Month: June 2014

FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas- It’s All About Information and More Information

An earlier post explained why U.S. citizens (and some LPRs)  cannot sign the new IRS Form W-8BEN. See, IRS Releases New IRS Form W8-BEN. * U.S. citizens and LPRs beware of completing such form at the request of a third party.

cannot sign the new IRS Form W-8BEN. See, IRS Releases New IRS Form W8-BEN. * U.S. citizens and LPRs beware of completing such form at the request of a third party.

IRS Forms, W-8, W-9, W-8BEN-E, W-7, W-8IMY, W-4, W-8ECI, W-8EXP are a confusing alphabet soup of IRS forms. They have become more difficult to understand now because of the intricacies of the law of FATCA. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act.

In short, these forms are designed to “track taxpayers”; their assets and their accounts. The forms track and identify USCs who are individuals and if they are “substantial owners” (basically 10%) in various foreign entities; explained more below.

U.S. tax lingo means that a “taxpayer identification number” (TIN) is a broad definition and can also include all of the following, which are TINs –

- “Social Security Number” (SSN) in the case of certain individuals (USCs, LPRs and those who have permission to work in the U.S. under a particular visa);

- “Individual Taxpayer Identification Numbers” (ITIN) in the case of other individuals who are not USCs or LPRs and not otherwise eligible for a SSN (another post will explain how ITINs are obtained);

- Employer identification numbers (EINs) for certain entities, such as corporations, partnerships and trusts.

Hence, an SSN, ITIN, EIN are all TINs, depending upon which context they are being used.

My earlier post warns U.S. citizens NOT to sign IRS Form W-8BEN, because such certification would be false. – Importantly, no U.S. citizen can legally sign and certify they are NOT a “U.S. person” under U.S. federal tax law. Hence, they cannot sign and complete IRS Form W-8BEN. –

Individual U.S. citizens should normally be signing IRS Form W-9, or the substitute form provided by the financial institution when asked for their U.S. taxpayer status. Banks and other third parties can have their own  substitute returns that comply with the regulations. Hence, the form might not look exactly like the official IRS forms reflected here.

substitute returns that comply with the regulations. Hence, the form might not look exactly like the official IRS forms reflected here.

The IRS Form W-9 is to request the U.S. taxpayer identification number of a U.S. citizen and LPR (or a TIN for a U.S. company – or other company). The IRS version is reflected herein. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs.

Why is all of this important, now with FATCA in effect and operational throughout the world?

There is greater focus on information that will be provided to foreign financial institutions (FFIs) around the world as they collect and track data on their account holders.

In the case of USC (and many – if not most LPRs) individuals residing overseas, they will NOT be able to sign an IRS Form W-8, as explained above and in the prior posts – such as IRS Releases New IRS Form W8-BEN. * U.S. citizens and LPRs beware of completing such form at the request of a third party.

However, if a USC (and/or LPR) is a shareholder, partner or other economic owner in a non-U.S. foreign entity (such as a corporation, certain other type of companies, certain “partnership” and “trusts” – which can be known as a non-financial foreign entity – “NFFE”), the entity itself will be required to identify the “substantial U.S. owners” of the NFFE. Sounds complicated? It is very complicated.

See the key provisions of the IRS Form W-8-BEN-E highlighted in this post that reflects some of these multiple categories. This form requires the person completing it to frankly understand the FATCA regulations (some 450+ pages worth – including preamble) and properly categorize the type of entity/taxpayer in some 30+/- different categories. That is why the Form W-8BEN-E is some 8 pages in length.

Worse, for the person signing it; they must certify under penalty of perjury that it is complete and accurate. There will undoubtedly be numerous good faith errors by those who attempt to complete these new forms. Indeed, the new IRS Form W-8IMY has not even been addressed in this post, which is another form that was substantially modified due to the FATCA regulations.

If this summary has not cleared up the confusion for you; don’t worry, you are not alone!

I will try to continue to provided key summary explanations of these rules during the course of the next few months, as persons need to understand how to complete and implement properly these IRS Forms or the substitute forms provided by various FFIs throughout the world; now including China and Hong Kong!

