Tax

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part II of VI

We ended the last post (I of VI) on this topic by referencing a crucial article I authored and published more than a decade ago in the International Tax Journal– titled Oops.. .Did I Expatriate and Never Know It – (2014)

- Key Background on LPRs and “Oops . . . Did I Expatriate”?

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below.

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below.

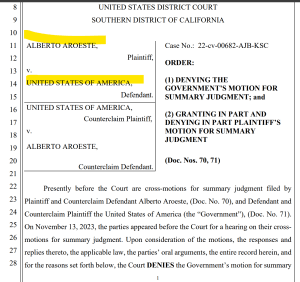

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

- Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Please read an earlier post from yours truly (About the Author: Patrick W. Martin), more than a decade ago –“Covered Expatriate” Status is a “Scarlet Letter”— which discusses the severe and often misunderstood consequences of covered expatriate status.

In addition, see another earlier post I authored explaining why covered expatriate status matters even for individuals with modest or limited assets: Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

- Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroeste decision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

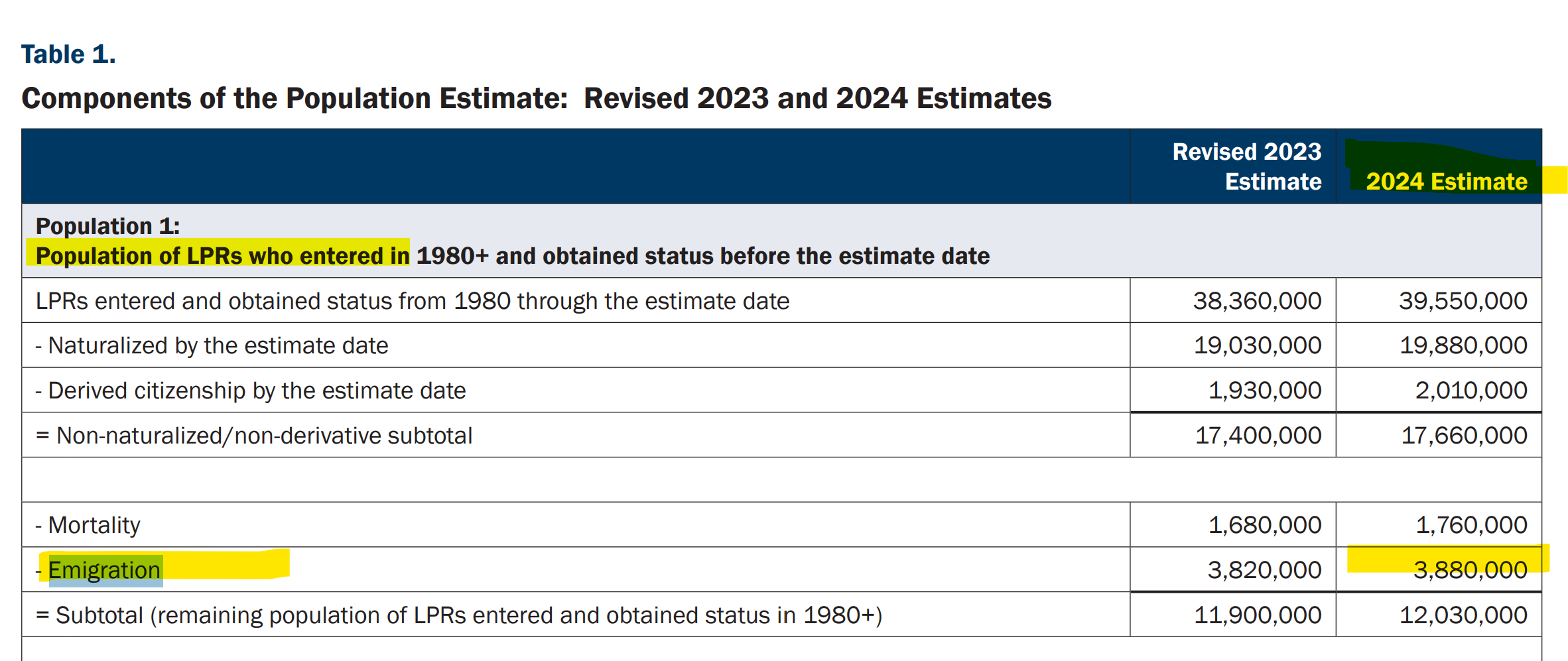

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023; see Table 1 in the report.

