IRS Creates “International Practice Units” for their IRS Revenue Agents in International Tax Matters

The U.S. international tax law has become increasingly complex. I am confident when I say that very few individuals in the world (including IRS revenue agents) understand the complexities of Title 26 and Title 31 as they apply to  international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

Most USCs and LPRs who live in the U.S. certainly know and understand the basics of IRS Form 1040.

However, the type and scope of international transactions contemplated by the law can be significant and are rarely understood in any depth, even by many tax professionals. I have seen cases during my career of sophisticated individuals ranging from Nobel prize winners to U.S. Ambassadors, who had not a clue about the application of U.S. federal tax law to their lives. See, the Nov. 2, 2015 post, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

The lack of knowledge of these complex laws within the IRS, and the LB&I (Large Business and International group) which specializes in international matters has led to IRS “International Practice Units”. These are designed to allow IRS revenue agents who are not necessarily specialists in the international tax area to review transactions and be prepared to assess taxes and penalties against USCs and LPRs in the international context. The preamble says in part ” . . . Practice Units provide IRS staff with explanations of general international tax concepts as well as information about a specific type of transaction. . . ”

There are currently 63 different IRS “International Practice Units” all with dates from the last 12 months. Several of them focus heavily on information return filings which carry stiff penalties, even if no U.S. income taxes are owing. For instance see, Monetary Penalties for Failure to Timely File a Substantially Complete Form 5471 –Category 4 & 5  Filers.

Filers.

Another interesting IRS International Practice Unit is titled – Basic Offshore Structures Used to Conceal U.S. Person’s Beneficial Ownership of Foreign Financial Accounts and Other Assets.

These IRS materials give a good perspective from where the IRS views the world; including the introduction to this particular IRS International Practice Unit where it states: “This Practice Unit focuses on a U.S. Person’s proactive steps to “conceal” their ownership of foreign financial accounts, entities and other assets for the purposes of tax avoidance or evasion, even though, there may be some situations where there are legitimate personal or business purposes for establishing such arrangements. This unit falls under the outbound face of the matrix and thus, will focus on U.S Persons living in the United States . . . Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .” [emphasis added]

This is a breathtaking statement from the IRS internal training manuals that “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and  other creditors . . .”?

other creditors . . .”?

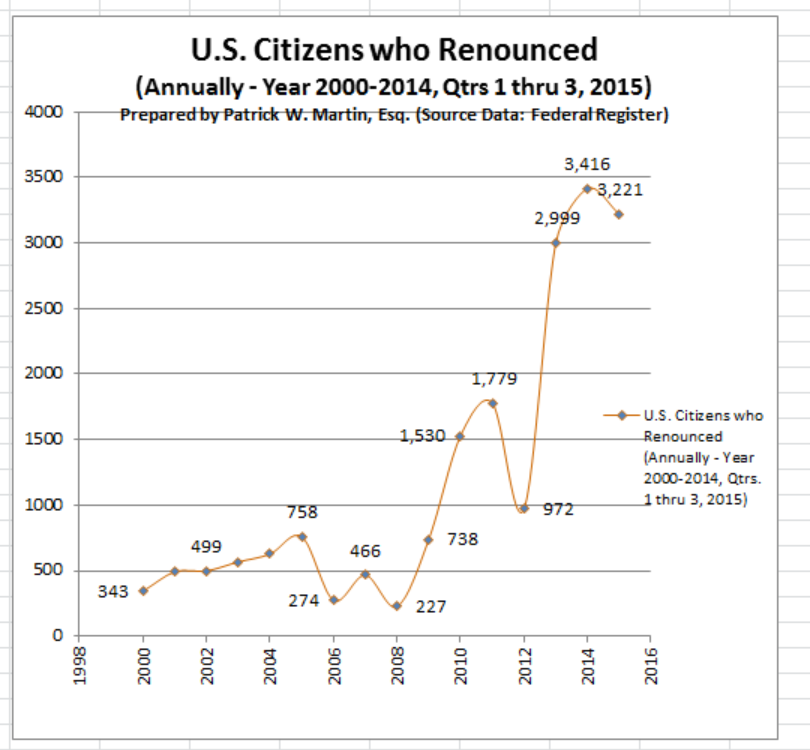

The vast majority of the USCs or LPRs who I see who renounce or abandon their citizenship or LPR status, are living outside the United States and in most cases have spent almost all (if not all) of their lives outside the U.S.

