Month: July 2014

529 College Plans – Funded by Former USCs and LPRs (“Long-Term” LPRs)

There is a basic tax planning opportunity for U.S. taxpayers who wish to fund the costs of higher education for family or friends. These are referred to as “529 Plans” with reference to the tax code section – IRC Section 529. In short, a 529 trust is established and funded with contributions for the benefit of named beneficiaries.

The principle benefit of a 529 plan, is that the income earned from the investments inside the 529 trust fund are exempt from U.S. income taxation.

There are multiple plans that are operated by various institutions, principally in conjunction with various States in the United States. Qualifying higher education expenses also apply to about 350 non-U.S. institutions that currently qualify for distributions out of a 529 Plan; e.g., University of Cambridge, University of Dublin Trinity College, University of Edinburgh, University of Oslo, The University of York, University of Wollongong, etc.

Unfortunately, non-U.S. citizens who are not resident in the U.S. generally are not eligible to establish and form a new 529 plan.

These “529 Plans” fall expressly into the category of a “specified tax deferred account” under the law. See, IRC Section 877A(e)(2).

In short, the law causes the entire amount in the 529 Plan to be treated as distributed to the “covered expatriate” the day before the expatriation date, although no early distribution tax will apply. If a 529 Plan has $500,000, that will represent taxable income to the “covered expatriate” to the extent of the tax-free growth in the plan. For instance, if the individual funded $200,000 into this plan, in this example, and he or she is subject to the 39.6% tax rate upon “expatriation”, this means there will be US$118,800 less to pay for college and universities (i.e., $500,000 less the $200,000 invested; leaving $300,000 X 39.6% = US$118,800 of tax).

This is yet another example, of how and why it is so important to avoid “covered expatriate” status; if permitted by the law in any particular circumstances. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute, also see Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Careful thought should be taken for the range of considerations and U.S. tax consequences that can befall a former USC or long-term LPR.

The Risks to USCs and LPRs – Filing Late U.S. Income Tax Returns via the so-called “Streamlined” process

I previously posted a note about the so-called “Streamlined” process the IRS [which are now gone and removed from the IRS website] had announced in June 2012, Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking. I explained that legally speaking, there is no legal protection to the taxpayer provided by this administrative procedure.

The new “streamlined” procedure from June 2014 does not provide any additional legal protection or finality. To be blunt, the government has used the FBAR as a “trap” for the taxpayer. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II).

If the individual did not check the right box on Schedule B, Part III, therefore the government may well argue they were “willfully blind” of the requirements of filing FBARs, even if they did not know of the filing requirements. The FBAR regulations are extremely complex and I am confident few tax experts anywhere in the world could take a basic exam of what is a “financial interest in” and “signature authority over” such accounts according to these regulations and get more than about 75% (a “C” or maybe “D” grade) of these questions rights. See, Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer.

The problem with this streamlined process is there is no protection from penalties for failure to file tax returns, failure to file information returns, failure to file FBAR forms; nor from IRS audits of prior years (when the statute of limitations is still open), etc. In short, the IRS (or the Justice Department) can always fully pursue a USC or LPR who has not properly filed U.S. income tax returns, information returns on foreign assets or FBARs for prior years, as provided under the law.

In the meantime, the government will never be required to refund the so-called “5% miscellaneous offshore penalty” (which of course is not a penalty under the law in the first place), pursuant to the very terms of the Certification. The taxpayer waives ” . . . all defenses against and restrictions on the assessment and collection of the [5%] miscellaneous offshore penalty.” It is a one way street.

In addition, the individual is now subjecting themselves to potential greater liability in the event the government ever wants to challenge the certification made under penalties of perjury. Indeed, the certification is not drafted in the words of the taxpayer, but rather the U.S. federal government. Many practitioners have been analyzing and parsing the meaning of “negligence” and “inadvertence” and “mistake” that is a “good faith misunderstanding” of the requirements of the law. It’s entirely unclear how these terms will be interpreted by the government in any particular case. Certainly the vast majority of these cases that are entered into this system will not be challenged; if for no other reason the limited resources of the IRS.

However, there are so many ways they can be challenged against any particular taxpayer. What if a taxpayer threw away the monthly bank statements for the year 2012 regarding a foreign account? Will that be a breach of the Certification? Will all bets be off against the taxpayer? The terms of the certification seem to provide such a result.

