International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

A U.S. Immigration Officer Stops You at at the Airport – @ the Point of Entry (Demands your Green Card be Turned Over))

Being stopped, searched, interrogated or simply questioned by U.S. federal government agents can be intimidating. Especially, if you do not know your legal rights.

It can be more intimidating on your arrival to the U.S. airport, if the CBP officer (U.S. Customs and Border Protection) demands that you physically “return voluntarily” your green card. The consequences they tell you will be immediate deportation from the U.S.

Removal from the U.S. – is it voluntary or not, under these circumstances?

What are the U.S. federal tax consequences if you “return voluntarily” your green card?

What if the CBP officer pulls out Forms W-8s you previously signed with your foreign financial institution and presents them to you in the airport and asks the following questions:

Why did you certify “under penalty of perjury” you were not a United States person on your foreign bank produced documents (you received in France, Germany, the U.K., Canada, Mexico, Japan, Indonesia, Australia — or any other foreign country)?

The officer then asks for all of the envelopes and papers in your luggage and opens the letters and files in your possession – See, the U.S. Supreme Court decision United States v. Ramsey, 431 U.S. 606 (1977).

Tax Problems that Turn Serious – can Cause a Green Card Holder to become a “Covered Expatriate”

In Kawashima v. Holder (565 U.S. 478 (2012), the United States Supreme Court held that certain tax offenses committed by lawful permanent residents constitute crimes involving “fraud or deceit” for purposes of the Immigration and Nationality Act (“INA”). Specifically, the Court concluded that lawful permanent residents (a husband and wife from Japan) who were convicted of filing false tax returns resulting in a tax loss exceeding $10,000 had been convicted of an “aggravated felony” within the meaning of the INA.

As a consequence, a conviction for such an aggravated felony renders a lawful permanent resident removable (deportable) from the United States under the immigration laws. Importantly, however, the criminal conviction itself does not automatically terminate lawful permanent resident status. Rather, it provides the legal basis for the Department of Homeland Security to initiate removal proceedings, after which an Immigration Judge may enter a final order of removal.

Once a final order of removal becomes effective, the individual’s lawful permanent resident status is considered to have been revoked. For U.S. federal income tax purposes, this generally results in the termination of lawful permanent resident status under 26 U.S.C. § 7701(b)(6)(B), which provides that an individual ceases to be a lawful permanent resident when “such status has been revoked or has been administratively or judicially determined to have been abandoned.” Accordingly, following a final order of removal, the individual is no longer treated as a lawful permanent resident for purposes of the tax law as summarized below:

Stage

Legal Effect

1. Criminal conviction (including guilty plea)

If the offense qualifies as an “aggravated felony” under INA §101(a)(43), the individual becomes deportable under 8 U.S.C. §1227(a)(2)(A)(iii). A guilty plea counts as a conviction for immigration purposes if the statutory definition of “conviction” is satisfied.

2. DHS initiates removal proceedings

DHS serves a Notice to Appear (NTA) charging removability before an Immigration Judge under 8 U.S.C. §1229a.

3. Immigration Judge determines removability

DHS bears the burden of proving deportability by clear and convincing evidence, typically through the certified judgment of conviction.

4. Final order of removal

If removability is sustained and no relief is available, the Immigration Judge orders removal. After appeals are exhausted (or waived), the removal order becomes final, and the person’s LPR status ends.

The 2012 case involved Akio and Fusako Kawashima, Japanese citizens who had been lawful permanent residents since 1984. Mr. Kawashima pleaded guilty to willfully filing a false tax return under 26 U.S.C. § 7206(1), while Mrs. Kawashima pleaded guilty to aiding and assisting in the preparation of a false tax return under 26 U.S.C. § 7206(2). The immigration judge issued the order of removal. The Board of Immigration Appeals affirmed. Holding that convictions under 26 U. S. C. §§7206(1) and (2) in which the Government’s revenue loss exceeds $10,000 constituted aggravated felonies, the Ninth Circuit affirmed and ultimately so too did the SCOTUS in this decision.

The Supreme Court concluded that these tax offenses necessarily involve fraud or deceit and, because the tax loss exceeded the statutory $10,000 threshold, they constituted aggravated felonies under immigration law. The Supreme Court of the U.S. therefore upheld the government’s order (which had been upheld through the Ninth Circuit Court of Appeals) removing the Kawashimas to Japan.

This of course is important for U.S. “expatriation tax” purposes, since the “lawful permanent resident” status for tax purposes will necessarily terminate upon the final order of removal. Not before. Once LPR status terminates, the individuals will become covered expatriates, if they meet the time period under the statute to become “long term residents” as was the case for Mr. and Mrs. Kawashima and meet either of the three tests: the tax liability, net asset and certifications of compliance with the federal tax laws. See, Why a “long-term” LPR can NEVER avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B) if Asset or Tax Liability Test is Satisfied!

