Month: November 2015

Survey of the Law of Expatriation from 2002: Department of Justice Analysis (Not a Tax Discussion)

Most discussions regarding renunciation/relinquishment of U.S. citizenship are highly focused towards the U.S. federal tax consequences. Today, the focus is on a 2002 report prepared by the DOJ for the Solicitor General, who supervises and conducts government litigation in the United States Supreme Court.

The report is found here, and I have highlighted some key excerpts: Survey of the Law of Expatriation: Department of Justice Analysis:

* * *

Another Common Misunderstanding of U.S. Tax Laws (Myth No. #8)

Myth #8: As a U.S. citizen (USC) there is no need to pay tax on income or gains from assets outside the U.S., as long as the proceeds are not repatriated to a U.S. bank or financial institution.

As a follow-on to the post of Nov. 19, 2015, See WSJ = World/Expats – For an Excellent Overview of U.S. Taxation for U.S. Citizen Individuals in Plain English, I just heard this one this past week from  a cross border businessman. It has a perfect logic to it the same as the idea that a controlled foreign corporation that moves cash to its own U.S. bank account (as opposed to a financial account outside the U.S.), is subject to U.S. income taxation at that moment.

a cross border businessman. It has a perfect logic to it the same as the idea that a controlled foreign corporation that moves cash to its own U.S. bank account (as opposed to a financial account outside the U.S.), is subject to U.S. income taxation at that moment.

Laypeople often focus on – “where is the money” not “who has *’recognized’ the income” irregardless of where the money or property is physically located.

This international business operator is thoughtful and has been doing cross border business for some 20+ years with a principle part of his business outside the U.S.; although he is a dual national citizen and hence necessarily a U.S. income tax resident.

It’s a fairly common misunderstanding that I have seen multiple times in my career.

The federal tax law does not look to where the property or income is physically located or earned; unlike some countries which have a territorial based taxation system for individuals, e.g., Costa Rica, Hong Kong, Malaysia, Panama, Singapore and Paraguay, among many others which are smaller economies.

Plus, the federal tax law is not changed by the laws of the country where the income was earned.

Instead, the tax law looks to who “recognized”* the income, irrespective of where the property or cash from that income is located.

A common sense example brings home the concept. Assume you live in Georgia (the one next to Florida not Russia) and sell real estate in Texas and leave the proceeds from the sale in a Texas bank. Texas may not impose individual income taxation on the sale of the Texas real estate (where the property was physically located), but still the state of Georgia looks to who earned the income. In this case, the income was earned by a resident of Georgia, so Georgia imposes taxation on the income from the sale, even though the cash proceeds from the sale are left in a Texas bank.

By analogy, this is how the U.S. federal government imposes taxation; with one important break in the analogy. The U.S. federal government treats USCs as income tax residents, irrespective as to where they reside; whereas George only taxes those who are physically resident in their state on a worldwide basis.

For instance, a U.S. citizen residing in Singapore, who sells real estate in a country outside both the U.S. and even Singapore, e.g., Malaysia where the tax rate on the real estate capital gains is 0%, will have earned that income in Malaysia (the where). Even if the U.S. citizen keeps his funds in a Malaysian bank or even moves the funds to a Singapore bank the country of residence (still the where), he or she will be subject to U.S. income taxation, since the USC status (the who) creates tax residency irregardless of the physical residency. See, Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) posted June 27, 2014 and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense? posted April 1, 2014.

It does not matter that the funds are not moved to a U.S. bank account, just like it did not matter for the Georgian resident that she kept her proceeds from the Texas real estate sale’s transaction in a Texas bank.

- * The term “recognized” is a technical U.S. federal tax term that determines at that moment in time a U.S. taxpayer has income for federal tax purposes; and hence, generally the requirement to report the income on their tax return.

See WSJ = World/Expats – For an Excellent Overview of U.S. Taxation for U.S. Citizen Individuals in Plain English

For an excellent overview (without penalty hype or exaggeration of the U.S. tax law), read the following article from Eric Scali of H&R Block’s expat-focused service titled –Puncturing 7 Common Myths about U.S. Expat Tax Rules, Nov. 15, 2015, WSJ = Globe, EXPAT, For global nomads everywhere

The following 7 myths are accurately addressed with respect to U.S. citizens residing outside the U.S. (although caution should be taken if you are a lawful permanent resident – “LPR”- residing inside a country with a U.S. income tax treaty – see, Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?, posted April 11, 2015 and the discussion of how many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

Myth #1: Individuals living outside of the U.S. and filing tax returns with a foreign government don’t have to file annual U.S. tax returns.

