Month: September 2014

How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

The separation of powers is often on full display when there are key Congressional hearings focused on the work (or lack thereof) undertaken by the key executive branch agencies responsible for tax enforcement:

1. Treasury/IRS, and

2. Justice Department.

There is an important reason why every day taxpayers should be interested in these hearings; particularly those who are considering renouncing United States Citizenship.

The actions and reactions of the IRS and Justice Department are often in response to Congressional hearings. This is very much the case with individual taxpayers with assets throughout the world.

A brief timeline of various hearings, and actions taken by the IRS and Justice Department (largely in response to such criticism) can be followed to demonstrate the influence of these hearings:

- Year 2006

U.S. Senate Permanent Subcommittee on Investigations, published their report on August 1, 2006, entitled Tax Haven Abuses: The Enablers, The Tools & Secrecy.

Little direct action was taken by the IRS or Justice Department in this year. It was the year 2008, where the direct hearings lead to more direct action taken.

- Year 2008

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on July 16, 2008, entitled Tax Haven Banks and U.S. Tax Compliance –

November 2008, a U.S. federal grand jury indicted the Chairman and CEO of UBS Global Wealth Management and Business Banking.

- Year 2009

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on March 4, 2009 Tax Haven Banks and U. S. Tax Compliance – Obtaining the Names of U.S. Clients with Swiss Accounts

UBS agrees in February 2009 to pay a US$780M fine to the U.S. government and enter into a deferred prosecution agreement on charges of conspiring to defraud the United States by impeding the Internal Revenue Service.

IRS Implements first Offshore Voluntary Disclosure Program (“OVDP”) on March 26, 2009

- Year 2010

Numerous taxpayers and several Swiss bankers were indicted and/or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

Congress passes and the President signs into law, the Foreign Account Tax Compliance Act (“FATCA”) in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act.

- Year 2011

IRS Implements its second Offshore Voluntary Disclosure Initiative (“OVDI”) in 2011.

Numerous taxpayers and several Swiss financial advisors were indicted; and a HSBC Indian client was also indicted or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

- Year 2012

IRS creates an open ended OVDP program in 2012 that continues; with modifications made in 2014.

Several taxpayers were indicted; including those implicating an Israeli bank for various tax crimes charges. . See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains commitments from various countries to sign various FATCA, intergovernmental Agreements (“IGAs”) for automatic exchange of financial information; France, Germany, Italy, Spain, United Kingdom, Denmark and Mexico.

- Year 2013

In January 2013, the U.S. Attorney’s Office in the Southern District of New York secured the guilty plea of Wegelin Bank, the oldest private bank in Switzerland and the first foreign bank to plead guilty to felony tax charges.

In August, 2013, the United States and Switzerland Issue Joint Statement Regarding Tax Evasion Investigations and ability of Swiss banks to enter into deferred prosecution agreements.

Several taxpayers were indicted and advisors; including multiple financial institutions outside of Switzerland for various tax crimes charges. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains more commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information;.

- Year 2014

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on February 26, 2014 Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

Posted on February 26, 2014 Updated on March 2, 2014

IRS announces on June 18, 2014, IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance

See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The Treasury Department obtains numerous commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information. See, HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

Why the terms “Relinquish” and “Renounce” are Not Legally Distinguishable for Immigration or Tax “Expatriation” Law Purposes

The topic of “relinquish” versus “renounce” has already been touched upon in an earlier post. See, The Semantically Driven Vortex of “Relinquishing” vs. “Renouncing”

Posted on June 21, 2014

Guest Post from Immigration Lawyer – Mr. Jan Bejar –

***

It seems that many individuals think there is an important distinction, legally speaking for U.S. federal tax purposes.

In sum, I am of the view that both terms are in effect interchangeable for federal tax purposes.

The important time reference under the law of IRC Sections 877 and 877A is the “expatriation date” as defined in Section 877A(g)(3) – which focuses on specific dates tied to meetings or events with the U.S. Department of State.

Indeed the tax statute uses the terms “renounce” and “relinquish” in the same breath.

The key terms of the statute are set out below:

Part III of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Mr. Jan Bejar

Part III of III: Tracking Travelers’ Entries and Exits –

Guest Immigration Law Post by Atty Mr. Jan Bejar

This post is a continuation of Part I and II of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Mr. Jan Bejar

. . .

