Month: November 2014

What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

A prior post identified the number of lawful permanent residents (LPRs) who file Form I-407 to formally abandon their lawful permanent residency. See, The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

These numbers of I-407 forms filed annually were obtained through a freedom of Information Act (“FOIA”) request and provided by the USCIS. See tabl:

Of course, this statistic does NOT identify the number of the approximate 13.3+ million LPRs who leave the U.S. to live elsewhere in another country without completing Form I-407 and formally abandoning. The estimated number of LPRs was 13.3 million for the year 2012 as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012.

Maybe the number of individuals who fall into this latter category (i.e., moving out of the U.S. without filing Form I-407) is several hundred of thousands of individuals annually?

Importantly, from a taxation perspective, anyone who moves and lives in a country with a U.S. income tax treaty (the list of these countries is set out below – from the IRS website), needs to be careful not to be deemed to be a “covered expatriate” due to the application of IRS Form 7701(b)(6). See, IRS Notice 2009-85.

See, the following posts with further explanation of the tax law for LPRs who move and live in one of the countries listed below. Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

See also, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Becoming a “covered expatriate” has U.S. tax consequences not just to the “former long-term LPR”, but also to their family and friends who are “U.S. persons” (as defined under Section 7701. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

A

Armenia

Australia

Austria

Azerbaijan

B

Bangladesh

Barbados

Belarus

Belgium

Bulgaria

C

Canada

China

Cyprus

Czech Republic

D

E

F

G

H

I

Iceland

India

Indonesia

Ireland

Israel

Italy

J

K

L

M

N

Netherlands

New Zealand

Norway

O

P

Pakistan

Philippines

Poland

Portugal

Q

R

S

Slovak Republic

Slovenia

South Africa

Spain

Sri Lanka

Sweden

Switzerland

T

Tajikistan

Thailand

Trinidad

Tunisia

Turkey

Turkmenistan

U

Ukraine

Union of Soviet Socialist Republics (USSR)

United Kingdom

United States Model

Uzbekistan

V

According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

The headlines read: “No Siree! Boris Johnson refuses to pay USA tax bill”

21 November, 2014 –

The following is a direct report from this article, and reflects the typical feeling and response of a dual national United States citizen who has spent virtually no time living in the United States, yet is required to pay taxes. This is largely a policy question and many have argued the law must change; see, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.-

Directly from article-

The prospective Conservative Parliamentary candidate, who was born in New York and holds a US passport, revealed his dispute with the US Treasury during an American radio phone-in while he was publicising his new book, The Churchill Factor. [See, Sir Winston Churchill – Famous People. Did he become a U.S. citizen at birth via “derivative citizenship”? Did he file U.S. income tax returns? – posted 1 April 2014]

His claims came after he was asked about renouncing his US citizenship, which the caller said was “very hard”, on National Public Radio.

Mr Johnson said: “I have to confess to you, that you’re right, it is a very – it is very hard, but I will say this, the great United States of America does have some pretty tough rules, you know.

“You may not believe this but if you’re an American citizen, America exercises this incredible doctrine of global taxation, so that even though tax rates in the UK are far higher and I’m Mayor of London, I pay all my tax in the UK and so I pay a much higher proportion of my income in tax than I would if I lived in America.

“The United States comes after me, would you believe it, for the – for capital gains tax on the sale of your first residence which is not taxable in Britain, but they’re trying to hit me with some bill, can you believe it?”

Presenter Susan Page then pressed him whether he would pay the bill, to which he said: “I think it’s outrageous.

“Well, I’m – no is the answer. Why should I? I haven’t lived in the United States for, you know, well, since I was five years old.

“I could but I pay – I pay the lion’s share of my tax, I pay my taxes to the full in the United Kingdom where I live and work.”

Part I: How the IRS “Non-Filer Program” Affects USCs and LPRs Residing Outside the U.S.

U.S. citizens who have spent most all of their lives outside the U.S. are often times shocked to learn about the scope of the U.S. citizenship based taxation system. In recent years, due to the aggressive pursuit of the IRS and Tax Division of the Department of Justice, there has become a keen focus on assets and accounts located outside the U.S.