Does the IRS mean that a family living in Switzerland that have dual national family members are “. . . .simply hiding the accounts from the Internal Revenue Service . . . ” if they are using, for instance, a Liechtenstein Stiftung to hold their family assets as part of an estate plan recommended to them by their Swiss legal and tax advisers?

Does the statement that this IRS International Practice Unit focuses on ” . . . U.S Persons living in the United States . . . ” give USCs and LPRs residing outside the U.S. relief from the IRS perspective of USCs simply hiding assets from the Internal Revenue Service? Will IRS revenue agents be sophisticated enough to distinguish between these two different groups; U.S. resident versus non-resident USCs and LPRs? Will the law be applied differently with respect to these resident versus non-resident U.S. taxpayers?

What role will these IRS “International Practice Units” play in forming perceptions and molding ideas of IRS revenue agents who have had little to no life experience in international affairs, multi-national families, global finance and international business operations?

More observations to come from specific IRS “International Practice Units.

U.S citizens (USCs) and Lawful Permanent Residents (LPRs): Caution When Making Gifts. US Tax Court Recently Ruled a 1972 Gift by Sumner Redstone Still Open to IRS Challenge

The statute of limitations is one of the most important considerations for any individual when considering what tax consequences the Internal Revenue Service (“IRS”) might argue they have for years past. This can occur many years into the future as explained further below.

Former USCs and LPRs can be in a particularly precarious position, as was recently demonstrated by a U.S. Tax Court case for a gift that was made decades ago in 1972. See, Redstone vs. Commissioner (TCM 2015-237). Although this U.S. Tax Court case involving Sumner Redstone had nothing to do with renunciation of citizenship, it shows how the IRS can reach back many years and even decades in assessing taxes it claims are owing. The newly (in year 2010) added IRC Section 6501(c)(8) makes this highly likely under current revised law.

- Transfers to U.S. Beneficiaries (e.g., U.S. resident or citizen children or grandchildren who might receive gifts or bequests from a “Covered Expatriate” the former USCs or “long-term resident” – Green Card Holders)

Former USCs and any U.S. beneficiaries of theirs (e.g., U.S. resident children or grandchildren who might receive gifts or bequests from the former USCs) should be cognizant of the statute of limitations. See a prior post from 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

As this prior post noted, there are at least three basic scenarios when there is no statute of limitations for federal tax matters are as follows:

1. The former USC or LPR does not file a U.S. income tax return, when they had a requirement to so file. IRC Section 6501(c)(3). See a post from 2014, When do I meet the gross income thresholds that require me to file a U.S. income tax return?

- Fraud when Tax Return Filed

2. There is fraud on the part of the taxpayer (e.g., the taxpayer intentionally does not report income). IRC Sections 6501(c)(1), (c)(2).

- Missing Information on Tax Return Filed – re: International Matters

3. The USC or LPR fails to report certain foreign transactions, including inadvertently neglecting to report. IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act” which also created FATCA. The types of transactions set above in the table provides a brief summary of when transactions can give rise to an “open” statute of limitations period. In other words, as many years and decades can pass (see Redstone 1972 gift transaction) before the IRS ever has to make a proposed assessment of taxes and penalties. These include numerous ownership or economic interests in foreign (non-U.S.) companies, partnerships, foreign trusts, foreign investment accounts, among others.