I suspect we will see cases where the government will go after (selectively) some taxpayers who enter into the streamlined process. They cases they will select are the ones they think the taxpayer should have gone in under the OVDP. That will be the determination of the government, not the individual taxpayer; and hence can put the taxpayer in further jeopardy.

Finally, the most troubling issue of this program for U.S. residents, is they are agreeing to pay something that does not exist under the law and may have no correlation with any income taxes owing; i.e., the so-called “5% miscellaneous offshore penalty.” Why should a “good faith” taxpayer be paying any portion of their principal to the government, if they made an inadvertent mistake of what are typically very complex provisions in the tax law?

A basic example can demonstrate the injustice of this approach. Taxpayer Pierre, moves from France to the U.S. some 10 years ago. He was an accounting major in France and practiced as an accountant before becoming a business and property manager. His English is horrible and he relies upon a tax return preparer at “J&Q Blockhead Return Preparers” who only speaks English. His return preparer has never asked good questions, about if he has any non-U.S. assets, as he meets with him for 60 minutes each year after taking his W-2 and 1099 forms to the office as requested.

Pierre inherited from his non-U.S. citizen parents accounts in Switzerland and France with a value of US$3M and some real estate outside Paris worth approximately US$2.5M that generates rents monthly. His return preparer always sent his returns with the “No” boxes checked on Schedule B, Part III and never filed FBARs or IRS Form 8938. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938. Pierre was told by his French tax advisers, who are very sophisticated, that the U.S. should not levy tax on his European assets; but rather he should only pay tax in France and Switzerland on these assets. Assume the taxes withheld at source in Europe are greater than the U.S. income tax that would be generated on this income; hence he can fully credit (with the U.S. foreign tax credit) the U.S. federal income tax, except about $700.

Pierre reads the news release on a French news website of the new “streamlined” program announced by the IRS in June 2014. He asks his return preparer about it – who has no idea what he is talking about.

What is Pierre to do? Why should Pierre pay approximately US$325,000 (5% of US$6.5M) to participate in this program when he owes less than US$1,000 of federal income tax?

When Pierre discusses this press release with the manager at “J&Q Blockhead Return Preparers”; the manager says all customers are given a (1) a package of documents and a pamphlet that says “Do you have any foreign assets?” on page 37, paragraph 3; and (2) a free coffee mug with “J&Q Blockhead Return Preparers” prominently displayed. The manager at “J&Q Blockhead Return Preparers” tells Pierre – “you are not going to pin this one on me!”

How is the payment of US$325,000 that is not contemplated under Title 26, a correct result under the law?

If Pierre does not go into the streamlined program and files amended tax returns, will the IRS and Justice Department try to “Zwerner” him (assess multiple year 50% willfulness penalties – arguing he was “willfully blind”)? What if they start an audit and investigation and ask the return preparers at “J&Q Blockhead Return Preparers” about the case with the response being “We tell all our customers they have to report their foreign assets and have it in writing. See our pamphlets and website.”

That is the risk Pierre will have to take; (1) comply with the law under Title 26 as amended returns are contemplated and risk the government will pursue him for 50% willfulness penalties (as the failure to file IRS Form 8938 – should be only for 3 years at $10,000 per year) or (2) be forced into a “streamlined” procedure that will make him pay a large portion of his family inheritance from Europe to the U.S. since he did not file IRS Form 8938 or FBARs.

Ineligibeility for a SSN after Taking Oath of Renunciation – TINs, ITINs, EINs, etc.

USCs and LPRs residing outside the U.S. have been increasingly renouncing their citizenship and abandoning their lawful permanently residency status, respectively. In some cases, individuals who have lived virtually all (or all) of their lives in a country other than the U.S. are a lmost making a “knee jerk” decision to renounce.

lmost making a “knee jerk” decision to renounce.

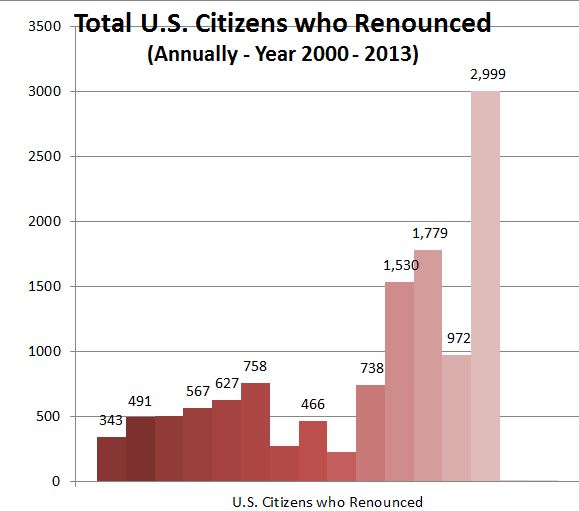

The statistics as to the absolute number and relative increases are astonishing. See, Wow, the number of 2,999 U.S. citizens who renounced in the year 2013 shattered the prior record set in 2011 of 1,782 renunciations. Why so many renunciations?

