International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

A U.S. Immigration Officer Stops You at at the Airport – @ the Point of Entry (Demands your Green Card be Turned Over))

Being stopped, searched, interrogated or simply questioned by U.S. federal government agents can be intimidating. Especially, if you do not know your legal rights.

It can be more intimidating on your arrival to the U.S. airport, if the CBP officer (U.S. Customs and Border Protection) demands that you physically “return voluntarily” your green card. The consequences they tell you will be immediate deportation from the U.S.

Removal from the U.S. – is it voluntary or not, under these circumstances?

What are the U.S. federal tax consequences if you “return voluntarily” your green card?

What if the CBP officer pulls out Forms W-8s you previously signed with your foreign financial institution and presents them to you in the airport and asks the following questions:

Why did you certify “under penalty of perjury” you were not a United States person on your foreign bank produced documents (you received in France, Germany, the U.K., Canada, Mexico, Japan, Indonesia, Australia — or any other foreign country)?

The officer then asks for all of the envelopes and papers in your luggage and opens the letters and files in your possession – See, the U.S. Supreme Court decision United States v. Ramsey, 431 U.S. 606 (1977).

Tax Problems that Turn Serious – can Cause a Green Card Holder to become a “Covered Expatriate”

In Kawashima v. Holder (565 U.S. 478 (2012), the United States Supreme Court held that certain tax offenses committed by lawful permanent residents constitute crimes involving “fraud or deceit” for purposes of the Immigration and Nationality Act (“INA”). Specifically, the Court concluded that lawful permanent residents (a husband and wife from Japan) who were convicted of filing false tax returns resulting in a tax loss exceeding $10,000 had been convicted of an “aggravated felony” within the meaning of the INA.

As a consequence, a conviction for such an aggravated felony renders a lawful permanent resident removable (deportable) from the United States under the immigration laws. Importantly, however, the criminal conviction itself does not automatically terminate lawful permanent resident status. Rather, it provides the legal basis for the Department of Homeland Security to initiate removal proceedings, after which an Immigration Judge may enter a final order of removal.

Once a final order of removal becomes effective, the individual’s lawful permanent resident status is considered to have been revoked. For U.S. federal income tax purposes, this generally results in the termination of lawful permanent resident status under 26 U.S.C. § 7701(b)(6)(B), which provides that an individual ceases to be a lawful permanent resident when “such status has been revoked or has been administratively or judicially determined to have been abandoned.” Accordingly, following a final order of removal, the individual is no longer treated as a lawful permanent resident for purposes of the tax law as summarized below:

Stage

Legal Effect

1. Criminal conviction (including guilty plea)

If the offense qualifies as an “aggravated felony” under INA §101(a)(43), the individual becomes deportable under 8 U.S.C. §1227(a)(2)(A)(iii). A guilty plea counts as a conviction for immigration purposes if the statutory definition of “conviction” is satisfied.

2. DHS initiates removal proceedings

DHS serves a Notice to Appear (NTA) charging removability before an Immigration Judge under 8 U.S.C. §1229a.

3. Immigration Judge determines removability

DHS bears the burden of proving deportability by clear and convincing evidence, typically through the certified judgment of conviction.

4. Final order of removal

If removability is sustained and no relief is available, the Immigration Judge orders removal. After appeals are exhausted (or waived), the removal order becomes final, and the person’s LPR status ends.

The 2012 case involved Akio and Fusako Kawashima, Japanese citizens who had been lawful permanent residents since 1984. Mr. Kawashima pleaded guilty to willfully filing a false tax return under 26 U.S.C. § 7206(1), while Mrs. Kawashima pleaded guilty to aiding and assisting in the preparation of a false tax return under 26 U.S.C. § 7206(2). The immigration judge issued the order of removal. The Board of Immigration Appeals affirmed. Holding that convictions under 26 U. S. C. §§7206(1) and (2) in which the Government’s revenue loss exceeds $10,000 constituted aggravated felonies, the Ninth Circuit affirmed and ultimately so too did the SCOTUS in this decision.

The Supreme Court concluded that these tax offenses necessarily involve fraud or deceit and, because the tax loss exceeded the statutory $10,000 threshold, they constituted aggravated felonies under immigration law. The Supreme Court of the U.S. therefore upheld the government’s order (which had been upheld through the Ninth Circuit Court of Appeals) removing the Kawashimas to Japan.

This of course is important for U.S. “expatriation tax” purposes, since the “lawful permanent resident” status for tax purposes will necessarily terminate upon the final order of removal. Not before. Once LPR status terminates, the individuals will become covered expatriates, if they meet the time period under the statute to become “long term residents” as was the case for Mr. and Mrs. Kawashima and meet either of the three tests: the tax liability, net asset and certifications of compliance with the federal tax laws. See, Why a “long-term” LPR can NEVER avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B) if Asset or Tax Liability Test is Satisfied!

EB-5 Visa – a common Path to a “Green Card” and then USC

Pathways to United States Citizenship – (USC): Focus on the EB-5

Every individual who ultimately becomes a naturalized U.S. citizen must first qualify for lawful permanent resident (“LPR”) status unless a narrow statutory exception applies. Although public attention frequently focuses on the EB-5 immigrant investor program, with the idea they are those with greater assets and income (contemplating taxes) EB-5 investors represent only a very small percentage of all individuals who become lawful permanent residents. Understanding the relative size of each immigration pathway is essential because every pathway ultimately raises many of the same U.S. tax issues—including worldwide income taxation, estate and gift taxation, and the tax consequences of later abandoning lawful permanent resident status or renouncing U.S. citizenship.

