WSJ (18 Feb. 2015): London Mayor Boris Johnson to Renounce U.S. Citizenship After Tussle With Uncle Sam

Ironically, the outspoken London Mayor has decided to renounce his U.S. citizenship, according to an article published by the Wall Street Journal.

See, WSJ: (18 Feb. 2015) – London Mayor Boris Johnson to Renounce U.S. Citizenship After Tussle With Uncle Sam

This article reported that his U.S. tax bill was at issue – :

In case you missed it: London Mayor Boris Johnson has said he will renounce his U.S. citizenship following a high-decibel tax squabble with his country of birth. At issue: a tax bill U.S. tax authorities claimed he owed on some London property. The mayor will (of course) keep his citizenship in the U.K. as his political ambitions continue to play out.

A previous post in November 2014 discussed a news report of the London Mayor and his U.S. citizenship and hence U.S. tax residency status. See, According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

Surely, he will be careful and thoughtful about the steps he is taking as part of his U.S. citizenship renunciation. His reported response to the news reporter last year could prove risky under U.S. law, to the extent he intentionally refuses to file U.S. income tax returns and pay taxes. The following line of questions and answers could be quite damning for him:

Presenter Susan Page then pressed him whether he would pay the bill, to which he said: “I think it’s outrageous.

“Well, I’m – no is the answer. Why should I? I haven’t lived in the United States for, you know, well, since I was five years old.

“I could but I pay – I pay the lion’s share of my tax, I pay my taxes to the full in the United Kingdom where I live and work.”

Here, the London Mayor has indicated he is not filing tax returns, yet knows he has a legal duty to file them and pay a tax owing under U.S. law. He goes further to say “I could . . . pay . . .” While rarely used standing alone by prosecutors (without other criminal claims brought), it is a crime that carries up to a 12 month prison sentence, to not file a U.S. return, supply information or pay tax; see, IRC § 7203. The relevant language of the statute is as follows:

Any person required under this title to pay any estimated tax or tax, or required by this title or by regulations made under authority thereof to make a return, keep any records, or supply any information, who willfully fails to pay such estimated tax or tax, make such return, keep such records, or supply such information, at the time or times required by law or regulations, shall, in addition to other penalties provided by law, be guilty of a misdemeanor and, upon conviction thereof, shall be fined not more than $25,000 ($100,000 in the case of a corporation), or imprisoned not more than 1 year, or both, together with the costs of prosecution.

Here, the government has yet another stick it can pull from its bag of sticks to be used against current and former U.S. citizens residing outside the U.S. It is of course, very common, that individuals who have spent most of their lives outside the U.S. have not filed any U.S. tax returns nor paid any U.S. income taxes. At what point, might these individuals have U.S. civil tax liability and what facts are necessary to give rise to criminal tax liability?

The vast majority of U.S. citizens residing overseas owe little to no U.S. income taxes because (i) modest income amounts and the impact of the “foreign earned income exclusion” or (ii) they reside in a country with higher taxes and tax rates than the U.S. because of the “foreign tax credit”. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

A couple observations about London Mayor Boris Johnson. First, he would be well advised not to make public statements about filing [or not] U.S. tax returns or paying [or not] U.S. taxes. Second, he will want to carefully consider completing and filing accurate U.S. tax returns as part of his formal renunciation process; particularly for the year in which he sold his London home tax free under UK laws. Third, he will want to understand carefully, the details of what is and should be filed on IRS Form 8854, after he has visited the U.S. embassy and files his Form DS-4080, Oath of Renunciation of the Nationality of the United States.

Finally, the case could present a unique international political and public relations nightmare for the U.S. Department of Justice, if they decided to bring any sort of criminal tax charges against the London Mayor. It would seem highly unlikely in my opinion.