There is a practical problem for an individual who has renounced his or her U.S. citizenship prior to obtaining a Social Security Number (“SSN”). The individual will NOT be able to obtain a SSN once they have taken the oath of renunciation. See, *Why the Oath of Renunciation is Not the Opposite of the Oath of Allegiance

Of course, as prior posts have explained, an individual must have a “taxpayer identifying number” which must be a SSN for a U.S. citizen. However, the Social Security Administration will not allow an individual who has taken the oath of renunciation to apply for a SSN. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs

Also, see, Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The only way an individual can avoid becoming a “covered expatriate” is by filing U.S. federal income tax returns and being able to satisfy the certification requirement of Section 877(a)(2)(C). Accordingly, if a SSN is not available, the former citizen will need to file for an ITIN, as explained in previous posts.

U.S. Tax Court Rules Against Lawful Permanent Resident (LPR) in Abrahamsen

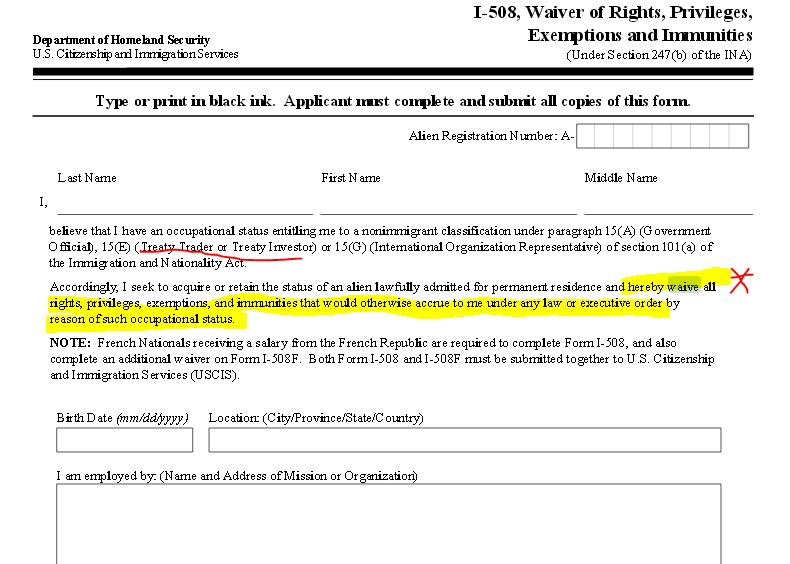

The U.S. Tax Court, in an opinion written by Judge Lauber (Abrahamsen v. Commissioner) placed much legal tax significance on the immigration form I-508 that Ms. Abrahamsen signed.

The Court noted this form, I-508, Waiver of Rights, Privileges, Exemptions and Immunities (Under Section 247(b) of the INA) specifically provides that the non-U.S. citizen “waive all rights, privileges, exemptions and immunities which would otherwise accrue to [her] under any law or executive order by reason of [her] occupational status.”

In that case, the individual was a Finnish citizen who eventually applied for lawful permanent residency. The immigration forms were not related to any specific tax form, such as the new IRS Forms W-8BEN; see, IRS Releases New IRS Form W8-BEN. * U.S. citizens and LPRs beware of completing such form at the request of a third party.

The takeaway from this opinion, is that individuals need to be aware of how signing a particular form (that is not a tax form) can have adverse tax consequences. In this case, the Court ruled that she had waived her benefits to IRC Section 893 by signing immigration Form I-508. The opinion of the Tax Court raises an interesting legal question about how signing a form (I-508) can seem to override the statutory protection granted which provides protection to a qualifying “. . . employee [who] is not a citizen of the United States . . . “

Signing various tax forms can cause even greater risks for non-citizen taxpayers; e.g., IRS Form W-9 versus W-8BEN. See, FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information*

Fortunately for the taxpayer in the Abrahamsen case, she was not subject to the Section 6662 accuracy related penalty (“negligence” penalty) assessed by the IRS.