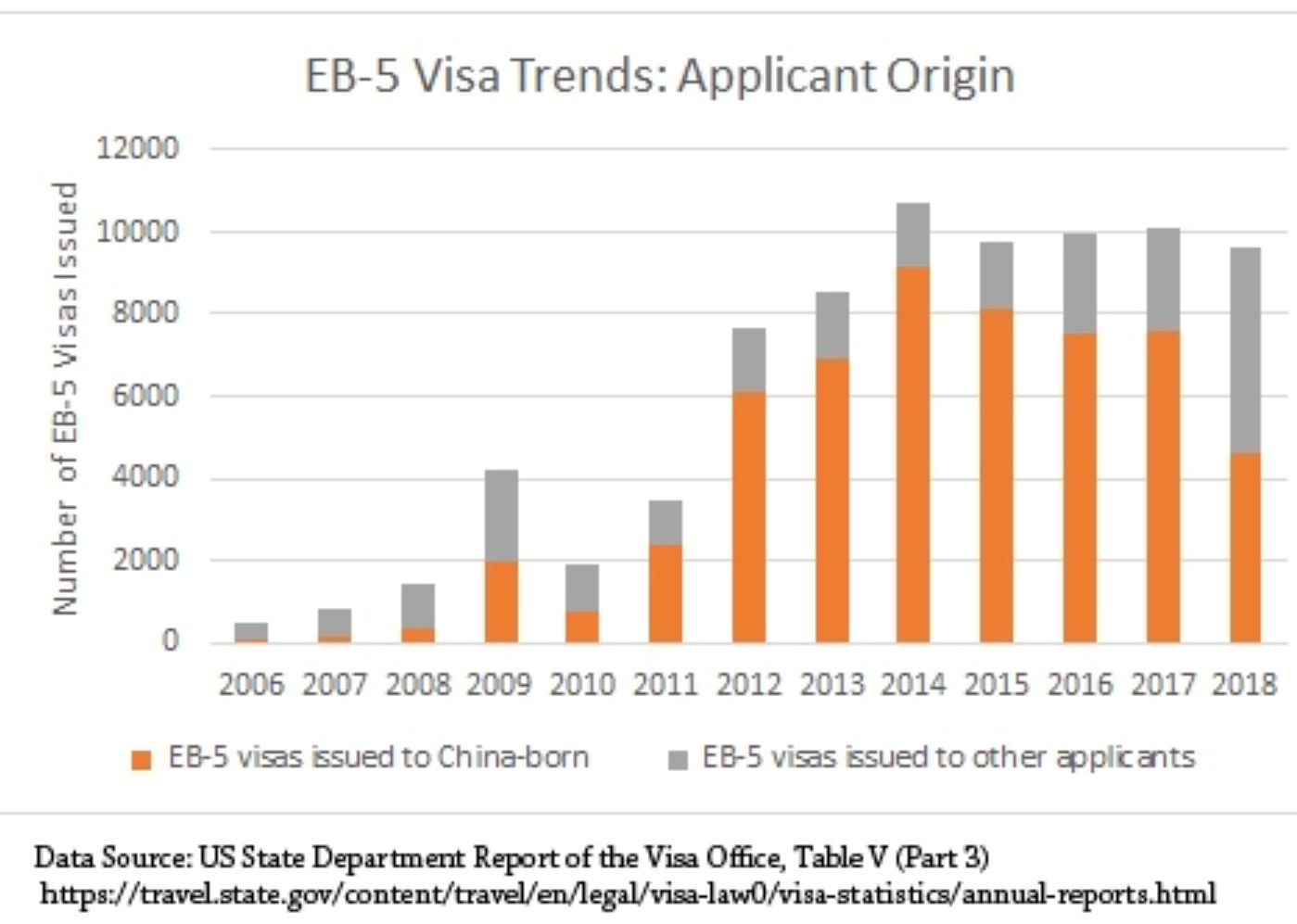

The EB-5 visa has been a fixture of U.S. law since the early 1990s. It was not until 2009 that a substantial number of EB-5 visas were issued in a given year, 4,218 to be exact. Statistically, the total EB-5 visa leading to LPR status is a fraction of the other categories as explained here. For an excellent overview of the law and categories, see the CRS report- Permanent Legal Immigration to the United States: Policy Overview (Updated November 4, 2024)

EB-5 Visa – to a “Green Card” then to United States Citizenship – (USC)

From the laws inception in 1992 through FY2004, there were only 6,024 EB-5 visas issued during that 12 year period. That is an annual average of only approximately 500 persons. See, the GAO Report on Immigrant Investors. As the program grew in popularity so too did the location of investors from around the world. It was not until 2009 when the total number of investors started growing substantially. Most significantly in 2009 when 4218 EB5 visas were issued, still less than 1/2 of the 10,000 allocated annually by the statute.

These numbers kept going at an annual pace especially starting in 2012, when 6,764 EB-5 visas were issued and then around 10K+/- annually for the last dozen years or so, up until the years that were impacted by a change in the law and a bit by COVID (2020 and 2021). There are important tax consequences that can have unintended outcomes for individuals who get a green card: See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

Chinese Investors Have Dominated the total Group of EB-5 Investors

The country-of-origin analysis is important because practitioners frequently advise clients from these jurisdictions regarding immigration planning, cross-border tax planning, and eventual expatriation planning with consequences in those countries.

