Month: March 2015

The Problem with PFICs! “Avoid PFICs Like the Plague”

There are typically numerous tax issues that USCs and LPRs need to consider prior to renouncing their citizenship; or abandoning th eir lawful permanent residency status.

eir lawful permanent residency status.

One of the most confusing comes from the complex rules of a so-called “PFIC” – the acronym for a “passive foreign investment company.” A prior post in March 2014 discussed the basics of these U.S. tax creatures – “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Most USCs and LPRs with basic mutual fund investments in their country of residence have PFICs and probably don’t even know it.

The IRS and Treasury have recently spent much attention and resources to the regulation of PFICs. In January of 2014, temporary regulations were issued regarding PFICs. See, Regulations §1.1291–0T, et. seq.

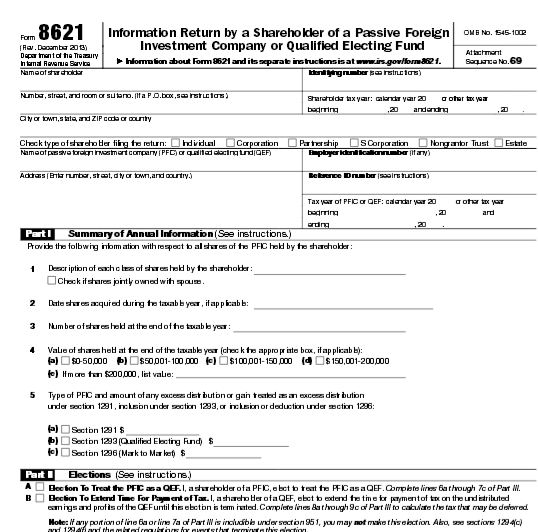

One of the many new requirements of these regulations are annual information filing requirements. This means that a U.S. taxpayer (e.g., U.S. citizen or LPR) residing outside the U.S., must file an annual report on IRS Form 8621.

- When Might You have a PFIC?

Taxpayers who have simple passive investments in mutual funds based outside the U.S.. e.g., in their country of residence, almost always have PFICs. There is no percentage ownership threshold in the foreign entity that triggers PFIC tax consequences. An ownership interest of 0.000001% triggers the consequences if either the “income test” or “asset test” are satisfied. Other type of investment funds in the form of a legal entity also typically qualify as a PFIC.

Specifically, a PFIC is a foreign corporation in which a U.S. person has some ownership in (without any percentage threshold requirement) if (i) at least 75% of its gross income is passive income (the “income test”), or (ii) at least 50% of its assets produce passive income (the “asset test”). See IRC § 1297(a).

Also, many retirement funds in various countries (including both private and many government run retirement plans) typically fall into the category of a PFIC. For instance, the Singapore retirement fund system, Central Provident Fund (“CPF”), is actually created by the government, but Singapore taxpayers who are obligated to contribute to the retirement fund will select various mutual funds to invest in through the CPF. Hence, these mutual fund investments are PFICs. See also the technical paper regarding Mexican retirement funds that argues, WHY MEXICAN RETIREMENT FUNDS SHOULD NOT BE SUBJECT TO THE NEW REPORTING REQUIREMENTS UNDER IRC SECTION 1298(f).

- Ugly Tax Consequences of a PFIC

PFICs are taxed to the U.S. taxpayer in a very complicated manner compared to taxation of U.S. based mutual funds or other U.S. based investments. In short, the income earned from PFICs, under the default regime, are taxed at the ordinary income rates, and for past years are typically taxed at the highest marginal ordinary income tax rate is 39.6% (even if the income would otherwise qualify for qualified dividend or long-term capital gains rates – which are taxed at no more than 20%).

There are three alternative regimes for how a U.S. investor is taxed in a PFIC: (i) the “excess distribution” regime (which is the default regime); (ii) the qualified electing fund (“QEF”) regime and (iii) the market-to-market (“MTM”) regime. Each of these regimes will be discussed in later posts.

One key point to know is that most foreign investment funds do not keep records and account for income and expenses in a manner that even allows a U.S. taxpayer to report accurately under the QEF or MTM regime, even if such treatment provides a lower overall U.S. tax.

More on how PFICs are taxed in a later post.

