FATCA – Chapter 4

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

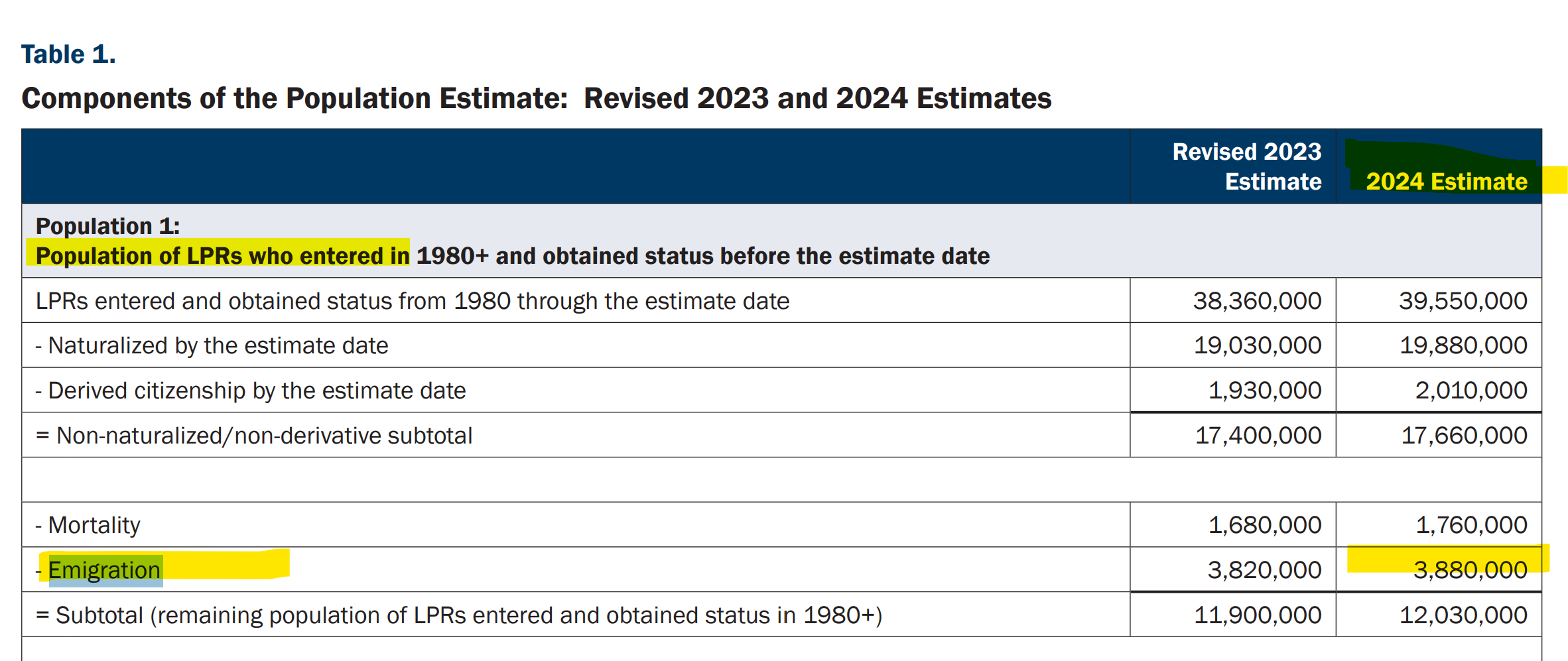

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023; see Table 1 in the report.