For travel between Canada and the U.S., DHS and the Canada Border Services Agency (CBSA) have partnered in the “Beyond the Border” initiative to jointly track entries and exits. The idea of the program is that an entry into one country serves as a record of exit from the other. The initiative was planned to roll-out in four phases.

During Phase I, which began September 30, 2012, and lasted through January 15, 2013, DHS and CBSA exchanged biographic data regarding third country nationals, permanent residents of Canada who are not U.S. citizens, and permanent residents of the U.S. who are not citizens of Canada, at four land ports of entry.

During Phase II, which began on June 30, 2013, the biographic data about the same population was exchanged for crossings at all automated land ports of entry.

Phases III and IV were supposed to begin June 30, 2014, and would have expanded the initiative to virtually all travelers, including U.S. and Canadian citizens, and to air travel, but apparently these phases have been delayed.

Finally, for nonimmigrants issued paper I-94 and I-94W records (either in the past or presently at land ports of entry), submission of those records at a port of entry or to the airlines upon departure ideally should create, or should have created, an exit record. Presently, for nonimmigrants who arrive by air or sea and do not have a paper I-94, but who then depart by land, such that APIS does not record the departure, CBP instructs travelers to keep proof of the departure. Nonimmigrants issued a paper I-94, either in the past at any port of entry or currently at a land port of entry, who did not submit them upon departure, can mail them to a designated address with proof of the departure to create a departure record in the NIIS.

In sum, regardless of your immigration status, the U.S. government likely knows when you arrive but may not know when you leave, particularly if you depart along a land port of entry on the southern border.

Part II of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Mr. Jan Bejar

Part II of III: Tracking Travelers’ Entries and Exits –

Guest Immigration Law Post by Atty Mr. Jan Bejar

This post is a continuation of Part I of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Mr. Jan Bejar

. . .

For certain classes of nonimmigrants at air and sea ports of entry, electronic I-94 and I-94W records are generated using APIS data and stored in the NIIS. As of April 30, 2013, CBP stopped issuing paper I-94 records at air and sea ports of entry. Currently, CBP still issues paper I-94 records at land ports of entry, which are then entered into the NIIS.

Trusted traveler programs are another method of tracking and recording entries into the U.S. Trusted traveler programs include Global Entry, NEXUS on the northern border, and SENTRI on the southern border, among others. Travelers voluntarily provide detailed biometric and biographic data to CBP in exchange for expedited admission at ports of entry. Members use their machine-readable identification documents and/or RFID cards when entering the U.S., and their entries are accordingly recorded and stored.

Even today, despite the high inspection rates and various technologies, it is occasionally possible that an entry into the U.S. at a land port of entry would not be recorded. For example, if an inspector at a land port of entry simply looks at a U.S. passport or other travel document that is not RFID-enabled and does not “swipe” it to use its machine-readable capabilities, then the traveler’s entry may not be recorded. Along the same lines, a minor under 16 years old entering the U.S. at a land port of entry with a birth certificate may not have the entry recorded.

The U.S does not have a history of tracking departing travelers, and therefore comprehensively tracking exits has proved more elusive, particularly for land departures. Various pilot programs have been tested and later discontinued. Presently, at certain land ports of entry on the southern border, travelers may be subjected to screening and inspection upon departure. CBP’s mandate in conducting these inspections is to address violence in Mexico and to interrupt transnational criminal organizations’ activities. Outbound screening tends to happen in short-term surges, followed by periods of reduced inspection.[1] Simply passing through the screening, however, does not create a record of the departure.

For travelers departing the U.S. by air and sea, as mentioned above, CBP uses APIS to collect commercial passenger and crew manifests for all outbound international departures. Compliance by carriers is near 100%. CBP then transfers this data for non-U.S. citizens to ADIS, which matches arrivals to and departures from the U.S. Anecdotally, this system for tracking exits from the U.S. is not foolproof.

For example, just a few months ago, a lawful permanent resident client who had applied for naturalization purchased a ticket to depart the U.S. while her naturalization application was pending (which is entirely permissible). Ultimately, however, she opted not to travel abroad and postponed her flight. At her recent naturalization interview, when the USCIS officer asked about her trips outside the U.S. during the past five years, he asked about her departure on the date of the canceled flight. He had presumably accessed APIS and/or ADIS, and presumably the airline carrier had shared her name as a passenger with CBP, even though she had not boarded the plane. She honestly denied departing the U.S. that day. Fortunately, the officer believed her and moved on, but the error could have been difficult and time-consuming to correct had it been necessary to do so. Further, if she had been a nonimmigrant with authorization only to remain in the U.S. until the day of her scheduled flight, the system may not have detected her overstay.