A subsequent post will analyze some potential U.S. tax consequences for individuals who sign immigration Form I-485, Application to Register Permanent Residence or Adjust Status

Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

U.S. citizens who meet certain income thresholds (currently about US$10,000 for individuals not filing married-jointly; and about US$20,000 for individuals filing married-jointly) who reside outside the U.S. have no choice but to obtain a SSN in order to file tax returns under U.S. law. See the specific income thresholds for who is required by law to file a U.S. tax return, here.

As explained in a previous post, under U.S. tax jargon a “taxpayer identification number” (TIN) is a broad definition and includes all of the following, which are TINs –

- U.S. Social Security Number (“SSN”) in the case of certain individuals (USCs, LPRs and those who have permission to work in the U.S. under a particular visa);

- “Individual Taxpayer Identification Numbers” (ITIN) in the case of other individuals who are not USCs or LPRs and not otherwise eligible for a SSN (another post will explain how ITINs are obtained);

- Employer identification numbers (EINs) for certain entities, such as corporations, partnerships and trusts.

Most importantly, the regulations specifically require a U.S. citizen to obtain a SSN to use it as the “taxpayer identifying number.” The relevant regulations provides that

The exceptions referred to above where a SSN is not required in these regulations are principally for individuals who are not U.S. citizens and not eligible to obtain a SSN. See, Social Security Numbers for Noncitizens as published by the Social Security Administration (“SSA”). Any U.S. citizen is eligible for obtaining a SSN. For information regarding applying for a SSN, see the SSA website.

Ironically, it can be very difficult (nearly impossible in some cases) for USCs who have spent most (if not all) of their lives outside the U.S.; considering the methods of proof required by the SSA when the Application For a Social Security Card (Form SS-5-FS) is submitted.

Once a SSN is obtained, the USC is required to complete IRS Form W-9 vis-a-vis third parties providing them proof of their status and SSN.

More will be discussed in later posts about how to get a SSN overseas from a U.S. Embassy and some Consulate offices. Also, see, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs.

Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

One issue on the minds of many United States Citizens (USCs) and Lawful Permanent Residents (LPRs) living overseas (overseas from a U.S. perspective – i.e., offshore from a U.S. perspective) is whether the IRS investigates these individuals.

The short answer is yes, with varying degrees of investigation; reviews or audits. Of course, not all individuals are audited or investigated. However, the new data that will be collected under FATCA will be an increasingly valuable source of information for the IRS. In practice, I am increasingly seeing the IRS automatically generate “substitute for returns” for individuals living overseas where no U.S. federal income tax return has been filed. In these cases, the IRS is receiving some type of income information (e.g., from a bank or company) and then issuing the substitute for return. See, IRM regarding “Substitute for return (SFR) and delinquent return procedures were developed to deal with taxpayers who do not file required tax returns.”

There are a host of techniques used by the IRS. A series of posts will discuss some of these techniques. There are also legal limitations imposed on the IRS and Justice Department when assets are located overseas. See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

First, there has been a much greater focus during the last 6 years on foreign, international tax matters. That focus continues under the current Commissioner.

Second, the IRS has been opening offices internationally in different countries. Most recently, an office in Beijing, China.

To learn more about the functions of the Tax Attachés (TA) and Deputy Tax Attachés (DTA) and how they serve in the IRS overseas Posts, see the IRM, 4.30.3 Overseas Posts

Third, with additional information that will be collected under FATCA (starting in 2015 for information for the calendar year 2014), the IRS will have additional information to sort, examine, audit, etc. This will undoubtedly cause more substitute for returns to be automatically generated by the IRS for those individuals who have not been filing U.S. income tax returns.

Fourth, the offshore voluntary disclosure program has been a treasure trove of information for the government regarding non-U.S. banks and non-U.S. advisers (bankers, accountants and attorneys).

Fifth, the deferred prosecution agreements entered into with various Swiss financial institutions will be an additional source of information regarding USCs and LPRs and their accounts and assets.

Sixth, the IRS has developed a number of methods of collecting, sorting and identifying information (including the information that will be collected above). For instance, in the Internal Revenue Manual provides the following, regarding USCs and LPRs, including those living overseas –

Section 18. Locating Taxpayers and their Assets (Cont. 1)

* * *

5.1.18.13.3 (05-20-2008)

Using Passport Information

- Use any new address or new asset information received from the passport office as discussed above.