In order to understand what issues anyone with a green card has (especially when living outside the U.S.), some key questions should be asked:

- Gifts and inheritances after I leave (what U.S. taxes)

-

- If I become a covered expatriate, can I still give money to my children who live in the U.S. without U.S. taxes?

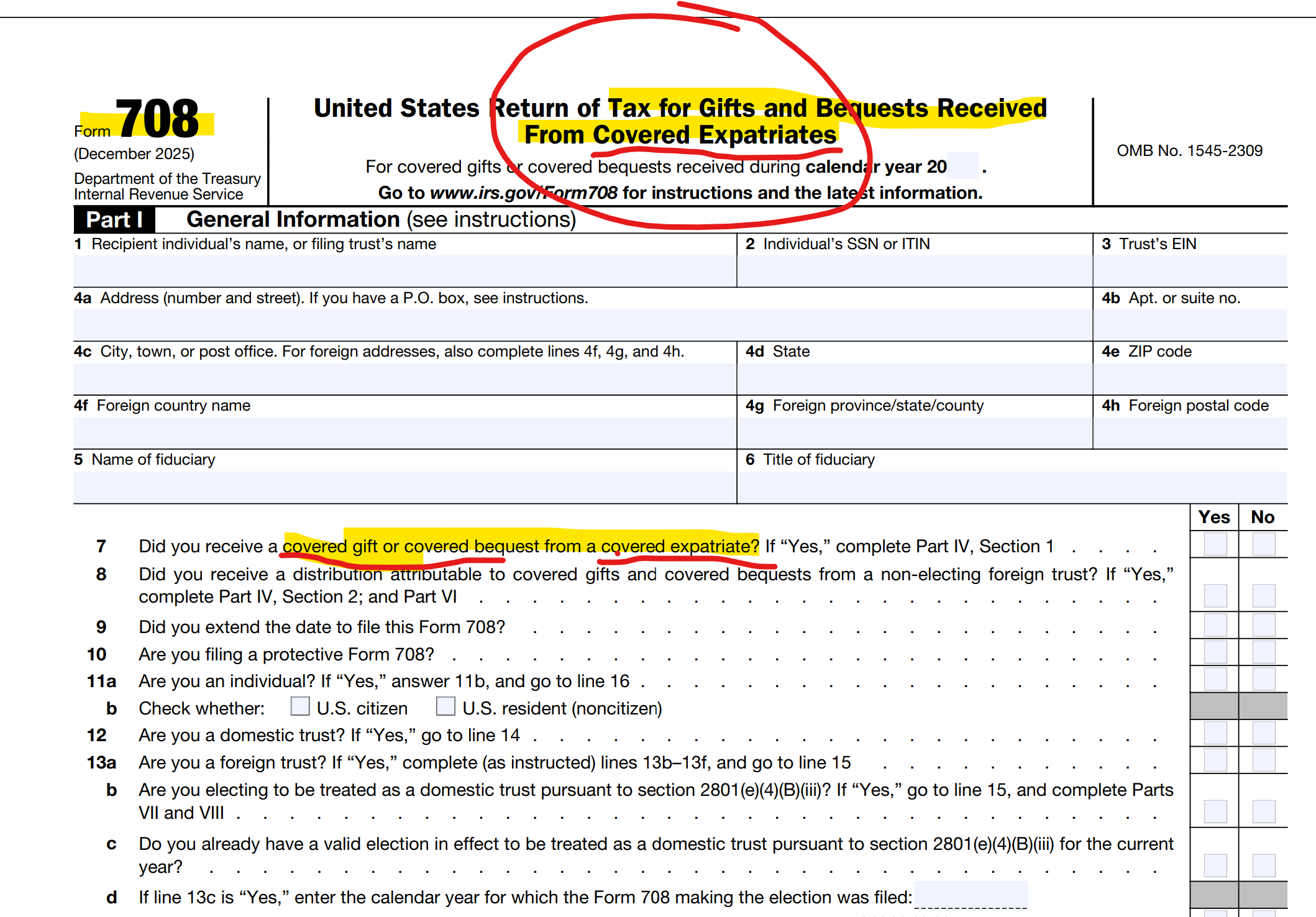

- When do I or my family members need to File IRS Form 708, United States Return of Tax for Gifts and Bequests Received From Covered Expatriates

- Worldwide income while I still have the green card

-

- Does the U.S. tax the salary I earn in my home country?