This is indeed one of those areas where the IRS can argue a “gotcha moment”; simply because the former USC or LPR was not aware of the extremely complex rules of reporting assets (normally in their own country of residence outside the U.S.). The consequences to these families can go on indefinitely, per post from September 2015, Finally – Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

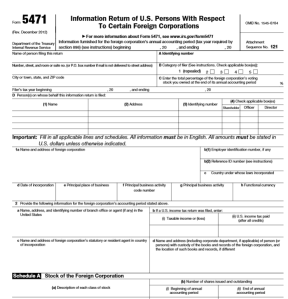

For a more in depth review of the international (non-U.S.) transactions that give rise to this reporting, see IRS Forms 3520, 3520-A, 5471, 8865, 5472, 8938, 8858, 926 among others.

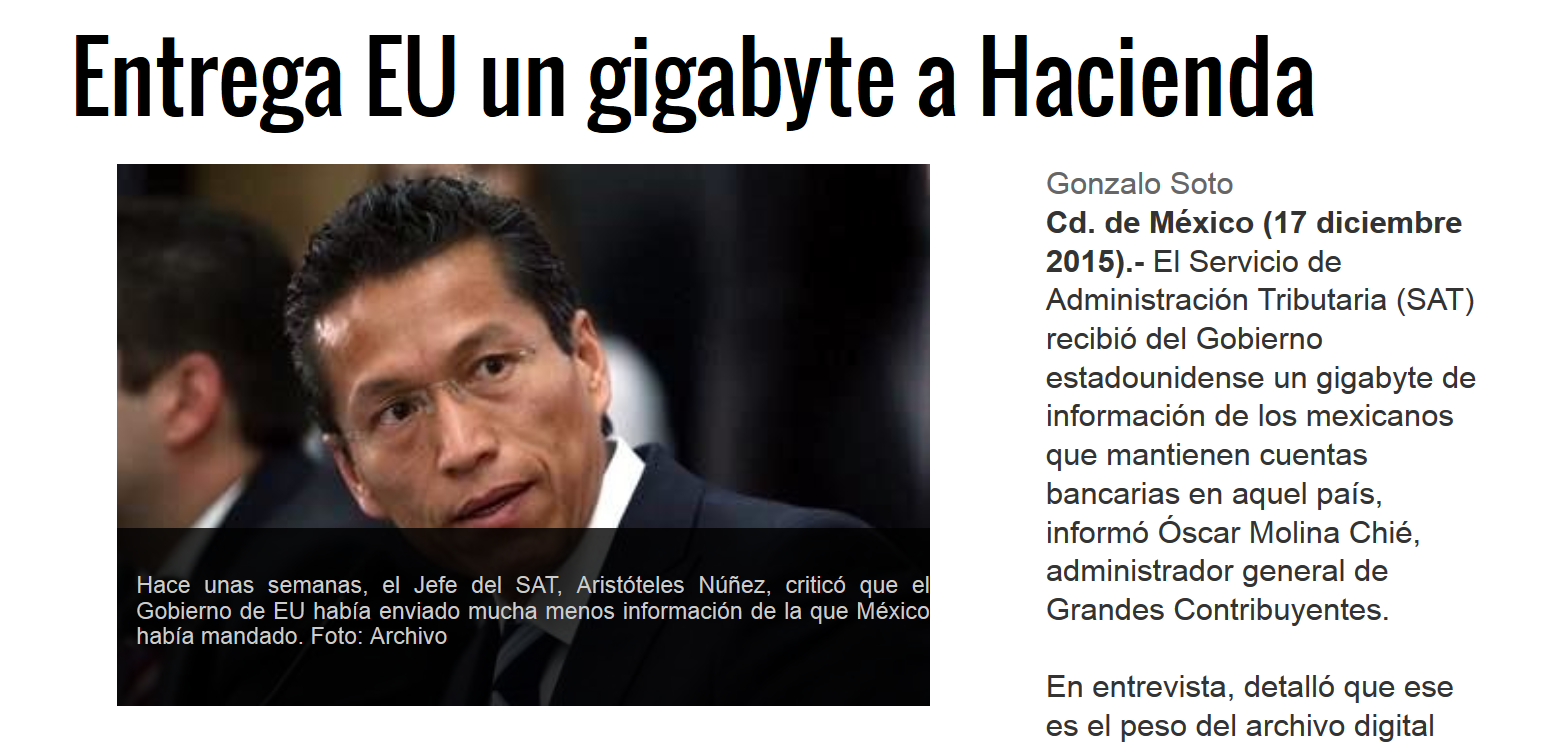

Foreign Government Receives a “FATCA Christmas Gift” from IRS: 1 Gigabyte of U.S. Financial Information

