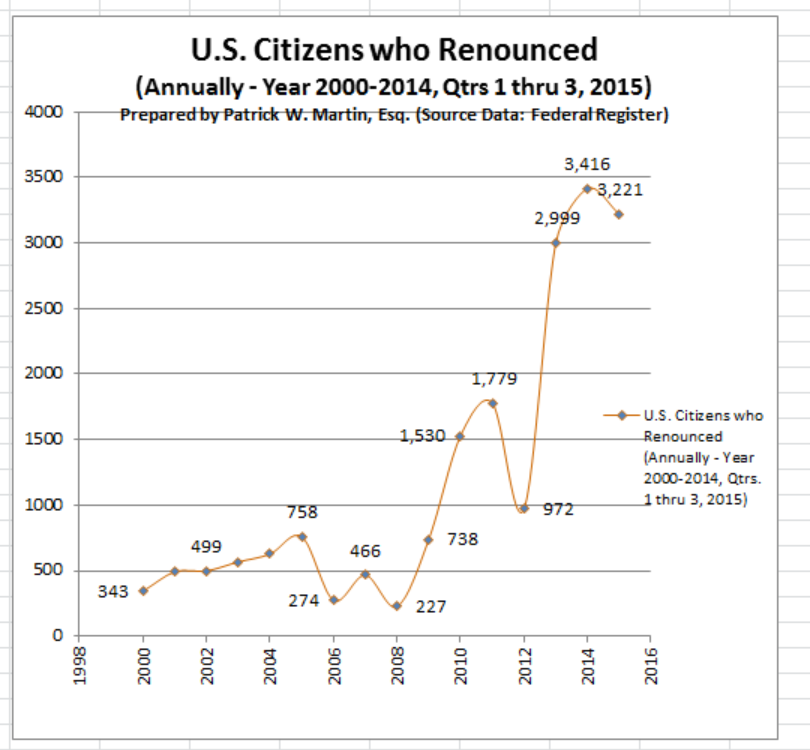

There is an idea that only recently has permanent resident US immigration status into the United States grown substantially. The peak years were in the early 1990s as to absolute numbers. However, the greatest number of permanent residents as a relative percentage of the population was in the early 1900s; by far. See the chart below that I created from DHS immigration statistics data.

There were more LPRs admitted, in absolute terms in 1905 (1,026,499) than in 2022 (1,018,349).

[arm_restrict_content plan=”2,” type=”show”]

In percentage terms the total number of LPRs in 1905 compared to the total population was more than four times (4X) greater than in 2022 when it was (about 3/10th of 1 percent or 0.306%; versus a total population of 333 million) . In 1905 the total population was about 84 million, with newly admitted LPRs representing 1.225 percent of the entire resident population (1.225%; is greater than 4X the 2022 relative percentage).

The “Mark to Market” Tax that did NOT Exist in 1820, 1913, 1966 (Not Until 1996)

The US tax expatriation laws now impose a “mark to market” tax on so-called “long-term residents” who become “covered expatriates.” Such a concept in the tax law never existed in the early part of the 20th century, and indeed only became law in 1996. See an earlier post, The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of US Tax Expatriation law

This so-called Mark to Market tax is based upon a legal fiction, as if the individuals sold their worldwide assets on the “expatriation date.” It applies, even though there’s no current sale of assets, no disposition, transfer, change of ownership, change of title, or other “realization” event. The term “realization” is very significant in US tax law, including as recently discussed by the United States Supreme Court. See below and Moore v. the United States (2024) .

Below is a table of LPRs who were admitted to that status, per year, over the last 200+ years starting in 1820:

Are you or any of your family members one of these millions (more than 88 million) of LPR individuals represented in the above graph over the last 200+ years?

No, not talking about Texas-Style Chili as reported in the – NYT Cooking Recipe.

Chile, the country in South America and the newest country to have an income tax treaty go into force with the United States. The U.S.-Chile Tax Treaty (in the works for more than a decade) went into force at the end of 2023, on 19 December 2023.

The question is how many “LPRs” are residing in a tax treaty country that are impacted favorably (presumably all of them) by the federal district court decisions we successfully handled against the IRS and DOJ, Tax Division: Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)?

As previously explained, the Aroeste decision will affect potentially millions of “Green Card” holders (a subset of the 3.89M estimated by the government) living outside the U.S. Those who have not formally abandoned their lawful permanent residency status. See, “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – (2020). This “LPR Tax Limbo” is no longer the case after the Aroeste decision.

These individuals who are living in tax treaty countries are not in “LPR Tax Limbo” any more since the Court clarified when the individual is not a United States tax resident. The Court explained, that filing a “late” tax treaty position, does not cause the non-U.S. citizen to have waived the benefits of the income tax treaty. It is the tax treaty with each of the 66 countreis that has the potential of unlocking the “escape hatch” described by the Court.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

The court in Aroeste outlined a 5-step analysis that becomes crucial for the 3.89 million LPRs residing abroad in one of the 66 tax treaty countries, in determining whether they are “United States persons” under the law. This will be covered in Part II.

Millions of LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in November 2023 as of 2014 (until the Chile treaty came into effect). The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importantly, anyone in these circumstances would be remiss, if they did not consider carefully the “mark to market” tax implications to them if they were to become a “covered expatriate” as defined in the law. These “mark to market” tax consequences can have potentially devastating consequences, including to U.S. beneficiaries in the future if not properly planned and considered.

