Part II: Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

A post in August 2014 explained the basic rule of who is a “long-term resident” as that technical term is defined for tax purposes in IRC Section 877 (e)(2). There is much confusion about how the tax law defines a “lawful permanent resident” (“LPR”) versus  how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

See –

Posted on August 19, 2014

This follow-up comment is to highlight some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law.

- A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particicular case.

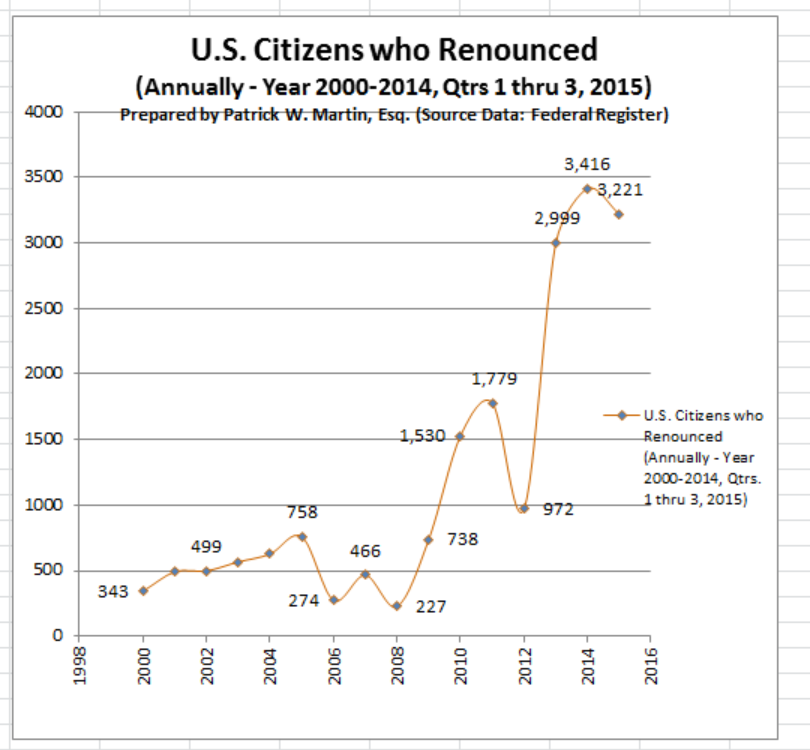

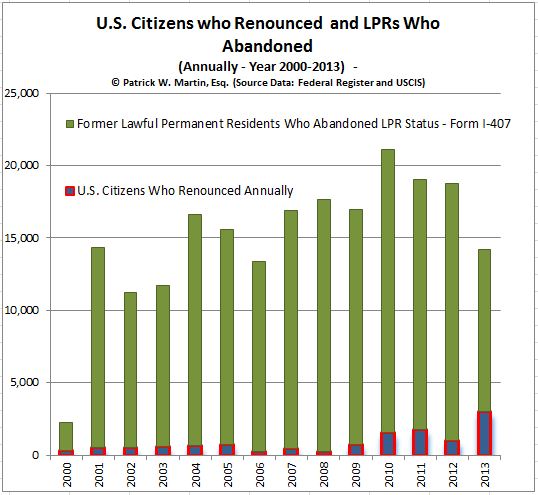

- There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

- Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

- There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card, Posted on August 15, 2015

Will U.S. Tax Law Regarding “Covered Expatriates” get Modified with Recent Government Push in International?

It is rare to have the President of the United States hold press conferences specifically dealing with international tax policy and tax enforcement. Nevertheless, this is what happened last week when President Obama announced his administration’s recent efforts in the field of international tax, anti-corruption and financial transparency.

His remarks can be watched here: President Obama’s Efforts on Financial Transparency and Anti-Corruption: What You Need to Know

Also, the White House is putting forward a series of initiatives in this area:

Fact Sheet: Obama Administration Announces Steps to Strengthen Financial Transparency, and Combat Money Laundering, Corruption, and Tax Evasion

To date, none of the specific initiatives address current “tax expatriation law” under IRC Sections 877, 877A, et. seq.