I have compiled the total list of countries from which EB-5 visa investors came from as summarized in the Country of Origin global graphic for FYE 2024. There are over 100 countries from which these investors came from, but again, China is the dominant country, followed by Vietnam, India, Taiwan and then South Korea as the countries with the greatest number of investors. South Africa comes next, followed by Brazil and then Mexico, but each with less than 200 total investors, each country as follows:

China

9547

Vietnam

1533

India

1428

Taiwan

513

Korea, South

325

South Africa

158

Brazil

157

Mexico

128

Hong Kong S.A.R.

116

Venezuela

97

Canada

81

Great Britain & N. Ireland

63

Russia

58

Nigeria

52

Turkey

44

Colombia

44

France

38

United Arab Emirates

30

Germany

29

Japan

25

Singapore

23

Kazakhstan

21

Peru

20

Ukraine

17

Sweden

15

Argentina

15

Egypt

14

The importance of this analysis is to help individuals (and their advisors) who fit into these categories, e.g., who have a pathway to a green card and then on to become a naturalized U.S. citizen, understand the potential “tax expatriation” consequences of their decisions over the long-run.

What are the U.S. “tax expatriation” consequences to individuals who go down these pathways, including to their dependent children, or spouses or any future beneficiaries who are “United States person”?

What are the tax expatriation consequences if the individual later decides they do not want to be a green card holder or a U.S. citizen and later wishes to abandon their lawful permanent residency status or formally renounce their U.S. citizenship?

These and many other questions should be considered, especially for long-term family planning. Not just for the investor, but for their children and spouse, who may be eligible for the visa that can lead to LPR status and eventually to USC. Facilitating younger children (under 21 years of age) is a common driver for EB-5 investors for families who want the United States to be a pathway for their children’s’ future.

Why These Immigration Pathways Matter from a Tax Perspective

Every pathway leading to lawful permanent resident status almost always subjects the individual to the comprehensive U.S. federal income tax system. Depending upon the individual’s assets, family structure, treaty residence, and future living plans, obtaining a green card will also have significant implications for:

worldwide income taxation;

estate and gift taxation;

foreign trust reporting;

information reporting obligations under various laws;

controlled foreign corporation rules;

PFIC reporting;

exit tax planning; and

long-term succession planning.

Equally important, many lawful permanent residents eventually decide to return permanently to their country of origin or another foreign jurisdiction. Those individuals—and frequently their spouses and dependent children—must carefully consider the tax consequences of formally abandoning lawful permanent resident status or, after naturalization, renouncing U.S. citizenship. The sooner individuals and their advisors realize these consequences, the better they can plan for important life decisions.

Those tax consequences are collectively referred to as the U.S. tax expatriation rules, and they form the principal subject of this website.

The legal pathways towards lawful permanent residency status can be broken down into the following categories and the EB-5 category is a fraction (only about 1%) of the total pool leading to LPR status:

This category includes EB-1 through EB-5 categories that include individuals with extraordinary ability, certain professionals, other skilled workers. The chart I prepared here reflects the total number of EB-5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b).

EB-1, EB-2 and EB-3 represent the greatest group of individuals who obtained LPR status (e.g., approximately 5X, each category compared to the EB-5 category). See Yearbook of Immigration Statistics, Table 6.

For instance, annually the EB-1 through EB-3 categories are processing about 50K per year of each, and the EB-5 category is only 131K over most of its 25 year life (or about 10K per year – for more recent years). Approximately 16% of all green card holders come through these employment based preferences.

Table – Approximate Decade-Average Share by Category, FY2014–FY2023

Category

Approx. Share

Notes

Family-sponsored (total)

~64%

Immediate relatives + family preferences combined

— Immediate relatives

~46%

Spouses ~26%, parents ~14%, children ~6%

— Family preferences (F1–F4)

~18%

Numerically capped at 226,000

Employment-based (EB-1–EB-5)

~16%

Capped at 140,000; breached in COVID years

Refugees & asylees

~12%

Numerically unlimited; ceiling-driven volatility

Diversity

~4%

Statutory ceiling 55,000

All other / special

~4%

SIV, U/T victims, cancellation, registry, etc.

C. Diversity Immigrant Program

The annual diversity lottery, allocated by random selection, to natives of countries with historically low rates of immigration to the United States. See, 8 U.S. Code § 1153(c). The Attorney General plays a key role by statute in this determination. There is a statutory maximum of 55,000 and only represents about 4% of all LPRs compared to the larger pool. This program is on hold as of December 19, 2025 when the USCIS policy memorandum (PM-602-0193) directs officers to place an immediate hold on pending adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

D. Humanitarian and Special Pathways: Refugees/Asylees

Several routes proceed outside the preference system (the three categories above). Refugees and asylees adjust under a specific statutory regime; self-petitioning abused spouses and children proceed under other provisions; victims of qualifying crimes and of trafficking can adjust from U and T nonimmigrant status; and certain children subject to qualifying juvenile-court findings can qualify, among others. There are statutory limits placed on this group.