The last post discussed how the director of the Mexican tax administration was critical of the U.S. federal government for not providing FATCA information on U.S. financial accounts. See, Foreign Government Criticizes U.S. Government for  NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

The automatic exchange of bank and financial information is driven by the U.S. Treasury driven Intergovernmental Agreement (IGA).

As a follow-up, the Mexican newspaper Reforma reported on the 17th of December that the U.S. just provided Mexico’s treasury with a gigabyte of Mexican taxpayer information regarding U.S. financial and bank accounts. See, Entrega EU un gigabyte a Hacienda, dated Dec 17, 2015.

This news comes on the heals of the earlier criticism by the Commissioner of the Mexican IRS (SAT – Servicio de  Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Finally, the article emphasized that Mexico has sent the IRS information regarding Mexican bank accounts of U.S. citizens.

The question is how much Mexican bank and financial information has actually been provided by SAT of the hundreds of thousands (if not more than 1 million) dual national taxpayers, who are citizens of both Mexico and the U.S.? See, Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand, dated January 28, 2015.

Foreign Government Criticizes U.S. Government for NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts

This news is ironic. The U.S. government has chastised various banks and governments around the world since 2009 for not providing financial information on U.S citizens (USCs) and other U.S. taxpayers regarding their foreign bank and financial accounts. See, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior, posted Sept 8, 2014.

Now, it is foreign governments’ turn, to criticize the U.S. Treasury and IRS for not keeping up with its promises to provide U.S. financial and bank information on taxpayers of their countries pursuant to all of the FATCA Intergovernmental Government Agreements (IGAs) that were pushed so hard by U.S. Treasury. See, FATCA IGA with Hong Kong Signed: U.S. Citizens and Lawful Permanent Residents Residing in or Around Hong Kong Need to Know, posted on Nov. 17, 2014.

The Commissioner of the Mexican IRS (SAT – Servicio de Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez just announced that the U.S. government is not holding up its side of the bargain under the U.S.-Mexico IGA. See, the Dec. 12, 2015 article en the national Mexican newspaper, El Universal, EU incumple entrega de informacion: SAT: Mexico ha hecho su parte, asegura Aristóteles Núñez

The article, which is in Spanish, explains that Mexico has complied with its obligations under the IGA by providing detailed information about U.S. taxpayers with accounts in Mexican financial institutions to the U.S. government. However, the U.S. government has not complied with its side of the bargain. The news report says no specific details were provided by Mr. Núñez about what type of information was provided.

Revocation or Denial of U.S. Passport: More on new section 7345 (Title 26/IRC) and USCs with “Seriously Delinquent Tax Debt”

New Section 7345 completely modifies how U.S. citizens (“USCs”) living and traveling around the world have to now consider very seriously actions taken by the Internal Revenue Service (“IRS”). It is the IRS which now holds the power under this new law that requires the U.S. Department of State (“DOS”) to revoke or deny to issue a U.S. passport in the first place.

New Section 7345(e) provides in relevant part as follows: “upon receiving a certification described in section 7345 of the Internal Revenue Code of 1986 from the Secretary of the Treasury, the Secretary of State shall not issue a passport to any individual who has a seriously delinquent tax debt described in such section. . . ” [emphasis added].

This new law mandates (not at the discretion of the DOS) that various U.S. passports be denied at the direction of the IRS. Once the IRS issues the certification of “seriously delinquent tax debt.”

All it takes, is for the IRS to claim tax or penalties are owing of at least US$50,000 through an assessment (plus start a lien or levy action).