Myth #2: Expats only need to report their U.S. income on their U.S. tax return.

Myth #3: If their foreign income is below the Foreign Earned Income Exclusion (FEIE), expats don’t need to file a U.S. tax return.

Myth #4: Work performed by an expat within the U.S. but paid by an expat’s foreign employer is foreign income because it’s paid by the foreign employer and not issued on a W-2.

Myth #5: Expats’ non-U.S.-based pension plans have the same tax treatment in the U.S. as they do in their country of residence.

Myth #6: When expats receive certain items of income, they’re only taxable in their country of residence under the rules provided for in the income tax treaty the foreign country has with the U.S.

Myth #7: An expat’s foreign investments are treated the same as they are in the foreign country.

Unfortunately, I have heard all of these and more (many times over) during my professional career as an international tax lawyer (and an accountant in the late 1980s) from both individuals and their tax advisers both inside the U.S. and outside the U.S. As someone who lives with their family outside the U.S., I have a good understanding about the difficulty of finding good U.S. tax resources that accurately and simply explain these very complex laws.

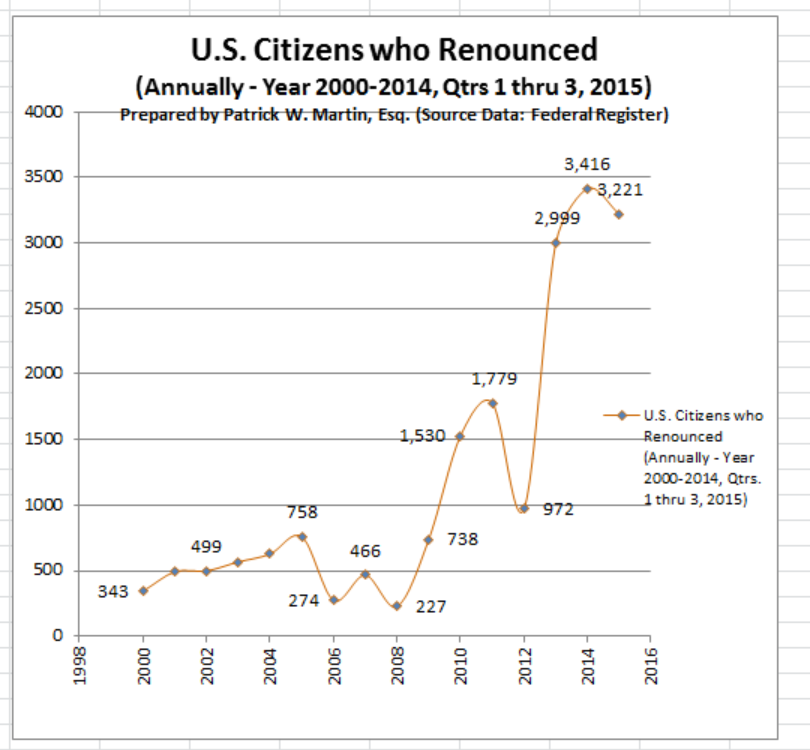

WSJ Asks the Question: Is the IRS Undercounting Americans Renouncing U.S. Citizenship?

Is the IRS Undercounting Americans Renouncing U.S. Citizenship?, posted Sept. 16, 2015.

The names of U.S. citizens who have renounced is published quarterly pursuant to IRC Section  6039G. See, prior related posts: 1,426 Individuals Give Up Passport: Record Number of U.S. Citizens Renouncing: Quarter 3 for 2015, October 30, 2015.

6039G. See, prior related posts: 1,426 Individuals Give Up Passport: Record Number of U.S. Citizens Renouncing: Quarter 3 for 2015, October 30, 2015.

No one knows for certain if the IRS (including the IRS per some of my conversations) is getting complete data from the Department of State regarding each name and individual.

The graph I have prepared shows the number of names reported quarterly as I track all reported names quarterly that related to clients and non-clients. The latest cumulative amounts for 2015 (which does not include the 4th quarter) shows 3,221 thus far in the year. If there is close to 1,400 as was the case for the last quarter, the total will be a record – by a bunch; i.e., close to 5,000 renunciations for the year.

Anecdotally, I have seen renunciations surge in our practice, largely as U.S. citizens residing around the world (typically in the “Accidental American” category) learn about the long arm of the U.S. tax law by way of their local financial institutions and reporting and documents requested as part of FATCA. See, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets, posted Nov. 2, 2015.