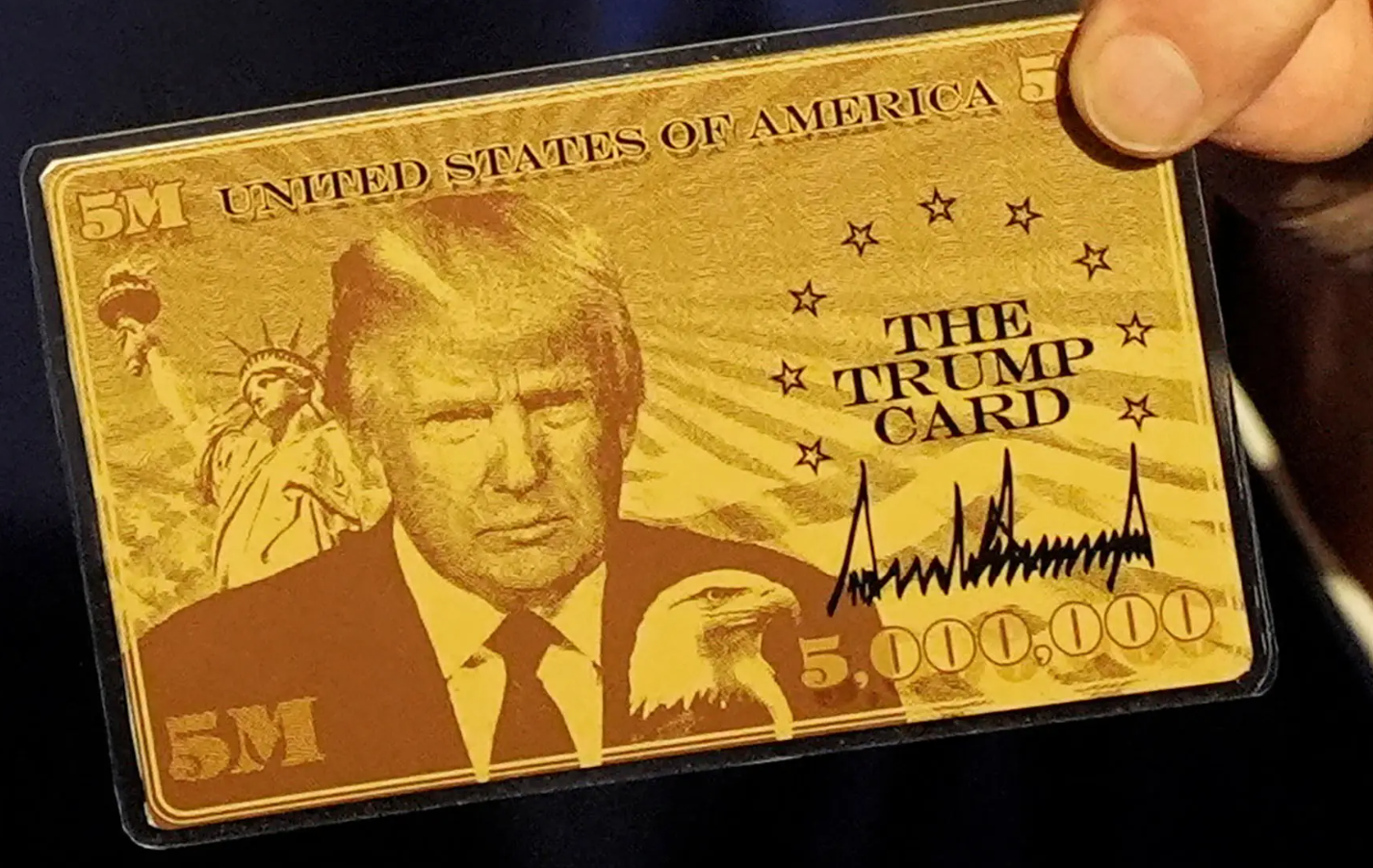

Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

See Part I for the background discussion, which was published more than a year ago.

This article focuses on the tax consequences of the “Trump Gold Card” program and, in particular, the implications if participation ultimately leads to U.S. citizenship (“USC”).

The final version of the Gold Card program requires a $1 million contribution to the federal government, rather than the $5 million amount initially discussed in April 2025. See the government website, The Trump Gold Card is Here.

It is also important to note that President Trump established the Gold Card program through Executive Order 14351 in September 2025. Congress did not enact the program through legislation.

The Cost of a Trump Gold Card

For a $15,000 Department of Homeland Security processing fee and, following successful background review, a $1 million contribution to the federal government, an applicant may obtain U.S. permanent residence through the Gold Card program.

Why Would an Ultra-High-Net-Worth Individual Voluntarily Enter the U.S. Tax Net?

A fundamental question arises: Why would an ultra-high-net-worth (“UHNW”) individual contribute $1 million to obtain U.S. residence and potentially U.S. citizenship, thereby becoming subject to one of the world’s most expansive tax systems?

For many individuals, acquiring U.S. citizenship or lawful permanent resident (“LPR”) status can result in exposure to:

U.S. income taxation on worldwide income;

U.S. gift taxation on worldwide transfers of property; and

U.S. estate taxation on worldwide assets at rates that currently reach 40%.

U.S. Estate and Gift Taxation of Worldwide Assets

The United States generally imposes estate and gift taxes on the worldwide assets of U.S. citizens. In addition, lawful permanent residents who are domiciled in the United States may become subject to the same worldwide transfer tax regime.

Unlike many countries, the United States generally does not permit its citizens to escape worldwide taxation simply by relocating abroad. Most U.S. income tax treaties and estate and gift tax treaties contain a “savings clause” that preserves the right of the United States to tax its citizens notwithstanding treaty provisions.[1]

U.S. Estate and Gift Taxation of Worldwide Assets

As a result, the worldwide assets of a U.S. citizen may be included in the U.S. transfer tax system under IRC §§ 2001 and 2031 (estate tax) and IRC §§ 2501 and 2511 (gift tax).

Consider a U.S. citizen who owns:

a residence in Norway;

shares of a Mexican corporation;

a bank account in Singapore;

an interest in a Liechtenstein foundation (Stiftung);

a portfolio of securities held through a London financial institution; and

an apartment in Dubai.

Subject to applicable valuation and ownership rules, each of these assets generally forms part of the individual’s worldwide taxable estate for U.S. estate tax purposes.

By contrast, a non-U.S. citizen who is not domiciled in the United States generally would not be subject to U.S. estate tax on any of these assets, unless they include U.S.-situs property such as stock issued by U.S. corporations.

The difference can be dramatic: no U.S. estate tax exposure versus potential exposure to a 40% U.S. estate tax on worldwide assets.

U.S. Income Taxation of Worldwide Income

The contrast is equally significant in the income tax context.

A nonresident generally is subject to U.S. income taxation only on limited categories of U.S.-source income and income effectively connected with a U.S. trade or business.

A U.S. citizen, however, remains subject to U.S. federal income taxation on worldwide income regardless of where the individual resides.

Consequently, a foreign entrepreneur, investor, or family office principal who acquires U.S. citizenship will find that income earned from businesses, investments, trusts, partnerships, and financial accounts throughout the world generally becomes reportable to the Internal Revenue Service and subject o U.S. income taxation.

That result raises an obvious question: if the program is available, why have so few ultra-high-net-worth individuals pursued it successfully?