The government has a strict requirement that prohibits a United States Attorney (e.g., the high profile Preet Bharara, U.S. Attorney for the Southern District of N.Y. Attorney ) from unilaterally bringing tax charges against individuals. See, 6-4.200, Tax Division Jurisdiction and Procedures, which provides in relevant part:

“. . . The Assistant Attorney General, Tax Division . . . must approve any and all criminal charges that a United States Attorney intends to bring against a defendant in connection with conduct arising under the internal revenue laws, regardless of which criminal statute(s) the United States Attorney proposes to use in charging the defendant. See 28 C.F.R. § 0.70.

Also, only the Tax Division can authorize warrants of public officials, which presumably would extend to London Mayor Boris Johnson. See, See, 6-4.130, Search Warrants.

On a related post, see, How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854? and Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C).

U.S. Tax and Expatriation Tax Laws – They Are What They Are . . .

The point of this post is a fairly simple one. The law is complex, it has evolved significantly over the years and continues to evolve; if for no other reason how the IRS enforces it. Some people might not like the law.

As those who have read and followed Tax-Expatriation.com know; it is not a place to seek legal advice. It provides lots of information – a comprehensive source of information. See, limitations. It also does not attempt to contemplate every scenario when a particular point is made; e.g., as the IRS modifies how they interpret rules or how they enforce them.

For instance, for a fairly comprehensive article about how the law works, see Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6. The net worth threshold (US$2M) and income tax thresholds (US$124,000, indexed for inflation) are spelled out in that article. It does not have the indexed inflation amounts. See, The “Average Annual Net Income Tax” Amounts for “Covered Expatriate Status” – Increases to US$160,000 for the Year 2015

Every individual who renounces their U.S. citizenship is taking, in what is my view, a very important decision. Many individuals do not like U.S. tax laws; nor the expatriation tax laws. Many individuals around the world do not like their home country tax laws; nor other laws.

This blog is not intended to be a policy blog debating whether the U.S. tax laws are good laws or bad laws. It’s designed to provide information about the law and important developments and relevant information.

Finally, the “blogosphere” is full of people who attempt to write about the law as if they understand it; particularly the complexity of Title 26, the regulations and a host of case law that spans almost 100 years. These opinions are a dime a dozen. Many get it terribly wrong – particularly in this politically charged topic – and will make statements and provide information that sounds attractive to the uninformed. The following is the type of decision that is made every day.

Path 1: If someone tells USC, Mr. X (or if he reads) the following, he might find it quite attractive: “You will have no U.S. tax liabilities if you simply do “steps Y and Z.” Plus, the U.S. federal government will never know and/or they will never be able to collect the taxes from you anyhow. Simple. Would you rather pay $0 or a bunch of money to the U.S. federal government?”

Path 2: On the other hand, if a qualified legal adviser accurately advises USC, Mr. X of the following, he may not find the answer so attractive: “Sorry, given your factual circumstances, you will have US$ 100,00X of immediate income tax liabilities if you simply do steps “Y and Z.” Plus, by doing so, if you ever bequeath or gift your U.S. citizen children, they will have to pay 40% (under current law) of the value of such inheritance or gift in U.S. taxes. This latter tax obligation will not be your obligation, but rather your U.S. citizen children.”

Not surprisingly, Mr. X may well want to take Path 1, because it is the answer he prefers. If Mr. X does steps “Y and Z”, he will now live with the U.S. legal consequences. He well might not like those legal consequences and think they are unfair, unjust or borderline immoral for any government to impose, but that is how laws often work.

U.S. Tax and Expatriation Tax Laws – They Are What They Are . . .

The President’s Proposal is NOT the Same as Current Law – Section 877A(g)(1)(B)

Some individuals are mistaken that the Obama proposal to exempt certain U.S. citizens from taxation (including the “mark to market” exit tax), is the same as the exception in IRC Section 877A(g)(1)(B).

It’s not. They are not the same, although they have some similar requirements (e.g., 5 years of certification of U.S. tax law compliance under penalty of perjury).