None of this answers the question of whether there is under-reporting of the names? Indeed, the question will likely not be answered without more information provided by the U.S. Department of State and the U.S. Treasury (i.e., the IRS officers responsible for issuing the names and report in the Federal Register).

The government is also likely to reject issuing information on these details to individuals and their advisers as part of a Freedom of Information Act (“FOIA”) request. I have had similar requests rejected by the government under the so called “Exemption 7(E)” of FOIA. See,

U.S. Citizens Overseas are Often Ill Advised to go into the (1) OVDP and sometimes even the (2) the Streamlined Filing Procedure

There have been prior posts discussing what is referred to as the offshore voluntary disclosure program (“OVDP”) and what the IRS later created – the so-called “streamlined program” filing procedure.

For more background, see, GAO Yr2014 Report on Offshore Voluntary Disclosure Program Indicates Less Than 4% of Taxpayers Lived Outside the U.S., posted March 11, 2014.

Importantly, these OVDP and streamlined programs created by the IRS are not creatures of any statutory law, for instance Title 26 (the Internal Revenue Code) or Title 31 (the so-called Bank Secrecy Act); or any law for that matter. There are no court cases or Treasury Regulations that spell out the terms of these programs as part of any legal framework.

I like to say they are similar to the Hasbro rules of “Monopoly”; a game I was fond of as a child. The IRS is like Hasbro in that they can change the rules of the game as they wish, and often do in the form of publicized frequently asked questions (“FAQs”). The IRS submits these rules of their game and ask, encourage and in some cases (in my view) browbeat taxpayers, often times through their advisers, into participating. See some of the various rule changes below –

- IRS OVDP FAQs and Answers 2012

- Transition Rules: Frequently Asked Questions (FAQs)

- IRS 2011 Offshore Voluntary Disclosure Initiative

- January 8, 2010 — added Q&As 53-54

- August 25, 2009 — added Q&A 52

- July 31, 2009 — modified A6, A21 and A22

- June 24, 2009 — modified A26 and added Q&A 31-51

- May 6, 2009 — posted Q&A 1-30

The above reflect just some of the modifications and rules the IRS has made, and keeps making to their rules of their proposed OVDP structure; which again, I repeat, is not part of the law.

Many taxpayers and their advisers, in my view have not thought carefully about the law and its application; but rather have focused on the “Monopoly” rules. They cite and read the FAQs if that is somehow the law! See How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Similarly, the streamlined filing procedures is not part of the law, and also has been modified several times by the IRS. Fortunately, the IRS realized that U.S. taxpayers residing outside the U.S. are not the same as those who reside in the U.S. when they created two separate programs last year in 2014.

The point of this post is that I have seen numerous cases where U.S. citizens residing around the world were ill advised to participate in the OVDP. In short, if an individual has no criminal tax liability, I think there is little purpose or reason for almost all USC overseas to participate into the OVDP. Analyzing thoughtfully the facts of each case and the law (not the Monopoly rules) is what is important for each individual.

Finally, a clear understanding of what are the Monopoly rules compared to the law is crucial when advising USCs residing overseas. Sometimes, filing through the streamlined procedure might be well advised for a particular taxpayer; e.g., if they would otherwise have substantial late payment and late filing penalties. However, there are plenty of cases where simply filing tax returns pursuant to the law will be preferable in a particular case. This is a process that needs to be thoughtfully considered in each case with a clear understanding of the law – not just the Monopoly rules.

For some related commentary on this topic, see the following posts:

Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

This post is written simply because so many U.S. citizens residing overseas are reasonably confused about the complexity of U.S. tax law. The mere requirement to file U.S. income tax returns for those overseas often comes as a great surprise. My non-U.S. born wife is an exception (as she also lives outside the U.S.) simply because I have repeatedly told her for our 20 some years of marriage.

Some in the IRS erroneously think U.S. citizens residing overseas do and should understand U.S. tax law. I posed one simple scenario to a very sophisticated IRS attorney not very long ago who specializes in the FATCA rules.

Her view is (hopefully was) that U.S. citizens throughout the world know or should know the U.S. tax laws because the instructions to IRS Form 1040 are clear.

This thought knocked me off my figurative chair onto the floor! Smack.