As another example along the same lines, the American Immigration Lawyers Association (AILA) just reported that USCIS has recently denied in error multiple applications for changes of status (to a different nonimmigrant status) and for adjustment of status (to permanent resident status) where the applicants had purchased, but not used, airline tickets to depart the U.S.[2]

These applications, in contrast to a naturalization application, typically require that the applicant remain in the U.S. until receiving a decision. The sole reason that USCIS cited in these denials was the applicants’ alleged departures from the U.S. and constructive abandonment of the applications. Presumably these officers accessed APIS, the NIIS, and/or ADIS but did not click through the electronic records deep enough to see that the applicants had not actually used the international plane tickets. USCIS is supposedly aware of this training issue, but these denials underscore the difficulty in tracking exits from the U.S.

[1] See, supra, at fn. 3.

[2] See “CBP Practice Alert: ‘Implied Departure’ and Denial of USCIS Benefits, AILA InfoNet Doc. No. 14090243 (posted Sep. 2, 2014); see also “Minutes from AILA CBP Liaison Committee Teleconference with Suzanne Shepherd, ESTA Director regarding I-94 web portal and travel history information,” August 6, 2014, AILA InfoNet Doc. No. 14082042 (posted August 20, 2014).

Jan Joseph Bejar, Esq.

(For: JAN JOSEPH BEJAR, APC)

Tel: (619) 291-1112

Fax:(619) 291-1102

E-mail: jbejar@immigrationlawclinic.com

Website: www.immigrationlawclinic.com

Part I of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Mr. Jan Bejar

Tracking Travelers’ Entries and Exits

Part I of III: Tracking Travelers’ Entries and Exits – Guest Immigration Law Post by Atty Jan Bejar

This immigration law guest post is related to prior posts: Global Entry, SENTRI and NEXUS after Renouncing – the “Trusted Traveler Programs” – SAFE TRAVELS!

See also, Tracking U.S. Citizens and LPRs in and Out of the Country – Tracking Taxpayers (Entry/Exit System)

For many years, since even before the 9/11 attack, the United States government has been trying to develop a comprehensive biometric system for tracking both entries to and exits from the United States. Although the government has a variety of mechanisms for tracking travelers’ entries into the U.S., tracking exits has proven to be a more difficult task.

For non-U.S. citizens, collecting data about a planned trip to the U.S. may begin even before an individual enters the U.S. For non-U.S. citizens who must first apply for a nonimmigrant visa to enter the U.S., the Department of State’s nonimmigrant visa application (Form DS-160) asks the applicant if he has made travel plans, and if so, for the details. Answering the question is optional, and obviously once the visa is issued, the Department of State does not track future travel plans. Additionally, the nonimmigrant visa application process requires an applicant to provide the Department of State with biographic and biometric data, which it stores in the Consular Consolidated Database (CCD). This database then links to some of the Department of Homeland Security (DHS) databases described below. The CCD has been in the news for the last month because it has been experiencing “system performance issues,” causing delays for thousands of U.S. passport and visa applicants.[1]

For non-U.S. citizens from the currently 38 Visa Waiver Program countries planning to travel to the U.S. for up to 90 days without a visa,[2] travelers must first submit biographic information and respond to eligibility questions through an online application, the Electronic System for Travel Authorization (ESTA). Customs and Border Protection (CBP), an agency within DHS, uses ESTA to screen applicants against terrorist, national security, and criminal watchlists.[3] The ESTA application requests information about travel plans, but providing travel details is optional.

For U.S. citizen and non-U.S. citizens alike traveling to the U.S. on commercial airlines, private aircraft, and commercial vessels such as cruise ships, CBP maintains the Advance Passenger Information System (APIS), an electronic data interchange system. Airlines and vessel carriers are required by law to provide CBP in advance with certain biographic information on all passengers and crew onboard all international departures and arrivals via APIS. The information transmitted to CBP includes biographic information, such as name, date of birth, gender, etc., and travel itinerary information. CBP also collects data from bus and rail carries on a voluntarily basis through APIS.