- Even Uglier Tax Reporting – Compliance Consequences of PFICs Driven by FATCA

Finally, the 2010 FATCA legislation has led to the new regulations that now require annual reporting of PFICs. This is done on IRS Form 8621. It is a laborious form and requires extensive and detailed information.

The consequences of not reporting can lead to disastrous tax results. See a prior post from March 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

- Why You Don’t Want to Die with a PFIC or Gift a PFIC Away (even to Your Favorite Charity or Spouse).

Lastly, a later post will explain in more detail why a USC or LPR generally wants to avoid PFICs if at all possible. Many countries require their residents to contribute on a mandatory basis to retirement funds that invest in mutual funds, which may not allow a USC to avoid PFICs. One of the principle reasons to avoid PFICs is the income tax that arises and is owed by the U.S. person, even if he or she tries to give the PFIC away. A gift of a PFIC will typically cause an income tax to the donor in addition to the estate/gift tax rules. This is true for gifts to charity and even to your own spouse.

- Why You Should Avoid PFICs Like the Plague

At the end of the day, the above complications, mean that most USCs and LPRs residing overseas should “avoid PFICs like the plague”.

In the context of USCs who wish to renounce their U.S. citizenship, they will not be able to avoid “covered expatriate” status if they have not complied with these PFIC rules, as they will not be able to “certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The ugly consequences of PFICs can be summarized as follows:

- Higher income tax rate than U.S. based investments on the earnings of the investment, at least under the default method;

- Practically impossible to report the earnings on a more favorable MTM or QEF method;

- Extensive information reporting requirements annually;

- Open ended statute of limitations in favor of the IRS to audit all items on the tax return, for failure to properly file IRS Form 8621;

- Paying a U.S. income tax, even if you gift away the PFIC to charity or to your spouse;

- Trying to even explain effectively the consequences of a PFIC to your tax return preparer; and

- Being subject to the “forever taint” of being a “covered expatriate” for failure to comply with the PFIC rules. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

The IRS Can Make an Assessment of Taxes and Penalties and Ask Questions Later

Taxpayers have a distinct disadvantage under the law vis-à-vis the IRS, since the law creates a “presumption of correctness” in favor of the IRS determination of taxes owing by any particular taxpayer.

This concept is decades old and is found in U.S. Supreme Court precedence at least as far back as 1933, where the Court in Welch v. Helvering (290 U.S. 111 (1933)) explained:

The Commissioner of Internal Revenue resorted to that standard in assessing the petitioner’s income, and found that the payments in controversy came closer to capital outlays than to ordinary and necessary expenses in the operation of a business. His ruling has the support of a presumption of correctness, and the petitioner has the burden of proving it to be wrong. Wickwire v. Reinecke,275 U. S. 101; Jones v. Commissioner, 38 F.2d 550, 552. [emphasis added]

This continues to be the law to this day.

What this means for taxpayers, particularly United States citizens and lawful permanent residents (“LPRs”) who reside outside the U.S., is that the IRS will often make erroneous tax determinations; yet the calculation of the amount of tax owing is presumptively correct.

The individual has the burden of proving the government wrong.

As an international tax practitioner, I have seen some of the most farfetched tax assessments by the IRS in the international context. If the IRS uses bad or incomplete information and then produces a tax assessment result, it is like the old computer saying; “junk in junk out.”

The IRS almost always, by definition, has incomplete information for taxpayers residing overseas. For that reason, it is not uncommon for them to make statutory notices of deficiency that are not supported by the law or the facts. See, the IRS explanation of a Notice of Deficiency CP3219N (“90-day letter”) proposing a tax assessment. Understanding Your CP3219N Notice

This power of the IRS under the law, is also compounded by the ability of the IRS to file a “substitiute return” for those USCS and LPRs residing overseas. See a prior post from November 2014, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas.

U.S. Department of State has Allowed (Starting in at least 2013) USCs to Keep their U.S. Passports After Oath and Prior to Receiving CLN

Washington Post journalist, Ms. had an interesting article on March 3, 2015, titled Yes, the State Department can jump on a problem and fix it in record time.

Washington Post journalist, Ms. had an interesting article on March 3, 2015, titled Yes, the State Department can jump on a problem and fix it in record time.

The focus of the article was that the U.S. Department of State can indeed fix a problem (in this case how and when U.S. passports are taken from U.S. citizens who take the oath of renunciation).