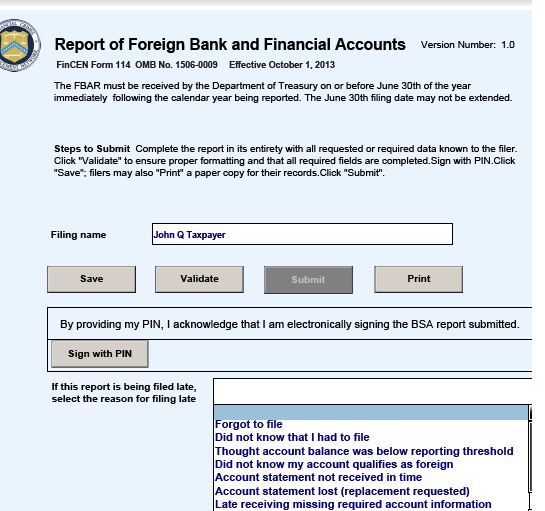

Of course, US$50,000 sounds like a large sum for many modest USCs, until an individual understands that there are a host of international reporting requirements for taxpayers. Specifically, the IRS can impose a US$10,000 penalty for each violation of failing to complete and file various IRS information forms; EVEN IF NO income  taxes are owing. See IRS website – FAQs 5 and 8 regarding civil penalties (see also How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas).

taxes are owing. See IRS website – FAQs 5 and 8 regarding civil penalties (see also How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas).

For a summary of these forms and filing requirements, see a prior post, Oct. 17, 2015, Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

Indeed, our office has seen and assisted numerous taxpayers around the world where the IRS has assessed tens of thousands, hundreds of thousands and in some cases in excess of US$1M (in proposed assessments) against an individual for failure to simply file information reporting forms. See, for instance, a prior post on Nov. 2, 2015, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

Also, we have seen several IRS assessments of income tax (not just penalties) against individuals of hundreds of thousands of dollars which are not supported by the law. For instance, it is not uncommon for the IRS to issue a “substitute for return” alleging income taxes owing. See, How the IRS Can file a “Substitute for Return” for those USCs and LPRs Residing Overseas, posted Nov. 8, 2015. We have a number of those cases pending, where the IRS has taken erroneous information and made such assessments against USCs residing and working outside the U.S. for much if not most of their professional lives.

New Section 7345 requires that USCs, wherever they might reside, take great care in knowing about any actions the IRS might be taking against them; as to tax and penalty assessments, whether or not they are supported under the law.

One basic method of learning more about the activities of the IRS is to make a transcript request directly to the IRS regarding the status of a USC’s federal tax status according to IRS records. See, IRM, Part 21. Customer Account Services . . . Section 3. Transcripts.

It is also possible for the USC to obtain additional tax information from the IRS through a Freedom of Information Act (“FOIA”) request.

Denial of U.S. Passports: President Obama and Congress Pass Law that will Require Department of State to Deny a U.S. Passport for a “Seriously Delinquent Taxpayer”

Entry in and out of the U.S. has just gotten more problematic under a new law for those U.S. citizens who the IRS asserts owes taxes. A new statutory concept has been added to the tax law called “seriously delinquent tax debt”; which is defined by new IRC Section 7345 as a tax that has been assessed, is greater than US$50,000, and where a notice of lien has been filed or levy made.

Prior posts have addressed current legal requirements surrounding social security numbers for U.S. federal tax compliance purposes. See, USCs without a Social Security Number (and a Passport) “Cannot?” Travel to the U.S., posted on May 17, 2015.

Other posts have focused on the dilemma facing U.S. citizens (USCs) who have no social security number (“SSN”). See an older post (23 July 2014) – Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The Joint Explanatory Statement of the Committee of the Conference provides the key provisions summary of the law as follows:

Present Law

The administration of passports is the responsibility of the Department of State. [“Passport Act of 1926,” 22 U.S.C. sec. 211a et seq.] The Secretary of State may refuse to issue or renew a passport if the applicant owes child support in excess of $2,500 or owes certain types of Federal debts. The scope of this authority does not extend to rejection or revocation of a passport on the basis of delinquent Federal taxes. Although issuance of a passport does not require a social security number or taxpayer identification number (“TIN”), the applicant is required under the Code to provide such number. Failure to provide a TIN is reported by the State Department to the Internal Revenue Service (“IRS”) and may result in a $500 fine.