The most obvious explanation is that the long-term U.S. tax consequences may outweigh the perceived immigration benefits for many globally mobile individuals.

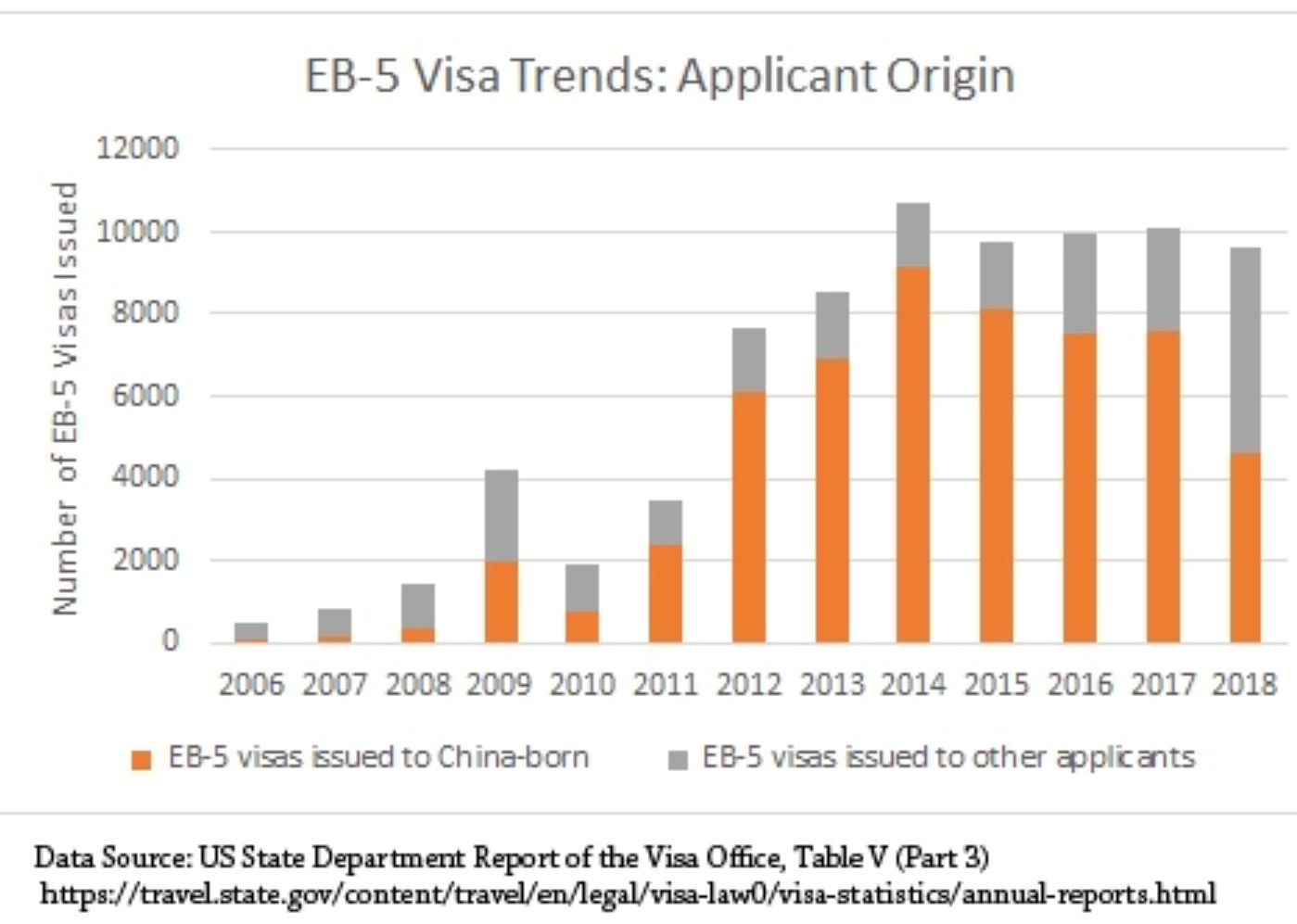

Comparison to the EB-5 Program

Different applicants may have different motivations.

The traditional EB-5 immigrant investor program generally requires a qualifying investment that, if successful, may ultimately be recovered. The program also requires satisfaction of statutory requirements, including job creation. Approximately 200,000+/- individuals have obtained a green card through the EB-5 program. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

EB-5 Visa Applicants by Country

By contrast, the Gold Card program requires a direct contribution to the federal government.

In either case, the successful applicant receives lawful permanent resident status. However, if the Gold Card ultimately serves as a pathway to naturalized U.S. citizenship, the applicant may become subject to the unique worldwide taxation regime applicable to U.S. citizens.

The Expatriation Problem

If Gold Card holders ultimately naturalize as U.S. citizens, future departure from the U.S. tax system will necessarily become significantly more complicated.

Individuals who later seek to relinquish U.S. citizenship will necessarily face the expatriation rules of IRC § 877A and be tainted with “covered expatriate” status.

As discussed in earlier posts, covered expatriate status can have substantial long-term tax consequences for both the expatriating individual and future recipients of gifts and inheritances.

Legal Questions Surrounding the Program

The Gold Card program also raises constitutional and statutory questions.

Unlike the EB-5 program, which was enacted by Congress, the Gold Card program was created through executive action. Congress did not amend Title 8 of the United States Code to establish a new immigrant category.

Whether the Executive Branch possesses sufficient statutory authority to create such a program remains an open legal question (I am doubtful it will be sustained – if challenged) and will likely be the subject of continued litigation and judicial review.

The outcome of pending litigation involving other immigration-related executive actions may provide useful guidance regarding the scope of presidential authority in this area. We await the outcome of the latest case litigated through the courts. See, Supreme Court appears likely to side against Trump on birthright citizenship which was also issued by an executive order.

Who Truly Benefits?

Who is the ideal candidate for a Trump Gold Card? Only one person thus far has one.

For almost all HNW individuals, the immigration benefits, travel flexibility, business opportunities, and potential pathway to U.S. citizenship would rarely justify the cost. Someone with assets below US$20M might find it attractive.

