Month: January 2015

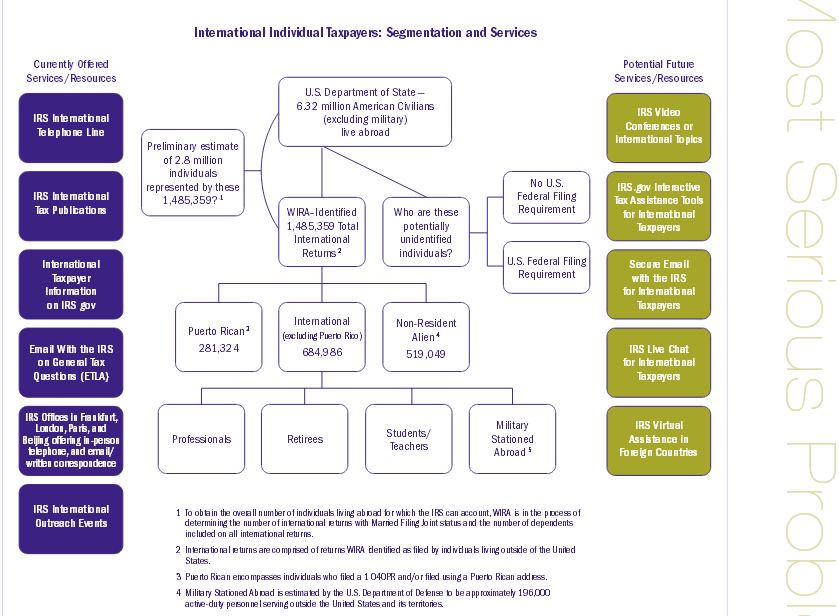

Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand

The IRS has key tax return filing information in their current records; pre-FATCA flow of financial information. Various reports indicate there are probably around 6-7 million U.S. citizens residing overseas, although there is no certainty in these numbers. See, Taxpayer’s Advocate Annual Report of 2012 – that  discussed both the number and type of individuals overseas, and potentially unidentified individuals.

discussed both the number and type of individuals overseas, and potentially unidentified individuals.

The IRS tracks and keep information on U.S. income tax returns filed by U.S. individual taxpayers overseas.

The information is not only the number of tax returns (head count), but also the amount of income reported. For instance, TAS reported about 700,000 returns were filed in 2010 by U.S. taxpayers abroad, while estimating about 6.32 million U.S. citizens reside abroad. See, p. 37 of the Taxpayer’s Advocate Annual Report of 2012 –

These numbers do not even try to quantify the number of lawful permanent residents (“green card holders”) who reside around the world, who are not filing U.S. income tax returns. In 2012, the estimated number of LPRs was 13.3 million as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012

How many of these LPRs are living outside the U.S. and not filing or reporting their worldwide income on U.S. income tax returns?

In addition, for the tax year 2011, the IRS Tax Statistics (“SOI”) in the “SOI Tax Stats – International Individual Tax Statistics” reported that only about 450,000 returns were filed with the foreign earned income exclusion. See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed

A detailed report of these statistics commissioned by the IRS and prepared by Scott Hollenbeck and Maureen Keenan Kahr titled Individual Foreign-Earned Income and Foreign Tax Credit, 2011 provides numerous insights about the likely under reporting and non-filers of U.S. income tax returns .

.

This report provides the following information reflecting the UK as the number one country with foreign earned income (Section 911) followed by Canada. Ironically Afghanistan (presumably due to the U.S. citizens working in that country as a result of the war?) is the country in the 4th location, ahead of Hong Kong and Japan.

Noticeably absent from that graph is Mexico, which reportedly has the largest number of U.S. citizens residing in any particular country. Canada is the second most populated country with U.S. citizens according to numerous reports.

Only about 46,000 returns were filed by Canadian residents claiming the foreign earned income exclusion, and even more surprising are the mere 7,000 returns from Mexican based U.S. taxpayers. See Table 2 of the report – Individual Foreign-Earned Income and Foreign Tax Credit, 2011

These are the two most populated countries with U.S. citizens.

As the IRS receives information around the world from governments and financial institutions via FATCA, of U.S. citizens and their bank accounts, it will be fairly easy for them to start targeting certain countries and commence tax audits against residents in those countries.

IRS Closing Overseas Offices – IRS Disconnect Between Civil versus Criminal International Tax Enforcement

The IRS announced a few days ago that it will close various “civil-side enforcement” overseas offices.

The IRS Statement is set out in part below:

The IRS is planning to close civil-side enforcement offices in Frankfurt, London and Paris this budget year. This is in addition to the closure of the Beijing office earlier this fiscal year. After budget reductions over the last 4 consecutive years, the IRS is forced to make tough choices during this period of fiscal austerity and these closures have relatively little impact on taxpayers and treaty partners. Considering our global mission, technological advances, and budgetary constraints, the Internal Revenue Service is realigning many functions and

positions from foreign-based to US-based.

. . .

IRS remains committed, however, to servicing our expatriate community and meeting our international obligations. We believe these services can be provided by other methods.

IRS will also continue to interact and collaborate with foreign tax authorities directly and through participation in many international forums and organizations, and through bilateral or group projects. This collaboration remains essential in

meeting the challenges of tax administration in a global economy.

This announcement comes on the heals of further comments in December from senior Tax Division/Department of Justice attorneys that offshore tax evasion remains among the highest priority areas for criminal enforcement in 2015.

The closing of IRS offices in important world centers that serve “normal” international taxpayers, while at the same time another part of the government (Department of Justice) continues to beat the “international tax evasion” drum, continues to send a bit of a mixed message.