It is during these next few months (prior to 31 December 2014) that this topic will be of great interest as FFIs around the world request this information from their account holders; not just USCs or LPRs. See, HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

Senator Reed Again Proposes Special “Tax Expatriation” Legislation Adverse to Former Citizens (not LPRs)

This blog has covered a number of posts related to Senator Reed, important to USCs who are considering (or who have already) renounced United States citizenship. See for instance, The 1996 Reed Amendment – The Immigration Law with “No Teeth” and “No Bite”

As previously explained, the 1996 Reed Amendment which is part of the immigration law (Title 8), but not the tax law (Title 26) –

A bit of background on Senator Jack Reed of Rhode Island is worthwhile at this point. Senator Reed has had a long and illustrious public service career in the U.S. government. He has a military background where he studied at West Point, served as an Army Ranger, studied law at Harvard and previously was in the House of Representatives.

Senator Reed tried in 2012 to convince then Department of Homeland Security, Secretary Napolitano to enforce the 1996 Reed Amendment to preclude Facebook co-founder Eduardo Saverin from re-entry to the U.S. after he renounced U.S. citizenship. See portion of the letter in this blog.

Of course, Mr. Saverin would have been obliged to pay any “mark to market” U.S. tax applicable to his assets at the time of expatriation. He could not have escaped taxation under the law as it was written; which is the current law in effect today.

This past week Senator Reed was a sponsor of a new appropriates bill for the Department of Homeland Security; the “2015 Homeland Security” bill that provides for US$47.2B (billion) in appropriates for a range of spending; such as $10.2B for the Coast Guard, $5.5B for Immigration and Customs Enforcement (ICE), $1.6B for the Secret Service, among other spending items.

Senator Reed is identified in his own website as ” . . . A member of the powerful Appropriations Committee, which controls the purse strings of the federal government, Reed has been described by the Boston Globe as “a relentless advocate for his home state.” –

Within Senator Reed’s “2015 Homeland Security” proposed amendments, he apparently introduces a new provision to the immigration law – which is explained in his website as –

- Reed’s provision to help prevent expatriate tax dodgers from reentering the United States calls on DHS to report within 90 days on their efforts to enforce the law that Senator Reed authored to prohibit individuals from reentering the United States if they renounced their citizenship in order to avoid taxes.

This Reed proposal seems very odd, since the motivation of how or why someone renounced their U.S. citizenship or formally abandoned their LPR status, became irrelevant for federal income tax purposes with the 2008 “mark to market” modifications. See, Joint Committee Reports – 2008 Report re: HEROES Act – Mark to Market Regime – New Section 877A (55 pages)

Indeed, the reason or purpose anyone decided to renounce their citizenship, became irrelevant for tax purposes with the 2004 amendments to Title 26. See, more detailed information on this blog in the Government Reports Re – Law.

Senator Reed’s proposal seems even more odd, when one considers that the federal government is already required to publish quarterly the list of USCs who have renounced. See, Will the IRS simply select the list of published former citizens for tax audits?

This begs the question – Why does Senator Reed propose such legislative modifications?

- for political reasons;

- to attract more press;

- to identify those who actually owe taxes – “tax dodgers”; or

- to generally demonize United States citizens living overseas who have decided to shed their USC?

Why does Senator Reed persist on trying to get former USCs barred from re-entering the U.S., if and when they fully comply with the tax provisions; IRC Sections 877, 887A, 2801, et. seq.? See, Reed Asks Homeland Security to Enforce Law on Ex-Citizen Tax

Also, see Senator Reed’s complete 17 May 2012 letter (Reed’s letter to Napolitano) on the subject; which of course was never enforced at the time. It was not enforced by the Department of Homeland Security or the U.S. Justice Department.

Finally, see also, Obtaining a U.S. Visa after Renouncing U.S. Citizenship – The Cloud of the Still Living “Reed Amendment”

Senator Reed’s shadow looms large, at least theoretically, over anyone considering renouncing their United States citizenship.

HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

On the absolute eve of the crucial July 1, 2014 FATCA deadline, China has apparently “reached [an] agreement in substance” -i.e., an IGA with the U.S. Treasury Department.

This has enormous implications, in my view, considering the amount of trade between the two countries and the number of U.S. citizens and LPRs residing in China (not to mention the number of US. companies doing business in China).

There had been much doubt whether China would sign an IGA. See, for instance, China’s Relationship with the Contentious U.S. FATCA. – In my view, had China not agreed to a FATCA IGA, enormous repercussions around the world would have followed – particularly regarding how FATCA would not have been able to be rolled out throughout the major economic countries.

China now joins the other IGA countries “deemed to have been entered into” by a total of some 80+/- countries. See, those countries-jurisdictions that have signed agreements and those who have reached agreements in substance and have consented to being included on [the Treasury] list.