For almost all others—particularly those with substantial foreign businesses, investment portfolios, trusts, and family wealth located outside the United States—the long-term consequences of worldwide U.S. income, estate, and gift taxation will almost always substantially outweigh the advantages.

As a result, any prospective applicant for a Trump Gold Card should carefully evaluate not only the immigration benefits of the program (+ the uncertainty in the law), but particularly the tax consequences that will follow for decades thereafter.

Why Long-Term Green Card Holders Cannot Escape the Exit Tax Rules

When long-term green card holders give up their green card, they face the same exit tax rules as US citizens who renounce citizenship. There is one exception in the law that allows certain dual citizens by birth to avoid covered expatriate status even if they meet the income or asset tests. Long-term green card holders cannot use it. Here is why.

When you give up your green card (or renounce US citizenship), the law determines whether you are a covered expatriate. You are a covered expatriate if you meet any one of three tests: an average annual income tax liability above an inflation-adjusted threshold, a net worth of $2 million or more on the date of expatriation, or a failure to certify 5 years of US tax compliance – where it is commonly certified on IRS Form 8854.

Meeting even one of these three tests makes you a covered expatriate. All three tests apply equally to US citizens who renounce and to long-term lawful permanent residents (LPRs) who give up their green card.

Is there an exception to the income and asset tests?

Yes, for some people. Under IRC Section 877A(g)(1)(B), certain individuals are exempt from the income and asset tests. If this exception applies to you, you can avoid covered expatriate status even if your net worth exceeds $2 million or your income exceeds the threshold. The certification requirement under Section 877(a)(2)(C) still applies to everyone, including those who qualify for this exception.

Who can use this exception?

The exception is narrow. Under the statute, it applies only to an individual who: became a citizen of the United States and a citizen of another country at birth; as of the date of expatriation, continues to be a citizen of and is taxed as a resident of that other country; and has been a US resident for no more than 10 taxable years during the 15-year period ending with the taxable year of expatriation. Only someone who acquired US citizenship automatically at birth, while also holding citizenship of another country from birth, can potentially qualify.

Why green card holders cannot use it

Lawful permanent residents are not US citizens. They hold a green card, which is a grant of permanent resident status, not citizenship. Because the exception in Section 877A(g)(1)(B) applies only to individuals who became US citizens at birth, long-term LPRs cannot satisfy this requirement by definition. The exception is simply not available to them.

What this means if you are a long-term green card holder

A long-term LPR who meets either the $2 million asset test or the income tax liability test will become a covered expatriate, even if they fully satisfy the 5-year certification requirement. Satisfying the certification requirement is necessary for everyone, but for long-term LPRs it is not sufficient on its own. If you also meet the income or asset test, you are a covered expatriate regardless.

The consequences include the mark-to-market exit tax on unrealized gains and the Section 2801 tax on covered gifts and bequests to US persons. These consequences can affect your US family members for decades. Understanding them well before you give up your green card, not after, is the only way to plan for them.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Green Card Holders (Abandonment) – so Many More than U.S. Citizens who Renounce: The Topsnik Problem(s)!

I have previously written (pre-Aroeste v. United States) about the thorny issues that LPRs face when spending substantial time outside the United States. See an earlier post titled:

I highlighted some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law and now the case law in Aroeste makes these risks clear as confirmed in the landmark case.

A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particular case.