In an article I wrote and published back in Jan-Feb 2012 in the International Tax Journal titled Unsettled Future for U.S. Taxpayers Residing Overseas: Mixed Messages from IRS Commissioner vs. Ambassador—Part I, I quoted then Commissioner Shulman from December 15, 2011, and his prepared remarks to the IRS/GWU 24th Annual Institute on Current Issues in International Taxation:

What is the 10 year “Collection Statute” and Why is it Suspended for USCs and LPRs Overseas?

There are different periods of time the federal tax law sets forth to protect both the taxpayer and the government. In short, after a certain period of time (assuming numerous conditions are satisfied), neither (i) the government can take action to assess or recover taxes, or (ii) the taxpayer can demand a tax refund.

This concept is known as the “statute of limitations” and is a concept deeply imbedded throughout U.S. law, not just taxation law.

There are two key aspects for how and when taxes are levied by the IRS. First, there is the “assessment” part, which helps determine a tax is owing in the first place. There have been chapters of tax treatises written on how and when an assessment is valid. A tax return is a “self-assessment”. See, for instance, the CCH® Expert Treatise Library: Tax Practice and Procedure, and its chapter on Assessment and Collection.

The IRS can also make an assessment through a so-called “substitute return.” See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas.

The focus of this post, is on the second aspect; the “collection” part of how the IRS collects upon a final tax assessment.

There is a 10 year collection statute of limitations imposed upon the IRS. See IRC Section 6502.

The general rule, is that the IRS cannot wait forever to collect against a taxpayer for the amount of taxes owing. If the taxes are not collected within this 10 year period, the general rule is that the IRS cannot continue to attempt to collect the taxes.

However, there is a huge exception in the 10 year collection statutory law, which does not apply when the individual is physically outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). This means that any USC or LPR residing predominantly outside the U.S. will have this 10 year collection statute suspended in favor of the government.

In other words, the IRS will be able to indefinitely use its collection efforts to lien and levy assets of the taxpayer, when she is living outside the U.S. The only way to “re-start” the collection statute, is for the individual to travel to the U.S. and not stay outside the U.S. for more than a six month period. Obviously, for those who live outside the U.S., this will typically be impractical, if not impossible, to live several month continuous periods within the U.S.

Finally, traveling to the U.S., can raise additional issues for the overseas USC or LPR who has taxes owing to the IRS. See, Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

See also, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

The Importance of Planning – PRIOR to Renouncing, Relinquishing or Abandoning

International tax law experts who specialize in a particular area of the law, have a fairly good understanding of the importance of tax planning. The reason is simple. The law is complex and without planning,  laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

“Tax expatriation” in the U.S. is particular complex for several reasons:

1. The general rule is that there is an immediate income tax payable from the “mark to market” taxation rules on unrealized gains. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

2. If a tax is recognized under the U.S. tax law, the only way to discharge the liability with the U.S. federal government is to pay the tax owing. The IRS generally can collect an income tax owing against a taxpayer who lives outside the U.S. indefinitely, as the 10 year collection statute does not apply when the individual outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). More on this topic in another post. In other words, the IRS can “forever” pursue the collection of the “expatriation tax” against USCs and LPRs living outside the U.S.

3. It is easy to fall into the general rule of expatriation, even if the taxpayer would not otherwise be subject to income taxation. See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

4. The friends and family of the “covered expatriate” – i.e., the former U.S. citizen and long-term lawful permanent resident can be subject to U.S. taxation during their lifetimes, even if they also live outside the U.S. See also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Each of these points help demonstrate the need for planning prior to running to the U.S. Department of State and completing and filing the following forms when you take the oath of renunciation:

See, Documents to Request the Consular Officer When Renouncing U.S. Citizenship

At the end of the day, if the individual lives outside the U.S. and does not travel to and from the U.S., it may be practically very difficult for the IRS to collect on the tax judgment owing if the individual has no assets in the U.S. There are legal means and steps the IRS can take in an attempt to try to collect U.S. taxes on overseas assets.

For a further discussion on collection of taxes overseas:

See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations, and

Ideally, a former U.S. citizen or long-term lawful permanent resident will wish to avoid all of the potential tax and collection issues, by engaging in thoughtful and strategic planning prior to their renunciation of U.S. citizenship or abandonment of lawful permanent residency.

IRS Warns of Breach of Individual Financial Information – Bank Account Details and other FATCA Related Account Data

This is not new news; indeed it is somewhat old and stale. It has become more relevant, however, as the exchange of financial information under FATCA is to commence in a few months in 2015.

The IRS issued a warning in September that reads in relevant part as follows:

IRS Warns Financial Institutions of Scams Designed to Steal FATCA-Related Account Data

WASHINGTON — The Internal Revenue Service today issued a fraud alert for international financial institutions complying with the Foreign Account Tax Compliance Act (FATCA). Scam artists posing as the IRS have fraudulently solicited financial institutions seeking account holder identity and financial account information.

The IRS does not require financial institutions to provide specific account holder identity information or financial account information over the phone or by fax or email. Further, the IRS does not solicit FATCA registration passwords or similar confidential account access information.

This statement may be a bit misleading, since the FATCA law does require specific individual account holder information be provided to the government. It is detailed in its scope of information required; including account numbers, names of account owners, addresses of account owners, income from such accounts, taxpayer identification numbers (which means Social Security Numbers for U.S. citizens), etc.

Time will tell, how effective governments will be in maintaining their taxpayers’ information confidential; as opposed to private institutions, such as JP Morgan. See, JPMorgan data breach entry point identified: NYT