IRS Creates “International Practice Units” for their IRS Revenue Agents in International Tax Matters

The U.S. international tax law has become increasingly complex. I am confident when I say that very few individuals in the world (including IRS revenue agents) understand the complexities of Title 26 and Title 31 as they apply to  international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

Most USCs and LPRs who live in the U.S. certainly know and understand the basics of IRS Form 1040.

However, the type and scope of international transactions contemplated by the law can be significant and are rarely understood in any depth, even by many tax professionals. I have seen cases during my career of sophisticated individuals ranging from Nobel prize winners to U.S. Ambassadors, who had not a clue about the application of U.S. federal tax law to their lives. See, the Nov. 2, 2015 post, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

The lack of knowledge of these complex laws within the IRS, and the LB&I (Large Business and International group) which specializes in international matters has led to IRS “International Practice Units”. These are designed to allow IRS revenue agents who are not necessarily specialists in the international tax area to review transactions and be prepared to assess taxes and penalties against USCs and LPRs in the international context. The preamble says in part ” . . . Practice Units provide IRS staff with explanations of general international tax concepts as well as information about a specific type of transaction. . . ”

There are currently 63 different IRS “International Practice Units” all with dates from the last 12 months. Several of them focus heavily on information return filings which carry stiff penalties, even if no U.S. income taxes are owing. For instance see, Monetary Penalties for Failure to Timely File a Substantially Complete Form 5471 –Category 4 & 5  Filers.

Filers.

Another interesting IRS International Practice Unit is titled – Basic Offshore Structures Used to Conceal U.S. Person’s Beneficial Ownership of Foreign Financial Accounts and Other Assets.

These IRS materials give a good perspective from where the IRS views the world; including the introduction to this particular IRS International Practice Unit where it states: “This Practice Unit focuses on a U.S. Person’s proactive steps to “conceal” their ownership of foreign financial accounts, entities and other assets for the purposes of tax avoidance or evasion, even though, there may be some situations where there are legitimate personal or business purposes for establishing such arrangements. This unit falls under the outbound face of the matrix and thus, will focus on U.S Persons living in the United States . . . Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .” [emphasis added]

This is a breathtaking statement from the IRS internal training manuals that “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and  other creditors . . .”?

other creditors . . .”?

The vast majority of the USCs or LPRs who I see who renounce or abandon their citizenship or LPR status, are living outside the United States and in most cases have spent almost all (if not all) of their lives outside the U.S.

Does the IRS mean that a family living in Switzerland that have dual national family members are “. . . .simply hiding the accounts from the Internal Revenue Service . . . ” if they are using, for instance, a Liechtenstein Stiftung to hold their family assets as part of an estate plan recommended to them by their Swiss legal and tax advisers?

Does the statement that this IRS International Practice Unit focuses on ” . . . U.S Persons living in the United States . . . ” give USCs and LPRs residing outside the U.S. relief from the IRS perspective of USCs simply hiding assets from the Internal Revenue Service? Will IRS revenue agents be sophisticated enough to distinguish between these two different groups; U.S. resident versus non-resident USCs and LPRs? Will the law be applied differently with respect to these resident versus non-resident U.S. taxpayers?

What role will these IRS “International Practice Units” play in forming perceptions and molding ideas of IRS revenue agents who have had little to no life experience in international affairs, multi-national families, global finance and international business operations?

More observations to come from specific IRS “International Practice Units.

U.S citizens (USCs) and Lawful Permanent Residents (LPRs): Caution When Making Gifts. US Tax Court Recently Ruled a 1972 Gift by Sumner Redstone Still Open to IRS Challenge

The statute of limitations is one of the most important considerations for any individual when considering what tax consequences the Internal Revenue Service (“IRS”) might argue they have for years past. This can occur many years into the future as explained further below.

Former USCs and LPRs can be in a particularly precarious position, as was recently demonstrated by a U.S. Tax Court case for a gift that was made decades ago in 1972. See, Redstone vs. Commissioner (TCM 2015-237). Although this U.S. Tax Court case involving Sumner Redstone had nothing to do with renunciation of citizenship, it shows how the IRS can reach back many years and even decades in assessing taxes it claims are owing. The newly (in year 2010) added IRC Section 6501(c)(8) makes this highly likely under current revised law.