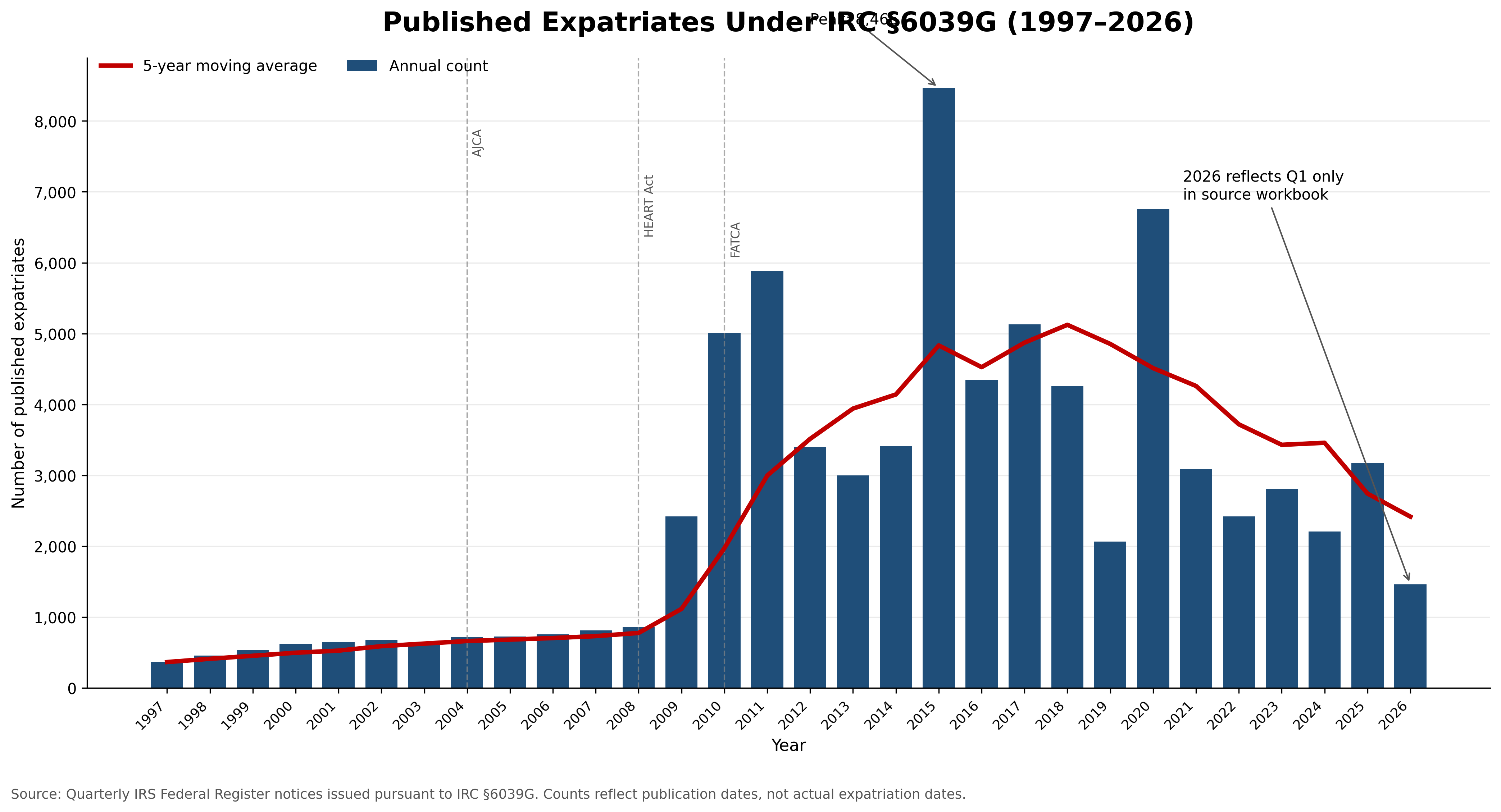

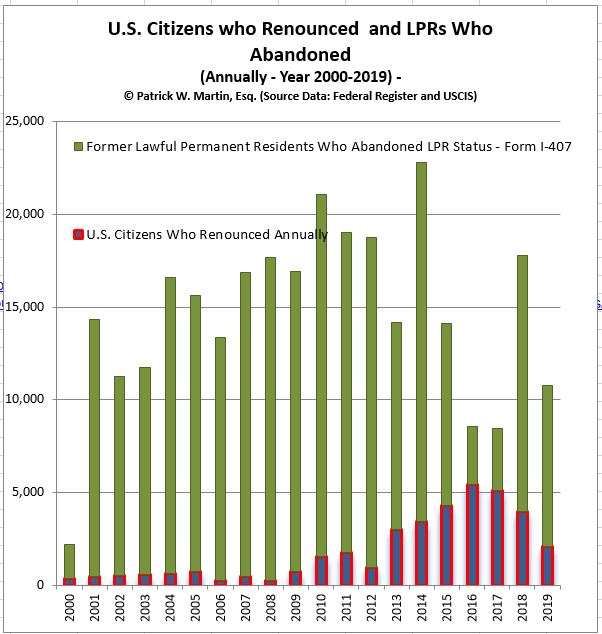

There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

* More Green Card Holders Abandon Status Than Citizens Renounce Citizenship

A frequently overlooked fact is that:

Formal Abandonment of LPR Status Is More Common Than Citizenship Renunciation

Each year, substantially more lawful permanent residents formally abandon their green cards than U.S. citizens formally renounce citizenship. The focus in the press and media is typically U.S. citizens who formally renounce. Here is my most recently compiled graph, the total number of U.S. citizens renouncing is typically in the thousands (few) each year. It has trended downward post-COVID.

However, with LPRs, formal recognition of abandonment by filing Form I-407 (not including informal abandonments which are multiple times greater) is multiple times greater.