Most recently in August of this year, the IRS has articulated its position for U.S. citizens and lawful permanent residents residing outside the U.S. in a document titled – “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers”

For a brief chronology of the actions taken by the IRS and DOJ and the U.S. Congress in the offshore world during the last few years see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

See, also IRS Audit Techniques – Expatriation, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The program is detailed in the Internal Revenue Manual, set out below. A follow-up post will discuss some uniquely complex issues affecting U.S. citizens and lawful permanent residents who reside outside the U.S.

- 4.19.17.1 Non-Filer Program

- 4.19.17.2 Non-Filer Strategy

- 4.19.17.3 Non-Filer Processing

- 4.19.17.4 Non-Filer Penalties

- 4.19.17.5 Undelivered Mail

- 4.19.17.6 Taxpayer Replies

- 4.19.17.7 Closures – Non Examined

NYT – More Federal Agencies Are Using Undercover Operations, Speficially Including the IRS

The Sunday morning front page New York Times article has an interesting summary of IRS agents (presumably special agents from the Criminal Investigation division) activities overseas:

More Federal Agencies Are Using Undercover Operations, by Eric Lichtblau and William Arkinnov (15 Nov. 2014)

. . . At the Internal Revenue Service, dozens of undercover agents chase suspected tax evaders worldwide, by posing as tax preparers, accountants, drug dealers or yacht buyers and more, court records show. . .

It’s possible now that the IRS and Justice Department were dealt big defeats in criminal tax prosecutions of non-resident individuals, it is less likely that the focus of these IRS efforts will be on non-resident U.S. citizens or lawful permanent residents who live throughout the world? See, Part II: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Re: Acquittals of Foreign Bank Employees

POSTED ON MARCH 2, 2014

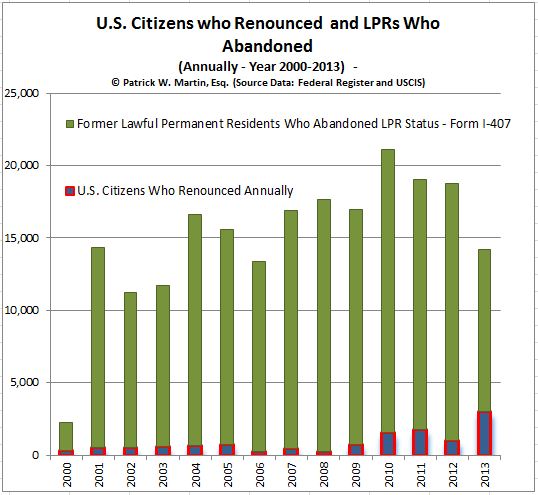

The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

The focus of Tax-Expatriation is to discuss legal matters of U.S. citizenship renunciation-relinquishment and lawful permanent residency abandonment.

There have been a great deal of resources discussing the number of USCs residing outside the U.S. and those who ultimately renounce citizenship.

See prior posts related to this topic –

The 2014 Third Quarter Renunciations Is probably the New Norm –

The List is Out – and Its 1,001 Former U.S. Citizens for the 1st Quarter 2014

There has not been any detailed discussion of the number of LPRs who leave the U.S. annually. The data provided by the U.S. Citizenship and Immigration Services reflects about 16 times more LPRs formally abandon their lawful permanent residency status by filing Form I-407 compared to U.S. citizens who renounce. The chart here shows a comparison for the years 2000 through 2013 of the total (i) USCs who have renounced compared to (ii) LPRs who have formally abandoned that status.

Note that for the year 2013, it is only through May 2013, so the total abandoned for the entire calendar year 2013 could well exceed 20,000.

Of course, this statistic does NOT identify the number of total current 13.3+ million LPRs who leave the U.S. to live elsewhere in another country without completing Form I-407 and formally abandoning. The estimated number of LPRs was 13.3 million for the year 2012 as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012

See also The Foreign-Born Population of the United States: Multi-National Families and “Tax Expatriation”

Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

· Myths – about Renouncing U.S. Citizenship

There are many misunderstandings of how the law works when someone renounces U.S. citizenship. The author regularly hears a range of myths that will befall an “Accidental American” when and if, they renounce. These “myths” include the following:

- Myth 1: There is a 10 year period of U.S. income taxation after renouncing citizenship.