- Transfers to U.S. Beneficiaries (e.g., U.S. resident or citizen children or grandchildren who might receive gifts or bequests from a “Covered Expatriate” the former USCs or “long-term resident” – Green Card Holders)

Former USCs and any U.S. beneficiaries of theirs (e.g., U.S. resident children or grandchildren who might receive gifts or bequests from the former USCs) should be cognizant of the statute of limitations. See a prior post from 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

As this prior post noted, there are at least three basic scenarios when there is no statute of limitations for federal tax matters are as follows:

1. The former USC or LPR does not file a U.S. income tax return, when they had a requirement to so file. IRC Section 6501(c)(3). See a post from 2014, When do I meet the gross income thresholds that require me to file a U.S. income tax return?

- Fraud when Tax Return Filed

2. There is fraud on the part of the taxpayer (e.g., the taxpayer intentionally does not report income). IRC Sections 6501(c)(1), (c)(2).

- Missing Information on Tax Return Filed – re: International Matters

3. The USC or LPR fails to report certain foreign transactions, including inadvertently neglecting to report. IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act” which also created FATCA. The types of transactions set above in the table provides a brief summary of when transactions can give rise to an “open” statute of limitations period. In other words, as many years and decades can pass (see Redstone 1972 gift transaction) before the IRS ever has to make a proposed assessment of taxes and penalties. These include numerous ownership or economic interests in foreign (non-U.S.) companies, partnerships, foreign trusts, foreign investment accounts, among others.

This is indeed one of those areas where the IRS can argue a “gotcha moment”; simply because the former USC or LPR was not aware of the extremely complex rules of reporting assets (normally in their own country of residence outside the U.S.). The consequences to these families can go on indefinitely, per post from September 2015, Finally – Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

For a more in depth review of the international (non-U.S.) transactions that give rise to this reporting, see IRS Forms 3520, 3520-A, 5471, 8865, 5472, 8938, 8858, 926 among others.