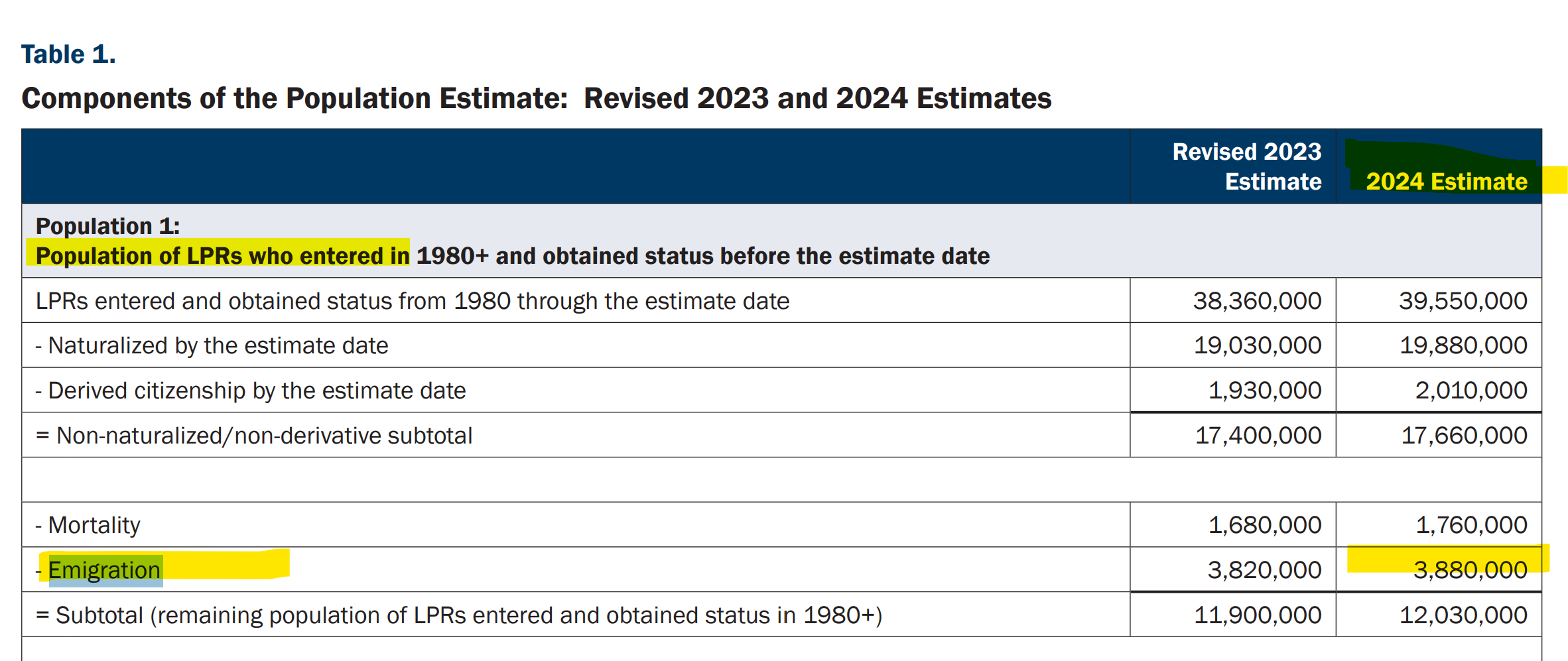

Whatever category one uses for LPR status, there will be important U.S. federal tax consequences to them and typically their family members. That’s the large part of the focus on this forum where the author has written about the subject of how it all ties to “tax expatriation”. As previously reported, there are 3.88 million “LPR” individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. See, Table 1 of the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023.

Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

See Part I for the background discussion, which was published more than a year ago.

This article focuses on the tax consequences of the “Trump Gold Card” program and, in particular, the implications if participation ultimately leads to U.S. citizenship (“USC”).

The final version of the Gold Card program requires a $1 million contribution to the federal government, rather than the $5 million amount initially discussed in April 2025. See the government website, The Trump Gold Card is Here.

It is also important to note that President Trump established the Gold Card program through Executive Order 14351 in September 2025. Congress did not enact the program through legislation.

The Cost of a Trump Gold Card

For a $15,000 Department of Homeland Security processing fee and, following successful background review, a $1 million contribution to the federal government, an applicant may obtain U.S. permanent residence through the Gold Card program.

Why Would an Ultra-High-Net-Worth Individual Voluntarily Enter the U.S. Tax Net?

A fundamental question arises: Why would an ultra-high-net-worth (“UHNW”) individual contribute $1 million to obtain U.S. residence and potentially U.S. citizenship, thereby becoming subject to one of the world’s most expansive tax systems?

For many individuals, acquiring U.S. citizenship or lawful permanent resident (“LPR”) status can result in exposure to:

U.S. income taxation on worldwide income;

U.S. gift taxation on worldwide transfers of property; and

U.S. estate taxation on worldwide assets at rates that currently reach 40%.

U.S. Estate and Gift Taxation of Worldwide Assets

The United States generally imposes estate and gift taxes on the worldwide assets of U.S. citizens. In addition, lawful permanent residents who are domiciled in the United States may become subject to the same worldwide transfer tax regime.

Unlike many countries, the United States generally does not permit its citizens to escape worldwide taxation simply by relocating abroad. Most U.S. income tax treaties and estate and gift tax treaties contain a “savings clause” that preserves the right of the United States to tax its citizens notwithstanding treaty provisions.[1]

U.S. Estate and Gift Taxation of Worldwide Assets

As a result, the worldwide assets of a U.S. citizen may be included in the U.S. transfer tax system under IRC §§ 2001 and 2031 (estate tax) and IRC §§ 2501 and 2511 (gift tax).

Consider a U.S. citizen who owns:

a residence in Norway;

shares of a Mexican corporation;

a bank account in Singapore;

an interest in a Liechtenstein foundation (Stiftung);

a portfolio of securities held through a London financial institution; and

an apartment in Dubai.

Subject to applicable valuation and ownership rules, each of these assets generally forms part of the individual’s worldwide taxable estate for U.S. estate tax purposes.

By contrast, a non-U.S. citizen who is not domiciled in the United States generally would not be subject to U.S. estate tax on any of these assets, unless they include U.S.-situs property such as stock issued by U.S. corporations.