China is now included as of 26 June 2014. Hong Kong had previously entered into a Model 2 IGA in 9 May 2014.

What does this mean for USCs and LPRs living in China and Hong Kong? In short, Chinese and Hong Kong financial institutions (FFIs) and non-financial foreign entities (NFFEs) will need to identify the accounts of USCs and LPRs pursuant to the FATCA rules set forth in the IGA. The reporting extends beyond individuals to companies and trusts which have so-called “substantial U.S. owners”.

Presumably, China will be issuing some type of implementing regulations to provide the details of how these Chinese FFIs and NFFEs will go about collecting this information. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs, for an overview of how these institutions will be requiring specific information of USC and LPR individuals in their home countries.

Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50)

The U.S. Supreme Court upheld as Constitutional the concept of citizenship based taxation in 1924 in Cook v. Tait. In that case, the U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife.

In those years, the Revenue Act of 1921 imposed a top income tax rate of 8%. The IRS made a demand against Mr. Cook to pay his tax. Mr. Cook paid it and sued for refund of the US$1,193 paid. That amount represents about  US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.

US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.

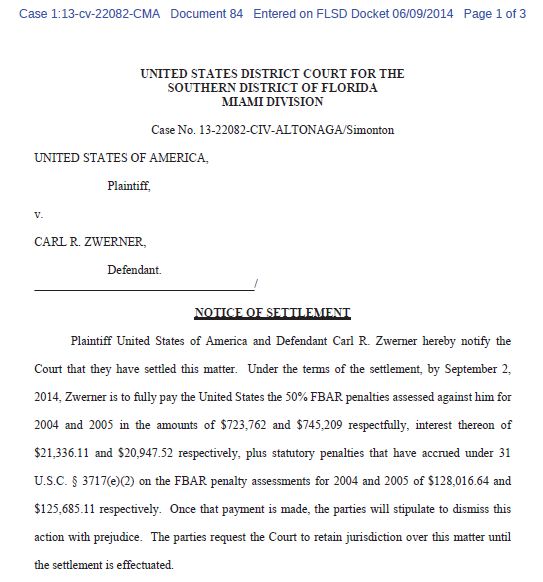

As a point of reference, Mr. Zwerner was alleged to owe US$3,630,119 (on an account with a maximum value during the years at issue of apparently no more than US$1.69M) and ultimately paid about US$ 1.75M (more than he even had in his account?) per the Notice of Settlement filed with the Court referenced here:

Even in 1922 dollars when Mr. Cook was living in Mexico City, the payment by Zwerner of about US$ 1.75M in current dollars, would represent about $123,581 in those dollars. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

There was no Foreign Account Tax Compliance Act (“FATCA”) in the days of Cook in Mexico City, so it would be interesting to know how and why the audit and tax assessment collection was commenced. This was long before e-mails and internet, and there was a very different system of international travel. Communication and technology in 2014 is quite different from technology nearly 100 years ago when the first transcontinental (not transnational) telephone call was made in 1915 a few years before the tax issue arose in the case of Mr. Cook.

Now to the key point of this post. The Supreme Court in Cook vs. Tait framed the question before the Court as follows:

- The question in the case . . . as expressed by plaintiff [Mr. Cook], whether Congress has power to impose a tax upon income received by a native citizen of the United States who, at the time the income was received, was permanently resident and domiciled in the city of Mexico, the income being from real and personal property located in Mexico.

Can the United States impose worldwide taxation on U.S. citizens who permanently live overseas and who only have income from property or services outside the U.S.? Of course, the Supreme Court, said, that such a citizenship based rule was Constitutional. The rationale of the Court was explained in the opinion as follows, specific to the rights of citizenship:

- . . . the scope and extent of the sovereign power of the United States as a nation and its relations to its citizens and their relation to it.’ And that power in its scope and extent, it was decided, is based on the presumption that government by its very nature benefits the citizen and his property wherever found, and that opposition to it holds on to citizenship while it ‘belittles and destroys its advantages and blessings by denying the possession by government of an essential power required to make citizenship completely beneficial.’ In other words, the principle was declared that the government, by its very nature, benefits the citizen and his property wherever found, and therefore has the power to make the benefit complete. Or, to express it another way, the basis of the power to tax was not and cannot be made dependent upon the situs of the property in all cases, it being in or out of the United States, nor was not and cannot be made dependent upon the domicile of the citizen, that being in or out of the United States, but upon his relation as citizen to the United States and the relation of the latter to him as citizen. [emphasis added]

The Supreme Court emphasizes at several points that it is because of the benefits of citizenship and the rights conferred to the citizen of the United States, that the United States government has the Constitutional power to impose worldwide taxation.