For a brief discussion on the President’s proposal, see –The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group

–

There are important differences. Most importantly, the I

RC Section 877A(g)(1)(B) exception requires the individual not only have been a dual citizen (of at least two or more countries) at birth, along with U.S. citizenship; but also continue to reside and be a tax resident of that country, i.e., the country of which they were also a citizen at the time of their birth. This tax residency/dual citizenship rule is necessarily required by I

RC Section 877A(g)(1)(B). If the person has moved to another country, they will not be eligible for this treatment and will be subject to the mark to market “exit tax” if they renounce their U.S. citizenship. Their U.S. heirs and beneficiaries will also be subject to the 40% (current tax rate) tax on “covered gifts” and “covered bequests.”

–

The President’s proposal (if it ever becomes law) will also apparently exempt all qualifying individuals from any type of U.S. taxation; other than tax that would apply to a “non-resident alien” (which would be no U.S. tax – if the individual had no U.S. source income). Not only would no “exit tax” apply, but so too would no U.S. income tax on their income from their country of residence or any other country outside the U.S. The President’s proposal would also exempt them from all U.S. tax filing requirements (other than the 5 years) and from FBAR filing requirements. See,

Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.–

–

The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group

A prior post explained the green book proposal published earlier in February: Obama Budget Proposal to “Provide Relief for Accidental Americans”? Will the Proposal to Modify the Expatriation Rules Become Law?

The unique consequence of such a proposal, would be to eliminate U.S. citizenship based taxation for a very small, select group of U.S. citizens. See, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

a very small, select group of U.S. citizens. See, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

The group affected would indeed be very small. Most importantly, the requirements that would limit the number of eligible persons to a very small class of individuals are the following:

- [those who] have never held a U.S. passport or . . . held a U.S. passport for the sole purpose of departing from the United States in compliance with 22 CFR §53.1,

- [those who] relinquish . . . his or her U.S. citizenship within two years after the later of January 1, 2016, or the date on which the individual learns that he or she is a U.S. citizen.

The immigration law regulations 22 CFR § 53.1 require that a U.S. citizen have a U.S. passport to enter or depart the United States. The relevant part of the regulations is § 53.1(a) which provides as follows:

Passport requirement; definitions.

(a) It is unlawful for a citizen of the United States, unless excepted under 22 CFR 53.2, to enter or depart, or attempt to enter or depart, the United States, without a valid U.S. passport.

*

These regulations were

first published in 2006, and rely in part on a Presidential Executive Order made by President Bush (Jr.).

*

*

Assuming an individual was aware of such regulatory rule, they could not qualify for this proposed exception, if they ever lived in the U.S. since becoming 18 1/2 years old. This means that only those individuals with U.S. passports who (i) obtained a U.S. passport as a child (presumably through their parents) while (ii) living in the U.S. and (iii) did so in order to comply with this regulation 22 CFR § 53.1 would be eligible. Since the regulations were just passed in 2006, anyone who obtained a U.S. passport, for instance in 2002 (even if they never lived in the U.S.) would presumably be disqualified from this tax treatment.

Also, if they did not get a passport when they were in the U.S., leaving the country after the 2006 passport regulations were adopted, would have been a violation of the law.

Bottom line, it seems nearly impossible that anyone who ever had a U.S. passport would ever qualify for this exception.

*

Further, the two year rule, would seem to exclude most all other foreign resident USCs (of course, virtually none of whom could ever have had a U.S. passport). Once an individual becomes aware they are a U.S. citizen (even if they are unaware of any U.S. tax or bank reporting requirements), the two year window starts ticking. If they do not renounce their U.S. citizenship within that time frame, they too would also not qualify for such an exception.

*

Finally, it is worth noting that it often takes several months to get an appointment with the U.S. Consulate or Embassy to even renounce in the first place.

*

Therefore, in conclusion, even if the Obama proposal were to make its way into the law, those who could actually obtain relief would be a rare group of individuals. In short, U.S. citizenship based taxation on worldwide income, will continue to be the law of the land.