The difference can be dramatic: no U.S. estate tax exposure versus potential exposure to a 40% U.S. estate tax on worldwide assets.

U.S. Income Taxation of Worldwide Income

The contrast is equally significant in the income tax context.

A nonresident generally is subject to U.S. income taxation only on limited categories of U.S.-source income and income effectively connected with a U.S. trade or business.

A U.S. citizen, however, remains subject to U.S. federal income taxation on worldwide income regardless of where the individual resides.

Consequently, a foreign entrepreneur, investor, or family office principal who acquires U.S. citizenship will find that income earned from businesses, investments, trusts, partnerships, and financial accounts throughout the world generally becomes reportable to the Internal Revenue Service and subject o U.S. income taxation.

That result raises an obvious question: if the program is available, why have so few ultra-high-net-worth individuals pursued it successfully?

The most obvious explanation is that the long-term U.S. tax consequences may outweigh the perceived immigration benefits for many globally mobile individuals.

Comparison to the EB-5 Program

Different applicants may have different motivations.

The traditional EB-5 immigrant investor program generally requires a qualifying investment that, if successful, may ultimately be recovered. The program also requires satisfaction of statutory requirements, including job creation. Approximately 200,000+/- individuals have obtained a green card through the EB-5 program. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

EB-5 Visa Applicants by Country

By contrast, the Gold Card program requires a direct contribution to the federal government.

In either case, the successful applicant receives lawful permanent resident status. However, if the Gold Card ultimately serves as a pathway to naturalized U.S. citizenship, the applicant may become subject to the unique worldwide taxation regime applicable to U.S. citizens.

The Expatriation Problem

If Gold Card holders ultimately naturalize as U.S. citizens, future departure from the U.S. tax system will necessarily become significantly more complicated.

Individuals who later seek to relinquish U.S. citizenship will necessarily face the expatriation rules of IRC § 877A and be tainted with “covered expatriate” status.

As discussed in earlier posts, covered expatriate status can have substantial long-term tax consequences for both the expatriating individual and future recipients of gifts and inheritances.

Legal Questions Surrounding the Program

The Gold Card program also raises constitutional and statutory questions.

Unlike the EB-5 program, which was enacted by Congress, the Gold Card program was created through executive action. Congress did not amend Title 8 of the United States Code to establish a new immigrant category.

Whether the Executive Branch possesses sufficient statutory authority to create such a program remains an open legal question (I am doubtful it will be sustained – if challenged) and will likely be the subject of continued litigation and judicial review.

The outcome of pending litigation involving other immigration-related executive actions may provide useful guidance regarding the scope of presidential authority in this area. We await the outcome of the latest case litigated through the courts. See, Supreme Court appears likely to side against Trump on birthright citizenship which was also issued by an executive order.

Who Truly Benefits?

Who is the ideal candidate for a Trump Gold Card? Only one person thus far has one.

For almost all HNW individuals, the immigration benefits, travel flexibility, business opportunities, and potential pathway to U.S. citizenship would rarely justify the cost. Someone with assets below US$20M might find it attractive.

For almost all others—particularly those with substantial foreign businesses, investment portfolios, trusts, and family wealth located outside the United States—the long-term consequences of worldwide U.S. income, estate, and gift taxation will almost always substantially outweigh the advantages.

As a result, any prospective applicant for a Trump Gold Card should carefully evaluate not only the immigration benefits of the program (+ the uncertainty in the law), but particularly the tax consequences that will follow for decades thereafter.

Can you keep your green card and still “expatriate” for US tax purposes?

Yes. Many lawful permanent residents (LPRs, or green card holders) assume they have not “expatriated” for US tax purposes as long as they have not handed their green card back to US Citizenship and Immigration Services (USCIS). That assumption can lead to a rude awakening. Under IRC Section 7701(b)(6), a green card holder can cease to be treated as a lawful permanent resident for federal tax purposes without ever formally abandoning the card with USCIS. See, an article written by Patrick W. Martin on this subject a dozen years ago: See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

What is IRC Section 7701(b)(6)?

IRC Section 7701(b)(6) is a provision Congress added in 2008 that says when a green card holder stops being treated as a lawful permanent resident for federal tax purposes. The relevant part provides that an individual shall cease to be treated as a lawful permanent resident if the individual commences to be treated as a resident of a foreign country under a tax treaty between the United States and that country, does not waive the benefits of the treaty applicable to residents of the foreign country, and notifies the Secretary of the commencement of such treatment.

What are the three tests for losing LPR status under Section 7701(b)(6)?

The statutory language sets out three tests. A green card holder is no longer an LPR for federal tax purposes when all three are met:

The individual is treated as a resident of a foreign country under the provisions of a tax treaty;

The individual does not waive the benefits of that treaty; and

The individual notifies the Secretary of the commencement of such treatment.

It can get more complicated than this too – depending upon the interpretation of the laws in various tax treaties.

Can filing Form 1040NR end your green card status for tax purposes?

It can. Each of the three tests under Section 7701(b)(6) appears to be satisfied by a green card holder who files IRS Form 1040NR as a non-resident while living in a country that has a US income tax treaty. In that situation the individual may be treated as having ceased to be a lawful permanent resident for federal tax purposes, even though the green card itself was never returned to USCIS.

What happens once you stop being a lawful permanent resident under the tax law?

There can be a host of unintended consequences for an individual who ceases to be a lawful permanent resident under the federal tax law. The expatriation provisions of Section 877A and Section 2801, among others, can be implicated, along with many other provisions of the law. For background, see “Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web,” International Tax Journal, CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

How does a green card holder formally abandon LPR status?