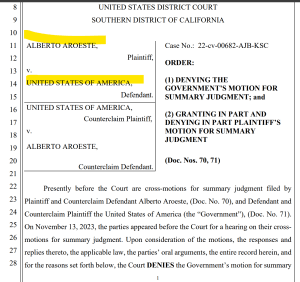

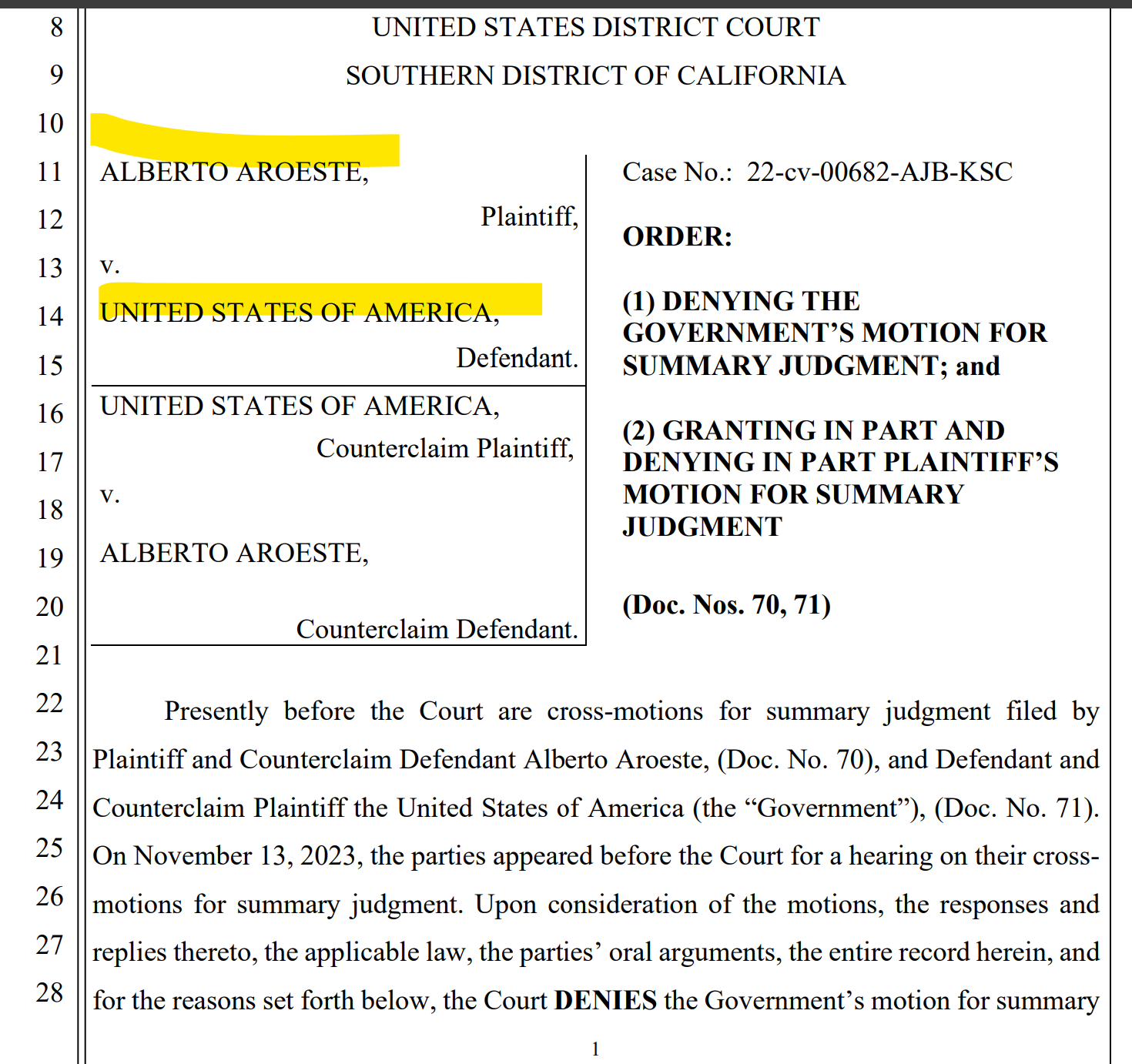

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

See an early related post titled –How Many LPRs are Living in Tax Treaty Countries like Aroeste (Now including Chile)? What are the Legal-Tax Consequences? (Part I of II)

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

- Am I still a U.S. taxpayer?

-

- What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

-

- I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

-

- The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

-

- Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

-

- Is there a difference between “giving up” my green card and just letting it lapse?

- Is there a difference between “giving up” my green card and just letting it lapse?

- Aroeste v. United States — what does it mean for me? –

- Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)

-

- What was the Aroeste case actually about?

-

- Why is Aroeste important if I’m a green card holder living abroad?

-

- Why did the U.S. federal government fight so hard against Mr. Aroeste and appeal/litigate the case to the 9th Circuit, (and ultimately give up)?

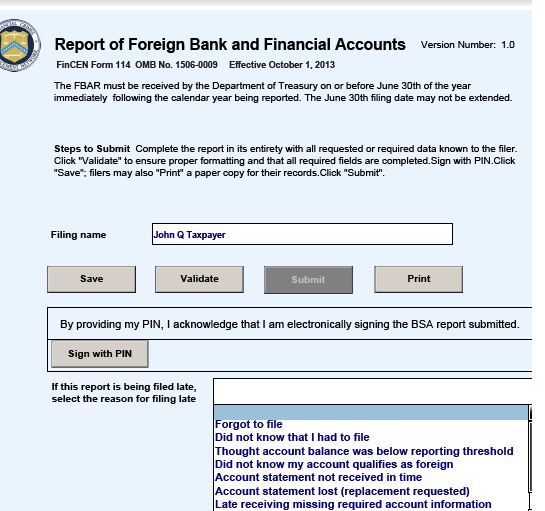

- FBAR and foreign account reporting

-

- What is an FBAR, and why do I have to tell the U.S. about a bank account in my own country?

-

- What is FATCA, and why is my local bank asking if I’m “American” – or if I ever had a green card?

-

- What is Form 8938, and how is it different from FBAR?

- What is Form 8938, and how is it different from FBAR?

-

- What about accounts I only sign on, like my parents’ or my employer’s?

- The exit tax / expatriation rules

-

- What is the “exit tax” I keep hearing about?

-

- Am I a “long-term resident” — and why does that label matter so much?

-

- What is a “covered expatriate,” and how do I know if I am one?

-

- What did the Court in Aroeste rule about the “exit tax” and IRS Form 8854 – Initial and Annual Expatriation Statement?

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Stay tuned . . . . . . . . .

Quaint?: U.S. Treasury 1998 Report: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues (Part I of Part II)

This is a classic report that now reads quaintly.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties in United States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

More comments to come – in Part II.