-

- What is the foreign earned income exclusion, and do I qualify?

- Must I file an IRS Form 8854, Initial and Annual Expatriation Statement

(and what are the legal implications of such filings)? - What if I do not file IRS Form 8854, Initial and Annual Expatriation Statement?

- Am I still a U.S. taxpayer?

-

- If I never told USCIS I left, does the IRS still consider me a U.S. tax resident?

-

- Can I be a U.S. tax resident and a tax resident of my home country at the same time?

-

- What is a “tax treaty tie-breaker” and how does it help or hurt me?

- Aroeste v. United States — what does it mean for me? –

- Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)

-

- If I use the treaty to be a non-resident, am I giving up my green card automatically?

-

- Can I be a non-resident for income tax under the treaty but still be considered a “U.S. person” for other rules like FBAR?

- Do all forms I file with the U.S. federal government (IRS, USCIS, ICE and others) subject me to claims of signing under penalty of perjury?

Stay tuned . . . . . . . . . for III of VI

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023; see Table 1 in the report.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

See an early related post titled –How Many LPRs are Living in Tax Treaty Countries like Aroeste (Now including Chile)? What are the Legal-Tax Consequences? (Part I of II)

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

- Am I still a U.S. taxpayer?

-

- What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

-

- I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

-

- The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

-

- Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

-

- Is there a difference between “giving up” my green card and just letting it lapse?

- Is there a difference between “giving up” my green card and just letting it lapse?

- Aroeste v. United States — what does it mean for me? –

- Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)

-

- What was the Aroeste case actually about?

-

- Why is Aroeste important if I’m a green card holder living abroad?

-

- Why did the U.S. federal government fight so hard against Mr. Aroeste and appeal/litigate the case to the 9th Circuit, (and ultimately give up)?

- FBAR and foreign account reporting

-

- What is an FBAR, and why do I have to tell the U.S. about a bank account in my own country?

-

- What is FATCA, and why is my local bank asking if I’m “American” – or if I ever had a green card?

-

- What is Form 8938, and how is it different from FBAR?

- What is Form 8938, and how is it different from FBAR?

-

- What about accounts I only sign on, like my parents’ or my employer’s?

- The exit tax / expatriation rules

-

- What is the “exit tax” I keep hearing about?

-

- Am I a “long-term resident” — and why does that label matter so much?

-

- What is a “covered expatriate,” and how do I know if I am one?

-

- What did the Court in Aroeste rule about the “exit tax” and IRS Form 8854 – Initial and Annual Expatriation Statement?

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Stay tuned . . . . . . . . .

Did USCs Born in the U.S. lately (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

The United States has respected citizenship for those born on U.S. soil, since the U.S. Supreme Court ruled on the issue back in 1898 in United States v. Wong Kim Ark. We know that notwithstanding stare decisis, SCOTUS sometimes overturns its prior precedent. See, Loper Bright Enterprises v. Raimondo (2024) overturning Chevron U.S.A. Inc. v. Natural Resources Defense Council (1984); Dobbs v. Jackson Women’s Health Organization (2022), overturing Roe v. Wade (1973); and Brown v. Board of Education (1954) overturning Plessy v. Ferguson (1896).

- President’s Executive Order 14160: Titled, Protecting the Meaning and Value of American Citizenship

It provides in relevant part:

Sec. 2. Policy. (a) It is the policy of the United States that no department or agency of the United States government shall issue documents recognizing United States citizenship, or accept documents issued by State, local, or other governments or authorities purporting to recognize United States citizenship, to persons: (1) when that person’s mother was unlawfully present in the United States and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth, or (2) when that person’s mother’s presence in the United States was lawful but temporary, and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth.