CBP sends the APIS data regarding non-U.S. citizens to the Arrival and Departure Information System (ADIS) to store and hold for matching against departure records.[4] DHS uses ADIS to store arrival and departure records, biographic data, and each traveler’s unique Fingerprint Identification Number System (FINS) identifier, which facilitates cross-referencing between ADIS and the Automated Biometric Identification System (IDENT) database, which is DHS’ primary biometric database. ADIS also aggregates records from a number of other DHS databases, including the CBP Nonimmigrant Information System (NIIS), the CBP Border Crossing Information System (BCI), the CBP TECS platform, the U.S. Immigration and Customs Enforcement (ICE) Student Exchange Visitor Information System (SEVIS), and the U.S. Citizenship and Immigration Services (USCIS) Computer Linked Information Management System (CLAIMS 3) among others, some of which will be discussed below.[5] ADIS stores this data for all non-U.S. citizens, including information on lawful permanent residents (“green card” holders), refugees, asylees, and nonimmigrants. There is a risk that ADIS might inadvertently retain data about U.S. citizens or retain data longer than permitted for travelers who subsequently become U.S. citizens.[6]

For commercial air travel, in addition to APIS, the Secure Flight Program requires domestic and international airlines to provide DHS with certain passenger manifest information at least 72 hours before flight time for all flights into or over the continental U.S.

For all travelers, including U.S. citizens, who either pass through preclearance inspections at certain foreign airports or through primary inspection at all U.S. ports of entry, CBP officers interview arriving travelers and check their travel documents. CBP collects basic biographic information, such as name, travel document number, and the date and location of arrival, for all travelers, including U.S. citizens. It captures the information and screens arriving travelers in TECS, CBP’s principal information-sharing platform for immigration screening and admissibility determinations. TECS is not only an information-sharing platform that allows inspectors to access different databases such as APIS, but also “a data repository to support law enforcement ‘lookouts,’ border screening, and reporting for CBP’s primary and secondary inspection processes.”[7] IRS officers can request that DHS add or delete travelers from lookout lists in TECS.[8] “CBP officers use TECS to check travelers against law enforcement and national security watchlists and to record and report on primary and secondary inspection results.”[9] Records of border crossings for all travelers, including U.S. citizens, are then stored in the BCI, and records for nonimmigrant visa holders are stored in the NIIS.

Several land ports of entry on both the northern and southern borders maintain dedicated “ready lanes” for travelers with radio frequency identification (RFID)-enabled travel documents, such as the U.S. passport card, the enhanced driver license, the newer enhanced permanent resident card, and the enhanced border crossing card. RFID-enabled documents allow CBP inspectors to quickly query TECS and create a record of the crossing.

Land ports of entry additionally utilize license plate readers in vehicle lanes to determine the plate number and issuing agency of vehicles passing through inspection, and that information is also used to query TECS. CBP denies maintaining a database of vehicle locations but will share license plate information in a law enforcement capacity, including with the National Insurance Crime Bureau and car insurance companies. License plate data is maintained for two years, unless it is moved to and maintained in another system with a different destruction schedule.

Also, most non-U.S. citizens arriving at air and sea ports are required to provide biometric data (fingerprints and digital photographs). The biometric data is added to IDENT, which is DHS’ primary biometric database, and vetted against additional biometric databases.[10] The Office of Biometric Identity Management (OBIM) maintains IDENT and provides DHS with biometric identification technological services, including storing, managing and analyzing the biometric data. OBIM is part of DHS’ National Protection and Programs Directorate, and it replaced DHS’ US-VISIT program in March 2013.

[More to follow . . . ]

[1] See http://travel.state.gov/content/travel/english/news/ccd-performance-issues.html, last updated August 4, 2014.

[2] See http://travel.state.gov/content/visas/english/visit/visa-waiver-program.html for more information on the Visa Waiver Program.

[3] See “Border Security: Immigration Inspections at Port of Entry,” Seghetti, Lisa, Section Research Manager, Congressional Research Service, January 9, 2014, last viewed at http://trac.syr.edu/immigration/library/P8498.pdf.

[4] See “Written testimony of U.S. Customs and Border Protection and U.S. Immigration and Customs Enforcement for a House Committee on Homeland Security, Subcommittee on Border and Maritime Security hearing titled ‘Fulfilling A Key 9/11 Commission Recommendation: Implementing Biometric Exit,’” released September 26, 2013, last viewed at http://www.dhs.gov/news/2013/09/26/written-testimony-cbp-and-ice-house-homeland-security-subcommittee-border-and.

[5] See “Privacy Impact Assessment Update for the Arrival and Departure Information System – Information Sharing Update,” March 7, 2014, last viewed at http://www.dhs.gov/sites/default/files/publications/privacy-pia-cpb-adis-update-20140305.pdf.