- See IRM 5.1.12.25, Outgoing Mutual Collection Assistance Requests, if you determine that the taxpayer:

- resides in a treaty country, or

- has assets in a treaty country.

- The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. It contains information about individuals and businesses suspected of, or involved in, violations of federal law.

- For IRS field Collection,TECS provides two sources to help make contact with taxpayers or locate assets :

- Revenue officers can request that delinquent balance due taxpayers be entered into TECS, and the Department of Homeland Security (DHS) will then advise IRS when those taxpayers travel into the United States for business, employment, or personal reasons. The taxpayers entered into TECS for this purpose are on a DHS lookout indicators list. IRS employees must help maintain the TECS database by requesting that appropriate taxpayers be entered into TECS or be deleted from TECS. (See IRM 5.1.18.14.6.1 for criteria for including taxpayers in TECS data base.)

- Revenue officers can also request information housed in TECS on past travel that a taxpayer has made to and from the United States.

- Many of the taxpayers entered into TECS for a DHS lookout indicator are International ones because the cases usually concern persons who reside abroad. However, domestic taxpayers may also be entered into TECS if we have been unable to locate them and if they are believed to travel outside the US . Taxpayers placed on TECS are often not subject to ordinary administrative and judicial collection procedures because they frequently reside outside the jurisdiction of the US Courts. Information derived from placing a taxpayer on TECS can facilitate contact with these taxpayers or provide asset information which, in turn, may facilitate collection of their delinquent liabilities.

Note:

IRM 9.4.2.4.2.5.3, Other IRS Functions, also discusses TECS and prescribes the use of Form 5523, TECS Query Request, to request information from TECS. However, SB/SE Collection Field (FC) employees should not use Form 5523.

- Consider the following example as an illustration of how using TECS to place a taxpayer on the DHS lookout indicator list could help in your casework.

Example: A FC RO has a balance due taxpayer in his/her inventory and he determines the taxpayer resides in Norway. The RO transfers the case to International. The International RO determines the taxpayer is “Unable to Contact” and closes the case from open inventory. The RO requests that the taxpayer be placed on TECS. One year later, the taxpayer travels to the US and initially arrives at an airport in New York. Upon the taxpayer’s arrival, Customs and Border Protection (CBP) informs the TECS Coordinator where the taxpayer is ultimately traveling to, how long the taxpayer plans to stay, and on which flight(s) the taxpayer will be departing. The taxpayer will be staying in Denver for one week. The ROs who had previously worked the case had not been aware of any connection the taxpayer had to Denver. The TECS Coordinator notifies the group manager (GM) in International who is responsible for cases in Norway (the country in which the taxpayer resides). The International GM issues an OI to the Collection group working the location in Denver where the taxpayer is staying. The GM in Denver assigns the case to an RO, and the RO meets with the taxpayer and secures a financial statement. When this happens, the IRS learns about the taxpayer’s assets for the first time as other research methods and attempted contacts were unsuccessful. The RO provides the information to International and closes the OI. After the OI is closed, the International RO does further research once he/she is aware of the Denver nexus. He/she discovers the taxpayer has real property held in the name of a trust and files a nominee lien.

* * *

More posts to follow on specific steps taken regarding investigations by IRS of USCs and LPRs living outside the U.S.

Part I: Then and Now: Certificates of Loss of Nationality (CLNs)

How the world has changed since the 1960s; or rather how the world has remained the same and we humans have changed it so!?!

Imagine the shock and fear one might have if they learn they are a U.S. citizen while at the same time learning about U.S. citizenship based taxation of worldwide income regardless of where one lives. I use these terms purposefully, because a U.S. citizen who has spent almost all of their lives in the U.S., will likely have the sam reaction if they were born in another country and they were just told they should have been filing tax returns and detailed bank account reports for the last several decades under the law of that country (e.g., France, Canada, Libya, Mexico, South Africa, Germany, Eritrea, etc.). That person would probably be shocked and would also have some “fear” – depending upon which country is identified.

See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . . This “shock and fear” was recently on display with a client who realized (rather should I say – “thought”) he was a U.S. citizen and therefore a U.S. income tax resident. For more background on U.S. citizenship and taxation, see – Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs.

