Month: April 2015

IRS Announcement this Month (April 2015): IRS Reminds Those with Foreign Assets of U.S. Tax Obligations

The IRS again this year reminded U.S. citizens residing overseas of their tax return filing obligations.

In the IRS announcement, IR-2015-70, April 10, 2015, titled IRS Reminds Those with Foreign Assets of U.S. Tax Obligations, the federal agency charged with enforcement of U.S. federal tax and financial account reporting laws, provides in part as follows:

* * *

Most People Abroad Need to File

A filing requirement generally applies even if a taxpayer qualifies for tax benefits, such as the foreign earned income exclusion or the foreign tax credit , that substantially reduce or eliminate their U.S. tax liability. These tax benefits are not automatic and are only available if an eligible taxpayer files a U.S. income tax return.

The filing deadline is Monday, June 15, 2015, for U.S. citizens and resident aliens whose tax home and abode are outside the United States and Puerto Rico, and for those serving in the military outside the U.S. and Puerto Rico, on the regular due date of their tax return. To use this automatic two-month extension, taxpayers must attach a statement to their return explaining which of these two situations applies. See U.S. Citizens and Resident Aliens Abroad for details.

. . .

Prior posts have discussed related filing issues, including the following:

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

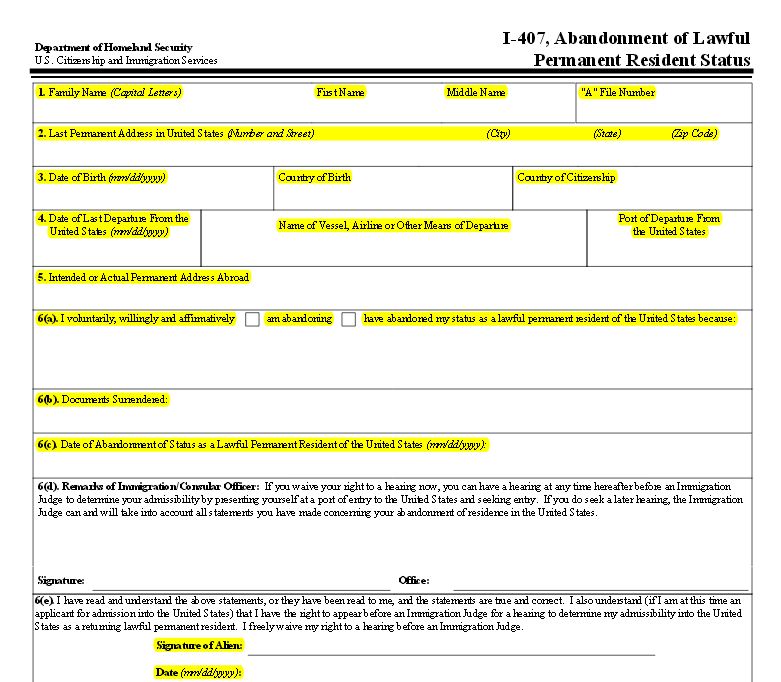

A prior post discussed the newly published USCIS immigration form I-407 for LPRs who must now use it when formally abandoning LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms  are set forth here. The new form requires the address overseas of the individual.

are set forth here. The new form requires the address overseas of the individual.

As readers here know, the names of former U.S. citizens are published quarterly by the U.S. federal government for the world to see. See a prior post, The 2014 Third Quarter Renunciations Is probably the New Norm –

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

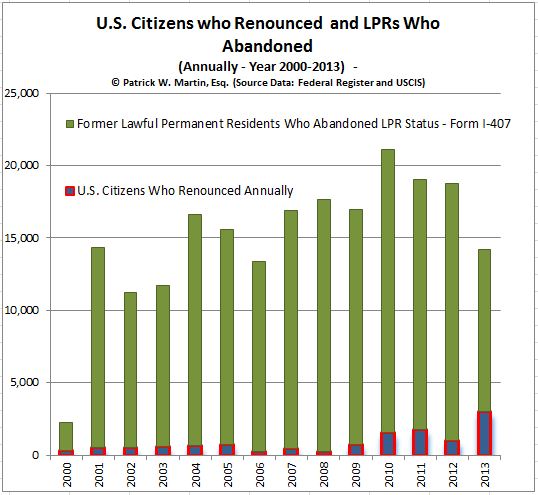

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

- “mark to market” taxation on their worldwide assets,

- 40% inheritance tax to U.S. beneficiaries,

- 40% tax on gifts to U.S. beneficiaries,

- etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”

The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

Categories of records in this system include:

A. The hardcopy paper A-File, which contains the official record material about each individual for whom DHS has created a record under the INA such as: naturalization certificates; various documents and attachments (e.g., birth and marriage certificates); applications and petitions for benefits under the immigration and nationality laws; reports of arrests and investigations; statements; other reports; records of proceedings before or filings made with the U.S. immigration courts and any administrative or federal district court or court of appeal; correspondence; and memoranda. Specific data elements may include:

- Alien Registration Number(s) (A-Numbers);

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

? Document type,

? issuing organization,

? document number, and

? expiration date;

- Military membership;

- Arrival/Departure information (record number, expiration date, class of admission, etc.);

- Federal Bureau of Investigation (FBI) Identification Number;

- Fingerprint Identification Number;

- Immigration enforcement history, including arrests and charges, immigration proceedings and appeals, and dispositions including removals or voluntary departures;

- Immigration status;

- Family history;

- Travel history;

- Education history;

- Employment history;

- Criminal history;

- Professional accreditation information;

- Medical information relevant to an individual’s application for benefits under the INA before DHS or the immigration court, an individual’s removability from and/or admissibility to the United States, or an individual’s competency before the immigration court;

- Specific benefit eligibility information as required by the benefit being sought; and

- Video or transcript of immigration interview

Subsequent posts will discuss how and when the law allows the IRS to access these records.

More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The U.S. Customs and Immigration Service (USCIS) just announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement, which announcment provides in part as follows:

New Version of Form I-407 Now Available

USCIS has published a new edition of USCIS Form I-407, Record of Abandonment of Lawful Permanent Status (OMB No. 1615-0130). You can download the form on our website.

You may begin using the revised Form I-407, Record of Abandonment of Lawful Permanent Resident Status today. The current edition is dated 02/26/2015, and we will not accept previous form editions

The new form has additional information compared to the prior form. Specifically, the Alien Registration Number and USCIS ELIS Account Number is required to be included.

Now, the individual is required to state the reasons for abandoning lawful permanent residency status.

Responses to  each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

One of the important enforcement and practical questions raised, is: Will the IRS be able to better track former “long-term residents” (certain former lawful permanent residents) for purposes of the “expatriation tax” under the new reporting form and system?

As has been explained, if an individual fails to certify under the tax law, they will necessarily be a “covered expatriate”; even if they do not meet the asset or income tax liability thresholds. See a prior post, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute.