Month: October 2018

Legal Question of the Day: FBAR Penalties for USCs and LPRs Residing Outside the U.S. Is the IRS Website correct as a matter of law?

The IRS website has a specific statement on their website titled Delinquent FBAR Submission Procedures

Importantly, the website provides the following comforting statement:

The IRS will not impose a penalty for the failure to file the delinquent FBARs if you properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs, and you have not previously been contacted regarding an income tax examination or a request for delinquent returns for the years for which the delinquent FBARs are submitted.

The question is the following:

Is the IRS bound by their own statement on their website as a matter of law?

In other words, can they go ahead and assess FBAR penalties notwithstanding the statement set forth above on their website?

USCs are necessarily subject to U.S. taxation on their worldwide income because they are defined as “United States persons” under title 26, Section 7701(a)(30)(A). See, The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for  Persons Living Outside the U.S. ***Does it still make sense?

Persons Living Outside the U.S. ***Does it still make sense?

Lawful permanent residents (“LPRs”) may, but are not necessarily defined as “United States persons” under title 26, Section 7701(a)(30)(A) by application of an applicable tax treaty and the flush language of Section 7701(b)(6). See, Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card and see the IRS practice unit discussion, Determining Tax Residency Status of Lawful Permanent … – IRS.gov

Now, this is all relevant to know and understand, in order to determine who exactly has a filing obligation under Title 31: regarding FBARs. See, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

Assuming you do have an FBAR filing requirement, e.g., residing in your country of residence with financial accounts in your  own country or in other financial institutions outside the U.S.; can the IRS assess a penalty against you for a delinquently filed FBAR? What if you have properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs?

own country or in other financial institutions outside the U.S.; can the IRS assess a penalty against you for a delinquently filed FBAR? What if you have properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs?

The answer may surprise you. It will be addressed in a subsequent post.