My surprise is based upon my own experience working with individuals and families throughout the world, in numerous countries. I have noticed a number of notions, based upon these andectodal experiences as follows:

- A minority of U.S. citizens (unless they lived most of their lives in the U.S. and recently moved overseas as an “expatriate”) have no real basic idea of how the U.S. federal tax laws work; let alone to their assets and income in their country of residence. See USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

- There are indeed plenty of immigrant U.S. residents (certainly less than 50% by my own experience – especially when concepts of PFICs and foreign tax credits start being discussed) who even understand the basics of U.S. international tax law.

- If they reside in an English speaking country that has relatively strong family or historical ties to the U.S. (e.g., England, Ireland, Scotland, and Canada, etc.) they are likely to have a better idea of the U.S. federal tax laws, but still the majority don’t know key concepts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

- Even those in English speaking countries that have less historical or family ties to the U.S. have a lesser understanding (e.g., New Zealand, Australia, Kenya, South Africa, India, etc.).

- Those who do not speak English know even less about U.S. tax laws and how they apply to them.

- Many individuals who learn of these requirements overseas are sometimes driven to great despair. The message they receive is not a correct one under the law in my view: as they read IRS materials (for instance, see FAQs 5, 6 and and former 51.2 from the Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers 2014) and come to the conclusion they will soon be going to jail, criminally prosecuted or otherwise be subject to tens of thousands of dollars worth of penalties for their failure to file a range of tax forms.

- Literally, sometimes as a tax lawyer I feel more like a psychologist, when these individuals come to me saying they can’t sleep, they can’t eat, they are seeing a cardiologist for high blood pressure, etc. and even in a most extreme case they thought suicide was a solution. See, How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas.

- Individuals around the world (even tax professionals) and certainly laypeople, are not commonly reading TaxAnalysts (nor would they subscribe) or other tax professional publications that explain many of the intricacies of U.S. tax laws.

- Learning and understanding U.S. tax laws, including just the basics, requires a great deal of time, aptitude for nuances and details, literacy, patience and a level of aptitude for such matters that simply escape many people around the world (most I would say). see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. I can relate to this personally, as I am an international tax professional (indeed I even studied a post graduate law course outside the U.S. in a non-English language), have spent my entire professional career of more than 25 years in the area, and yet only generally have a very superficial understanding of tax laws throughout the countries where I am dealing with clients. I don’t try to understand the details of those laws.

- Many people are angry and frustrated (justifiably so, in my view, in many cases) after learning they are subject to these rules. See comment above about being a psychologist. Plus, USCs and LPRs residing outside the U.S. – and IRS Form 8938. In addition, see, Taxpayer Advocate Report on Burdens of Benign Taxpayers who Make Mistakes

Back to the intelligent IRS tax attorney. My question to her was: “Why would you, as a U.S. born individual not be reviewing the tax laws, tax forms and tax instructions of the country where your parents were born prior to immigrating to the U.S.?” I asked: “Are you not reviewing those laws in the original language of your parents (not English, but the other language of your parent’s country) to understand what tax forms and returns you should be filing?”

The IRS attorney’s response was: “What: of course, I am not reviewing such tax forms or filing information or tax laws, as I would have no tax obligations in that foreign country where I have no income, no assets or no bank or financial accounts!”

My follow-up question was a simple one: “Don’t you realize that U.S. federal tax law (Title 26) and financial bank reporting laws (Title 31) do just that!”

“Hmm she paused: how can that be?” I don’t recall if she said this out loud, or just said it with her puzzled expression.

The answer of course is that through citizenship (including derivative citizenship through a U.S. parent even though the child never spent a single day of residence in the U.S., let alone received any income or assets); that same individual in the mirror position as that IRS attorney is subject to a host of U.S. federal tax and financial reporting laws. See, Sir Winston Churchill – Famous People. Did he become a U.S. citizen at birth via “derivative citizenship”? Did he file U.S. income tax returns?

Here is the big disconnect. It’s not just among the ill-informed or those lesser educated on the fine points of law. I had the pleasure this week along with my wife to host two educated, worldly and engaging individuals who have been married some 20 years together. They are well read and highly educated. Both are lawyers by training, one practices law that often pushes him fairly deeply into the tax law and his wife is a wonderful and experienced judge in the California state courts.

I asked them (as I like to ask people around the world) if they had ever heard or understood that the U.S. federal tax law imposes taxation and very detailed reporting on the worldwide income and assets of U.S. citizens who reside outside the U.S. I discussed  Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

All of it was a great surprise to them! They were in utter shock and both are residents in the U.S., highly educated in the law and are like the vast majority of the world, including U.S. citizens who reside outside the U.S.

This is the common response for many U.S. citizens residing overseas.