(b) Subsection (a) of this section shall apply only to persons who are born within the United States after 30 days from the date of this order.

- SCOTUS Announced it Will Hear Arguments on May 15, 2025

See, SCOTUS order – here, and repo rted here: Birthright citizenship cases to be heard at the Supreme Court in May

rted here: Birthright citizenship cases to be heard at the Supreme Court in May

The Congressional Research Service has an excellent summary article it prepared in 2018, titled – The Citizenship Clause and “Birthright Citizenship”: A Brief Legal Overview (1 Nov. 2018). This report was drafted when President Trump during his first term questioned the validity of “birthright citizenship”. Below is an excerpt from that 2018 article, relevant to the:

Under federal law, nearly all people born in the United States become citizens at birth. This rule is known as “birthright citizenship,” and it derives from both the Constitution and complementary statutes and regulations. The Citizenship Clause of the Fourteenth Amendment states that “[a]ll persons born or naturalized in the United States, and subject to the jurisdiction thereof, are citizens of the United States and of the State wherein they reside.” The Immigration and Nationality Act (INA), in turn, declares certain persons to be U.S. citizens and nationals at birth. INA § 301(a) more or less tracks the Citizenship Clause in stating that “a person born in the United States, and subject to the jurisdiction thereof” is a “national[] and citizen[] of the United States at birth.” (The INA also extends citizenship at birth to various persons not protected by the Citizenship Clause, such as those born abroad to some U.S. citizen parents.) Federal regulations—including those that govern the issuance of passports and access to certain benefits—implement the INA by providing that a person is a U.S. citizen if he or she was born in the United States, so long as the parent was not a “foreign diplomatic officer” at the time of the birth.

persons not protected by the Citizenship Clause, such as those born abroad to some U.S. citizen parents.) Federal regulations—including those that govern the issuance of passports and access to certain benefits—implement the INA by providing that a person is a U.S. citizen if he or she was born in the United States, so long as the parent was not a “foreign diplomatic officer” at the time of the birth.

The report goes on to explain –

The weight of current legal authority suggests that these executive and legislative proposals to restrict birthright citizenship would contravene the Citizenship Clause. At least since the Supreme Court’s decision in the 1898 case United States v. Wong Kim Ark, the prevailing view has been that all persons born in the United States are constitutionally guaranteed citizenship at birth unless their parents are us born individuals foreign diplomats, members of occupying foreign forces, or members of Indian tribes. In Wong Kim Ark, the Court held that a man born in the United States in 1873 to parents who were Chinese nationals acquired citizenship at birth under the Fourteenth Amendment. The parents were ineligible to naturalize under the law of the time, but they had established “permanent domicile and residence in the United States.” The Court reasoned that the Citizenship Clause should be “interpret[ed] in light of the common law” and grounded its holding in the common law principle of jus soli or “right of the![]() soil.” Pursuant to that principle, “every child born in England of alien parents was a natural-born subject, unless the child of an ambassador or other diplomatic agent of a foreign state, or of an alien enemy in hostile occupation of the place where the child was born.”

soil.” Pursuant to that principle, “every child born in England of alien parents was a natural-born subject, unless the child of an ambassador or other diplomatic agent of a foreign state, or of an alien enemy in hostile occupation of the place where the child was born.”

- Tax Expatriation Consequences –

As to “tax expatriation” – of these individuals? I suspect these babies (i.e., those born after 30 days from the executive order; on or after February 19, 2025) will have bigger issues to worry about other than their U.S. tax issues if SCOTUS rules against them.

Did USCs Born in the U.S. (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

Part I of Part II: The Gold Card – “It’s like the green card, but better and more sophisticated.”

Will the “gold card” sell to ultra high net worth investors around the world who want U.S. citizenship (“USC”)? What are the tax costs of USC? * About the Author: Patrick W. Martin

President Trump again announced on April 3, aboard Air Force One his plan:

See, the New York Post – Trump unveils $5 million ‘gold card’ for rich migrants emblazoned with his image

Whether the U.S. adopts a new “Gold Card” “For $5 million [that] we will allow the most successful job-creating people from all over the world to buy a path to U.S. citizenship,” is up to the U.S. government.

* Congressional Powers: Article I, Section 1, and Article I, Section 8 of the U.S. Constitution.