What is the difference, if someone is NOT a U.S. citizen? How can the U.S. federal government impose worldwide taxation on property outside the U..S. when the individual is not a citizen, has no right to even enter the United States and generally has no benefits or protections afforded to a U.S. citizen? Indeed, a recent interpretation of the U.S. government in a Justice Department memo spells out the rights of certain U.S. citizens. See New York Times recent article, Court Releases Large Parts of Memo Approving Killing of American in Yemen Targeting Anwar al-Awlaki Was Legal, Justice Department Said

Back on topic, the rationale in Cook v. Tait did not extend to someone who was not a citizen. For example, the Internal Revenue in the 1920s was of course not attempting to impose taxation on Mr. Cook’s Mexican national wife who lived exclusively in Mexico.

Herein, is a most interesting problematic and possibly (maybe – probably?) unconstitutional aspect of current law under the provisions off IRC Section 7701(a)(5)(if the loss of nationality is retroactive to a date long ago in the past but the tax code/IRS is not recognizing that past date as the expatriation date.

If someone has lost all rights to U.S. citizenship years or decades ago, how can the U.S. federal government continue to impose worldwide income taxation for all of the intervening years?

How can the tax law impose a “Constitutional fiction” that a person continues to be “. . . treated as a United States citizen . . . ” simply because they did not file a paper notification with the U.S. federal government. See, Section 7701(a)(50) was adopted and has a very clear timing rule about when a person “. . . cease[s] to be treated as a United States citizen. . . ” It is not the same as for immigration law purposes. It’s a fiction in the tax law as to when one ““. . . cease[s] to be . . . a United States citizen. . . ”

The statute says ” . . . An individual shall not cease to be treated as a United States citizen before the date on which the individual’s citizenship is treated as relinquished under section 877A (g)(4). . .”

How can the U.S. federal government continue to impose U.S. worldwide income taxation on former U.S. citizens because of the provisions under Section 7701(a)(50) and 877A (g)(4)?

The U.S. Supreme Court in Cook vs. Tait found the U.S. citizenship based taxation system as Constitutional since ” . . . government by its very nature benefits the citizen and his property wherever found . . .” and because of “ . . . his relation as citizen to the United States and the relation of the latter to him as citizen. . . . ” [emphasis added]

A person who is not a citizen, obviously does not receive these benefits from the government as does a United States citizen.

In practice, the only body that can determine whether a law is Constitutional or not, is the U.S. Supreme Court. It’s not likely that this question will reach the Supreme Court any time soon; if ever. Meanwhile, the IRS generally has the duty to enforce the law as currently written.

IRS Sting Operation and Criminal Tax Indictments of Canadian Citizens – Investigations Overseas – Enabling U.S. Taxpayers with Offshore Accounts

The U.S. Department of Justice reported that two Canadian citizens along with a U.S. citizen were indicted for enabling tax evasion with offshore accounts. The press release from three months ago, 24 March 2014, can be reviewed here. Some highlights of the press release are below:

- According to the indictment, . . . Poulin, an attorney at a law firm based in Turks and Caicos, worked and resided in Canada and in the Turks and Caicos. His clientele also included numerous U.S. citizens.

- According to the indictment, Vandyk, St-Cyr and Poulin solicited U.S. citizens to use their services to hide assets from the U.S. government. Vandyk and St-Cyr directed the undercover agents posing as U.S. clients to create offshore foundations with the assistance of Poulin and others because they and the investment firm did not want to appear to deal with U.S. clients. Vandyk and St-Cyr used the offshore entities to move money into the Cayman Islands and used foreign attorneys as intermediaries for such transactions.

- According to the indictment, Poulin established an offshore foundation for the undercover agents posing as U.S. clients and served as a nominal board member in lieu of the clients.

The facts of this case will be interesting to cover, to see how and to what extent the IRS and Justice Department will be focusing on U.S. citizens residing overseas and their reporting (or failure to report) their “foreign” accounts; i.e., their financial accounts in their home countries of residence.

Since the withholding tax provisions under the Foreign Account Tax Compliance Act (“FATCA”) come into effect in a matter of days, it will be interesting to see if the government has more indictments along these lines planned for the summer of 2014.