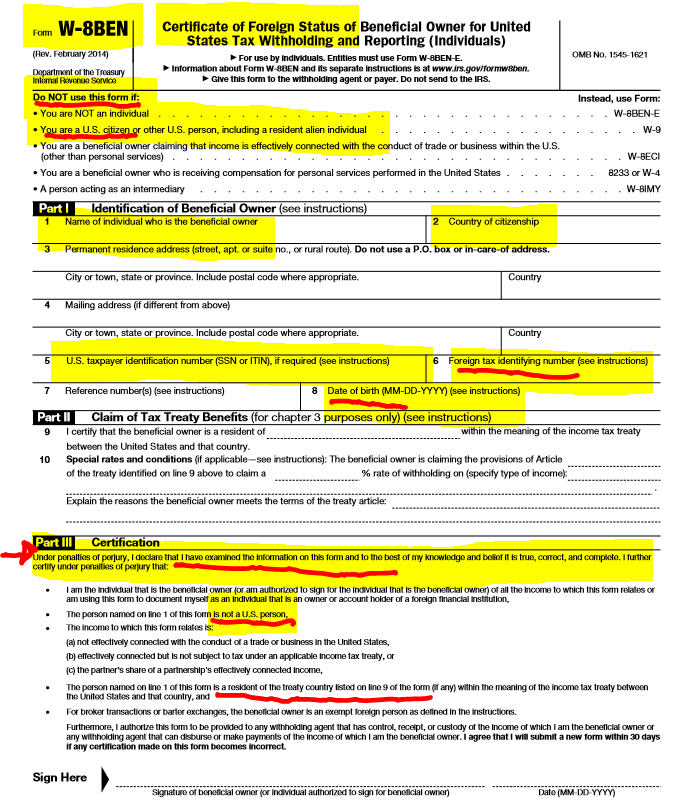

IRS Form W-8 or W-9? “Green Card” Holders (LPRs) – Certifications Re: Tax Status after Aroeste v. United States

The author has extensively discussed the appropriate IRS Form for individuals to sign under penalties of perjury when dealing with their banks and third parties, irrespective of the banks’ location. The choice between IRS Forms W-8 and W-9 hinges on the U.S. income tax residency status of the individual. Forms W-8 and W-9 serve the purpose of conveying the tax residency status of the individual to third parties. The correct (or incorrect form) can have a range of different tax and legal consequences to the individual. A non-resident is generally not subject to income taxation in the United States, except for on limited types of income. In contrast, a resident (for federal income tax purposes) is subject to taxation on their worldwide income. If an income tax resident of the United States falsely certifies their status using Form W-8, severe adverse legal consequences can follow. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

- IRS Forms W-8 or W-9 (or Other)?

For U.S. citizens, the process is straightforward—they must sign IRS Form W-9. However, for individuals without U.S. citizenship, the situation becomes more intricate. The following posts delve into critical legal considerations surrounding IRS Form W-8BEN.

See, IRS Releases New IRS Form W8-BEN. * U.S. citizens and LPRs beware of completing such form at the request of a third party (2014/2015)

Also, W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

These comments provide in-depth insights into the legal consequences of filing and signing specific IRS forms (or their equivalents produced by financial institutions: W-8 vs. W-9). Notably, UBS’s explanation titled “UBS One Source Understanding tax forms—non U.S. taxpayers” sheds light on the efforts foreign financial institutions need to dedicate to assist clients who are not “United States persons” for federal tax purposes, ensuring compliance with U.S. federal tax laws.

- Green Card Holders Living Abroad Have Further Analysis to Consider

The complexity heightens for “Green Card” holders living abroad, especially those residing in countries covered by an income tax treaty with the United States. See, Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. Aroeste v United States – Order Nov 2023, emphasizes a 5-step analysis for Green Card holders who have not formally abandoned their status. The ultimate test is whether the individual is entitled to be treated as a resident of a foreign country under a tax treaty.

- Aroeste v. United States: Decision’s Impact on LPR Individuals

The decision could potentially affect millions of Green Card holders living outside the U.S. Aroeste Court’s 5-step analysis becomes crucial for the 3+ million LPRs residing abroad, determining whether they qualify as “United States persons” under the law.

- LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in 2023 as of 2014. The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

- Importance of Figuring Out your Residency Status if you Never Formally Abandoned your Green Card and Live in an Income Tax Treaty Country.

The impact of the Aroeste v United States decision presents a dual scenario for individuals who have not formally abandoned their “lawful permanent residency” status. On the positive side, there is an opportunity to inform the Internal Revenue Service (IRS) of their non-resident status by utilizing the applicable income tax treaty. There are specific steps to take as explained by the Court in Aroeste vs. United States. This action can relieve them of U.S. federal income tax filing obligations and Foreign Bank Account Report (FBAR) filing requirements, helping to steer clear of potential penalties and taxes that might otherwise be owed. The Court in Aroeste concluded such late filings could subject the individual ” . . . to penalties pursuant to I.R.C. § 6712(a) equal to $1,000 per failure to timely report his Treaty position. . . “

Aroeste v United States – Order Nov 2023Download

- Potential Downside for “LPRs” Living in an Income Tax Treaty Country.

However, on the flip side, this termination of U.S. income tax residency status may lead to the individual “cease[ing] to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)).” Such a shift can trigger adverse U.S. tax consequences, affecting not only the individual but also extending to children, spouses, family members, and friends who could receive “covered gifts” or “covered bequests.” This classification may result in the individual being deemed a “covered expatriate” under the expatriation tax law, as outlined in IRC 877A(g)(3). See, IRC 877A(g)(3). Potentially severe adverse tax consequences can follow from this edge of the sword. The Court in Aroeste vs. United States did not address these adverse tax consequences as they were not at issue.

See, Patrick W. Martin, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Important resources for United States international tax rules for those considering renouncing or relinquishing United States citizenship or abandoning lawful permanent residency

This Blog is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Blog.

Although the author has taken great care to make sure that the information contained herein is accurate and useful, it is necessary that you consult an experienced attorney to address any particular situation. Most importantly, if you are contemplating renouncing (or proving relinquishment) of U.S. citizenship or formally abandoning your LPR status, you must get legal advice. This is a very important decision with a range of complex legal consequences.

W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks

Individuals who do not specialize in U.S. federal tax law, often have little detailed understanding of the U.S. federal “Chapter 3” (long-standing law regarding withholding taxes on non-resident aliens and foreign corporations and foreign trusts) and “Chapter 4” (the relatively new withholding tax regime known as the “Foreign Account Tax  Compliance Act”) rules.

Compliance Act”) rules.