- Fact: The old tax law from 1996 and the modifications in 2004 had a 10 year period of taxation concept after “expatriation.” There is no longer such a 10 year period of taxation for those persons who renounce on or after June 17, 2008.

- Myth 2: Former U.S. citizens will not be allowed to enter into the U.S.; i.e., will be barred from re-entry at a point of entry by a U.S. immigration officer.

- Fact: Former U.S. citizens are generally entitled to any visa status, the same as any other non-U.S. citizen. There is not a single case where a former U.S. citizen was barred re-entry to the U.S., due to tax motivated purposes.

- Myth 3 : Former U.S. citizens will not be allowed to ever re-obtain citizenship.

- Fact: Former U.S. citizens are generally entitled to U.S. citizen status, the same as any other non-U.S. citizen. Importantly, U.S. citizenship may simply not be available to any particular non-U.S. citizen, depending upon the particular circumstances.

- Myth 4: U.S. citizens do not need to renounce their U.S. citizenship if they live in a country with an income tax treaty with the U.S.; since the tie breaker rules of residency will keep them from being U.S. income tax residents.

- Fact: U.S. citizens cannot escape worldwide taxation, both income and gift/estate taxes, by living outside the U.S., since all U.S. bilateral income tax treaties and estate and gift tax treaties have a “savings clause” allowing the U.S. government to impose taxation on U.S. citizens notwithstanding the treaty.[1] This is how the U.S. tax net works on worldwide assets and income.

There are many more myths which will be discussed in a later post.

[1] See footnote no. 14 of Crow v. Commissioner, 85 T.C. 376 (1985):

14/ . . . The Treasury Department’s explanation of the Maltese treaty . . . :

“Paragraph (3) contains the traditional ‘saving clause’ under which each Contracting State reserves the right to tax its residents, as determined under Article 4 (Fiscal Residence), and its citizens as if the Treaty had not come into effect. [Department of Treasury, Technical Explanation of the Agreement Between the United States of America and the Republic of Malta with Respect to Taxes on Income 2 (Published in Treasury Department Press Release R 367 on Sept. 24, 1981), 1984-2 C.B. 366.]” This interpretation is consistent with the typical interpretations accompanying recent treaties containing general savings clauses.