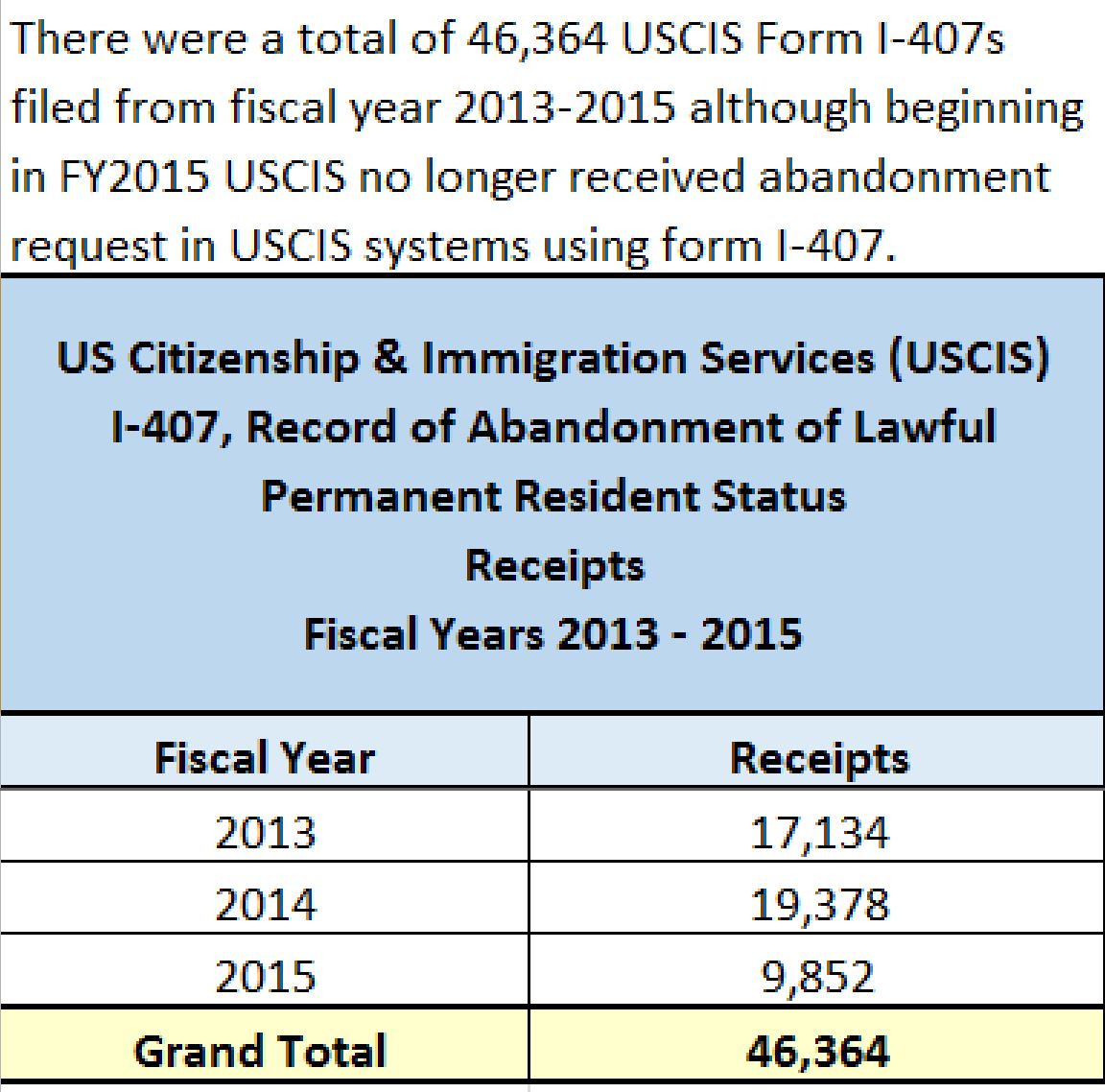

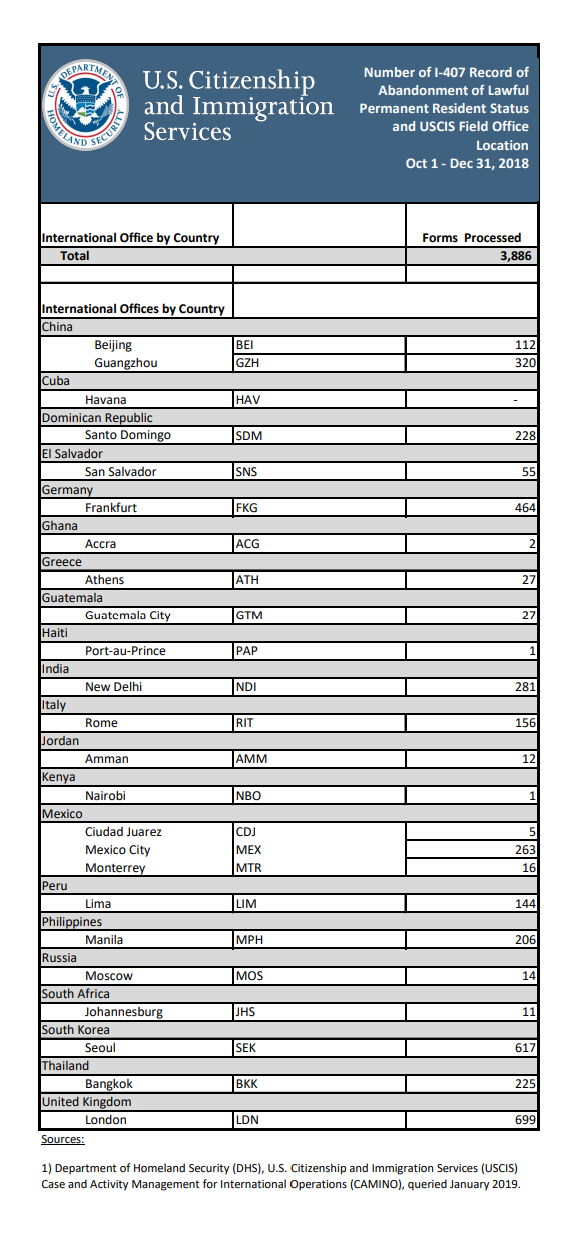

The graph I created several years ago, shows that formal LPR abandonments are mlutiple times greater than citizenship renunciation. I made a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

I have made a new FOIA request for more recent records, since this data is no longer public after the year 2019 year.

The statistics reflected above demonstrate that:

Formal green card abandonment significantly exceeds formal citizenship renunciations.

The population potentially affected by the expatriation rules is therefore much larger than many individuals around the world appreciate.

Lack of Control Over the Timing of Termination

One of the greatest risks for green card holders is that they often do not control the legal date on which their LPR status terminates, especially if they reside in a tax treaty country, per the analysis in the landmark case:

If abandonment is later determined by tax treaty law, effectively an CPB officer, the Executive Office for Immigration Review (EOIR) immigration court, the Board of Immigration Appeals (BIA)or a even a Federal District Court:

The taxpayer may not control the effective date of termination – “expatriation”.

If they are a “covered expatriate” or not.

The tax consequences may arise unexpectedly.

The timing can directly impact whether the tax expatriation rules apply and all of the potential consequences.

These timing issues become important when the IRS challenges tax positions taken on tax returns filed (or filed late) as was the case in Topsnik v. Commissioner (143 T.C. 240 (2014) – “Topsnik I”) and the subsequent case of Topsnik v. Commissioner (146 T.C. No. 1, 2016) – “Topsnik II”). In Topsnik II, Judge Kerrigan agreed with the IRS and ” . . . determined that P [taxpayer] was a “covered expatriate” who expatriated in 2010 and must recognize gain on the deemed sale of his installment obligation on the day before his expatriation under I.R.C. sec. 877A.” The U.S. Tax Court cited IRS Notice 2009-85 and explained it was not legally binding as follows:

We are not bound by Notice 2009-85, supra, see Compaq Computer Corp. v. Commissioner, 113 T.C. 363, 372 (1999), but it is an official statement of the Commissioner’s position and we may let it persuade us, see Nationalist Movement v. Commissioner, 102 T.C. 558, 583 (1994), aff’d, 37 F.3d 216 (5th Cir.1994).

The Tax Court went on to conclude these facts caused the court to conclude and uphold the IRS assessment of the “exit tax” on the German citizen Mr. Topsnik as a “covered expatriate” quoted as follows:

Notice 2009-85, sec. 8, 2009-45 I.R.B. at 611, explains that for purposes of certifying tax compliance for the five years before expatriation pursuant to section 877(a)(2)(C):

All U.S. citizens who relinquish their U.S. citizenship and all long-term residents who cease to be lawful permanent residents of the United States (within the meaning of section 7701(b)(6)) must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation. Individuals who fail to make such certification will be treated as covered expatriates within the meaning of section 877A(g) * * *

For the year of his expatriation petitioner failed to complete and file a Form 8854 certifying under penalties of perjury that he has complied with all of his U.S. Federal tax obligations for the five taxable years preceding the taxable year that includes his expatriation date. Respondent [IRS] has provided evidence that petitioner did not file all of his U.S. income tax returns before expatriatingand was not in payment compliance for taxes owed for the five years before expatriation in taxable year 2010. Thus petitioner could not have certified under penalties of perjury on a Form 8854 that he had been in tax compliance for the five years before expatriation. Consequently, because petitioner failed to certify tax compliance for the five years before expatriation, he is a “covered expatriate” as defined by section 877A(g)(1)(A).