For those who wish to formally abandon their lawful permanent resident status, there is a specific DHS/USCIS form used for that purpose: Form I-407. Filing this form is the route to formally relinquishing the green card with the immigration authorities, which is separate from the tax-law treatment described above under Section 7701(b)(6).

World Cup & Playing in the United States: Green Card Holders, the Treaty Tiebreaker, and the Global Athlete or Entertainer

As the world’s athletes have arrived to perform on U.S. soil, the U.S. tax system is a broad net. The 2026 FIFA World Cup—hosted across the United States, Mexico, and Canada—is a useful occasion to revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

This blog is dedicated to issues of “tax expatriation” which crosses into different professions and global lifestyles. See, for instance the following prior blogs:

There are of course many famous athletes who were not U.S. citizens and then became green card holders and oftentimes then became naturalized U.S. citizens. Since the Knicks just won the NBA championship after 53 years, one of their greatest, Patrick (mi tocayo) Ewing left Jamaica as a boy, became a green card holder and then a naturalized citizen. A 1985 New York Times article, A Favorite Son Goes Home, describes his first return to the island since a boy.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

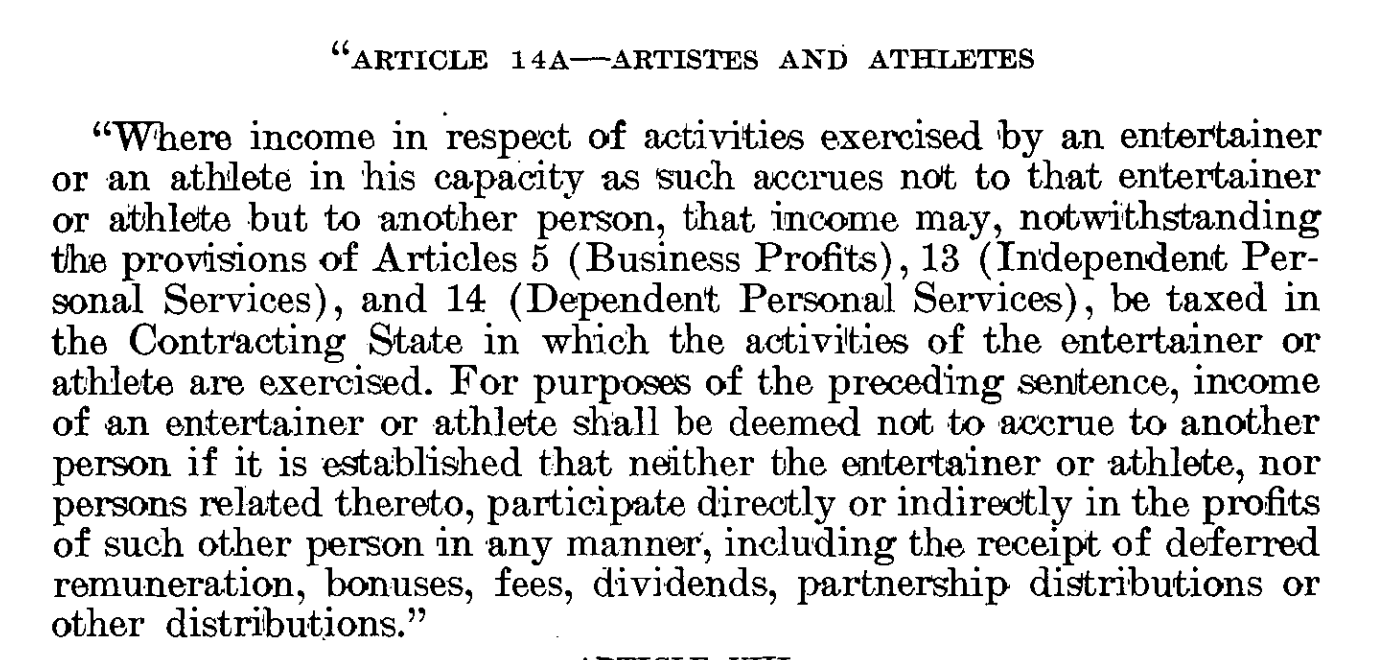

Athletes and entertainers are specially taxed in the U.S. in the sense they typically receive few benefits from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

A protocol to the treaty adopted in 1980 has a “new” article 14A specific to artists and athletes as reflected here in its entirety allowing the government to tax athletes and entertainers when they perform in the country (overriding other protective provisions of the treaty – e.g., Business Profits Art. 5, Independent Personal Services Art. 13 and Dependent Personal Services Art. 14):

The IRS also adopted a specific program, called the Central Withholding Agreement (“CWA”) program created by Revenue Procedure 89-47 specific to artists and athletes. I personally think it is a program that is not authorized by the statute and often applied by the IRS in a manner that violates the withholding tax regime we have in Chapter 3 of our statutory tax law, Subtitle A. In practice, third parties are subject to the 30% withholding tax on certain gross proceeds paid to companies other than the artist or athlete, if the athlete or artist doe not participate with the IRS in their CWA.

Mexico

In the case of global soccer players, even one with a “lawful permanent resident” card (i.e., a “green card”) they may be subject to the Chapter 3 withholding tax rules if the athlete is like Mr. Aroeste (Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC)) holding a green card in his pocket, but not a U.S. income tax resident by application of the residency rules set forth in an income tax treaty. Will the soccer player become a “covered expatriate” and not even know it (oops)?! It can get tricky quickly. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

Meanwhile, Mexico and the U.S. have both advanced to the knockout round.