***

Senate Amendment

Under the Senate Amendment, the Secretary of State is required to deny a passport (or renewal

of a passport) to a seriously delinquent taxpayer and is permitted to revoke any passport

previously issued to such person. In addition to the revocation or denial of passports to delinquent taxpayers, the Secretary of State is authorized to deny an application for a passport if the applicant fails to provide a social security number or provides an incorrect or invalid social security number. With respect to an incorrect or invalid number, the inclusion of an erroneous number is a basis for rejection of the application only if the erroneous number was provided willfully, intentionally, recklessly or negligently. Exceptions to these rules are permitted for emergency or humanitarian circumstances, including the issuance of a passport for short-term use to return to the United States by the delinquent taxpayer.

The provision authorizes limited sharing of information between the Secretary of State and

Secretary of the Treasury. If the Commissioner of Internal Revenue certifies to the Secretary of

the Treasury the identity of persons who have seriously delinquent Federal tax debts as defined

in this provision, the Secretary of the Treasury or his delegate is authorized to transmit such

certification to the Secretary of State for use in determining whether to issue, renew, or revoke a

passport. Applicants whose names are included on the certifications provided to the Secretary of

State are ineligible for a passport. The Secretary of State and Secretary of the Treasury are held

harmless with respect to any certification issued pursuant to this provision.

The Supreme Court Denies Certiorari for USC Taxpayer Who Claimed Foreign Earned Income Exclusion

The U.S. Supreme Court only rarely takes tax cases for certiorari review. It is common that no more than one federal tax case is reviewed by the U.S. Supreme Court during their entire annual term.

Accordingly, it was not surprising that the U.S. Supreme Court refused to hear a decision of a Hong Kong-based flight attendant who as a U.S. citizen took the foreign earned income exclusion (“FEIE”) pursuant to IRC Section 911 on all of her income. The Treasury Regulations §1.911-3(a) have a specific rule regarding source of income and provides: “Earned income is from sources within a foreign country if it is attributable to services performed by an individual in a foreign country or countries.”

The IRS assessed tax and a 20% “negligence” penalty against the Hong Kong based flight attendant Ms. Yen-Ling K. Rogers. Judge Cohen of the U.S. Tax Court wrote the 2013 opinion, Rogers vs. Commissioner, TC Memo. 2013-77 – U.S. Tax Court

The Court found the following facts and made the following legal determinations:

–

“Yen-Ling K. Rogers (petitioner) was a U.S. citizen and a bona fide resident of Hong Kong. She worked as a flight attendant for United Airlines (United) on international flights based out of Hong Kong International Airport. . . Section 61(a) specifies that “[e]xcept as otherwise provided”, gross income includes “all income from whatever source derived”. Although most countries employ territorial tax systems, the United States employs a worldwide tax system–it taxes its citizens on their income regardless of its geographic source. See Crow v. Commissioner, 85 T.C. 376, 380 (1985) (“The United States was historically, and continues to be, virtually unique in taxing its citizens, wherever resident, on their worldwide income, solely by reason of their citizenship.”) . . .” [emphasis added]

–

The Tax Court went on to find that the working time of the flight attendant over international waters could not be apportioned to or treated as “foreign earned income” as defined by the statute. Accordingly, it said:

–

“Consistent with this regulation, this Court has held that a U.S. taxpayer is allowed the foreign earned income exclusion only with respect to wages earned while in or over foreign countries and not for wages earned in international airspace or in or over the United States.”

See prior posts on the FEIE; The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed, April 21, 2014.

See also USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms, dated March 17, 2014 that discusses in some detail IRS Form 2555.

The Court of Appeals for the District Of Columbia upheld the Tax Court and the Supreme Court let stand the Court of Appeals decision.

international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc. Filers.

Filers. other creditors . . .”?

other creditors . . .”?