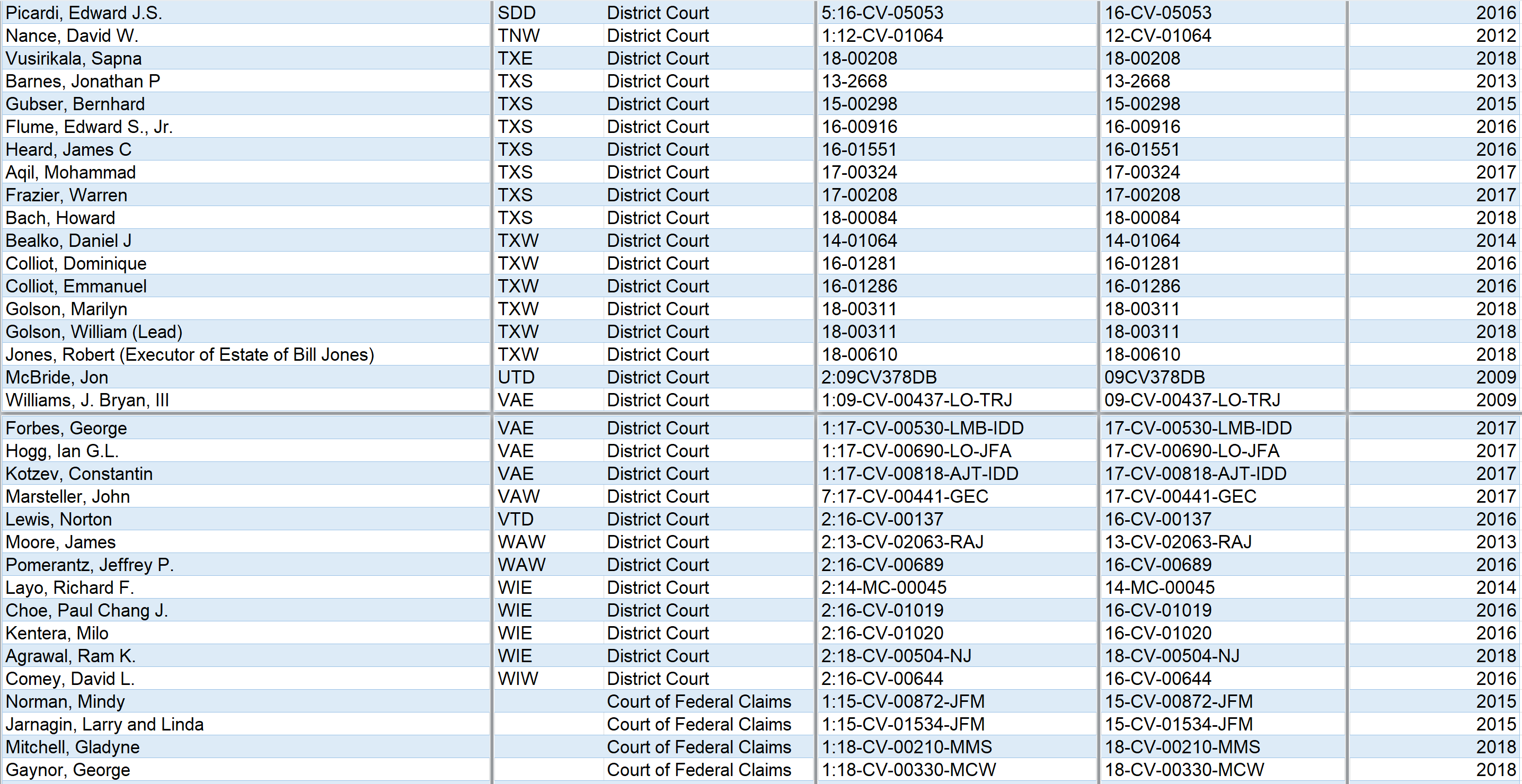

Incidentally, to date, there have been more than 200 FBAR civil penalty cases filed in U.S. federal courts. The Federal District Courts have seen approximately 200+ civil penalty cases and the Court of Federal Claims, much less popular venue, has seen 5 cases thus far.

Additional Time for Tax Return Filing – Extension until December 15th for USCs Residing Overseas: “Avoiding the Acceleration of the ‘Repatriation’ Tax”

A prior post explained how a USC can avoid the acceleration of the 965 Repatriation tax for a USC residing outside the U.S., by timely filing an extension. See, the following comment regarding the relief granted by the IRS –

- a timely election under Section 965(h)(1) needs to have been made, which is typically extends the return due date until October 15, 2018 (USCs residing outside the U.S., the extension due date was June 15th, 2018 and requires the filing of a specific automatic extension form (IRS Form 4868) by that date); and . . .

Also, the IRS provides in its Questions and Answers to Reporting Related to Section 965 – Q16 in relevant part as follows:

. . . the IRS has determined that, if an individual’s net tax liability under section 965  in the individual’s 2017 taxable year is less than $1 million, the individual makes a timely election under section 965(h), and the individual did not pay the full amount of the first installment by the due date under section 965(h)(2), the failure to make the payment will not result in an acceleration event under section 965(h)(3) so long as the individual pays the full amount of the first installment (and its second installment) by the due date for its 2018 return (determined without regard to extensions).

in the individual’s 2017 taxable year is less than $1 million, the individual makes a timely election under section 965(h), and the individual did not pay the full amount of the first installment by the due date under section 965(h)(2), the failure to make the payment will not result in an acceleration event under section 965(h)(3) so long as the individual pays the full amount of the first installment (and its second installment) by the due date for its 2018 return (determined without regard to extensions).

The only way to make a timely election, is to do so prior to the due date of the tax return. For USCs residing outside the U.S. (who already properly filed an extension by June 15th, 2018 with IRS Form 4868, the due date of the election and return filing is days away – due October 15, 2018.

There is a way to further extend the due date from October 15th for USCs residing overseas until December 15th.

Treas. Reg. Section 1.6081-1(b)(1) allows USCs residing overseas to request an additional extension until December 15th, provided

. . . A taxpayer desiring an extension of the time for filing a return, statement, or other document shall submit an application for extension on or before the due date of such return . . . ; however, taxpayers may apply for an extension in a letter that includes the information required by this paragraph. . . . the taxpayer should make the application for extension to the Internal Revenue Service office where such return . . . is required to be filed . . . the application must be in writing, signed by the taxpayer or his duly authorized agent, and must clearly set forth—

1.6081-1(b)(1)(i) – The particular tax return, information return, statement, or other document, including the taxable year or period thereof, for which the taxpayer requests an extension; and

1.6081-1(b)(1)(ii) – An explanation of the reasons for requesting the extension to aid the internal revenue officer in determining whether to grant the request.

A sample letter requesting an additional extension might look like this – with the foreign address of the USC reflected on the top of the letter:

Taxpayer 1 (USC) & Taxpayer 2 (USC)

No. 807 Address Foreign Street

Foreign City, Foreign Country, Codigo 87903-187

October 3, 2018

Department of the Treasury

Internal Revenue Service Center

Austin, TX 73301-0215

VIA CERTIFIED MAIL

Re: Additional Extension of Time to File IRS Form 1040: Taxpayer 1 (USC – SSN ***-**-7497) & Taxpayer 2 (USC SSN ***-**-4916)

Dear Sir or Madam:

We previously filed Form 4868 to extend our 2017 personal tax return. We live overseas outside of the good old US of A. Pursuant to Treas. Reg. §1.6081-1 (b), we are requesting an additional 2 months extension so that we can accurately file complete and accurate returns.

We are shareholders of certain foreign companies (in our country of residence, and the records are kept in Foreign Country and are in foreign currency and in Foreign Language. Additional time is required for the complex international information recording requirements on our tax returns, including IRS Forms 8865 and 8938 (which we know you would like to assess us penalties of US$10,000 for each form that you might argue are substantially incomplete in their presentation).

Please confirm this is approved. All taxes due were paid when we requested the extension in June, 2018.

Kind regards,

_________________________Signature Taxpayer 1 (USC)

__________________________Signature Taxpayer 2 (USC)

For some additional guidance in layman’s terms, you might want to look at the IRS website that is somewhat helpful and titled: Frequently Asked Questions (FAQs) About International Individual Tax Matters