U.S. citizens who are in the process of renouncing citizenship should be aware of each of the steps required as part of the process; both under U.S. federal tax law and immigration law.

Obtaining a U.S. Visa after Renouncing U.S. Citizenship – The Cloud of the Still Living “Reed Amendment”

To state the obvious, every non-U.S. citizen must have a visa (or participate in the visa waiver program as a citizen or national of one of the 38 countries such as Chile, Hungary, Estonia, Spain, Monaco, etc.) to enter into the U.S. There are numerous visas all with different immigration law requirements and restrictions and many which have specific U.S. federal income tax consequences.

A future post with immigration counsel will discuss the type of visas available for entry into the U.S.

To date, I have yet to see any clients not be able to obtain a visa for re-entry back into the U.S.; after renouncing U.S. citizenship.

Importantly, the Attorney General still has the statutory authority to make a determination that a former U.S. citizen is inadmissible under the so-called “Reed Amendment” that was passed into the law in 1996 into the immigration law, Title 8 ((8 U.S.C. § 1182(a)(10)(E)) as part of the so-called Illegal Immigration Reform and Immigrant Responsibility Act of 1996. That provision, which should be obsolete based upon intervening changes in the tax law, nevertheless provides as follows:

- (E) Former citizens who renounced citizenship to avoid taxation

- Any alien who is a former citizen of the United States who officially renounces United States citizenship and who is determined by the Attorney General to have renounced United States citizenship for the purpose of avoiding taxation by the United States is inadmissible.

There are no regulations or administrative guidelines implemented by the US Government agencies to enforce this provision and no former US citizens have ever been found to fall under this category to date. More posts to follow on this important topic, including federal government reports on its applicability.

Please see also, The 1996 Reed Amendment – The Immigration Law with “No Teeth” and “No Bite”

Can the Attorney General make this provision have “teeth”? Will it ever be invoked by the government to make a former U.S. citizen inadmissible into the U.S.?

Wide Window of Wait Times for CLN: One Month to 9 Months (or More?)

The Certificate of Loss of Nationality (“CLN”) is a most crucial part of the steps and process for renouncing U.S. citizenship.

The formal acknowledgement/approval by the Department of State (DOS) is manifested by the issuance of a Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN). See sample form in this post.

For U.S. federal income tax purposes, the actual receipt of the CLN by the individual is necessary for numerous reasons too. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act.

See, also, Who makes the loss of US nationality determination? [Guest Post from Immigration Lawyer], Posted on May 19, 2014

You should be aware that the wait times to receive the CLN can vary wildly depending upon where (which Embassy or Consulate office) and when one goes to take the oath of renunciation. I have seen some issued as soon as 30 days. More commonly, 4 months is a fairly common time frame; but I have also seen cases where it took more than 9 months.

More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The June 2014 changes by the IRS in its offshore voluntary disclosure (“OVD”) program are significant and worthy of discussion for USCs and LPRs residing overseas.

I will dedicate several blogs to this topic over the next few weeks. See, these posts on the topic for additional background: See, “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

See,earlier post –Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking,

This post is dedicated to some background, about the legal framework of the OVD and what the IRS calls “streamlined” filing.

First, it is worth reiterating, that the tax law, Title 26, is not the source of the terms of either the OVD or Streamlined. For some basic background of the statutory regime and Title 26 (along with Title 31, et. seq), see, Why the FBAR (late filed or never filed) is not a requirement for the Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance)

In addition, the Bank Secrecy Law, title 31, is not the source of the terms of either the OVD or Streamlined.

Rather, the Internal Revenue Service (the agency responsible for enforcing Title 26) has created its own terms and conditions as part of both the OVD and the “Streamlined” process. See,the “FAQs” that are published by the IRS: Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers: Effective for OVDP Submissions Made On or After July 1, 2014

The terms of these FAQs are not law. The IRS can change them at anytime and without notice to anyone. Indeed the IRS has changed and modified them on numerous occasions since the initial OVD program in 2009.