Indeed, plenty of U.S. tax law professionals (CPAs, tax attorneys and enrolled agents) do not understand well the interplay between these two different withholding regimes –

- 26 U.S. Code Chapter 3 – WITHHOLDING OF TAX ON NONRESIDENT ALIENS AND FOREIGN CORPORATIONS

- 26 U.S. Code Chapter 4 – TAXES TO ENFORCE REPORTING ON CERTAIN FOREIGN ACCOUNTS

Plus, the IRS forms have been significantly modified over the years; with increasing factual representations that must be made by individuals who sign the forms under penalty of perjury. They are complex and not well understood. For instance, the older 2006 IRS Form W-8BEN for companies was one page in length and required relatively little information be provided.

The entire form is reproduced here; indicating how foreign taxpayer information was optional and generally there was no requirement to obtain a U.S. taxpayer identification number. It was governed exclusively by Chapter 3 and the regulations that had been  extensively produced back in the early 2000s.

extensively produced back in the early 2000s.

The forms were even easier before those regulations (see old IRS Form 1001). No taxpayer identification numbers were ever required and virtually no supporting information regarding reduced tax treaty rates on U.S. sources of income.

Life was simple back then – compared to today!

The one thing all of these forms have in common is that all information was provided and certified under penalty of perjury. Current day IRS Forms W-8s can typically be completed accurately by experts who understand the complex web of rules. Plus, multiple versions of W-8s exist today; most running some 8+ pages in length.

See the potpourri of current day W-8 forms –

Making certifications under penalty of perjury are more complex, the more and more factual information that is being certified. If I certify the dog I see in front of me is “white and black” that is not a complex certification, if I see the dog and see the “white and black”. If the dog also has some brown coloring, my certification would necessarily not be false.

However, if I have to certify as to the colors of each dog in a pack of 8 dogs (and each and every color that each dog is/was), that becomes a much more complicated certification.

That’s my analogy for the old IRS Forms W-8s and the current day IRS Forms W-8s.

Compare that form, of just 10 years ago, with what is required and must be certified to under current law. It can be daunting.

Now to the rub. Individuals who certify erroneously or falsely, can run a risk that the government asserts such signed certification was done intentionally. I have seen it happen in real cases; even though the individual layperson (particularly those who speak little to no English and live outside the U.S.) typically has little understanding of these rules. They typically sign the documents presented to them by the third party; usually the banks and other financial institutions.

The U.S. federal tax law has a specific crime, for making a false statement or signing a false tax return or other document – which is known as the perjury statute (IRC Section 7206(1)). This is a criminal statute, not civil. Some people are also under the misunderstanding that a false tax return needs to be filed. The statute is much broader and includes “. . . any statement . . . or other document . . . “.

(1) Declaration under penalties of perjury

Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that it is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; or . . .

Therefore, if a U.S. citizen living overseas (or anywhere) signs IRS Form W-8BEN (or the bank’s substitute form, which requests the same basic information), that signature under penalty of perjury will necessarily be a false statement, as a matter of law. Why? By definition, the statute says a U.S. citizen is a “United States person” as that technical term is defined in IRC Section 7701(a)(30)(A). Accordingly, IRS Form W-8BEN, must only be signed by an individual who is NOT a “United States person”; who necessarily cannot be a United States citizen. To repeat, a United States citizen is included in the definition of a “United States person.” Plus, the form itself, as highlighted at the beginning of the form, warns against any U.S. citizen signing such form.

Accordingly, if a U.S. citizen were to sign IRS Form W-8BEN which I have seen banks erroneously request of their clients, they run the risk that the U.S. federal government will argue that such signatures and filing of false information with the bank was intentional and therefore criminal under IRC Section 7206(1). See a prior post, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Indeed, criminal cases are not simple, and I am not aware of any single criminal case that hinged exclusively on a false IRS Form W-8BEN. However, I have seen cases, where the government has alleged the U.S. born individual must have signed the form intentionally, knowing the information was false. It’s a question of proof and of course U.S. citizens wherever they reside, should take care to never sign an IRS Form W-8BEN as an individual certifying they are not a “United States person”; even if they think they are not a U.S. person

For further background information on this topic, see a prior post: FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