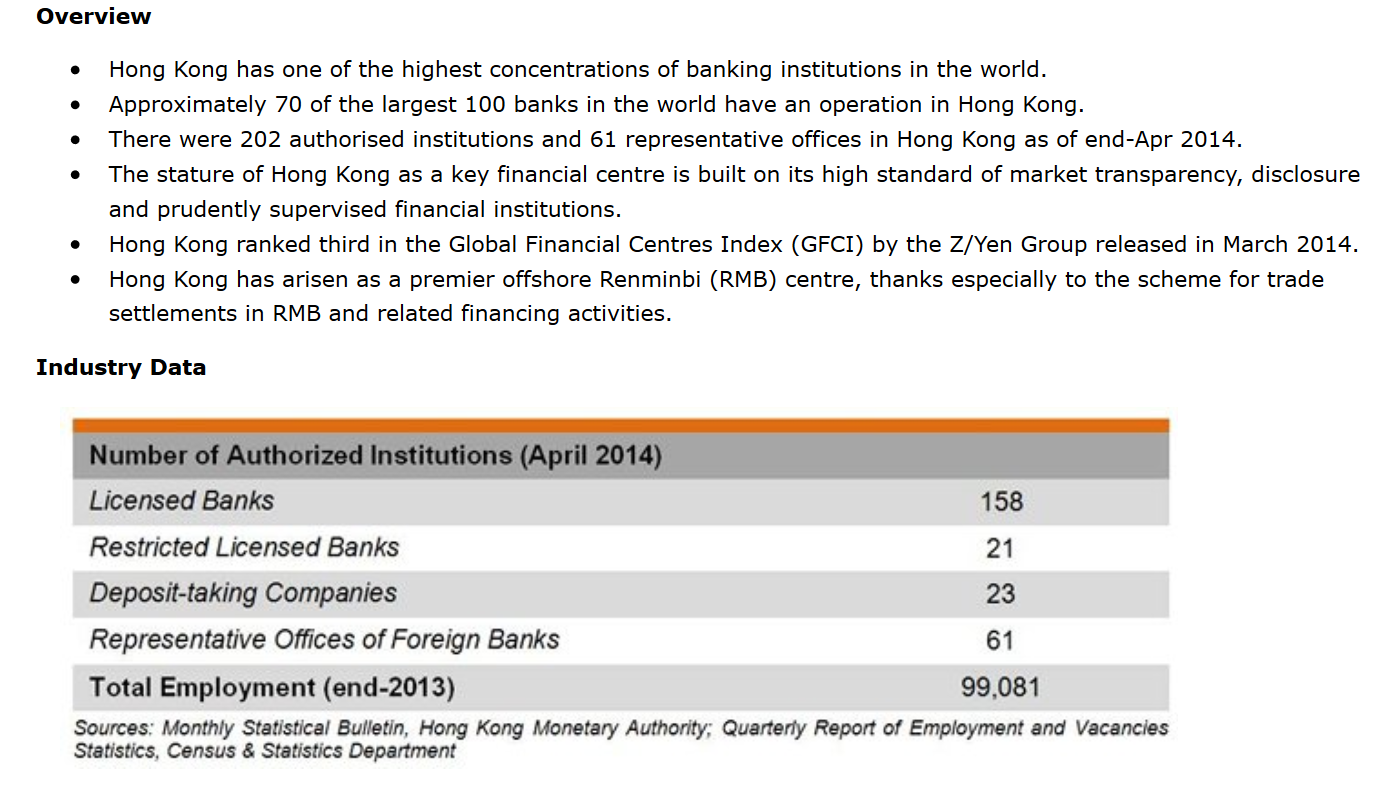

FATCA IGA with Hong Kong Signed: U.S. Citizens and Lawful Permanent Residents Residing in or Around Hong Kong Need to Know

Those USCs and LPRs who are living in Hong Kong or the Pacific Rim with accounts in the Hong Kong financial sector, need to be aware of the FATCA implications and the Intergovernmental Agreement (IGA) that was just signed.

The Hong Kong government’s press release with pictures can be viewed here. Of course, even those not resident in Asia with accounts, investments, financial instruments and other activities such as private equity funds, will be effected by this IGA.

The U.S. Treasury had announced in May 2014 that Hong Kong had previously ” . . . reached agreements in substance and have consented to being included on this list . . . “

The Government of the Hong Kong Special Administrative Region (HKSAR) publishes facts about the financial sector that can be reviewed here:

“Covered Expatriate” Status is a “Scarlet Letter”

Throughout Tax-Expatriation, I have tried to emphasize the importance of avoiding “covered expatriate” status, if at all possible – and at all costs. It is a technical term defined in the tax law.

“Covered Expatriate” status is a “Scarlet Letter”.

There is much misunderstanding about how the tax expatriation provisions of the law apply. Many people think they only apply to wealthy individuals. This is not the case.

See various posts explaining the importance of the Certification Requirement of Section 877(a)(2)(C):

Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)

Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

As explained throughout, there are many ways for individuals to fall into the “covered expatriate” category. I liken it here to the “Scarlet Letter”. The fictional protagonist in Nathaniel Hawthorne book, could never shed herself of the consequences of her infidelity and wore the Scarlet Letter for life. It had devastating consequences to her, her loved ones around her and especially her daughter.

This is also true for “covered expatriate” status; but it is not fictional. Covered expatriate status can never be shed and can have disastrous consequences not only for the former USC or LPR; but also to the friends and family of the individual who carries around the “covered expatriate” status for life. See, The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

In the book, the protagonist took the Scarlet Letter to her grave and had it on her tombstone. “Covered expatriate” status extends beyond the grave and beyond the tombstone. Any loved one who is a U.S. person of a “covered expatriate” who receives a gift or inheritance, will be subject to a tax; even if the inheritance occurs many years after the death of the covered expatriate. In this case, the Scarlet Letter transfers to the loved one who receives property in the future and continues on for another generation. At least in Nathaniel Hawthorne’s book, the daughter Pearl received an inheritance not tainted by the Scarlet Letter.