This post is written simply because so many U.S. citizens residing overseas are reasonably confused about the complexity of U.S. tax law. The mere requirement to file U.S. income tax returns for those overseas often comes as a great surprise. My non-U.S. born wife is an exception (as she also lives outside the U.S.) simply because I have repeatedly told her for our 20 some years of marriage.

Some in the IRS erroneously think U.S. citizens residing overseas do and should understand U.S. tax law. I posed one simple scenario to a very sophisticated IRS attorney not very long ago who specializes in the FATCA rules.

Her view is (hopefully was) that U.S. citizens throughout the world know or should know the U.S. tax laws because the instructions to IRS Form 1040 are clear.

This thought knocked me off my figurative chair onto the floor! Smack.

My surprise is based upon my own experience working with individuals and families throughout the world, in numerous countries. I have noticed a number of notions, based upon these andectodal experiences as follows:

A minority of U.S. citizens (unless they lived most of their lives in the U.S. and recently moved overseas as an “expatriate”) have no real basic idea of how the U.S. federal tax laws work; let alone to their assets and income in their country of residence. See USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

There are indeed plenty of immigrant U.S. residents (certainly less than 50% by my own experience – especially when concepts of PFICs and foreign tax credits start being discussed) who even understand the basics of U.S. international tax law.

Even those in English speaking countries that have less historical or family ties to the U.S. have a lesser understanding (e.g., New Zealand, Australia, Kenya, South Africa, India, etc.).

Those who do not speak English know even less about U.S. tax laws and how they apply to them.

Many individuals who learn of these requirements overseas are sometimes driven to great despair. The message they receive is not a correct one under the law in my view: as they read IRS materials (for instance, see FAQs 5, 6 and and former 51.2 from the Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers 2014) and come to the conclusion they will soon be going to jail, criminally prosecuted or otherwise be subject to tens of thousands of dollars worth of penalties for their failure to file a range of tax forms.

Individuals around the world (even tax professionals) and certainly laypeople, are not commonly reading TaxAnalysts (nor would they subscribe) or other tax professional publications that explain many of the intricacies of U.S. tax laws.

Learning and understanding U.S. tax laws, including just the basics, requires a great deal of time, aptitude for nuances and details, literacy, patience and a level of aptitude for such matters that simply escape many people around the world (most I would say). see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. I can relate to this personally, as I am an international tax professional (indeed I even studied a post graduate law course outside the U.S. in a non-English language), have spent my entire professional career of more than 25 years in the area, and yet only generally have a very superficial understanding of tax laws throughout the countries where I am dealing with clients. I don’t try to understand the details of those laws.

Back to the intelligent IRS tax attorney. My question to her was: “Why would you, as a U.S. born individual not be reviewing the tax laws, tax forms and tax instructions of the country where your parents were born prior to immigrating to the U.S.?” I asked: “Are you not reviewing those laws in the original language of your parents (not English, but the other language of your parent’s country) to understand what tax forms and returns you should be filing?”

The IRS attorney’s response was: “What: of course, I am not reviewing such tax forms or filing information or tax laws, as I would have no tax obligations in that foreign country where I have no income, no assets or no bank or financial accounts!”

My follow-up question was a simple one: “Don’t you realize that U.S. federal tax law (Title 26) and financial bank reporting laws (Title 31) do just that!”

“Hmm she paused: how can that be?” I don’t recall if she said this out loud, or just said it with her puzzled expression.

Here is the big disconnect. It’s not just among the ill-informed or those lesser educated on the fine points of law. I had the pleasure this week along with my wife to host two educated, worldly and engaging individuals who have been married some 20 years together. They are well read and highly educated. Both are lawyers by training, one practices law that often pushes him fairly deeply into the tax law and his wife is a wonderful and experienced judge in the California state courts.

All of it was a great surprise to them! They were in utter shock and both are residents in the U.S., highly educated in the law and are like the vast majority of the world, including U.S. citizens who reside outside the U.S.

This is the common response for many U.S. citizens residing overseas.

For decades, the IRS largely worked in a vacuum, relative to other government agencies.

Changes started in earnest in 2003 after September 11, 2001, when Congress past various anti-terrorism laws. For details of the history and how and when the IRS became responsible for these functions, the IRS Internal Revenue Manual has a detailed explanation – Part 4, Chapter 26, Section 5. Bank Secrecy Act History and Law

Today there are a host of governmental inter-agency activities along with foreign government exchanges of information; e.g., DHS, Department of State, ICE, USCIS, foreign government exchanges of information under FATCA IGAs, a plethora of federal “intelligence agencies” for “terrorism related requests” as identified in IRM pursuant to IRC Section 6103(i), foreign governments under tax treaty exchanges, among many others.

The law is not even clear as to which agencies qualify as “intelligence agencies” as they are not identified in the statute and many are presumably classified organizations.

Who is an “intelligence agency” for purposes of the statute?

The following is a list of some of the intelligence agencies that are presumably included in the federal tax statute Section 6103(i)(7):

State Department INR – Bureau of Intelligence & Research

INL – Bureau for International Narcotics and Law Enforcement Affairs

CT – Counterterrorism Office

DS – Bureau of Diplomatic Security

A less secret organization is the Social Security Administration which now increasingly intersect with the work of

the IRS. Also, the Department of State now provides warnings on its Passport applications about tax consequences and requirements of social security numbers (“SSN”s).

Finally, see also how on the last page (page 28) of currently issued U.S. Passport (“Book“) and paragraph D that explains generally the taxation obligations of citizenship.

Revenue Manual has a detailed explanation –

Revenue Manual has a detailed explanation –