Part II: U.S. Department of State Communications to USCs overseas Regarding Tax Obligations with IRS

A recent post discussed a rather surprising development of how the – U.S. Department of State, Starts Communicating with U.S. Citizens Overseas Regarding Tax Obligations with the IRS

There are several observations to be made about this approach.

First, some USCs living overseas will find this a welcome development, as it provides a method of  basic education of how U.S. tax laws work. The newer U.S. passports do have an obscure reference to U.S. tax obligations of USCs. In the past, there was generally no communications from the U.S. Department of State to USCs, including newly naturalized U.S. citizens about their U.S. tax obligations.

basic education of how U.S. tax laws work. The newer U.S. passports do have an obscure reference to U.S. tax obligations of USCs. In the past, there was generally no communications from the U.S. Department of State to USCs, including newly naturalized U.S. citizens about their U.S. tax obligations.

Second, there is much helpful information provided in the U.S. Department of State’s explanation. The key tax forms that are most relevant for USCs and LPRs residing overseas are explained in the government e-mail. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

All of the following forms are identified by the U.S. Department of State:

- Substantive Income Tax Forms (Affecting Tax Liability)

- Information Tax Forms (Not Affecting Tax Liability, but with Substantial Penalties for Failure to File)

These are the most relevant forms for the majority of USCs and LPRs; although there are numerous other forms and calculations that may be required depending upon the particular circumstances, income, assets, employment, etc. for each individual

The third observation, relates to how employees of the U.S. Department of State will use this information and communicate with USCs? Will they begin asking (even if infrequently) whether a U.S. citizen overseas is in compliance with their U.S. federal tax requirements? What are the consequences to the U.S. citizen if they state yes, no or refuse to answer? What can happen to an individual if they provide a false statement to a federal employee or file a false document? See What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The fourth and last observation, is whether the IRS will begin providing USC taxpayer information on a regular basis to the U.S. Department of State? The law provides limitations upon how the IRS can disclose and provide taxpayer information. See, 26 U.S. Code § 6103 – Confidentiality and disclosure of returns and return information

However, there are significant exceptions in the law, that do allow disclosure of taxpayer financial and taxpayer information to other agencies (particularly “Intelligence Agencies,” which presumably includes the U.S. Department of State). See, for instance, IRC Section 6103(i)(7). The statutory requirements of 6103(i)(7) are not particularly rigid.

Obama Budget Proposal to “Provide Relief for Accidental Americans”? Will the Proposal to Modify the Expatriation Rules Become Law?

[See follow-on post: The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group– published 18 Feb. 2015]

Every year, the President of the United States, releases his proposed budget. The budget is prepared by his team of advisers at the Treasury Department and is known as the “green book“.

For a complete copy of the proposal, that was released on February 2, 2015, see, General Explanations of the Administration’s Fiscal Year 2016 Revenue Proposals (Released February 2015)

Buried deep into the proposal of the US$3.99 trillion fiscal year 2016 expenditure plan, is a provision to “provide relief for certain accidental dual citizens.” See pages 282 and 283 of the proposal.

It appears someone is listening in the Administration at Treasury; at least a little bit? Will Congress similarly be interested in such proposals? See, Will Congress Intervene to make USC based Tax Laws More User Friendly to USCs and LPRs Residing Outside the U.S.?

The proposal would not adopt residency based taxation for all U.S. citizens, as exists in the rest of the world, but would exclude certain U.S. citizens from the “mark to market” tax on expatriation (i.e., the “exit tax”). See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

Those excluded from the exit tax and the tax to their U.S. heirs or beneficiaries who receive gifts or inheritances (See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”) are those individuals who:

- became at birth a citizen of the United States and a citizen of another country,

- at all times, up to and including the individual’s expatriation date, has been a citizen of a country other than the United States,

- has not been a resident of the United States (as defined in section 7701(b)) since attaining age 18½,

- has never held a U.S. passport or has held a U.S. passport for the sole purpose of departing from the United States in compliance with 22 CFR §53.1,

- relinquishes his or her U.S. citizenship within two years after the later of January 1, 2016, or the date on which the individual learns that he or she is a U.S. citizen, and

- certifies under penalty of perjury his or her compliance with all U.S. Federal tax obligations that would have applied during the five years preceding the year of expatriation if the individual had been a nonresident alien during that period.