The “Phantom” Gain Exclusion from the “Mark to Market” Tax – Increases to US$690,000 for the Year 2015

This website Tax-Expatriation explains throughout its contents, various articles and posts about the general U.S. federal tax law and rules applicable to those individuals, who are –

- U.S. citizens who “renounce” or “relinquish” their U.S. citizen (“USC”), or

- Lawful permanent residents (“LPR”) who “abandon” that status (either intentionally or inadvertently by application of the law).

This website does not purport to provide legal advice and indeed cautions anyone from taking specific actions or steps based upon the explanation of  these very complex rules that are principally set forth in IRC Sections 877, 877A and 2801. See – limitations. The Table 1 in this post comes from my article that explains how the tax is calculated; which is itself out of date because (a) a change in the long-term capital gains rates, and (b) the inflation adjusted gain exclusion amount.

these very complex rules that are principally set forth in IRC Sections 877, 877A and 2801. See – limitations. The Table 1 in this post comes from my article that explains how the tax is calculated; which is itself out of date because (a) a change in the long-term capital gains rates, and (b) the inflation adjusted gain exclusion amount.

I have seen disastrous results for individuals who took steps without proper or good legal advice or counseling.

Enough of the “cautions” – “warnings” and “disclaimers.”

Today’s post simply explains that the amount of worldwide gain from the mark to market tax is indexed for inflation. When the law was initially adopted in 2008, the gain exclusion was US$600,000, but is one of the rare provisions in the Internal Revenue Code that is indexed for inflation.

The 2015 amount of gain exclusion will be US$690,000, which is increased from the 2014 amount of US$680,000. See, the IRS Revenue Procedure 2014-16, published this month that references those code sections which are indexed for inflation.

For an understanding of how this gain is determined and calculated, please see Table 1 in my article published in the International Tax Journal, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” , CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p52. Specifically, the example in the table set forth on page 52, which is reproduced here, should help provide a better understanding of how it is calculated.

That article used old long-term capital gains rates of 15%, which is no longer the law. It also used the original statutory exclusion from tax on the US$600,000 gain amount, which will increase to US$690,000 for the year 2015.

The Importance of Planning – PRIOR to Renouncing, Relinquishing or Abandoning

International tax law experts who specialize in a particular area of the law, have a fairly good understanding of the importance of tax planning. The reason is simple. The law is complex and without planning,  laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

“Tax expatriation” in the U.S. is particular complex for several reasons:

1. The general rule is that there is an immediate income tax payable from the “mark to market” taxation rules on unrealized gains. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

2. If a tax is recognized under the U.S. tax law, the only way to discharge the liability with the U.S. federal government is to pay the tax owing. The IRS generally can collect an income tax owing against a taxpayer who lives outside the U.S. indefinitely, as the 10 year collection statute does not apply when the individual outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). More on this topic in another post. In other words, the IRS can “forever” pursue the collection of the “expatriation tax” against USCs and LPRs living outside the U.S.

3. It is easy to fall into the general rule of expatriation, even if the taxpayer would not otherwise be subject to income taxation. See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

4. The friends and family of the “covered expatriate” – i.e., the former U.S. citizen and long-term lawful permanent resident can be subject to U.S. taxation during their lifetimes, even if they also live outside the U.S. See also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Each of these points help demonstrate the need for planning prior to running to the U.S. Department of State and completing and filing the following forms when you take the oath of renunciation:

See, Documents to Request the Consular Officer When Renouncing U.S. Citizenship

At the end of the day, if the individual lives outside the U.S. and does not travel to and from the U.S., it may be very difficult (at least practically speaking) for the IRS to collect on the tax judgment owing, if the individual has no assets in the U.S. There are legal means and steps the IRS can take in an attempt to try to collect U.S. taxes on overseas assets.

For a further discussion on collection of taxes overseas:

See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations, and

Ideally, a former U.S. citizen or long-term lawful permanent resident will wish to avoid all of the potential tax and collection issues, by engaging in thoughtful and strategic planning prior to their renunciation of U.S. citizenship or abandonment of lawful permanent residency.