Second, it is crucial to understand the basic framework of the law from Title 26 that all USCs living overseas are subject to; and the various consequences of the law. Plus, many LPRs living overseas are subject to Title 26 (but not all of them – depending upon a number of factors). The U.S. tax law is complex and there are numerous compliance requirements with onerous penalties that can be assessed. For instance, see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Also, see, US Citizenship Based Taxation. In addition, see, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

In that post, I summarize the principle criminal statutory rules in Title 26 – which are set out below:

1. Criminal Offenses under Title 26 (Federal Tax Law)

a. Tax Evasion (IRC Section 7201)

b. Filing a False Return or Other Document – Perjury (IRC Section 7206(1) )

- (i) Aiding or assisting in the perpetration of a false or fraudulent document (26 U.S.C. § 7206(2))

- (ii) Removal or concealment with intent to defraud, commonly related to untaxed liquor (26 U.S.C. § 7206(4))

- (iii) Compromises and closing agreements involving fraud or concealment (26 U.S.C. § 7206(5))

c. Failure to File Return, Supply Information, or Pay Tax – (IRC § 7203 – Misdemeanor – up to 12 months imprisonment)

d. Fraudulent Returns, Statements, or Other Documents (IRC § 7207)

e. “Structuring” Transactions to Evade Cash Reporting (IRC § 6050I)

In addition to these tax specific crimes, other key crimes commonly used by IRS CI agents in tax cases, particularly international cases, include:

2. Tax Related Criminal Offenses under Titles 18 and 31 (Not Tax Law Specific)

a. Conspiracy (Section 371 of Title 18)

- (i) Elements of the Offense

- (ii) Penalties and Statute of Limitations

b. False Statements (Title 18 U.S.C. § 1001)

- (i) Penalties and Statute of Limitations

c. Perjury

d. Mail fraud

e. Principals and those Who Aid and Abet (Title 18)

f. Accessory After the Fact

You may be asking – “If the terms and conditions of OVD and Streamlined are not the law – why should I consider either in my circumstances?”

The OVD is a bargain between the IRS/Justice Department and taxpayers. In short, if you participate by its terms, you will not (at least “should not”) be criminally prosecuted. The OVD program is in my view a program worthy of consideration for those who have committed any of the above tax and tax related crimes; and this will depend entirely upon the facts of each case. How, when and if these laws have been violated, can only be analyzed and considered for each particular case, based upon the detailed factual circumstances of each individual.

For those individuals, who have not committed any of the above tax related crimes, the OVD program is probably not a good option for such USC or LPR residing overseas. See an earlier article I published titled – The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

There is one caveat to this issue, which arises from the willfulness FBAR penalty. The government has argued (at least in one case) that multiple year 50% willfulness penalties can apply, even if the individual had no knowledge of the law – See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

Clearly, the facts of the Zwerner case need to be considered carefully in how and why the government argued their position. It seems, maybe the biggest fact used against the taxpayer was that he had “touched the money”; i.e., drawn and spent some of the funds over the years?

Next, if there is little risk of a 50% willfulness penalty and there is no criminal liability, the so-called “Streamlined” process is an option. However, again, the terms of the “Streamlined” are not terms set forth in Title 26; they are made up by the IRS. They also do not bind the IRS. I strongly recommend reading the post, –Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking, which provides the following about the process (before modified in its current form – which continues to be applicable today):

Does any of the above [referring to Streamlined] protect the USC residing outside the U.S. from an audit for any year a U.S. federal income tax return was not filed? The short answer is – NO!

Does any of the above statements in the IRS announcement mean that a USC residing overseas could not be subject to late payment or late filing penalties for not previously filing U.S. tax returns. The short answer is – NO!

Does any provision in the IRS announcement mean the FBAR penalties could not apply for failure to file. The short answer is – NO! See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

Does any of the above statements in the IRS announcement mean that a USC residing overseas can never be subject to penalties for not filing information returns regarding their non-U.S. international assets and “specified foreign financial assets”? The short answer is – NO! See, USCs and LPRs residing outside the U.S. – and IRS Form 8938

Importantly, there is nothing in the law (e.g., Title 26 or elsewhere) that would obligate any USC or LPR residing overseas to participate in either OVD or the “streamlined” process. Both have different consequences, potential benefits, and certainly legal risks.

Finally, the last option, that is actually subject to the law, i.e., Title 26, is filing tax returns through normal channels. Most all U.S. taxpayer file tax returns through this normal procedure.

As always is the case, but particularly for those who have not filed tax returns or FBARs, the facts of each particular case need to be considered, to determine the legal risks, benefits and consequences of any of these three approaches.