This would be a significant change from current law. However, the no passport requirement will narrow significantly the number of individuals who may be eligible for this relief; if it becomes law?

Most interesting about the proposal, is that it seems to say these U.S. citizen individuals (who meet all 6 criteria) will not be subject to any U.S. tax as a U.S. citizen. In other words, it seems to say they will be taxed the same as a non-resident alien, which in effect is residency based income taxation for this narrow class of U.S. citizens. The word tax is used generically, to presumably also exclude them from U.S. estate, gift and generation skipping transfer taxes.

The proposal has a window of opportunity that starts to close with time and then shuts in January 1, 2018; i.e., the 2 year period after January 1, 2016. This will mean that those future “Accidental Dual Citizens/Americans” who later learn of their U.S. citizenship, will only have 2 years from the moment they became aware of their U.S. citizenship status. One thing is to know you are a U.S. citizen as you live wherever you may around the world; another is to know and understand the U.S. taxes that are imposed upon you on your worldwide assets.

Laura Saunders of the WSJ: “Record Number Gave Up U.S. Citizenship or Long-Term Residency in 2014”

Ms. Saunders writes thoughtfully on the subject of taxation and U.S. citizens who have renounced citizenship.

*

Her most recent article has a number of excellent observations, including the following regarding an academic study of those citizens living abroad:

According to a recent survey of 1,546 U.S. citizens and former citizens living abroad, 31% of participants have actively considered renouncing their U.S. citizenship and 3% are in the process of doing so. Many who were considering the move cited increasingly onerous and intrusive financial reporting requirements. The survey was conducted between Dec. 5 and Jan. 20 by Amanda Klekowski von Koppenfels, a researcher at the University of Kent in the U.K.

For other articles written by Ms. Laura Saunders, on this related subject, see the Media: News & Articles section –

Wall Street Journal: Expats Left Frustrated as Banks Cut Services Abroad Americans Overseas Struggle With Implications of Crackdown on Money Laundering and Tax Evasion, (The Wall Street Journal, 11 Sept 2014) By –Laura Saunders

IRS Eases Up on Accidental Tax Cheats: Agency Lowers Some Offshore-Account Penalties, Raises Others (The Wall Street Journal, June 18, 2014), By – Liam Pleven and Laura Saunders

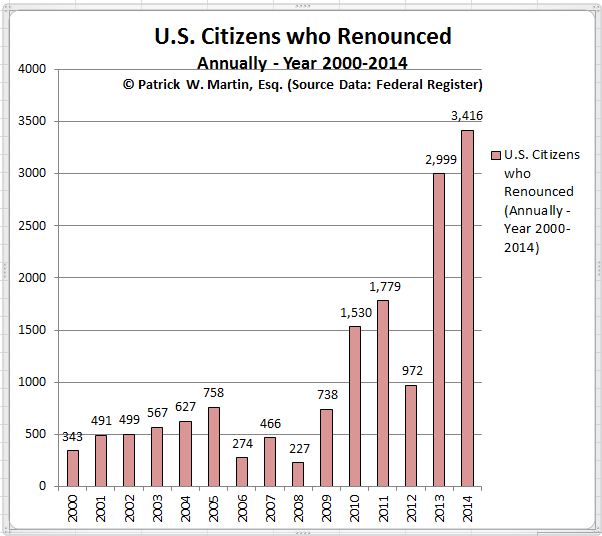

New Record of U.S. Citizens Renouncing – The New Normal

The U.S. Treasury released the names of those who renounced U.S. citizenship for the 4th Quarter of 2014. The year 2014 again saw a record number of U.S. citizens who renounced.