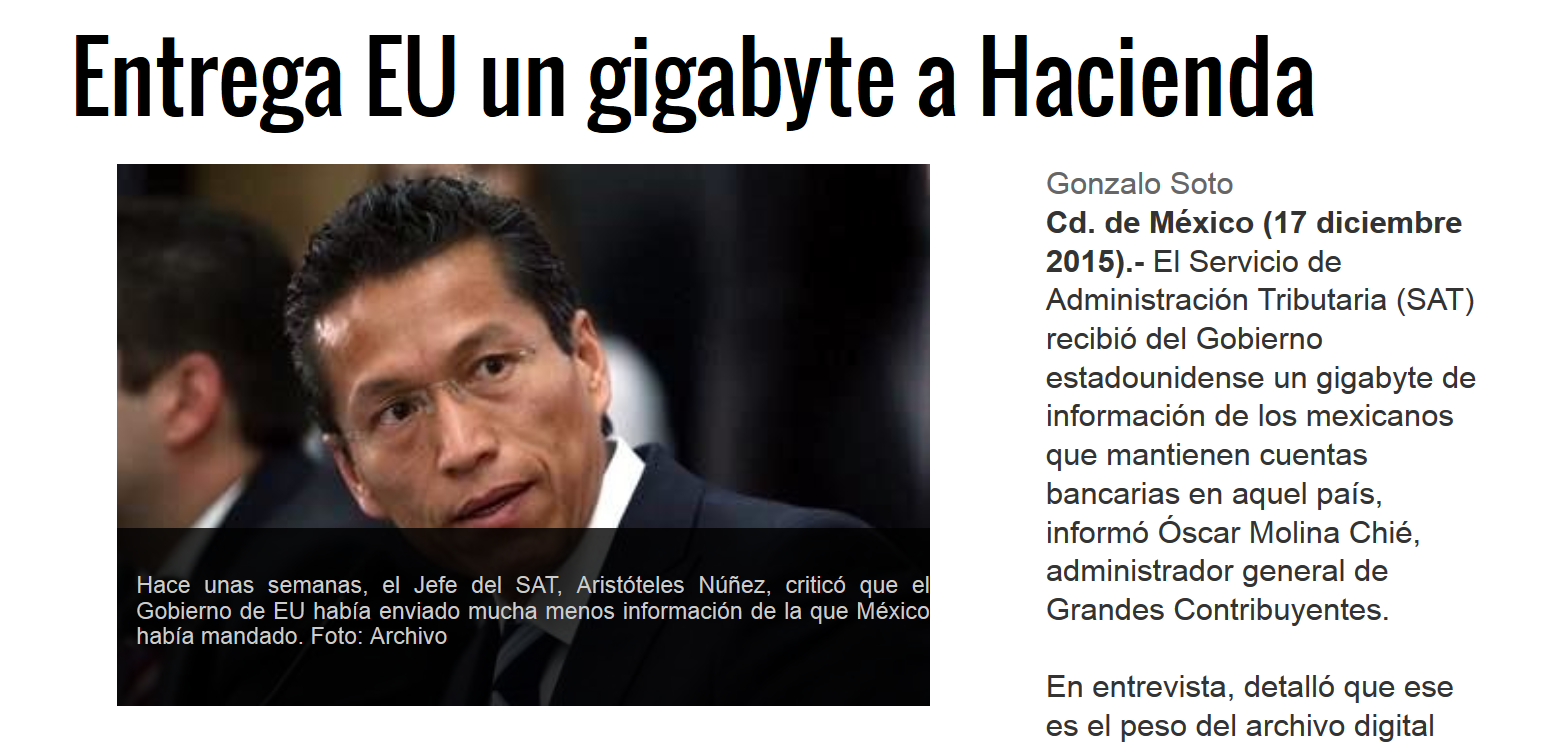

Foreign Government Receives a “FATCA Christmas Gift” from IRS: 1 Gigabyte of U.S. Financial Information

The last post discussed how the director of the Mexican tax administration was critical of the U.S. federal government for not providing FATCA information on U.S. financial accounts. See, Foreign Government Criticizes U.S. Government for  NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

The automatic exchange of bank and financial information is driven by the U.S. Treasury driven Intergovernmental Agreement (IGA).

As a follow-up, the Mexican newspaper Reforma reported on the 17th of December that the U.S. just provided Mexico’s treasury with a gigabyte of Mexican taxpayer information regarding U.S. financial and bank accounts. See, Entrega EU un gigabyte a Hacienda, dated Dec 17, 2015.

This news comes on the heals of the earlier criticism by the Commissioner of the Mexican IRS (SAT – Servicio de  Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Finally, the article emphasized that Mexico has sent the IRS information regarding Mexican bank accounts of U.S. citizens.

The question is how much Mexican bank and financial information has actually been provided by SAT of the hundreds of thousands (if not more than 1 million) dual national taxpayers, who are citizens of both Mexico and the U.S.? See, Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand, dated January 28, 2015.

Foreign Government Criticizes U.S. Government for NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts

This news is ironic. The U.S. government has chastised various banks and governments around the world since 2009 for not providing financial information on U.S citizens (USCs) and other U.S. taxpayers regarding their foreign bank and financial accounts. See, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior, posted Sept 8, 2014.

Now, it is foreign governments’ turn, to criticize the U.S. Treasury and IRS for not keeping up with its promises to provide U.S. financial and bank information on taxpayers of their countries pursuant to all of the FATCA Intergovernmental Government Agreements (IGAs) that were pushed so hard by U.S. Treasury. See, FATCA IGA with Hong Kong Signed: U.S. Citizens and Lawful Permanent Residents Residing in or Around Hong Kong Need to Know, posted on Nov. 17, 2014.

The Commissioner of the Mexican IRS (SAT – Servicio de Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez just announced that the U.S. government is not holding up its side of the bargain under the U.S.-Mexico IGA. See, the Dec. 12, 2015 article en the national Mexican newspaper, El Universal, EU incumple entrega de informacion: SAT: Mexico ha hecho su parte, asegura Aristóteles Núñez

The article, which is in Spanish, explains that Mexico has complied with its obligations under the IGA by providing detailed information about U.S. taxpayers with accounts in Mexican financial institutions to the U.S. government. However, the U.S. government has not complied with its side of the bargain. The news report says no specific details were provided by Mr. Núñez about what type of information was provided.