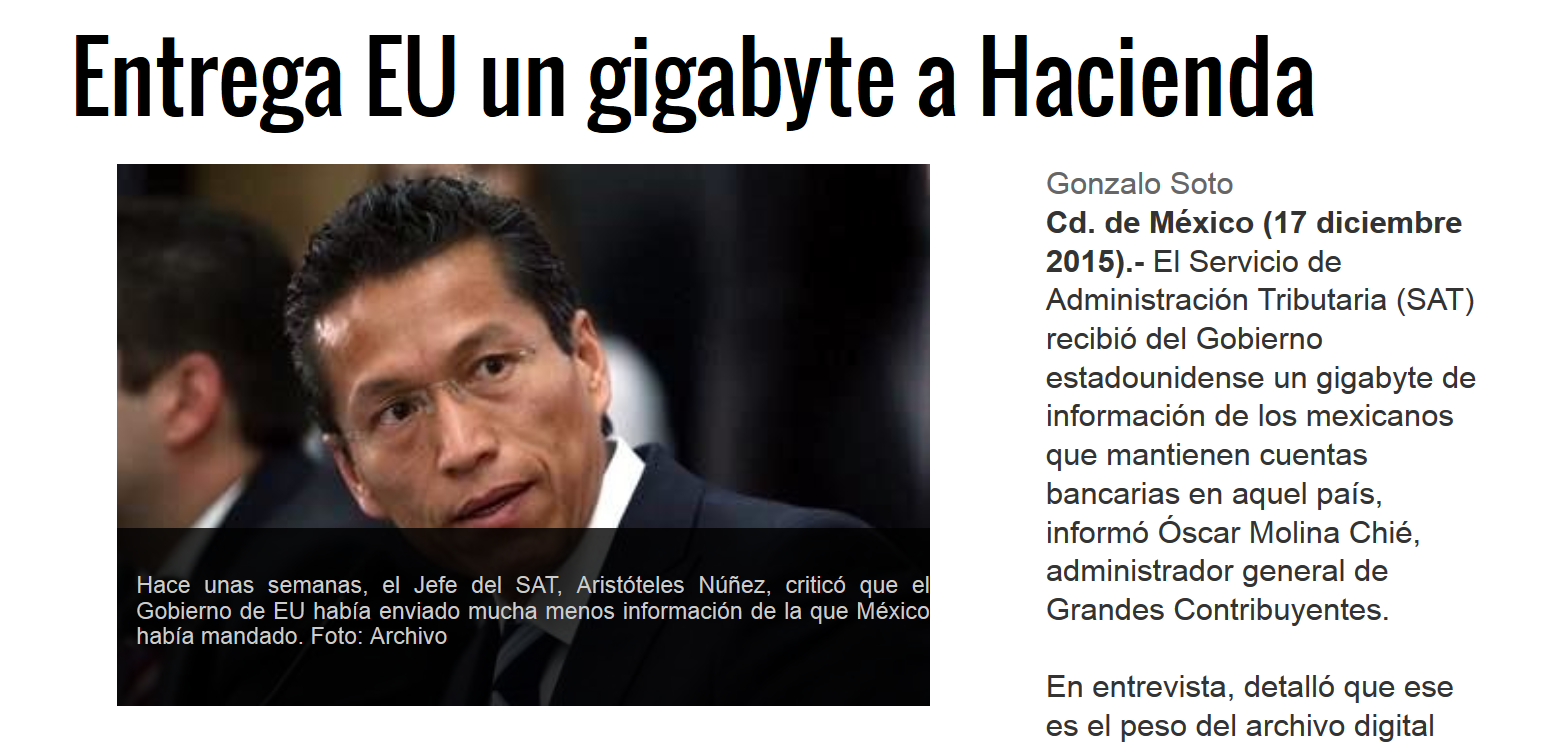

Foreign Government Receives a “FATCA Christmas Gift” from IRS: 1 Gigabyte of U.S. Financial Information

The last post discussed how the director of the Mexican tax administration was critical of the U.S. federal government for not providing FATCA information on U.S. financial accounts. See, Foreign Government Criticizes U.S. Government for  NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

The automatic exchange of bank and financial information is driven by the U.S. Treasury driven Intergovernmental Agreement (IGA).

As a follow-up, the Mexican newspaper Reforma reported on the 17th of December that the U.S. just provided Mexico’s treasury with a gigabyte of Mexican taxpayer information regarding U.S. financial and bank accounts. See, Entrega EU un gigabyte a Hacienda, dated Dec 17, 2015.

This news comes on the heals of the earlier criticism by the Commissioner of the Mexican IRS (SAT – Servicio de  Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Finally, the article emphasized that Mexico has sent the IRS information regarding Mexican bank accounts of U.S. citizens.

The question is how much Mexican bank and financial information has actually been provided by SAT of the hundreds of thousands (if not more than 1 million) dual national taxpayers, who are citizens of both Mexico and the U.S.? See, Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand, dated January 28, 2015.

Revocation or Denial of U.S. Passport: More on new section 7345 (Title 26/IRC) and USCs with “Seriously Delinquent Tax Debt”

New Section 7345 completely modifies how U.S. citizens (“USCs”) living and traveling around the world have to now consider very seriously actions taken by the Internal Revenue Service (“IRS”). It is the IRS which now holds the power under this new law that requires the U.S. Department of State (“DOS”) to revoke or deny to issue a U.S. passport in the first place.

New Section 7345(e) provides in relevant part as follows: “upon receiving a certification described in section 7345 of the Internal Revenue Code of 1986 from the Secretary of the Treasury, the Secretary of State shall not issue a passport to any individual who has a seriously delinquent tax debt described in such section. . . ” [emphasis added].

This new law mandates (not at the discretion of the DOS) that various U.S. passports be denied at the direction of the IRS. Once the IRS issues the certification of “seriously delinquent tax debt.”

All it takes, is for the IRS to claim tax or penalties are owing of at least US$50,000 through an assessment (plus start a lien or levy action).