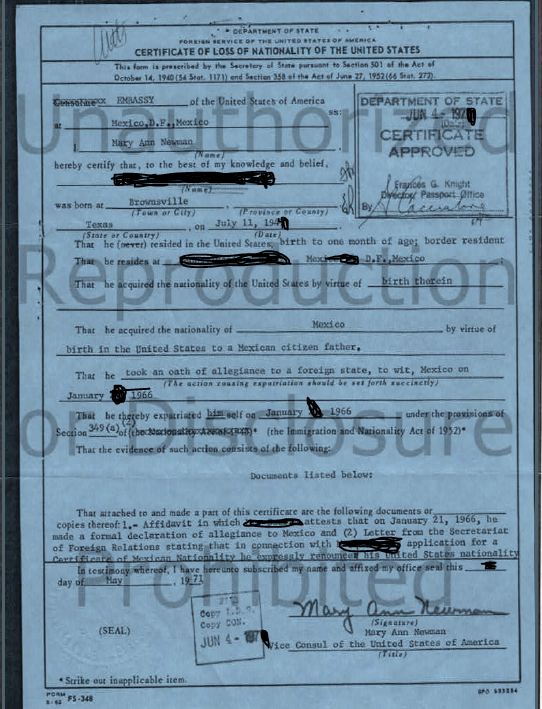

Ironically, the CLNs issued by the then U.S. Department of Sate versus the CLNs issued today are surprisingly similar in format and content. See Wide Window of Wait Times for CLN: One Month to 9 Months (or More?)

Imagine you have lived all of your life in your home country, for decades and decades. You were raised, educated and built your business or profession in your home country. Indeed you have become quite successful in your own country after a long life dedicated to your work.

However, by a pure act of arbitrariness (at least as far as you are concerned – since it was your mother who gave birth – without any input from you), you were born on U.S. soil. For those of us who live along the international border, this is a common occurrence.

Here in San Diego, the border crossing is one of the busiest land crossing in the world (if not the busiest). The U.S. federal government has reported (in the year 2000, which was presumably much less busier than today) it “ . . . processed over 41.5 million northbound passengers in personal vehicles and 8 million northbound pedestrians.” That is nearly 50 million going northbound, not counting the border crossing going southbound to Mexico.

The United States Department of Transportation reported that ” . . . Personal vehicles entered the United States nearly 96 million times in 2012, 33.1 million from Canada, and 62.7 million from Mexico, according to the U.S. Department of Transportation’s Bureau of Transportation Statistics’ (BTS). Border crossings also included 10.7 million trucks, 320 thousand buses, and 37 thousand trains in 2012 (Table 1).. . . ”

Needless to say lots of Canadians and Mexicans are born in the U.S. as part of the transit to and from the U.S., just along the borders.

This gentleman was born in the border town of Brownsville, Texas, many decades ago, where thousands of Mexicans are born to this day. He took an oath of allegiance to the Mexican government in the 1960s as was required at that time pursuant to the Mexican Constitution, so as not to lose Mexican citizenship. See, the 1997 article by Paula Gutierrez in the LMU of LA International and Comparative Law Review, Mexico’s Dual Nationality Amendments: They Do Not Undermine U.S. Citizens’ Allegiance and Loyalty or U.S. Political Sovereignty.

Recently, his U.S. citizenship and tax journey began after some 40+ years.

The redacted CLN from the 1970s is part of the story.

Subsequent posts will discuss the tax and other legal implications of this CLN, when it was issued, how and why;

- what the tax law said then versus now;

- what the immigration law said then versus now;

- what it meant (under U.S. immigration law) to take an oath of allegiance to a foreign country;

- the timing of when and what date is used for “renunciation” (how many years back in time?);

- what penalties (if any) he might have vis-à-vis U.S. law?

In this case, the basic fact that he never remembered taking these specific steps back when he was a teenager of 18 years of age and shortly thereafter as a young man.

He never notified the IRS of his USC renunciation (or maybe you prefer to call it relinquishment – though there is no clear legal distinction between these two terms) pursuant to Section 7701(a)(50). – See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

His story, fortunately has a very happy ending considering the application of Section 877, et. seq.

To be continued . . .