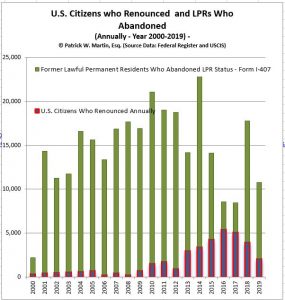

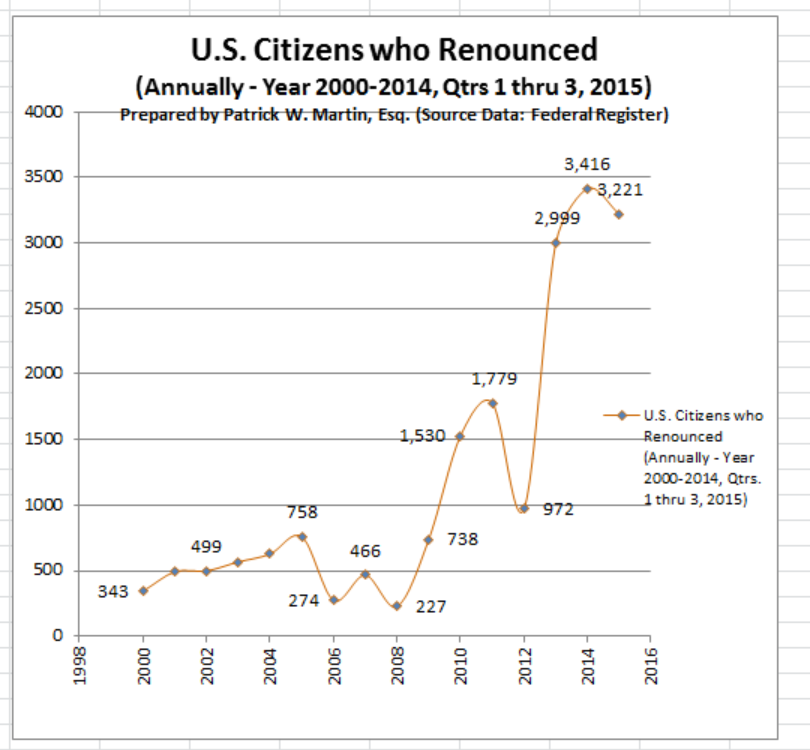

WSJ Asks the Question: Is the IRS Undercounting Americans Renouncing U.S. Citizenship?

Is the IRS Undercounting Americans Renouncing U.S. Citizenship?, posted Sept. 16, 2015.

The names of U.S. citizens who have renounced is published quarterly pursuant to IRC Section 6039G. See, prior related posts: 1,426 Individuals Give Up Passport: Record Number of U.S. Citizens Renouncing: Quarter 3 for 2015, October 30, 2015.

No one knows for certain if the IRS (including the IRS per some of my conversations) is getting complete data from the Department of State regarding each name and individual.

The graph I have prepared shows the number of names reported quarterly as I track all reported names quarterly that related to clients and non-clients. The latest cumulative amounts for 2015 (which does not include the 4th quarter) shows 3,221 thus far in the year. If there is close to 1,400 as was the case for the last quarter, the total will be a record – by a bunch; i.e., close to 5,000 renunciations for the year.

Anecdotally, I have seen renunciations surge in our practice, largely as U.S. citizens residing around the world (typically in the “Accidental American” category) learn about the long arm of the U.S. tax law by way of their local financial institutions and reporting and documents requested as part of FATCA. See, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets, posted Nov. 2, 2015.

None of this answers the question of whether there is under-reporting of the names? Indeed, the question will likely not be answered without more information provided by the U.S. Department of State and the U.S. Treasury (i.e., the IRS officers responsible for issuing the names and report in the Federal Register).

The government is also likely to reject issuing information on these details to individuals and their advisers as part of a Freedom of Information Act (“FOIA”) request. I have had similar requests rejected by the government under the so called “Exemption 7(E)” of FOIA. See,

Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

This post is written simply because so many U.S. citizens residing overseas are reasonably confused about the complexity of U.S. tax law. The mere requirement to file U.S. income tax returns for those overseas often comes as a great surprise. My non-U.S. born wife is an exception (as she also lives outside the U.S.) simply because I have repeatedly told her for our 20 some years of marriage.

Some in the IRS erroneously think U.S. citizens residing overseas do and should understand U.S. tax law. I posed one simple scenario to a very sophisticated IRS attorney not very long ago who specializes in the FATCA rules.

Her view is (hopefully was) that U.S. citizens throughout the world know or should know the U.S. tax laws because the instructions to IRS Form 1040 are clear.

This thought knocked me off my figurative chair onto the floor! Smack.

My surprise is based upon my own experience working with individuals and families throughout the world, in numerous countries. I have noticed a number of notions, based upon these andectodal experiences as follows:

- A minority of U.S. citizens (unless they lived most of their lives in the U.S. and recently moved overseas as an “expatriate”) have no real basic idea of how the U.S. federal tax laws work; let alone to their assets and income in their country of residence. See USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

- There are indeed plenty of immigrant U.S. residents (certainly less than 50% by my own experience – especially when concepts of PFICs and foreign tax credits start being discussed) who even understand the basics of U.S. international tax law.

- If they reside in an English speaking country that has relatively strong family or historical ties to the U.S. (e.g., England, Ireland, Scotland, and Canada, etc.) they are likely to have a better idea of the U.S. federal tax laws, but still the majority don’t know key concepts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

- Even those in English speaking countries that have less historical or family ties to the U.S. have a lesser understanding (e.g., New Zealand, Australia, Kenya, South Africa, India, etc.).

- Those who do not speak English know even less about U.S. tax laws and how they apply to them.

- Many individuals who learn of these requirements overseas are sometimes driven to great despair. The message they receive is not a correct one under the law in my view: as they read IRS materials (for instance, see FAQs 5, 6 and and former 51.2 from the Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers 2014) and come to the conclusion they will soon be going to jail, criminally prosecuted or otherwise be subject to tens of thousands of dollars worth of penalties for their failure to file a range of tax forms.

- Literally, sometimes as a tax lawyer I feel more like a psychologist, when these individuals come to me saying they can’t sleep, they can’t eat, they are seeing a cardiologist for high blood pressure, etc. and even in a most extreme case they thought suicide was a solution. See, How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas.

- Individuals around the world (even tax professionals) and certainly laypeople, are not commonly reading TaxAnalysts (nor would they subscribe) or other tax professional publications that explain many of the intricacies of U.S. tax laws.