Canada plays Switzerland and presumably has a 99% chance of advancing to the Round of 23.

What Tax Forms Do US Citizens and Green Card Holders Living Abroad Need?

Living outside the United States does not eliminate your US tax obligations. US citizens and green card holders abroad must file a US tax return every year and may also need to file additional reports on foreign assets and accounts. Here is an overview of the key forms, what they cover, and how they interact.

Is my foreign income automatically exempt from US reporting?

No. A common misconception is that foreign income is exempt because it can be excluded. Foreign earned income is not exempt. You must report it on a US tax return, and you must be a qualifying individual to elect the exclusion.

What types of income qualify for the exclusion on Form 2555?

The exclusion is available only for “earned” income. It cannot be used for passive investment income such as dividends, interest, or capital gains.

Foreign Tax Credits (FTC)

How does a Foreign Tax Credit work?

A Foreign Tax Credit provides a dollar-for-dollar reduction, subject to limitations, of your US federal tax burden for income taxes you paid to another country on income sourced there. It is claimed on Form 1116.

Can I claim both the FEIE and the Foreign Tax Credit?

No. Once you choose to exclude foreign earned income or housing costs, you cannot take a foreign tax credit on that same income. If you do take the credit, your previous choice to exclude that income may be treated as revoked.

Are there different forms for lawful permanent residents (LPRs)?

US citizens and LPRs generally use Form 1040. However, LPRs residing in a country with a US income tax treaty may be eligible to file Form 1040NR as a non-resident.

Information Reporting and FBAR

What is Form 8938?

Form 8938 (Statement of Specified Foreign Financial Assets) is used to report specified foreign financial assets. It often overlaps with FBAR reporting and must be attached to your annual income tax return when filed with the IRS.

Who must file an FBAR (Form 114)?

US citizens and LPRs with a financial interest in or signature authority over foreign accounts must file a Foreign Bank Account Report (FBAR). The definitions of “ownership interest” and “signature authority” are interpreted very broadly under the regulations.

Where is the FBAR filed?

Unlike other tax forms, the FBAR is not filed with the IRS. You must file it electronically with FinCEN (the Financial Crimes Enforcement Network) through the BSA E-Filing System on Form 114.

What are the penalties for FBAR non-compliance?

The statutory penalty for failing to file, or filing late, is $10,000 per failure. If the failure to file was intentional, the penalty can increase to 50% of the account balances.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

Tax Preparation Software

Can I use standard tax software for these international forms?

Often, no. Most tax preparation software does not support Form 8938 or other forms related to non-US assets. These forms frequently require manual completion using an Adobe Acrobat version of the form.

Can You Lose Your Green Card Just by Living Outside the United States?

Many green card holders who move abroad assume their permanent resident status is safe as long as they return to the United States occasionally. Under US immigration law, that assumption can be wrong. A green card can be abandoned automatically, without any formal filing, simply by how long you spend outside the United States.

A lawful permanent resident (LPR) can lose permanent resident status through removal (deportation) ordered by an immigration court, or through abandonment. Abandonment can happen formally, by filing Form I-407 (Abandonment of Lawful Permanent Resident Status), or automatically, by operation of law, when an LPR takes an action that constitutes abandonment under immigration law, such as departing the United States for more than a temporary visit abroad. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

What triggers an automatic abandonment finding?

The Department of Homeland Security (DHS) will make an abandonment finding if an LPR takes a single trip outside the United States lasting more than one year. After a trip of more than one year, the LPR can only challenge the finding in removal proceedings. For a single trip lasting between 6 months and one year, DHS presumes the LPR intended to abandon their permanent resident status, but the LPR may rebut that presumption. Even for shorter trips, DHS may find abandonment if the LPR has spent a significant amount of time outside the United States on multiple trips.

What factors does DHS consider?

DHS and the immigration courts look at: the purpose and duration of the trip abroad; whether there was a specific event after which the LPR planned to return; and the LPR’s family ties, employment, property holdings, and business affiliations in the United States versus the foreign country.

How does filing a tax return as a non-resident affect your status?

Filing a US income tax return as a non-resident alien raises a rebuttable presumption of abandonment of LPR status for immigration purposes.

What can you do if you expect a long absence?

If an LPR knows they will need to spend significant time outside the United States, they should apply for a reentry permit before departing. A reentry permit alone does not guarantee readmission following a long absence, but it is evidence of the intent to return to the United States and maintain permanent resident status.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Why Long-Term Green Card Holders Cannot Escape the Exit Tax Rules

When long-term green card holders give up their green card, they face the same exit tax rules as US citizens who renounce citizenship. There is one exception in the law that allows certain dual citizens by birth to avoid covered expatriate status even if they meet the income or asset tests. Long-term green card holders cannot use it. Here is why.

When you give up your green card (or renounce US citizenship), the law determines whether you are a covered expatriate. You are a covered expatriate if you meet any one of three tests: an average annual income tax liability above an inflation-adjusted threshold, a net worth of $2 million or more on the date of expatriation, or a failure to certify 5 years of US tax compliance – where it is commonly certified on IRS Form 8854.

Meeting even one of these three tests makes you a covered expatriate. All three tests apply equally to US citizens who renounce and to long-term lawful permanent residents (LPRs) who give up their green card.

Is there an exception to the income and asset tests?

Yes, for some people. Under IRC Section 877A(g)(1)(B), certain individuals are exempt from the income and asset tests. If this exception applies to you, you can avoid covered expatriate status even if your net worth exceeds $2 million or your income exceeds the threshold. The certification requirement under Section 877(a)(2)(C) still applies to everyone, including those who qualify for this exception.