Congress can amend Title 8 and include a new “Gold Card” option.

Current law provides the EB-5 visa as one path towards a “green card” that ultimately can lead to U.S. citizenship through naturalization.

President Trump presented at his March 4th speech to a joint session of Congress, explaining the concept: “It’s like the green card, but better and more sophisticated. And these people will have to pay tax in our country.”

* Reducing the Deficit: $1.31 trillion more than Gov’t has collected in fiscal year (FY) 2025

Sounds like a panacea to help the U.S. federal deficit problem? If 100,000 of these “Gold Cards” were sold for $5M each, and these funds were paid directly over to the federal government, that would raise $500 billion dollars. If 1 million were sold, that would be $5 trillion dollars to use to pay down the deficit (running annually at far greater than $1 trillion dollars since 2019).

To put that into perspective, the EB-5 visa that also leads to a “green card” that can further lead to U.S. citizenship through naturalization has an annual visa limit of about 10,000. See, USCIS’s article – (16 Aug 2024) – Annual Limit Reached in the EB-5 Unreserved Category There have been multiple years where the annual visa limit was not met. Prior to 2015, the 10,000 visa limit was never met and in several years there were less than 500 EB-5 visas issued annually.

- EB-5 visa – Leading to a Green Card

There have been less than 150,000 EB-5 visas issued over the last 35 years since its adoption in 1990. Is it realistic to be able to “sell” even ten thousand $5M gold visas annually, when the “green EB-5 visa” costs $800,000 and has had less than 150,000 issued in nearly 35 years?

Plus, see the U.S. Department of State’s Immigrant Visa Statistics, including the – Annual Numerical Limits for Fiscal Year 2025 for more details about the EB-5 visa program statistics.

-

- Equity Investment for EB-5 visa – $800,000 (Does NOT go to the Government)

The total required equity investment amount for an EB-5 visa in the qualifying project, is only $800,000 (if in a “TEA”). See, EB-5 Immigrant Investor Program, as published by the U.S. Citizenship and Immigration Services (USCIS). See, USCIS’s Chapter 2 – Immigrant Petition Eligibility Requirements. It used to be only $500,000 (1/10th of $5M). A TEA is a targeted employment area (“TEA”) that meets specific requirements under the law. If the capital investment is not in a TEA, the required minimal capital investment amount is $1,050,000 that increases in January 1, 2027 and each 5 years thereafter. Still about 1/5th the cost of a “gold visa”.

- U.S. Estate and Gift Tax Consequences for U.S. Citizens and those with a Green Card (“Gold Card”?)

Finally, maybe the biggest impact on who wants an investor visa that leads to U.S. citizenship depends largely upon the U.S. income tax and U.S. estate and gift tax consequences. There are many tax implications. See, my case Aroeste v United States – Order Nov 2023, that was appealed to the 9th Circuit by the Office of Solicitor General (DOJ). U.S. District Court ruled in favor of green card holder.

Ultra high net worth individuals around the world want to know the tax costs of U.S. citizenship. Importantly, new regulations were issued in January 2025 regarding the tax consequences of  renouncing USC and triggering the U.S. “expatriation tax” that is the primary focus of these materials. See, these regulations – here: Guidance Under Section 2801 Regarding the Imposition of Tax on Certain Gifts and Bequests From Covered Expatriates

renouncing USC and triggering the U.S. “expatriation tax” that is the primary focus of these materials. See, these regulations – here: Guidance Under Section 2801 Regarding the Imposition of Tax on Certain Gifts and Bequests From Covered Expatriates

These tax consequences of the “gold visa” will be explored in more detail in Part II.

For a more detailed discussion of tax issues tied to pre-immigration to the U.S., see my chapter of the tax implications of immigration to the U.S. (as opposed to emigration from it). I wrote the tax chapter in the latest edition of the American Immigration Lawyers Association (“AILA’s) – Immigration Options for Investors & Entrepreneurs (out of print) titled Key U.S. Tax Considerations for Investor Visa Applicants by Patrick W. Martin.