Importantly, the court in Aroeste concluded IRS Form 8854 was not required to be filed (even though the DOJ attorney argued it was required – as set forth in the instructions to the form) as explained below:

C. Whether Aroeste Was Required to File Form 8854

The Government next argues that even if the IRS had accepted Aroeste’s amended

returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009- 85.(Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both

amended forms. (Id.)

Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply

with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley

Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under

the APA, agencies must follow a three-step procedure for “notice-and-comment”

rulemaking, but this requirement does not apply to “interpretive rules, general statements

of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In

Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found

that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure.

Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Both the Green Valley Investors LLC case and Mann Construction were 2022 cases, some 6 years after Topsnik II.

My law firm, Chamberlain Hrdlicka, successfully represented the taxpayers in Green Valley and of course in Aroeste.

Practical Lessons for Green Card Holders

The combined lessons from Aroeste, Topsnik I, and Topsnik II are significant.

Before Obtaining a Green Card

Individuals should understand:

The long-term resident rules and their U.S. tax obligations and reporting obligations;

The expatriation tax provisions and how they generally apply;

The “covered expatriate” tax regime and what steps to take;

The impact of income tax treaties with countries in the United States.

Before Formally Reporting the Abandonment (or Informally Abandoning) a Green Card

Individuals should carefully evaluate:

The date expatriation may occur;

Whether Form I-407 should be filed;

Tax compliance under U.S. tax laws (and what that means), including for the preceding five years to abandonment;

What notifications should be provided and when (not necessarily formal tax form filings);

Potential exit tax exposure – depending upon total assets, liabilities, type of assets and anticipated future income and gains;

Treaty residency positions and the particular facts of each case;

Reporting obligations, and which ones are mandatory or not – including IRS Forms 8833 and 8854.

Most Important Takeaway?

A green card holder does not necessarily need to spend seven or eight years physically living in the United States before becoming subject to the long-term resident and expatriation tax rules. The interaction of immigration law, tax law, treaty provisions, and reporting requirements can produce unexpected results. The recent landmark decision in Aroeste that I handled, confirms that these issues are not merely theoretical—they are increasingly becoming the subject of significant litigation and judicial scrutiny.

Part I of Part II: The Gold Card – “It’s like the green card, but better and more sophisticated.”

Will the “gold card” sell to ultra high net worth investors around the world who want U.S. citizenship (“USC”)? What are the tax costs of USC? * About the Author: Patrick W. Martin

President Trump again announced on April 3, aboard Air Force One his plan:

Whether the U.S. adopts a new “Gold Card” “For $5 million [that] we will allow the most successful job-creating people from all over the world to buy a path to U.S. citizenship,” is up to the U.S. government.

Congress can amend Title 8 and include a new “Gold Card” option.

Current law provides the EB-5 visa as one path towards a “green card” that ultimately can lead to U.S. citizenship through naturalization.

President Trump presented at his March 4th speech to a joint session of Congress, explaining the concept: “It’s like the green card, but better and more sophisticated. And these people will have to pay tax in our country.”

Sounds like a panacea to help the U.S. federal deficit problem? If 100,000 of these “Gold Cards” were sold for $5M each, and these funds were paid directly over to the federal government, that would raise $500 billion dollars. If 1 million were sold, that would be $5 trillion dollars to use to pay down the deficit (running annually at far greater than $1 trillion dollars since 2019).

To put that into perspective, the EB-5 visa that also leads to a “green card” that can further lead to U.S. citizenship through naturalization has an annual visa limit of about 10,000. See, USCIS’s article – (16 Aug 2024) – Annual Limit Reached in the EB-5 Unreserved Category There have been multiple years where the annual visa limit was not met. Prior to 2015, the 10,000 visa limit was never met and in several years there were less than 500 EB-5 visas issued annually.

There have been less than 150,000 EB-5 visas issued over the last 35 years since its adoption in 1990. Is it realistic to be able to “sell” even ten thousand $5M gold visas annually, when the “green EB-5 visa” costs $800,000 and has had less than 150,000 issued in nearly 35 years?

Equity Investment for EB-5 visa – $800,000 (Does NOT go to the Government)

The total required equity investment amount for an EB-5 visa in the qualifying project, is only $800,000 (if in a “TEA”). See, EB-5 Immigrant Investor Program, as published by the U.S. Citizenship and Immigration Services (USCIS). See, USCIS’s Chapter 2 – Immigrant Petition Eligibility Requirements. It used to be only $500,000 (1/10th of $5M). A TEA is a targeted employment area (“TEA”) that meets specific requirements under the law. If the capital investment is not in a TEA, the required minimal capital investment amount is $1,050,000 that increases in January 1, 2027 and each 5 years thereafter. Still about 1/5th the cost of a “gold visa”.

U.S. Estate and Gift Tax Consequences for U.S. Citizens and those with a Green Card (“Gold Card”?)

Finally, maybe the biggest impact on who wants an investor visa that leads to U.S. citizenship depends largely upon the U.S. income tax and U.S. estate and gift tax consequences. There are many tax implications. See, my case Aroeste v United States – Order Nov 2023, that was appealed to the 9th Circuit by the Office of Solicitor General (DOJ). U.S. District Court ruled in favor of green card holder.

These regulations are extensive and provide an explanation of the purpose of these rules.