The Semantically Driven Vortex of “Relinquishing” vs. “Renouncing”

Guest Post from Immigration Lawyer – Mr. Jan Bejar – The Semantically Driven Vortex of “Relinquishing” vs. “Renouncing”

“Relinquishing” citizenship means to give up U.S. citizenship voluntarily by committing any of the expatriating acts described in INA § 349(a), 8 U.S.C. § 1481(a). One of the expatriating acts described in INA § 349(a)/8 U.S.C. § 1481(a) is “renouncing” or as it says in the statute, “… (5) making a formal renunciation of nationality before a diplomatic or  consular officer of the United States in a foreign state, in such form as may be prescribed by the Secretary of State.”

consular officer of the United States in a foreign state, in such form as may be prescribed by the Secretary of State.”

Renouncing citizenship is a way to relinquish it, so when discussing this form of relinquishment, the two words can be used interchangeably.

For immigration purposes, the distinction between renunciation and the other forms of relinquishment may become meaningful when a former citizen is appealing or challenging the loss of nationality because establishing a lack of intent or duress during a formal renunciation is much more difficult than establishing a lack of intent when performing one of the other expatriating acts. See 7 FAM 1211 (h).

Jan Joseph Bejar, Esq.

(For: JAN JOSEPH BEJAR, APC)

Tel: (619) 291-1112

Fax:(619) 291-1102

E-mail: jbejar@immigrationlawclinic.com

Website: www.immigrationlawclinic.com

New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas – The Thorny “Certification Requirement”

“Be careful what you wish for . . . “, so goes the saying. Yesterday’s post discusses the breaking news of the IRS announcement of revisions to how individuals who have not filed tax returns can “come into compliance”. See, “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

I have argued for years that the IRS has neglected to identify the unique circumstances of USCs and LPRs residing outside the U.S.; and how the OVD programs in particular threw both resident and non-resident U.S. taxpayers into the same big bucket.

There is much to be said about the new “Streamlined” procedure just announced. Particular focus has been made for USCs and LPRs living outside the U.S., and the IRS rules specific to these individuals are set forth in – U.S. Taxpayers Residing Outside the United States.

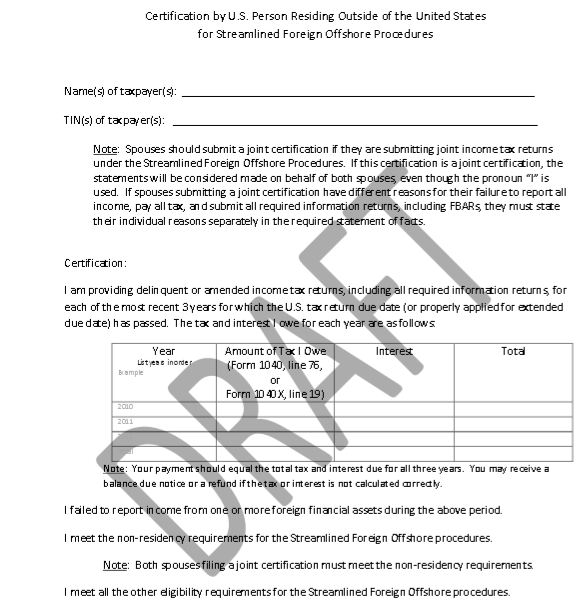

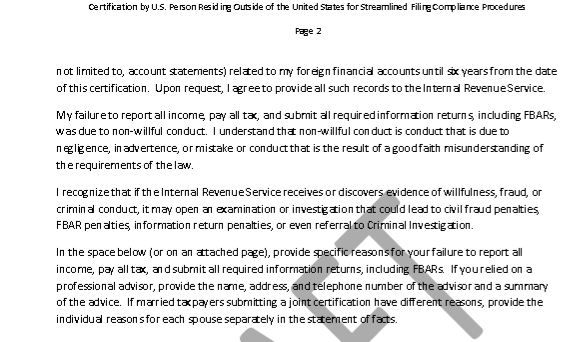

Importantly, a certification must be signed by the taxpayer, subject to the penalties of perjury under U.S. law. The sample IRS certification document, Certification by U.S. Person Residing Outside of the U.S., is set forth in part in this blog –

Signing such a Certification carries with it specific legal rights and obligations to the person who signs and certifies to its accuracy. See, a discussion of what constitutes perjury under the tax code – Filing a False Return or Other Document – Perjury (IRC Section 7206(1) ). See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The summary of the steps regarding certification are explained in the IRS website, and include most importantly the following requirement:

3. Complete and sign a statement on the Certification by U.S. Person Residing Outside of the U.S. certifying (1) that you are eligible for the Streamlined Foreign Offshore Procedures; (2) that all required FBARs have now been filed (see instruction 8 below); and (3) that the failure to file tax returns, report all income, pay all tax, and submit all required information returns, including FBARs, resulted from non-willful conduct.