IRA Distributions – (Counter-intuitive Results) U.S. Tax Consequences to Former USCs and Long Term Residents (LPRs)

IRA Distributions – (Counter-intuitive Results) U.S. Tax Consequences to Former USCs and Long Term Residents (LPRs)

Those USCs who have renounced citizenship (or who are contemplating renunciation) and those LPRs who (were/are/will) fall into the category of “long-term residents” who have qualified retirement accounts, known as “Individual Retirement Arrangement” (“IRAs”) have special considerations to consider under IRC Sections 877, et. seq. For more details on how IRAs work and the deduction limits, see the IRS website explanation.

In short, if an individual is a “covered expatriate” upon renunciation (or LPR abandonment), they will generally be subject to U.S. income taxation on the entire amount of the IRA (along with all other assets with unrealized gains), reduced by the exemption amount (currently US$680,000 for the year 2014).

Unfortunately, it is fairly easy to become a “covered expatriate” even if the asset or tax liability tests are not satisfied, simply if the individual fails to satisfy the certification requirement under Section 877(a)(2)(C). There are multiple posts that address this important certification requirement of Section 877(a)(2)(C), irrespective of how poor or how few of assets might be held by the individual. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute, also see Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Plus, the topic is covered yet further in More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

Generally “covered expatriate” status is to be avoided, give the various adverse tax consequences. See, for instance, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

However, since the U.S. tax law is complex and oftentimes full of unintended consequences, there may be times when “covered expatriate” status is desirable in any particular circumstance. I have seen and advised on several; including scenarios, where some planning steps can help get a much better U.S. tax result in various cases.

Assume a former USC does not meet the certification requirement (e.g., since they neglected to properly file a complete and accurate IRS Form 8854, or they otherwise did not comply with Title 26 for one or more of the five years preceding the renunciation/abandonment). Further, let us assume, she has an IRA with a total value of US$1.4M and all of her other assets have no unrealized gain (e.g., Euros in a bank in Europe and an apartment she purchased in her country of residence in Europe that continues to have depressed real estate prices). These other assets, the apartment and Euros are US$500,000 in value; hence, less than the US$2M net worth threshold. However, we will assume she did not timely comply with the certification requirements under the law.

In such an “unfortunate” case, she would have to accelerate all of the income (gain) from her IRA in the year she has her “date of expatriation”. This would cause a U.S. federal income tax liability of about US$260,000 that would become immediately due and payable. This amount is calculated as follows: US$1.4M total IRA, less the $680,000 exclusion amount, for a total taxable income of about $720,000 (which will generate an approximate US$260,000 income tax for someone who is not married filing jointly. This represents an effective tax rate of approximately 36% on the taxable income portion (US$260,000/US$720,000). Remember, however, $680,000 escapes taxation under the exclusion amount. Hence, the effective tax rate on the entire IRA portion is actually only about 18.6% in this case. This amount is calculated as total IRA income of US$1.4M against tax of US$260,000 (i.e., $260,000/$1.4M= 18.6%).

An 18.6% tax rate is generally a very “attractive” U.S. individual income tax rate for those who have high amounts of income, as is this case with US$1.4M.

If instead, she is not a “covered expatriate” at the time she renounces her citizenship in 2014 (as she did comply with the certification requirements and otherwise would not meet the $2M net worth and her average annual net income tax liability for the preceding 5 years did not exceed $157,000) she would have a very different tax result. In short, she would not have to accelerate the entire tax liability. That sounds like good news, until one considers the U.S. tax rate on future IRA distributions to her after she ceases to be a U.S. citizen. Absent, an income tax treaty, she would have a 30% tax withheld at source (i.e., by the U.S. payer – trustee of the IRA) on each distribution made. If all US$1.4M is distributed out in one lump sum, there will be a tax of US$420,00 (US$1.4M X 30%); much more than the $260,000 for the “covered expatriate” scenario above. See calculations in this table:

Also, if she prefers to defer the IRA distributions (e.g., to make 14 annual distributions of US$100,000), she will have the same 30% tax withheld on each payment; hence, a total tax of US$420,00.

Obviously, a 30% tax is much worse than an 18.6% tax. Accordingly, this is a scenario where an individual may prefer to be a “covered expatriate” as opposed to avoiding such status. A bunch of factual analysis and strategic considerations would need to be considered in her case (e..g, where are her future heirs, what other income might she receive, will she receive any future gifts of inheritances herself, etc. etc.?).

Indeed, in this particular case, I can imagine a scenario (if accompanied by some focused tax planning), she could pay no more than a total effective tax rate of 12.2% on her income. Of course, 12.2% is better than 18.6% and 30%.