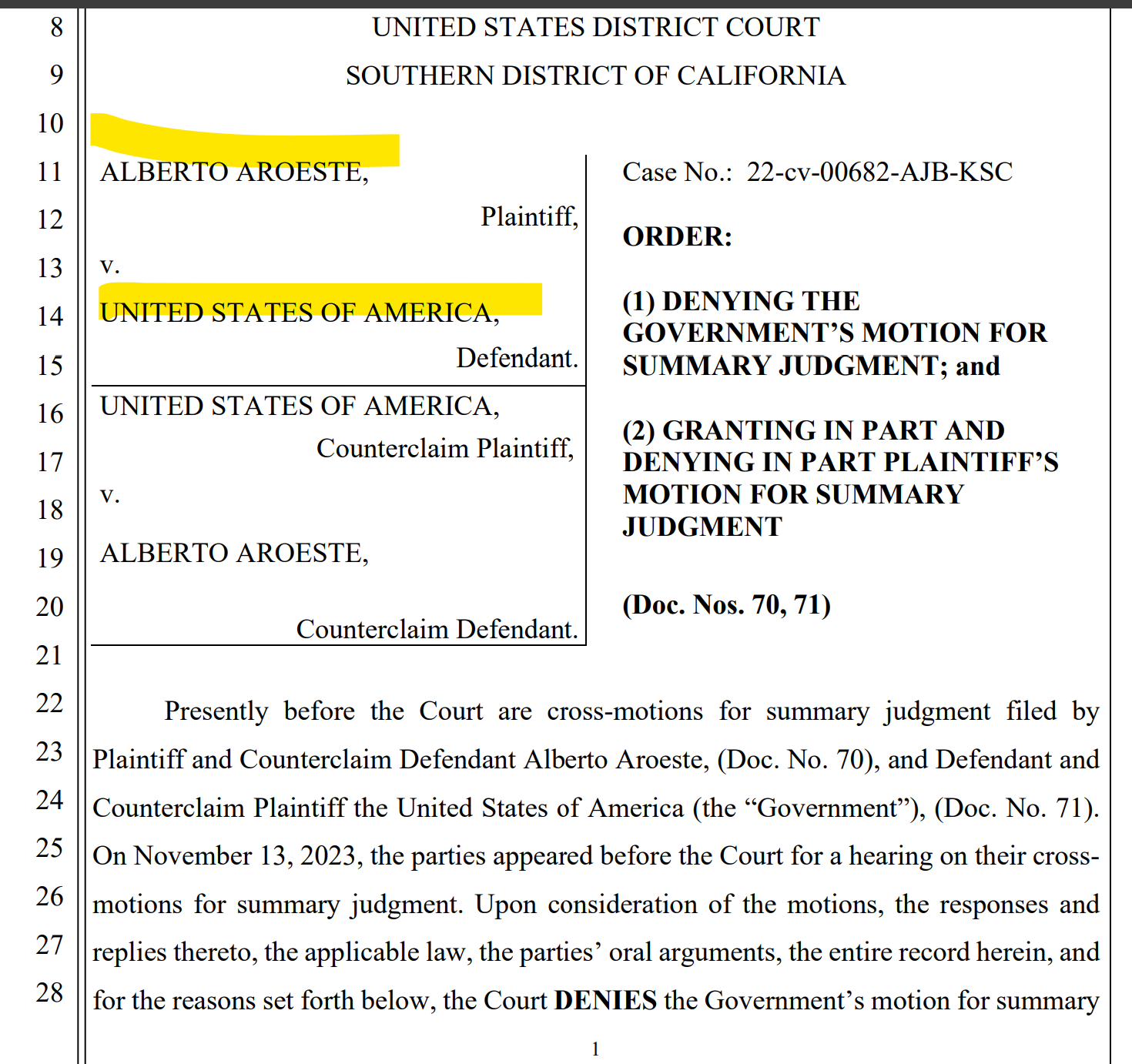

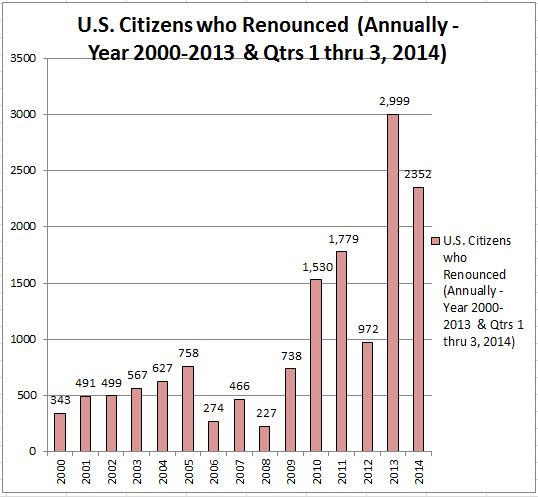

The 2014 Third Quarter Renunciations Is probably the New Norm –

The Treasury Department announced 776 renunciations, which brings the 2014 total to 2,353, on track to match last year’s record breaking 2,999 citizens who renounced.

US Citizen Renunciations  Q1 thru Q3 – 2014

Q1 thru Q3 – 2014

See, Will Qtr 2 Exceed Qtr 1 – 2014, Record of USC Renunciations?

As has been mentioned previously, this list does not include lawful permanent residents who have terminated their LPR status for purposes of these tax law provisions. For further reading on LPRs, see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Maybe the LPR list represents several hundred thousands of individuals? The current total estimated number of LPRs is 13.3 million for the year 2012 as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012

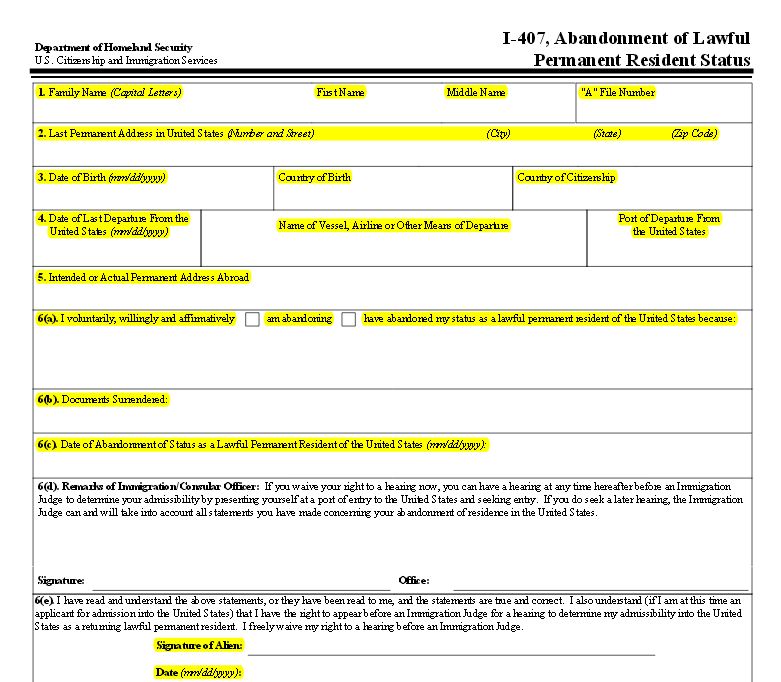

There are two distinct ways that LPRs can terminate their tax residency status. First, through the formal immigration law process typically involving filing Form I-407. See, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Second, they can terminate their LPR status, for tax purposes, by merely meeting the statutory  requirements of IRC Section 7701(b)(6). This simply requires the individual to move from the U.S. and live in a country with a U.S. income tax treaty and meet the other two statutory requirements.

requirements of IRC Section 7701(b)(6). This simply requires the individual to move from the U.S. and live in a country with a U.S. income tax treaty and meet the other two statutory requirements.

This statutory language has three tests for when the individual is no longer a LPR for federal tax purposes:

- The individual is treated as a resident of a foreign country under the provisions of a tax treaty;

- The individual does not waive the benefits of the treaty, and

- Notifies the Secretary of the commencement of such treatment.

Global Entry, SENTRI and NEXUS after Renouncing – the “Trusted Traveler Programs” – SAFE TRAVELS!

The U.S. federal government has made the life of world travelers much simpler over the last few years, for those who have signed up and participate in one of the “trusted traveler programs.“

Entry into the U.S. through customs and immigration checkpoints is fast tracked and explained in more detail below.