- Learning and understanding U.S. tax laws, including just the basics, requires a great deal of time, aptitude for nuances and details, literacy, patience and a level of aptitude for such matters that simply escape many people around the world (most I would say). see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. I can relate to this personally, as I am an international tax professional (indeed I even studied a post graduate law course outside the U.S. in a non-English language), have spent my entire professional career of more than 25 years in the area, and yet only generally have a very superficial understanding of tax laws throughout the countries where I am dealing with clients. I don’t try to understand the details of those laws.

- Many people are angry and frustrated (justifiably so, in my view, in many cases) after learning they are subject to these rules. See comment above about being a psychologist. Plus, USCs and LPRs residing outside the U.S. – and IRS Form 8938. In addition, see, Taxpayer Advocate Report on Burdens of Benign Taxpayers who Make Mistakes

Back to the intelligent IRS tax attorney. My question to her was: “Why would you, as a U.S. born individual not be reviewing the tax laws, tax forms and tax instructions of the country where your parents were born prior to immigrating to the U.S.?” I asked: “Are you not reviewing those laws in the original language of your parents (not English, but the other language of your parent’s country) to understand what tax forms and returns you should be filing?”

The IRS attorney’s response was: “What: of course, I am not reviewing such tax forms or filing information or tax laws, as I would have no tax obligations in that foreign country where I have no income, no assets or no bank or financial accounts!”

My follow-up question was a simple one: “Don’t you realize that U.S. federal tax law (Title 26) and financial bank reporting laws (Title 31) do just that!”

“Hmm she paused: how can that be?” I don’t recall if she said this out loud, or just said it with her puzzled expression.

The answer of course is that through citizenship (including derivative citizenship through a U.S. parent even though the child never spent a single day of residence in the U.S., let alone received any income or assets); that same individual in the mirror position as that IRS attorney is subject to a host of U.S. federal tax and financial reporting laws. See, Sir Winston Churchill – Famous People. Did he become a U.S. citizen at birth via “derivative citizenship”? Did he file U.S. income tax returns?

Here is the big disconnect. It’s not just among the ill-informed or those lesser educated on the fine points of law. I had the pleasure this week along with my wife to host two educated, worldly and engaging individuals who have been married some 20 years together. They are well read and highly educated. Both are lawyers by training, one practices law that often pushes him fairly deeply into the tax law and his wife is a wonderful and experienced judge in the California state courts.

I asked them (as I like to ask people around the world) if they had ever heard or understood that the U.S. federal tax law imposes taxation and very detailed reporting on the worldwide income and assets of U.S. citizens who reside outside the U.S. I discussed  Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

All of it was a great surprise to them! They were in utter shock and both are residents in the U.S., highly educated in the law and are like the vast majority of the world, including U.S. citizens who reside outside the U.S.

This is the common response for many U.S. citizens residing overseas.

Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

This is Part II, a follow-on discussion of older U.S. case law and IRS rulings that address how and when individuals are subject to U.S. taxation before and after they assert they are no longer U.S. citizens.

I might point out that I am of the belief that we humans always like to hear the news we want to hear; and/or interpret it in the way we find most beneficial to us. Who doesn’t like good news versus bad news? Whether we (laypeople and tax lawyers alike) interpret Section 877A(g)(4) in any particular way; it is of no real consequence when it is the IRS that will enforce the law and ultimately the Department of Justice, Tax Division who will handle any such case interpreting this provision before a U.S. District Court or the Court of Federal Claims. For those who have not litigated before these Courts and seen how aggressive are the government lawyers in advocating for the government, the following discussion will hopefully be illustrative.

See, Part I: Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4)), dated October 16, 2015.

The question is what is the correct date of “relinquishment of citizenship” as defined in the statute; IRC Section 877A(g)(4)? Many argue the law cannot be applied retroactively?

However, the specific case discussed here, did just that; applied the law retroactively to determine U.S. citizenship status of an individual and corresponding tax obligations. This was also in a time of a much simpler tax code with (i) no international information reporting requirements (e.g., IRS Forms 8938, 8858, 5471, 8865, 3520, 3520-A, 926, 8621, etc.), (ii) no Title 31 “FBAR” reporting requirements and (iii) no constant drumbeat by the IRS of international taxpayers and enforcement. See, recent announcement by IRS on Oct. 16, 2015 (one day after tax returns were required to be filed by many) Offshore Compliance Programs Generate $8 Billion; IRS Urges People to Take Advantage of Voluntary Disclosure Programs. However, for cautionary posts on the IRS OVDP and the deceptive numbers published (e.g., “$8 Billion”), see How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Of course, the answer to this question helps determine if and when will the individual be subject to the federal tax laws of the U.S. on their worldwide income and global assets. In the case of Ms. Lucienne D’Hotelle (an interesting 1977 appellate opinion from the firs circuit) she had spent little time in the U.S. and had sent a letter in her native language French to the U.S. Department of State, which stated “I have never considered myself to be a citizen of the United States.” This is not unlike many individuals around the world today; at least as of late – in the era of FATCA, who assert they are not a U.S. citizen because they “relinquish[ed] it by the performance of certain expatriating acts with the required “intent” to give up the US citizenship” and did not notify the U.S. federal government.

The Court nevertheless found Ms. Lucienne D’Hotelle retroactively subject to U.S. income taxation on her non-U.S. source income (up until she received a certificate of loss of nationality from the Department of State); for specific years even when the immigration law provisions of the day said she was no longer a U.S. citizen during that same retroactive period.