Finally, there is one more important wrinkle that can modify these results yet further; a particular income tax treaty with the U.S. that has a specific tax result that is better than the statutory 30% rate on distributions from an IRA to a non-resident alien. The U.S. has numerous income tax treaties with numerous countries, almost all of which have different terms and conditions. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

This admonition might sound a bit silly, considering we are talking about a “Tax Organizer”; which is often (but not always) provided by the tax return preparer to their clients simply to collect and organize information. It’s a communication between the taxpayer and the tax return preparer.

Tax Organizers come in all shapes, flavors and colors and have no real legal significance in and of themselves. They ask a range of questions and request  various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

The AICPA has a sample Tax Organizer that is 95 pages in length. Most taxpayers quickly lose patience with detailed Tax Organizers and feel they are doing the work the tax return preparer is supposed to do in the first place. Some taxpayers simply do not complete these Tax Organizers, or do so summarily, with only partial information provided.

In years past, Tax Organizers often did not ask any questions or information about foreign bank accounts or foreign financial accounts. There are still plenty of Tax Organizers that are being used, which do not expressly raise this question.

The first set of questions in the image at the beginning of the post, is from a Tax Organizer that asks a series of questions regarding foreign accounts. This becomes important due to the law of Title 31 regarding foreign accounts. Of course, for the USC and LPR residing outside the U.S., their accounts in their home country of residence are necessarily “foreign accounts” as defined under the law, even if they are in the country where the person resides (which does not sound “foreign”). See, *Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The admonition in this post is because the government has made Tax Organizers a very big deal in cases where they have asserted the 50% civil willfulness penalty (including for multiple years in Zwerner). The government argued vociferously that since the taxpayers checked the box “No” on the Tax Organizer regarding foreign accounts, in both the Williams (very bad facts – due to admitted tax criminal conduct) and the Zwerner cases, this indicated the taxpayers had either “constructive knowledge” or were “willfully blind” as to the requirements they had under the law to file FBARs.

Of course, filling out an incomplete Tax Organizer with your tax return preparer is not a crime; unless the individual knows the information is false and will be provided to the IRS by their accountant. For a summary of the crime of filing a “false document”, see What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The “takeaway” from these two cases and how Tax Organizers are used by accountants, is that the individual is probably better off simply not using at all any Tax Organizer. This way, how it was completed (or not) cannot be construed and used against the individual as somehow showing willfulness under the FBAR penalty.

Part I: What is “Willful” and what is “Non-Willful” for USCs and LPRs Residing Overseas Who Have Not Filed U.S. Tax Returns or FBARs?

Part I: What is “Willful” and what is “Non-Willful” for USCs and LPRs Residing Overseas Who Have Not Filed U.S. Tax Returns or FBARs?

This will be one of the most important questions to understand for any USC or LPR residing outside the U.S. who has not been filing U.S. income tax returns or FBARs. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The willfulness question is important, when the USC or LPR decides what steps they need to take regarding the filing of U.S. income tax returns.

A LPR residing predominantly in a country with a US. income tax treaty (of which there are 68) may be in the best position to “clean up” their U.S. tax filing and return positions. Specifically their facts might allow them to file as a non-resident under the “tie-breaker provisions” – typically Article 4); and indeed such filings might be applicable for several prior years.

See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) for a comprehensive list of each income tax treaty and country.

The issue of “expatriation” becomes front and center for the LPR who notifies the IRS that he or she is not a resident of the U.S, pursuant to an applicable income tax treaty and files the treaty position accordingly.

Specifically, the statutory language of IRC Section 7701(b)(6) has three tests for when the individual is no longer a LPR for federal tax purposes:

- The individual is treated as a resident of a foreign country under the provisions of a tax treaty;

- The individual does not waive the benefits of the treaty, and

- Notifies the Secretary of the commencement of such treatment.

If the LPR has had that status for the requisite number of 8 years or more, to be treated as a “long term resident”, he or she would generally be subject to the “exit tax” of Sections 877 and 877A (plus a tax to any future U.S. persons who receive gifts or inheritances from such former LPR). See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

If the LPR has not been “non-willful” (double negative intended) by not filing U.S. income tax returns, interesting legal questions are raised as to the consequences to the LPR.

In addition, the IRS “streamlined” procedure announced on June 18th, 2014, has specific requirements obligating the taxpayer to certify “non-willful” behavior.

Various consequences of signing these certifications under penalty of perjury, will be discussed in later posts.