023):

The tax residency analysis for those who have kept their “green card” in their pocket, can be even more complex as was analyzed by the Court. There are additional provisions of the law that must be considered including old Treasury Regulations that pre-date many provisions of various U.S. income tax treaties.

For instance, each of the following federal tax statutory rules, which will be considered in more detail in later posts (II and III):

Additional posts will review the impact of these provisions in the law and how various immigration forms (including I-485 and I-407, Record of Abandonment of Lawful Permanent Resident Status) and tax forms (including 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858) and FinCEN form 114, can impact the determination of whether someone who has a “green card” in their pocket is or is not a United States person.

What Questions Need to be Asked if You Live (with a “green card”) in one of the 67 Countries – with a U.S. Income Tax Treaty?

Depending upon the factual circumstances of each individual, they may be able to benefit from the international tax treaty law articulated by the U.S. Federal District Court in Aroeste v United States – Order (Nov 2023). Future posts will explore the legal relevance of some of the following questions to consider:

Has the individual filed any U.S. federal income tax returns since leaving the United States?

Was a professional tax return preparer hired or consulted about the filing of a federal income tax return (e.g., a certified public accountant, an enrolled agent, a full time tax return preparer, ta tax attorney, etc.)?

Has the individual been filing IRS Form 1040 Resident Tax Returns in the same way Mr. Aroeste was filing – based upon the advice (that turned out to be erroneous -although given in good faith) from their U.S. tax return preparer?

What steps if any have been taken to notify the U.S. federal government (irrespective of the agency) regarding their physical residency outside the United States?

This information is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

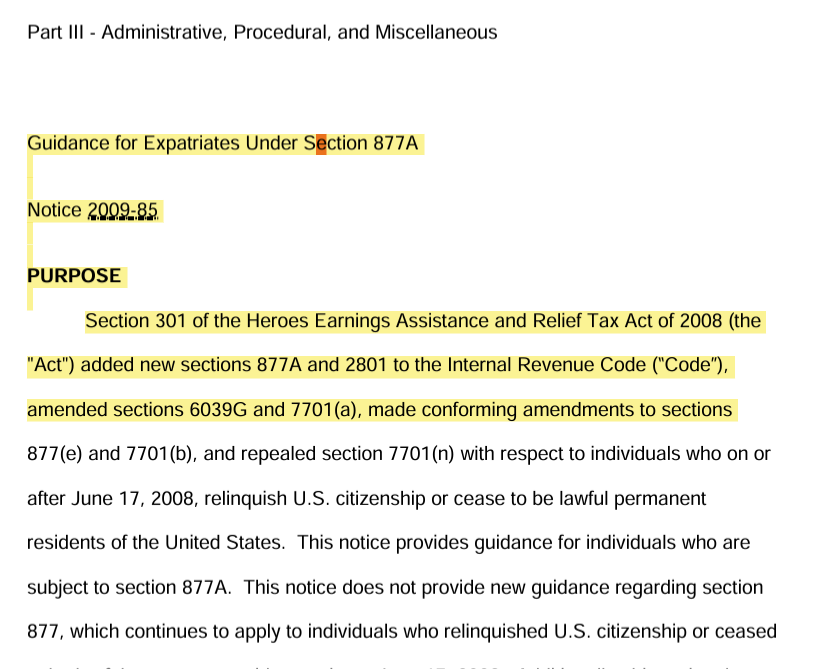

Federal Court Determines IRS “Guidance for Expatriates Under Section 877A” – IRS Notice 2009-85: “Is Not Binding Authority”

The Federal District Court made numerous key legal findings in its Order on November 20, 2023; in Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. One of the more significant findings was that IRS Notice 2009-85 is not binding authority. This blog is dedicated to tax expatriation related matters under U.S. law.

IRS Notice 2009-85 is Not Binding Authority per the Court

expatriation.com has represented him for several years throughout the IRS audits and the on-going U.S. Tax Court cases along with his wife.