The article was a bit of a surprise to me, as I have had experience with several clients where the Consulate offices have indeed allowed the U.S. citizen to physically maintain their U.S. passport after taking the Oath of Renunciation (Form DS-4080, Oath of Renunciation of the Nationality of the United States) but prior to actually receiving the “Certificate of Loss of Nationality” (“CLN”).

After a U.S. citizen has formally renounced (or relinquished) their U.S. citizenship, the U.S. Department of State provides a CLN. This form can be located here at – Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN)

You can go to the page “U.S. Department of State” under “Resources” for further U.S. Department of State Documents related to loss of nationality.

Sometimes, the U.S. Department of State will take several months to process the file in Washington D.C., before they actually issue the CLN. I have had cases (worst case scenarios) that take upwards of 9-10 months. See, The IRS does not give a “Certificate of Expatriation” or similar tax document . . .

However, my experience on several cases is that consular officer will generally allow t he individual to physically keep the U.S. passport until the CLN is actually issued and received by the individual in exchange for their passport. This has been the case for some 2 +/- years.

he individual to physically keep the U.S. passport until the CLN is actually issued and received by the individual in exchange for their passport. This has been the case for some 2 +/- years.

This procedure has been formalized in the Foreign Affairs Manual which added the additional key language in paragraph (4) regarding U.S. citizens who need their passport for travel to the U.S.

Key Concepts of Senate Finance Chairman Hatch’s Proposal Re: “Non-Resident U.S. Citizens”

The complete report can be located at the Senate Finance Committee website at Comprehensive Tax Reform for 2015 and Beyond – Senate Republican Staff –

The crucial policy considerations are set out in the report. The key paragraph of the report is reproduced here:

The principle idea is to impose U.S. income taxation on U.S. sources only for U.S. citizens residing overseas. The report leaves many unanswered questions. One of those questions is how to integrate the “expatriation tax rules” into such a concept? There is one sentence addressing this point, which contemplates the “mark to market exit tax” will continue as part of the law, if such a proposal were to become law.

The report does not discuss how the U.S. transfer tax system (U.S. estate, gift and generation skipping transfer taxes) might be reformed. Current law, imposes worldwide U.S. estate, gift and generation skipping transfer taxes on the worldwide assets of a U.S. citizen.

Time will tell if such a proposal gets any political traction in Congress or at the White House.

Will Congress and the President Finally Act in 2015 to Repeal or Modify U.S. Citizenship Based Taxation?

U.S. citizenship based taxation has been the law since its origins from the U.S. civil war. See, The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Throughout most of the last 100+/- years, there has never bee n a repeal of U.S. citizenship based taxation. Indeed, it is difficult to locate any legislative proposals from years past (if there were any) that proposed such a modification.

n a repeal of U.S. citizenship based taxation. Indeed, it is difficult to locate any legislative proposals from years past (if there were any) that proposed such a modification.

However, it is worth noting the following string of events over the last 18 months, which may indicate U.S. citizenship based tax reform could be possible:

- For the first time, both political parties and the President have identified issues with the current U.S. citizenship based taxation rules which they have proposed to modify;

- Second, there have been a number of serious proposals to modify and repeal U.S. citizenship based taxation. See, the American Citizens Abroad proposal (ACA proposal). See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, among several others;

- Third, a little over a year ago, the Senate Finance Committee, which was then controlled by Democrats identified U.S. citizenship based taxation as an international competitiveness issue. See, Senate Finance Report on International Competitiveness Identifies Possible “Expatriation” Reforms for U.S. Citizens Residing Overseas. Will U.S. citizens who live outside the U.S. find any relief soon?

- Fourth, in December of 2014, the the Senate Finance Committee Republican Staff issued a detailed report dedicating substantial discussion and analysis to “Non-Resident U.S. Citizens”. See pages 282 and 283 of the Comprehensive Tax Reform for 2015 and Beyond – Senate Republican Staff

- Fifth, the President in his Green Book proposal in February 2015, addressed (although in only the most narrow of circumstances), the need for reform of U.S. citizenship based taxation. See, The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group

This is the first time in my career, where both political parties and the President are at least talking about the possibility of tax reform in this area.