II. Purpose of Foreign Gift and Trust Provisions

During the mid- to late-1990s, abusive tax schemes, including offshore schemes involving foreign trusts, reemerged in the United States after reaching their last peak in the 1980s. GAO, Efforts to Identify and Combat Abusive Tax Schemes Have increased, but challenges remain, GAO–02–733 (Washington, DC: May 22, 2002). In these schemes, foreign trusts were used to transfer large amounts of assets abroad, where it was much more difficult for the IRS to identify whether U.S. persons owned a trust.

interest in such trusts, and whether such persons were reporting and paying the required taxes on their income from such trusts. Many of the foreign trusts were established in tax haven jurisdictions with bank secrecy laws. Before the 1996 Act amended sections 6048 and 6677, there was no Form 3520-A), which was limited to five percent of the transfer or corpus of the trust, as applicable, not to exceed $1,000. In light of this, it was difficult for the IRS to obtain information about income earned by U.S.-owned foreign trusts and distributions to U.S. beneficiaries from foreign trusts, and Sections 6048 and 6677 were generally ineffective in ensuring that U.S. persons provided this information. information. The result was “rampant tax evasion.” 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan). Requirement for U.S. Persons to Report Distributions from Foreign Trusts and the Penalty for Failure to Report Transfers to a Foreign Trust or an Annual Foreign Trust Information Statement (in Federal Register/Vol. 89, No. 90/Wednesday, May 8 of 2024/Proposed Rules and 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan).

What Questions Need to be Asked if You Live (with a “green card”) in one of the 67 Countries – with a U.S. Income Tax Treaty?

Depending upon the factual circumstances of each individual, they may be able to benefit from the international tax treaty law articulated by the U.S. Federal District Court in Aroeste v United States – Order (Nov 2023). Future posts will explore the legal relevance of some of the following questions to consider:

Has the individual filed any U.S. federal income tax returns since leaving the United States?

Was a professional tax return preparer hired or consulted about the filing of a federal income tax return (e.g., a certified public accountant, an enrolled agent, a full time tax return preparer, ta tax attorney, etc.)?

Has the individual been filing IRS Form 1040 Resident Tax Returns in the same way Mr. Aroeste was filing – based upon the advice (that turned out to be erroneous -although given in good faith) from their U.S. tax return preparer?

What steps if any have been taken to notify the U.S. federal government (irrespective of the agency) regarding their physical residency outside the United States?

This information is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

Revocation or Denial of U.S. Passport: More on new section 7345 (Title 26/IRC) and USCs with “Seriously Delinquent Tax Debt”

New Section 7345 completely modifies how U.S. citizens (“USCs”) living and traveling around the world have to now consider very seriously actions taken by the Internal Revenue Service (“IRS”). It is the IRS which now holds the power under this new law that requires the U.S. Department of State (“DOS”) to revoke or deny to issue a U.S. passport in the first place.

New Section 7345(e) provides in relevant part as follows: “upon receiving a certification described in section 7345 of the Internal Revenue Code of 1986 from the Secretary of the Treasury, the Secretary of State shall not issue a passport to any individual who has a seriously delinquent tax debt described in such section. . . ” [emphasis added].

This new law mandates (not at the discretion of the DOS) that various U.S. passports be denied at the direction of the IRS. Once the IRS issues the certification of “seriously delinquent tax debt.”

All it takes, is for the IRS to claim tax or penalties are owing of at least US$50,000 through an assessment (plus start a lien or levy action).

Also, we have seen several IRS assessments of income tax (not just penalties) against individuals of hundreds of thousands of dollars which are not supported by the law. For instance, it is not uncommon for the IRS to issue a “substitute for return” alleging income taxes owing. See, How the IRS Can file a “Substitute for Return” for those USCs and LPRs Residing Overseas, posted Nov. 8, 2015. We have a number of those cases pending, where the IRS has taken erroneous information and made such assessments against USCs residing and working outside the U.S. for much if not most of their professional lives.

New Section 7345 requires that USCs, wherever they might reside, take great care in knowing about any actions the IRS might be taking against them; as to tax and penalty assessments, whether or not they are supported under the law.

Denial of U.S. Passports: President Obama and Congress Pass Law that will Require Department of State to Deny a U.S. Passport for a “Seriously Delinquent Taxpayer”

Entry in and out of the U.S. has just gotten more problematic under a new law for those U.S. citizens who the IRS asserts owes taxes. A new statutory concept has been added to the tax law called “seriously delinquent tax debt”; which is defined by new IRC Section 7345 as a tax that has been assessed, is greater than US$50,000, and where a notice of lien has been filed or levy made.

The administration of passports is the responsibility of the Department of State. [“Passport Act of 1926,” 22 U.S.C. sec. 211a et seq.] The Secretary of State may refuse to issue or renew a passport if the applicant owes child support in excess of $2,500 or owes certain types of Federal debts. The scope of this authority does not extend to rejection or revocation of a passport on the basis of delinquent Federal taxes. Although issuance of a passport does not require a social security number or taxpayer identification number (“TIN”), the applicant is required under the Code to provide such number. Failure to provide a TIN is reported by the State Department to the Internal Revenue Service (“IRS”) and may result in a $500 fine.

***

Senate Amendment

Under the Senate Amendment, the Secretary of State is required to deny a passport (or renewal

of a passport) to a seriously delinquent taxpayer and is permitted to revoke any passport

previously issued to such person. In addition to the revocation or denial of passports to delinquent taxpayers, the Secretary of State is authorized to deny an application for a passport if the applicant fails to provide a social security number or provides an incorrect or invalid social security number. With respect to an incorrect or invalid number, the inclusion of an erroneous number is a basis for rejection of the application only if the erroneous number was provided willfully, intentionally, recklessly or negligently. Exceptions to these rules are permitted for emergency or humanitarian circumstances, including the issuance of a passport for short-term use to return to the United States by the delinquent taxpayer.

The provision authorizes limited sharing of information between the Secretary of State and

Secretary of the Treasury. If the Commissioner of Internal Revenue certifies to the Secretary of

the Treasury the identity of persons who have seriously delinquent Federal tax debts as defined

in this provision, the Secretary of the Treasury or his delegate is authorized to transmit such

certification to the Secretary of State for use in determining whether to issue, renew, or revoke a

passport. Applicants whose names are included on the certifications provided to the Secretary of

State are ineligible for a passport. The Secretary of State and Secretary of the Treasury are held

harmless with respect to any certification issued pursuant to this provision.

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this