While many may consider this case to be a Title 31/FBAR case (which it is), it has greater ramifications under the tax expatriation laws in the author’s view. The finding by this Court regarding IRS Notice 2009-85 is significant with far reaching implications. The IRS Notice 2009-85 is broad in its scope and is more than 60 pages in length. It notes that, “Section 877A(i) provides that the Secretary shall prescribe such regulations as may be necessary or appropriate to carry out the purposes of section 877A.” (p.4)

No Treasury Regulations Ever Issued – After 15 Years of IRS Notice 2009-85

The Treasury Department never issued regulations under 877A, which is now 15 years old. The notice provides the historical background as follows:

Notice 2009-85 PURPOSE Section 301 of the Heroes Earnings Assistance and Relief Tax Act of 2008 (the “Act”) added new sections 877A and 2801 to the Internal Revenue Code (“Code”), amended sections 6039G and 7701(a), made conforming amendments to sections 877(e) and 7701(b), and repealed section 7701(n) with respect to individuals who on or after June 17, 2008, relinquish U.S. citizenship or cease to be lawful permanent residents of the United States. This notice provides guidance for individuals who are subject to section 877A.

The Court in Aroeste concluded that Mr. Aroeste ceased to be a lawful permanent resident.

Specifically, the Court finds Aroeste . . . ceased to be treated as a lawful permanent resident of the United States because he commenced to be treated as a resident of Mexico under the Treaty, did not waive the benefits of such Treaty, and notified the Secretary of the commencement of such treatment.

Many practitioners have questioned the accuracy and validity of many of the conclusions asserted in the 2009 notice; such as the timing of when someone becomes a “covered expatriate”. How and why they become a “covered expatriate” by the concepts introduced in the 2009 notice. The multiple examples presented, reflecting various tax outcomes according to the IRS, were never commented on by the public.

Another question many have raised is the effectiveness of IRS Form 8854? Throughout the notice, the IRS uses the word “must” some 88 times regarding the individual who ceased to be a U.S. citizen or a “lawful permanent resident” (or in some instances references to third parties). Does the IRS imply that if any of these “must”/conditions imposed under the notice are not satisfied, the individual is necessarily a “covered expatriate” with the adverse tax consequences that might follow?

Are their other adverse tax consequences that might follow? For instance, can the IRS repeatedly assert international information penalties regarding the individual’s

companies in her own country,

beneficiary rights of a trust or an estate in her own country, or

other investment assets or financial accounts in her country of residence that might be deemed a “specified foreign financial asset” if the individual is a United States person”?

For instance, the 2009 notice provides that a “covered expatriate” must file a “dual status return” and file a Form 1040NR with a 1040 attached as a schedule for the “year of expatriation”. See, IRS Notice 2009-85, p. 49.

The IRS goes on to say in that notice that individuals “must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation.” Id., p. 50. The government asserts that if this condition is not satisfied, the individual will necessarily be treated as ” . . . covered expatriates within the meaning of section 877A(g) whether or not they also meet the tax liability test or the net worth test.“

These would be pretty damning consequences to an individual, if they otherwise met the statutory test of certifying compliance with the tax laws for the preceding five years.

Importantly, the Court in Aroeste v. United States concluded as a matter of law that 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). It concluded Mr. Aroeste did not need to file Form 8854 with his amended returns. He had filed Form 8833 – treaty based reporting.

The court cited to ” . . . Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.”

None of these comments represent legal advice. Complex laws applied to specific facts require a legal expert to opine on the consequences and recommended courses of action. It is worth noting that individuals who have a “green card” and who have not previously articulated the application of a U.S. income tax treaty, should consider taking proactive steps to protect their rights under the law. Also, United States citizens who formally renounced their citizenship, who may never have taken specific tax reporting positions should consider taking proactive steps to help avoid the risk the IRS might assert substantial penalties or conclude the individual became a “covered expatriate”.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this