There have been many contemporary commentators who argue an individual does not need to (i) have, (ii) do, or (iii) receive any of the following, and yet still should be able to successfully argue they have shed themselves of U.S. citizenship and hence the obligations of U.S. taxation and reporting on their worldwide income and global assets –

(i) receive a U.S. federal government issued document (e.g., a certificate of loss of nationality “CLN” per 877A(g)(4)(C)),

(ii) receive a cancelation of a naturalized citizen’s certificate of naturalization by a U.S. court (per 877A(g)(4)(D)),

(iii) provide a signed statement of voluntary relinquishment from the individual to the U.S. Department of State (per 877A(g)(4)(B)), or

(iv) provide proof of an in person renunciation before a diplomatic or consular officer of the U.S. (per paragraph (5) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481(a)(5)), in accordance with 877A(g)(4)(C)).

Some older tax cases that interpreted similar concepts are worthy of consideration. They will certainly be in any brief of the attorneys for the U.S. Department of Justice, Tax Division and/or Chief Counsel lawyers for the IRS in any case where the individual challenges that none of the above items are required in their particular case to avoid U.S. taxation and reporting requirements.

The D’Hotelle case is illustrative of the efforts taken by the Department of Justice, Tax Division in collecting U.S. income tax on a naturalized citizen. You will notice they did not take a sympathetic approach to her case. Ms. Lucienne D’Hotelle was born in France in 1909 and died in 1968 in France, yet the U.S. government continued to pursue collection of U.S. income taxation on her foreign source income from the Dominican Republic, France and apparently Puerto Rico even after her death during a period of time when she used a U.S. passport. Lucienne D’Hotelle de Benitez Rexach, 558 F.2d 37 (1st Cir.1977). She, not unlike many individuals today, claimed she was not a U.S. citizen – or at least stated “I have never considered myself to be a citizen of the United States.”

Some of the particularly interesting facts relevant to Ms. D’Hotelle, a naturalized citizen, which are relevant to the question of U.S. taxation of citizens, were set forth in the appellate court’s decision as follows:

Lucienne D’Hotelle was born in France in 1909. She became Lucienne D’Hotelle de Benitez Rexach upon her marriage to Felix in San Juan, Puerto Rico in 1928. She was naturalized as a United States citizen on December 7, 1942. The couple spent some time in the Dominican Republic, where Felix engaged in harbor construction projects. Lucienne established a residence in her native France on November 10, 1946 and remained a resident until May 20, 1952. During that time s 404(b) of the Nationality Act of 19402 provided that naturalized citizens who returned to their country of birth and resided there for three years lost their American citizenship. On November 10, 1947, after Lucienne had been in France for one year, the American Embassy in Paris issued her a United States passport valid through November 9, 1949. Soon after its expiration Lucienne applied in Puerto Rico for a renewal. By this time she had resided in France for three years.

* * *

On May 20, 1952, the Vice-Consul there signed a Certificate of Loss of Nationality, citing Lucienne’s continuous residence in France as having automatically divested her of citizenship under s 404(b). Her passport . . . was confiscated, cancelled and never returned to her. The State Department approved the certificate on December 23, 1952. Lucienne made no attempt to regain her American citizenship; neither did she affirmatively renounce it.

* * *

Predictably, the United States eventually sought to tax Lucienne for her half of that income. Whether by accident or design, the government’s efforts began in earnest shortly after the Supreme Court invalidated *40 the successor statute4 to s 404(b). In in Schneider v. Rusk, 377 U.S. 163 (1964), the Court held that the distinction drawn by the statute between naturalized and native-born Americans was so discriminatory as to violate due process. In January 1965, about two months after this suit was filed, the State Department notified Lucienne by letter that her expatriation was void under Schneider and that the State Department considered her a citizen. Lucienne replied that she had accepted her denaturalization without protest and had thereafter considered herself not to be an American citizen.

There are other facts that make clear the government was not fond of her husband, the income that he earned and how he managed his and his wife’s assets during and after her death. The Court also discusses at length the fact that she had used a U.S. passport during the years when she alleges she was not a U.S. citizen. The Court goes on to analyze her U.S. citizenship, and the following discussions are illustrative of the ultimate tax consequences.

The government contends that Lucienne was still an American citizen from her third anniversary as a French resident until the day the Certificate of Loss of Nationality was issued in Nice. This case presents a curious situation, since usually it is the individual who claims citizenship and the government which denies it. But pocketbook considerations occasionally reverse the roles. United States v. Matheson, 532 F.2d 809 (2nd Cir.), cert. denied 429 U.S. 823, 97 S.Ct. 75, 50 L.Ed.2d 85 (1976). The government’s position is that under either Schneider v. Rusk, supra, or Afroyim v. Rusk, 387 U.S. 253, 87 S.Ct. 1660, 18 L.Ed.2d 757 (1967), the statute by which Lucienne was denaturalized is unconstitutional and its prior effects should be wiped out. Afroyim held that Congress lacks the power to strip persons of citizenship merely *41 because they have voted in a foreign election. The cornerstone of the decision is the proposition that intent to relinquish citizenship is a prerequisite to expatriation.

411 F.Supp. at 1293. However, the district court went too far in viewing the equities as between Lucienne and the government in strict isolation from broad policy considerations which argue for a generally retrospective application of Afroyim and Schneider to the entire class of persons invalidly expatriated. Cf. Linkletter v. Walker, supra. The rights stemming from American citizenship are so important that, absent special circumstances, they must be recognized even for years past. Unless held to have been citizens without interruption, persons wrongfully expatriated as well as their offspring might be permanently and unreasonably barred from important benefits.6 Application of Afroyim or Schneider is generally appropriate.* * *

During the interval from late 1949 to mid-1952, Lucienne was unaware that she had been automatically denaturalized.

* * *