See, Qtr 2 Numbers (2014) and Names of Former U.S. Citizens are Announced – 576 Who Renounced

The names of each citizen can be located in the list published in the Federal Register.

I have updated my diagram to reflect the numbers to date, through the end of 2014, which were recently released.

There are a number of key considerations and strategic decisions that most all U.S. citizens need to consider prior to renouncing citizenship. See, for instance –

Can the U.S. Federal Government Bar Entry into the U.S. to a U.S. Citizen without a U.S. Passport?

Global Entry, SENTRI and NEXUS after Renouncing – the “Trusted Traveler Programs” – SAFE TRAVELS!

U.S. Department of State, Starts Communicating with U.S. Citizens Overseas Regarding Tax Obligations with the IRS

The IRS is in charge of U.S. federal tax administration. It’s mission statement is set out below and is very different from the mission of the U.S. Department of State:

The IRS Mission

Provide America’s taxpayers top quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

This mission statement describes our role and the public’s expectation about how we should perform that role.

- In the United States, the Congress passes tax laws and requires taxpayers to comply.

- The taxpayer’s role is to understand and meet his or her tax obligations.

- The IRS role is to help the large majority of compliant taxpayers with the tax law, while ensuring that the minority who are unwilling to comply pay their fair share.

The U.S. Department of State is in charge of something very different from taxes and tax policy. Below is its Mission Statement –

Department Mission Statement

The Department’s mission is to shape and sustain a peaceful, prosperous, just, and democratic world and foster conditions for stability and progress for the benefit of the American people and people everywhere. This mission is shared with the USAID, ensuring we have a common path forward in partnership as we invest in the shared security and prosperity that will ultimately better prepare us for the challenges of tomorrow.

–From the FY 2014 Agency Financial Report,

released November 2014

In my career of more than 25 years as a tax professional, working in the international tax area, I have never before seen communications sent by the U.S. Department of State, directly discussing U.S. federal tax obligations.

However, there have been many changes in the last few years in how aggressive the IRS (and Tax Division, Department of Justice) has become in enforcing U.S. tax laws overseas. See, Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

This seems to be part of a bigger trend of the IRS to use other governmental agencies and their resources in identifying and locating U.S. taxpayers and their assets overseas.

One recent development is the communication sent by the U.S. Department of State via e-mail to U.S. citizens residing overseas. The following is the complete text of the tax compliance communication sent by the U.S. Department of State, which ends with a reference: “I Haven’t Filed All My Tax Returns, What Can I Do?.” It then references the IRS offshore programs (which includes the OVDP, which in my view, should be reserved for only those U.S. taxpayers who have criminal tax liability – see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior):

Dear U.S. citizens,

The Internal Revenue Service (IRS) has provided the following guidance for U.S. citizens abroad preparing for the 2015 tax filing season. This IRS guidance is posted under Federal Benefits and Obligations on travel.state.gov. U.S. embassies and consulates cannot mail tax returns on behalf of U.S. taxpayers living abroad.

1. Who Must File?

All U.S. citizens and resident aliens must file a U.S. individual income tax return, even if they permanently live outside the United States and may not owe any tax because of income exclusion or tax credit.

2. When is the 2014 Federal Tax Return Due?

Due date for Form 1040: April 15, 2015

Extensions:

- An automatic extension to June 15, 2015, is granted for taxpayers living outside the United States and Puerto Rico. No form is required; write “Taxpayer Resident Abroad” at the top of your tax return.

- Caution: This extension applies only for filing your tax return, not for payment. If you owe any taxes, you’re required to pay by April 15, 2015. Interest and penalties will generally be applied if payment is made after this date.

- To request an additional extension to October 15, 2015, use Form 4868.

- Caution: This extension applies only for filing your tax return, not for payment. If you owe any taxes, you’re required to pay by April 15, 2015. Interest and penalties will generally be applied if payment make after this date.