It’s the last item that carries with it a host of legal responsibilities when certifying under penalty of perjury that ” . . . failure to file tax returns, report all income, pay all tax, and submit all required information returns, including FBARs, resulted from non-willful conduct. . . “

What is “non-willful conduct”? It is the term “willful” that is defined by the Courts, “not – non-willful”; to use the double negative. For a thoughtful discussion on what is willful, I suggest reading a precise overview by Jack Townsend. The New Streamlined Processes’ Requirement of Certifying Non-Willfulness (6/19/14)

He summarizes it – As courts have noted, the word “willful” is a “chameleon” which changes in tone and color according to the Code section involved and the circumstance. See e.g., former Justice Souter’s opinion in United States v. Marshall, 2014 U.S. App. LEXIS 10415 (1st Cir. 2014), discussed in More On Willfulness (Federal Tax Crimes Blog 6/13/14), here. But, I think it is clear that, in both the income tax context and the FBAR context, willful means “voluntary intentional violation of a known legal duty.” Readers will recognize this as the Cheek standard.

Unfortunately, this Cheek standard, is not the one asserted by the government in FBAR willfulness cases. As I noted in a post just a few days ago regarding the Zwerner case (See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.)

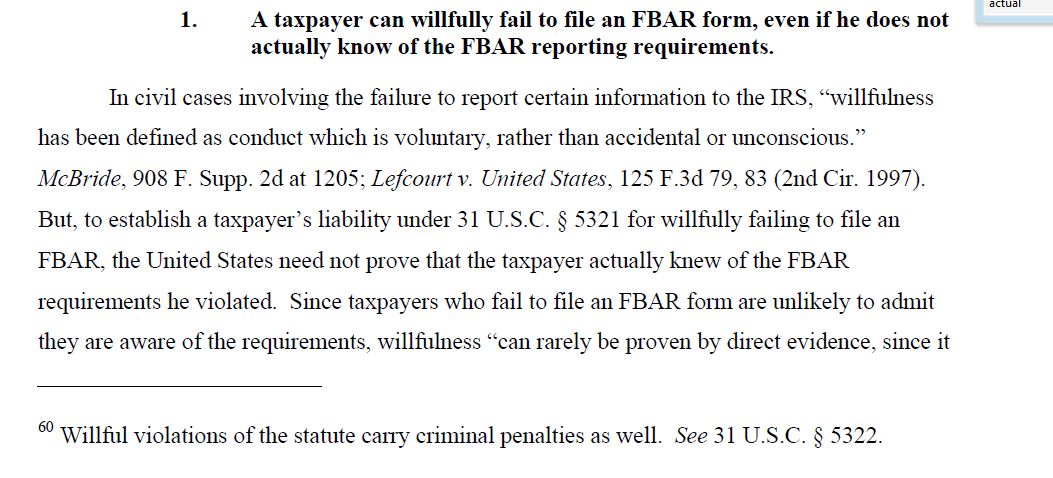

Finally, maybe the most troubling for USCs and LPRs who live outside the U.S., is the government’s assertion that an individual can be liable for the willfulness penalty, for “willfully failing to file a FBAR” – ” . . . even if the person does not actually know of the FBAR reporting requirements.” See, page 4 of the government’s motion for Summary Judgment in the Zwerner case. This is a position they have argued consistently in at least three different cases.

Why will the government not argue in those cases it selectively chooses to prosecute the following argument:

- Worldwide press about UBS, Credit-Suisse and other foreign accounts held by U.S. persons has made virtually all individuals generally aware of U.S. tax and reporting requirements.

- Any individual with a most basic level of sophistication must have known of these requirements, if they ever read a paper or the Internet (or should have known).

- FATCA news throughout the world since its passing into law in 2010, has been impossible to ignore.

- Ergo – Unless you have been living on a remote island or the rain forest, without access to the Internet, you can be liable for willful FBAR penalties, for the USC or LPR living overseas for their “willful blindness” – ” . . . even if the person does not actually know of the FBAR reporting requirements.”

Should such an argument prevail? Most private practitioners would say “no”; but the Zwerner case was illustrative of the strategies and approach taken by the government in a 150% FBAR penalty it obtained at a jury trial.