[6] See id.

[7] See “Privacy Impact Assessment for the TECS System: CBP Primary and Secondary Processing,” Department of Homeland Security, December 22, 2010, last viewed at http://www.dhs.gov/xlibrary/assets/privacy/privacy-pia-cbp-tecs.pdf.

[8] See https://tax-expatriation.com/2014/07/22/does-the-irs-investigate-united-states-citizens-uscs-and-lawful-permanent-residents-lprs-residing-overseas/

[9] See supra at fn. 3.

Jan Joseph Bejar, Esq.

(For: JAN JOSEPH BEJAR, APC)

Tel: (619) 291-1112

Fax:(619) 291-1102

E-mail: jbejar@immigrationlawclinic.com

Website: www.immigrationlawclinic.com

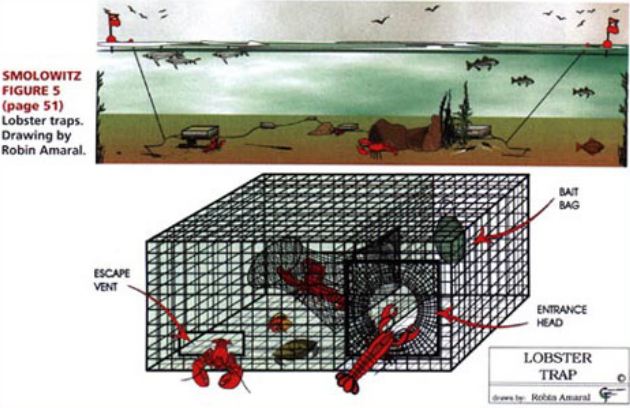

Avoiding the Lobster Pot: Why becoming a Naturalized Citizen or LPR can be the proverbial “Lobster [Tax] Pot”

Two famous tax professors coined a wonderful analogy that can largely be applicable to any non-U.S. citizen who is considering either becoming a (1) lawful permanent resident (LPR), or (2) a naturalized citizen.

Tax professors Boris I. Bittker (Yale) and James S. Eustice (NYU), both of whom are now deceased, wrote –

- “[Under the tax laws] a corporation is like a lobster pot: it is easy to enter, difficult to live in, and painful to get out of.”

I think the same analogy is very much appropriate to a non-U.S. citizen who becomes a LPR or a naturalized citizen, without fully understanding the U.S. federal tax consequences of such a decision. The word “corporation” merely should be changed with “lawful permanent resident” or “naturalized citizen” in the quote from Bittker and Eustice when considering the potential long-term application of the “expatriation tax” rules.

The analogy is particularly applicable for two reasons. First, individuals are usually less sophisticated and, often times, simply unaware of complex tax laws. Corporate taxpayers often can have a better understanding of complex U.S. tax laws – i.e., the “lobster trap” via sophisticated tax advisers.

Second, some lobster traps have an “escape vent” for small lobsters. Similarly, the tax laws on expatriation can treat individuals with smaller amounts of assets or U.S. tax liabilities, very differently and more favorably under the law. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute,

Non-U.S. citizens who are not certain they will spend the rest of their lives in the U.S., should carefully consider if they indeed wish to obtain LPR or become a naturalized citizen. This is because of the long-term tax consequences of Sections 877, 877A, 2801, etc. for those who later abandon their LPR status or renounce their U.S. citizenship.

Of course, this blog, is dedicated to shedding light on the income tax, estate and gift tax, and “covered gift” and “covered” inheritance tax consequences to those who enter the “lobster trap.”

Many more may wish to simply shy far away from the lobster trap to begin with.

Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)

A previous post explained why lawful permanent residents (LPRs) can never satisfy this exception in the law to avoid “covered expatriate status.” See, Why a “long-term” LPR can NEVER avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B) if Asset or Tax Liability Test is Satisfied!

For the same reasons, a naturalized citizen cannot satisfy the statutory requirement since they will never be able to meet the IRC Section 877A(g)(1)(B)(i)(I) requirement of becoming ” . . . at birth a citizen of the United States . . . ”

See the relevant provisions of the statute as follows:

(B) Exceptions

Of course a naturalized United States citizen by definition was not a citizen at birth and only became one upon completing the lengthy legal requirements of naturalization. See, USCIS website – Citizenship Through Naturalization

Posted on May 19, 2014

.