- Other extensions may be available on IRS.gov.

3. Can I Mail My Return and Payment?

You can mail your tax return and payment using the postal service or approved private delivery services. A list of approved delivery services is available on IRS.gov. If you mail a return from outside the United States, the date of filing is the postmark date. However, if you mail a payment, separately or with your return, your payment is not considered received until the date of actual receipt.

4. Can I Electronically File My Return?

You can prepare and e-file your income tax return, in many cases for free. Participating software companies make their products available through the IRS. E-File options are listed on IRS.gov.

5. What Forms May I Need?

- 1040, U.S Individual Income Tax Return

- Instructions to Form 1040

- 1116, Foreign Tax Credit

- 2013 Instructions to Form 1116 – 2014 instructions will be available soon, please check on http://www.irs.gov

- 2350, Application for Extension of Time to File U.S. Income Tax Return (for U.S. citizens and residents abroad)

- 2350 in Spanish

- 2555, Foreign Earned Income Exclusion

- Instructions to Form 2555

- 2555-EZ, Foreign Earned Income Exclusion

- Instructions to Form 2555-EZ

- 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return

- 4868 in Spanish

- 8802, Application for United States Residency Certificate

- Instructions to Form 8802

- 8938, Statement of Specified Foreign Financial Assets

- Instructions to Form 8938

- 14653, Certification by U.S. Person Residing Outside of the United States for Streamlined Foreign Offshore Procedures

6. How Do I Pay My Taxes?

You must pay your taxes in U.S. dollars.

- Direct pay. You can pay online with a direct transfer from your U.S. bank account using Direct Pay, the Electronic Federal Tax Payment System, or by a U.S. debit or credit card. You can also pay by phone using the Electronic Federal Tax Payment System or by a U.S. debit or credit card.

- Foreign wire transfers. If you have a U.S. bank account, you can use the Electronic Federal Tax Payment System. If you do not have a U.S. bank account, ask whether your financial institution has a U.S. affiliate that can help you make same-day wire transfers.

- Foreign electronic payments. International taxpayers who do not have a U.S. bank account may transfer funds from their foreign bank account directly to the IRS for payment of their tax liabilities.

7. Other Reporting?

You also may have to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR), by June 30, 2015.

8. Does the IRS Provide Help in Other Languages?

The IRS provides tax information in Chinese, Korean, Russian, Spanish, and Vietnamese. Go to http://www.irs.gov and use the drop down box under “Languages” on the upper right corner to select your language.

9. Where Can I Get Help?

Contact the International Taxpayer Service Call Center by phone or fax. The International Call Center is open Monday through Friday, from 6:00 a.m. to 11:00 p.m. (Eastern Time).

Tel: 267-941-1000 (not toll-free)

Fax: 267-941-1055

You may also contact the IRS office in London, Paris, or Frankfurt. For addresses and telephone numbers, contact my local office internationally.

10. I Received a Notice from the IRS, What Do I Do?

If you receive a notice from the IRS and need to contact the IRS, call the number listed on the notice or the International Taxpayer Service Call Center (see above).

11. Where Can I Get More Information?

For information on the IRS website about international taxpayers, see this page.

For general information about international taxpayers, see Publication 54, “Taxation of U.S. Citizens and Residents Abroad.”

For information on the Affordable Care Act and taxpayers outside the United States, see Publication 5187, “Health Care Law.”

12. I Haven’t Filed All My Tax Returns, What Can I Do?

If you have not filed all the returns required of you and want to catch up on your filing obligations, see this announcement: IRS makes changes to offshore-programs.

Where the IRS will Likely Look in Latin America: Country Specific Tax Returns filed by U.S. Individual Taxpayers – Latin America (Excluding Mexico)

The prior post asked the “question”: Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand [?]