Also, a related program that provides much convenience to travelers is the Pre-TSA. This is a program described on the government website as –

What does TSA Pre?™ mean for travelers?

TSA Pre?™ Experience:

|

No Removal of:

|

Obtaining approval for Pre-TSA. is facilitated if an individual has already been approved for one of the “trusted traveler programs.”

You can typically avoid long lines of travelers who do not have such clearances and it provides a more convenient way of traveling in and out of the U.S.

However, once a USC renounces, they can no longer travel on their previous status as a USC under a “trusted traveler program” where they previously applied and represented they are a USC.

Once a person ceases to be a USC, they can no longer represent themselves to be a citizen. Indeed, there is a specific statutory provision that holds that any person falsely claiming citizenship can be found to be inadmissible for entry into the U.S. 8 U.S. Code § 1182 – Inadmissible aliens

Accordingly, you should not continue to travel on your existing/old “trusted traveler program” documents. You will need to re-apply as a non-USC. More details on the Global Entry program are provided below from the government’s own website –

Global Entry

What is Global Entry?

Global Entry is a U.S. Customs and Border Protection (CBP) program that allows expedited clearance for pre-approved, low-risk travelers upon arrival in the United States.

How Does the Global Entry Program Work?

Global Entry is a U.S. Customs and Border Protection (CBP) program that allows expedited clearance for pre-approved, low-risk travelers upon arrival in the United States. Though intended for frequent international travelers, there is no minimum number of trips necessary to qualify for the program. Participants may enter the United States by using automated kiosks located at select airports.

At airports, program participants proceed to Global Entry kiosks, present their machine-readable passport or U.S. permanent resident card, place their fingertips on the scanner for fingerprint verification, and make a customs declaration. The kiosk issues the traveler a transaction receipt and directs the traveler to baggage claim and the exit.

Travelers must be pre-approved for the Global Entry program. All applicants undergo a rigorous background check and interview before enrollment.

SAFE TRAVELS!

How does the basic premiss that there are ‘Unpaid Taxes on Billions in Hidden Offshore Accounts'” hurt the average U.S. citizen taxpayer living overseas?

Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

Permanent Subcommittee on Investigations

Location: Dirksen Senate Office Building

Agenda

The Permanent Subcommittee on Investigations will hold a hearing, “Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts,” on Wednesday, February 26, 2014, at 9:30 a.m., in Room G-50 of the Dirksen Senate Office Building.

The hearing will continue the Subcommittee’s examination of tax haven bank facilitation of U.S. tax evasion, focusing on the status of efforts to hold Swiss banks and their U.S. clients accountable for unpaid taxes on billions of dollars in hidden assets. Witnesses will include representatives from a Swiss bank and the U.S. Department of Justice. A witness list will be available Monday, February 24, 2014.

Do some former U.S. citizens now consider this a “badge of honor” to have renounced their U.S. citizenship?

A record number of U.S. citizenship renunciations in 2013, some 3,000, begs the question: “Why are so many U.S. citizens renouncing?”

???????????????? ?Please click here to view the above in Chinese.?

Wow, the number of 2,999 U.S. citizens who renounced in the year 2013 shattered the prior record set in 2011 of 1,782 renunciations. Why so many renunciations?

The U.S. Treasury Department released the number of U.S. citizens who renounced for 2013. The Federal Registry reported some 631 U.S. citizens who renounced for the quarter; for a total of 2,999 former citizens for the entire year of 2013.

Click here for complete details of the registry

See also more information in this blog under the “Government Resources” section for more details.

???????????????? ?Please click here to view the above in Chinese.?

Is the Senate Finance “Punting” on reforming international tax rules for U.S. citizens living overseas?

Summary of Staff Discussion Draft: International Business Tax Reform

Chairman Max Baucus

U.S. Senate Committee on Finance

11/19/13

“The staff discussion draft does not address the international tax rules addressing individuals, whether for U.S. citizens living overseas or foreign nationals moving to the United States. The Chairman’s staff is considering reforms to simplify the rules in this area while appropriately taxing such individuals. Comments are requested regarding the scope and mechanics of reforms in this area.”

???????????????? ?Please click here to view the above in Chinese.?