There is one key piece of the legislative puzzle missing from the above picture. The House has not weighed in on a proposal to modify substantially or repeal U.S. citizenship based taxation. See, former House Ways and Means Committee Chair Camp’s proposal to modify substantially international tax policy and rules (Making America A More Attractive Place To Hire and Invest: International Tax Reform). These House proposals do not include U.S. citizenship based taxation reform. In addition, I am not aware of any Democrats in the House who are pushing such a reform.

Even if there is approval in both the Senate and with the President (as there has been in other major legislative reform proposal, such as immigration), it is entirely possible the House will block any such U.S. citizenship based tax reform.

What Collection Efforts (if any) will the IRS Undertake to Collect U.S. Income Taxes from the Gain from the Sale of the London Mayor’s House?

What Collection Efforts will the IRS Undertake to Collect U.S. Income Taxes from the Gain from the Sale of the London Mayor’s House?

U.S. citizens and lawful permanent residents (LPRs) residing overseas must always consider what collection efforts the U.S. government might undertake for taxes owing.

I have posed the question regarding the London Mayor, Boris Johnson, since it raises a number of unique issues. First, under the law, the IRS should administer Title 26 the same for high profile, political, non-political, educated and uneducated individuals. In practice, the judgment of a particular Revenue Agent (and his or her manager) often weighs into how a case is pursued; or not pursued.

The fact that Boris Johnson is a public individual, does impose certain limitations on the ability to investigate his particular case. That is largely because of Department of Justice policy. As explained in the last post, only the Tax Division of the Department of Justice can authorize warrants of public officials, which presumably would extend to London Mayor Boris Johnson. See, 6-4.130, Search Warrants.

Previous posts have explained some of the basic legal tools at the disposal of the IRS and the Department of Justice, Tax Division. See an earlier post, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations and the following excerpt:

1. INFORMATION – The collection of asset and financial information under FATCA has a very “long arm” around the world. Indeed, the image of the Uncle Sam octopus published in the June 28, 2014 article in the The Economist entitled Taxing America’s diaspora: FATCA’s flaws captures well the idea of the reach of FATCA.

2. INFORMATION VS COLLECTION – However, enforcing tax assessments and penalties and collecting against assets located outside the U.S. is a very different legal question, without such a “long arm”; simply because the reach and jurisdiction of U.S. law is necessarily limited and regularly in conflict with local laws of different countries.

To say it another way, Uncle Sam can indeed enforce the collection of financial and asset information under FATCA, due to the economic costs and ramifications to financial institutions and their investors if they did not comply with the automatic information exchange. However, Uncle Same cannot simply enforce the collection of U.S. taxes and penalties through the worldwide financial institutional network, the same way it can in the U.S.

The U.S. has broad lien, levy and seizure powers under U.S. tax law. The IRS can simply seize assets from U.S. bank accounts without going to a judge or court for final (or jeopardy) tax assessments provided they comply with various provisions of the law. This is not a typical concept in the law for other creditors (other than the IRS) who must generally first take steps through the courts to get some type of judicial action (e.g., a court order) before simply seizing and taking assets from an individual.

The IRS’s broad lien and levy powers against assets, however, has significant limitations overseas. See the 1998 Treasury Report – Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs, I hav e worked with IRS Revenue Officers who specialize in international collection matters who argue and assert they can merely exercise this lien and levy power overseas against foreign financial institutions. However, this is where the power of the IRS comes to a screeching halt (or at least a major slowdown); when the collection of overseas assets is at stake.

e worked with IRS Revenue Officers who specialize in international collection matters who argue and assert they can merely exercise this lien and levy power overseas against foreign financial institutions. However, this is where the power of the IRS comes to a screeching halt (or at least a major slowdown); when the collection of overseas assets is at stake.

The IRS is not without remedies to collect foreign assets, but it is not a simple process; if it can be done at all in any particular circumstance.

Finally, it is worth noting that a powerful tool at the disposal of the IRS (working in conjunction with the Department of Homeland Security) is the TECs database, which tracks the movement of individuals, specifically including U.S. citizens, who are necessarily U.S. taxpayers. See a prior related post: “Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –

Time will tell, how this tool is used in practice against U.S. citizens residing overseas; particularly those with accounts in various banks that have been the highlight of U.S. international tax evasion investigations, such as UBS, Credit Suisse and HSBC (see, The Guardian, US government faces pressure after biggest leak in banking history).