Of course, US$50,000 sounds like a large sum for many modest USCs, until an individual understands that there are a host of international reporting requirements for taxpayers. Specifically, the IRS can impose a US$10,000 penalty for each violation of failing to complete and file various IRS information forms; EVEN IF NO income  taxes are owing. See IRS website – FAQs 5 and 8 regarding civil penalties (see also How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas).

taxes are owing. See IRS website – FAQs 5 and 8 regarding civil penalties (see also How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas).

For a summary of these forms and filing requirements, see a prior post, Oct. 17, 2015, Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

Indeed, our office has seen and assisted numerous taxpayers around the world where the IRS has assessed tens of thousands, hundreds of thousands and in some cases in excess of US$1M (in proposed assessments) against an individual for failure to simply file information reporting forms. See, for instance, a prior post on Nov. 2, 2015, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

Also, we have seen several IRS assessments of income tax (not just penalties) against individuals of hundreds of thousands of dollars which are not supported by the law. For instance, it is not uncommon for the IRS to issue a “substitute for return” alleging income taxes owing. See, How the IRS Can file a “Substitute for Return” for those USCs and LPRs Residing Overseas, posted Nov. 8, 2015. We have a number of those cases pending, where the IRS has taken erroneous information and made such assessments against USCs residing and working outside the U.S. for much if not most of their professional lives.

New Section 7345 requires that USCs, wherever they might reside, take great care in knowing about any actions the IRS might be taking against them; as to tax and penalty assessments, whether or not they are supported under the law.

One basic method of learning more about the activities of the IRS is to make a transcript request directly to the IRS regarding the status of a USC’s federal tax status according to IRS records. See, IRM, Part 21. Customer Account Services . . . Section 3. Transcripts.

It is also possible for the USC to obtain additional tax information from the IRS through a Freedom of Information Act (“FOIA”) request.

IT AIN’T FAIR: First (1) taxing me as a U.S. citizen and then (2) taxing me on my relinquishment or renunciation of U.S. citizenship or LPR abandoment and further (3) taxing my children on their inheritance from me!@!@!

This sums up the argument of many critics of U.S. citizenship based taxation of worldwide income.

Many may agree with this conclusion from an equity or sense of fairness argument. See proposal below at the end of this post.

However, the argument of fairness has little place in interpretations of Title 26, the U.S. federal tax law. For example, the U.S. Tax Courts are not courts of equity. See, The United States Tax Court – An Historical Analysis, Dubroff and Hellwig, footnote 668.

Also, virtually no courts of the U.S. find U.S. tax laws to be unconstitutional. It is a very rare occurrence that the U.S. Supreme Court even takes up a tax case to determine its constitutionality. The “Obamacare” with broad application throughout society was a case heard by the Supreme Court which upheld a law signed by President Obama on March 23, 2010, more correctly called the Patient Protection and Affordable Care Act. That law increased Medicare taxes and imposed a penalty surcharge on individuals who do not maintain certain health coverage.

In contrast, U.S. citizens and lawful permanent residents (LPRs) residing overseas are a relatively small population of the U.S. taxpayer population. Accordingly, it was only until late the U.S. government even began focusing on this population to collect taxes from them. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?, posted March 6, 2014.

Finally, see various proposals to modify the law: e.g., U.S. Citizenship Based Taxation – Proposals for Reform – “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

Executive Summary

This paper proposes to eliminate the U.S. citizenship based taxation and create a consistent exit tax system. The complex web of the current U.S. tax law has made it nearly impossible for all but the most sophisticated U.S. citizens and lawful permanent residents (“LPRs”) residing overseas to file complete and accurate tax returns. The proposal should bring consistency, tax simplicity for taxpayers residing outside the U.S., and do so in part by eliminating the U.S. citizenship based tax system, which is unique in the world, dates to the civil war and is inappropriate for the global world we live in.

- Summary of Current Status of the Law

To date, there is no serious and comprehensive proposal to modify the U.S. federal tax law imposing U.S. taxation of the worldwide income of USCs and LPRs residing outside the U.S.