As a continuation of the prior post, some further analysis by geographical region is provided here. This post is focused on Latin American countries  where U.S. citizens, lawful permanent residents (“LPRs”) or other individuals who may be U.S. tax residents (e.g., those individuals who make an election to be treated as a “U.S. person” for federal income tax purposes) are or are not filing U.S. tax returns. For an important discussion of LPRs, see, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

where U.S. citizens, lawful permanent residents (“LPRs”) or other individuals who may be U.S. tax residents (e.g., those individuals who make an election to be treated as a “U.S. person” for federal income tax purposes) are or are not filing U.S. tax returns. For an important discussion of LPRs, see, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

The IRS provides detailed statistical information on tax returns filed; how many, and in various groupings and from various locations. One such grouping by the IRS office of statistics, is by those individuals who filed tax returns which contained the “foreign earned income exclusion” which is reported on Form 2555: Foreign-Earned Income Exclusion, Housing Exclusion, and Housing Deduction.

See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is File

The IRS reports that less than 15,000 tax returns were filed from all of of Latin/South America (excluding Mexico); for the year 2011, the last year they reported these statistics reflecting the foreign earned income exclusion. One of the more surprising statistics is that according to the U.S. Department of State, some 120,000 U.S. citizens reside in Costa Rica alone, yet only about 2,100 U.S. income tax returns were filed from Costa Rica with the foreign earned income exclusion.

Indeed, according to the U.S. federal government’s own numbers, there are approximately more than 8 times the number of U.S. citizens, simply living in Costa Rica (approx. 120,000) compared to the total number of U.S. tax returns (14,732) filed from all of the Latin/South American countries (excluding Mexico) that had the foreign earned income exclusion.

Similarly, Panama according to the U.S. Department of State, has ” . . . About 25,000 American citizens reside in Panama, many retirees from the Panama Canal Commission and individuals who hold dual nationality. There is also a rapidly growing enclave of American retirees in the Chiriqui Province in western Panama.” However, only about 1,200 U.S. income tax returns were filed from Panama with the foreign earned income exclusion.

Each Latin/South America country from which the number of U.S. tax returns were filed in 2011, with the foreign earned income exclusion is set out below:

| Latin/South America, total |

14,732 |

| Argentina |

986 |

| Brazil |

3,351 |

| Chile |

1,383 |

| Colombia |

1,524 |

| Costa Rica |

2,147 |

| Panama |

1,187 |

| Peru |

1,098 |

| Venezuela |

778 |

| Other Latin and South American countries |

2,280 |

This analysis is surely the type of analysis being conducted by the IRS which will be supplemented with information as they start receiving financial account and income information from countries and their financial institutions around the world (not just Latin America) from FATCA and the IGAs. See, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

Three key observations about the above analysis.

First, there are many U.S. citizens residing overseas who have (a) income below certain thresholds, (b) are simply retired or unemployed – and have no foreign earned income, and/or (c) are not aware of how they can benefit from the foreign income exclusions; and therefore are not filing U.S. tax returns with the foreign earned income exclusion. However, the disproportionate number of U.S. citizens living throughout Latin America compared with the tax returns that are filed in this category is a strong indicator of low compliance by these taxpayers. The IRS will surely take note of this key consideration.

Second, the above numbers do not try to identify the number of LPRs who are residing in these Latin American countries who are also not filing U.S. income tax returns. There are some 13-14 million LPRs. See, What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

Third, Latin America has the largest percentage of the population throughout the world where more U.S. citizens reside. See, a 2012 proposal I prepared for the State Bar of California, Taxation Section: Proposed Expansion of Category of Registered Deemed-Compliant FFI: “The Good Faith Local FFI” and the Accidental American along with Liliana Menzie that describes the high concentration of U.S. citizens throughout the region. “Latin America, as a prime example, has a high concentration of U.S. citizens residing in various countries pursuant to the State Department data, in some cases representing a large percentage of the population (e.g., nearly one half of a percent -0.4%- of the total population of the Americas consisted of U.S. citizen[s] . . .”