Who can use this exception?

The exception is narrow. Under the statute, it applies only to an individual who: became a citizen of the United States and a citizen of another country at birth; as of the date of expatriation, continues to be a citizen of and is taxed as a resident of that other country; and has been a US resident for no more than 10 taxable years during the 15-year period ending with the taxable year of expatriation. Only someone who acquired US citizenship automatically at birth, while also holding citizenship of another country from birth, can potentially qualify.

Why green card holders cannot use it

Lawful permanent residents are not US citizens. They hold a green card, which is a grant of permanent resident status, not citizenship. Because the exception in Section 877A(g)(1)(B) applies only to individuals who became US citizens at birth, long-term LPRs cannot satisfy this requirement by definition. The exception is simply not available to them.

What this means if you are a long-term green card holder

A long-term LPR who meets either the $2 million asset test or the income tax liability test will become a covered expatriate, even if they fully satisfy the 5-year certification requirement. Satisfying the certification requirement is necessary for everyone, but for long-term LPRs it is not sufficient on its own. If you also meet the income or asset test, you are a covered expatriate regardless.

The consequences include the mark-to-market exit tax on unrealized gains and the Section 2801 tax on covered gifts and bequests to US persons. These consequences can affect your US family members for decades. Understanding them well before you give up your green card, not after, is the only way to plan for them.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Which IRS Form Do I Give My Foreign Bank? A Guide for U.S. Expats and LPRs

If you’re a U.S. citizen or green card holder living abroad, your foreign bank will likely ask for your U.S. tax status under FATCA. The form you need is Form W-9 — not Form W-8BEN. W-8BEN is strictly for non-U.S. persons; signing it as a U.S. citizen or LPR is a false certification under penalty of perjury. Use W-9 to confirm your U.S. taxpayer status and provide your SSN.

What are all the IRS forms and their purposes?

W-9: Used by U.S. citizens and Lawful Permanent Residents (LPRs) to provide their Taxpayer Identification Number (TIN) to a third party.

W-8BEN: Used by non-U.S. individuals to certify they are not “U.S. persons” for tax purposes.

W-8BEN-E: An eight-page form used by foreign entities to identify “substantial U.S. owners”.

W-7: Used by individuals who are not eligible for a Social Security Number to apply for an Individual Taxpayer Identification Number (ITIN).

W-8IMY: A form for foreign intermediaries or flow-through entities that was substantially modified due to FATCA.

W-4: Used to determine an employee’s federal income tax withholding.

W-8ECI: Used by foreign persons to claim that income is effectively connected with a U.S. trade or business.

W-8EXP: Used by foreign governments or other foreign organizations to claim an exemption from withholding.

W-8: A general category of forms for foreign status reporting.

What are Taxpayer Identification Numbers (TINs)?

A TIN is a broad term for the identification number used for U.S. tax purposes. Its sub-types include:

Social Security Number (SSN): For U.S. citizens, LPRs, and individuals with permission to work in the U.S. under specific visas.

Individual Taxpayer Identification Number (ITIN): For individuals who are not U.S. citizens or LPRs and are ineligible for an SSN.

Employer Identification Number (EIN): For business entities such as corporations, partnerships, and trusts.

Is Form W-9 the standard for Americans abroad?

Yes. If a foreign bank or company asks for your U.S. tax status, Form W-9 is the standard form you should use. It’s how you officially tell them, “I’m a U.S. taxpayer, and here is my ID number”.

Who Can Sign Form W-8BEN?

U.S. Citizens: They cannot sign this form. Doing so would be a false certification that they are not a “U.S. person” under federal tax law.

Lawful Permanent Residents (LPRs): Generally, they also cannot sign this form, as they are considered U.S. persons for tax purposes.

Former Citizens with a CLN: While the source highlights the importance of a Certificate of Loss of Nationality (CLN) in relation to FATCA status, it does not explicitly state that holding one allows for the signing of a W-8BEN, though it notes that only non-U.S. persons can legally sign the form.

What are the banking requirements for U.S. Persons?

When a bank asks for tax status, a U.S. person should sign Form W-9. However, many Foreign Financial Institutions (FFIs) use substitute forms that comply with regulations but may not look exactly like the official IRS version.

What is the Form W-8BEN-E?

Who completes it: Non-Financial Foreign Entities (NFFEs).

Definitions: A “substantial U.S. owner” is generally a U.S. person who holds a 10% or greater economic interest in the foreign entity.

Burdens: The form is eight pages long and requires the user to understand over 450 pages of FATCA regulations to select from roughly 30 different categories.

Consequences: The form is signed under penalty of perjury. Due to its complexity, the source notes that many “good faith errors” are inevitable.

When does the 8-page Form W-8BEN-E become necessary?

This massive 8-page form is usually for businesses, not just individuals. If you own 10% or more of a foreign company, that company has to use this form to report you to the IRS as a “substantial U.S. owner”.

What are the risks of misfiling these complex entity forms?

It’s a major headache because the instructions for these forms are over 450 pages long, and you have to pick from about 30 different categories. If you check the wrong box, even by mistake, you’ve technically signed a false legal document under penalty of perjury.

Why are foreign banks suddenly demanding this information?

Because of a law called FATCA, banks all over the world—including those in China and Hong Kong—are now required to hunt down and report data on any account holders who might be U.S. taxpayers.

How does this affect my ability to maintain a bank account?

It puts you in a “Catch 22” situation. If you live abroad and want to open or keep a local bank account, you are often forced to give up this private tax info to the bank, or they might refuse to work with you.