There are also no serious proposals to repeal the current U.S. “expatriation tax” on (1) mark to market income and gains (When does “Covered Expatriate” Status -NOT- matter?) and (2) the 40% tax on covered gifts and inheritances (see, Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

One sure way to “get expatriated” as a lawful permanent resident (even if that was not the plan) is to file a false federal tax return, statement or provide false information to the government. U.S. citizens cannot be deported for filing false tax returns, due to Constitutional rights.

Kawashima vs. Holder, (2012), is a story of a Japanese family that lived legally in the U.S. with lawful permanent residency status. According to the L.A. Times,

“Akio and Fukado Kawashima came to Southern California in 1984 as lawful Japanese immigrants determined to succeed in business. They operated popular sushi restaurants in Thousand Oaks and Tarzana and recently opened a new eatery in Encino.

But after they underreported their business income in 1991, they paid a hefty price. The Internal Revenue Service hit them with $245,000 in taxes and penalties. The couple pleaded guilty and paid in full. A decade later, the Immigration and Naturalization Service decided to deport them. . . “

The crucial mistake was the filing of a false return as defined under IRC Section 7206(1):

“(1) Declaration under penalties of perjury . . . Willfully makes and subscribes any return, statement, or other document . . . made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter . . . “

The Supreme Court ruled in this case that the false return that generated a revenue loss of at least US$10,000 for the government was properly classified by the government as an “aggravated felony.” In other words, the tax returns were materially false (which the taxpayers had plead to previously) and created an unpaid tax liability of at least US$10,000. The Supreme Court cited the immigration law (Title 8) and found such an offense to be a violation of Section 1227(a)(2)(A)(iii) as an:

“(iii) Aggravated felony

Any alien who is convicted of an aggravated felony at any time after admission is deportable.

The false tax return which created a tax liability of a relatively low threshold of US$10,000 therefore carries potentially sever consequences.

See a prior post that briefly discusses IRC Section 7206(1), see, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

While most USCs residing overseas will never be concerned about deportation (which should generally not be available to the government, due to constitutional rights of the U.S. citizen) LPRs filing tax returns will indeed want to consider carefully the implications of ” . . . any [and all tax and other] return[s], statement[s], or other document[s] . . . ” submitted to the federal government.

Also, prior posts discussed the law and risks associated with filing or sending false documents, information or returns to the Internal Revenue Service (“IRS”) –

See,Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer, posted July 19, 2014;

*Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?* posted March 6, 2014, Will the Justice Department and Criminal Investigation Division of the IRS Turn Their Sights on USCs or LPRs living Overseas? posted March 19, 2014,

The relevance of the Kawashima case to readers of this blog, is how a “long-term resident” may inadvertently find they will trigger the “mark-to-market” tax on their worldwide assets and later cause their U.S. beneficiaries to be subject to what is currently a 40% tax on the receipt of certain gifts and inheritances. See, prior posts on LPR status – Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?, posted August 19, 2014.

Some prior news coverage of the Kawashima v. Holder case here:

Legal immigrants face deportation for filing false tax return

The Supreme Court rules against a couple who pleaded guilty and paid in full, saying the crime was an ‘aggravated felony’ subject to automatic deportation. Tax lawyers say the decision is ominous.

February 26, 2012|By David Savage and Catherine Saillant, Los Angeles Times

Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card

The “tax expatriation” statutory provisions are fraught with ambiguity and incomplete answers for those individuals who have cases that span different time periods. This is because the law has been changed numerous times over the last several years and ad hoc concepts added, including the technical concept of “long-term residents” for the first time in 1996. As has been previously explained, the first “expatriation tax” law was not adopted until 1966 as part of the The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of U.S. Tax Expatriation Law (Posted on April 6, 2014).

Next, 1996 amendments kept the basic regime but added a number of key concepts, including “long-term residents”. The changes in the law in 2004 made significant changes and in 2008 the first “mark to market” regime was adopted. Each time, the concept of “long-term residents” was maintained, but without clear thought as to the meaning and timing of “expatriation” in various cases. See, Timeline Summary of Changes in Tax Expatriation Provisions Since 1996, (Posted on April 9, 2014)

Unfortunately, none of these amendments to the law over the years carefully incorporated transition and timing rules for cases where the individual has lived in (or had U.S. citizenship or LPR) during one more of these time periods:

- 1966-1996

- 1996-2004

- 2004-2008

- 2008-present

There are many inconsistent concepts among the law and one clear example is demonstrated by an individual who became a lawful permanent resident prior to 1996 and prior to amendments in the definition of a “resident alien” which was adopted generally in the federal tax in the law in 1984. This 1984 definition was not part of any specific “expatriation tax” provisions.

Remember, the technical definition of who is a “resident alien” is the basic definition of who is generally subject to U.S. income taxation on their worldwide income. See, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

Prior to 1984, a LPR was not necessarily an income tax resident of the U.S. This concept of LPR (i.e., a “green card”) driving U.S. income tax residency was adopted in 1984, long before Congress became obsessed with U.S. individual tax expatriation. For background in the law, see the 1985 Penn State Law Review Article – Internal Revenue Code 7701(b): A More Certain Definition of Resident

The Joint Committee on Taxation report on the 1984 changes in the tax law (“General explanation of the revenue provisions of the Deficit Reduction Act of 1984 : (H.R. 4170, 98th Congress; Public Law 98-369)“) addressing the tax residency test of “lawful permanent residency” rules provides the following language:

. . . The Act defines “lawful permanent resident” to mean an individual who has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, if such status has not been revoked or administratively or judicially determined to have been abandoned. Therefore, an alien who comes to the United States so infrequently that, on scrutiny, he or she is no longer legally entitled to permanent resident status, but who has not officially lost or abandoned that status, will be a resident for tax purposes. The purpose for this requirement of revocation or determination is to prevent aliens from attempting to retain an apparent right to enter or remain in the United States while attempting to avoid the tax responsibility that accompanies that right.

The logic of the LPR test is clear based upon this explanation. If one has the right to live in the U.S., they cannot avoid the tax responsibility that accompanies that right. However, as immigration lawyers will explain, there is no right to enter the U.S. after you have abandoned your LPR status and moved outside the U.S. on a permanent basis.

At the same time, there is other discussion in the report that would support the position that these provisions only apply for the years 1985 and thereafter (long after many individuals obtained LPR status, but who moved out of the country – e.g., in cases where individuals obtained LPR in the 1970s and left before 1985). Specifically, the explanation in the Joint Committee of Taxation is as follows:

. . . The purpose of this effective date rule is to delay tax resident status for only new green cardholders for a short time. Congress understood further that an alien may acquire lawful permanent resident status for immigration purposes before U.S. presence. Congress sought to impose tax resident status on all lawful permanent residents once they arrive in the United States. The Act does not affect the determination of residence, even for green card holders, for taxable years beginning before January 1, 1985.

Of course, the report by the Joint Committee on Taxation (“JCT”) is not the law and does not bind the IRS or the taxpayer. However, the JCT usually get their explanations of the law right.

Why is all of this important for LPRs who never formally abandoned their “green card”? The IRS might well try to argue they never terminated their U.S. federal income tax residency for purposes of the “tax expatriation provisions”, as later versions of the statute impose an obligation to notify the IRS. If the individual never notified the IRS, the government might ar

See, for instance Section 7701(b)(6) with specific rules for LPR individuals who live in a country with a U.S. income tax treaty. Importantly, the definition of a lawful permanent resident for tax purposes (as defined in Section 7701(b) ) is not identical to the definition for immigration law purposes as the legislative history to the 1984 amendments to the law explains.

See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9.

Finally, the information required as part of the process of formal abandonment is much more extensive than in the past.

A prior post discussed the published USCIS immigration form I-407 for LPRs who must now use it when formally abandoning LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

See, new I-407 Form requires that much more information and is 2 pages in length.

“Expatriation” Implies Leaving the U.S., But Many More Want to Come to the U.S.: Tax Consequences

U.S. citizens and long-term residents who are considering renouncing their citizenship or abandoning their lawful permanent residency (“LPR”) are increasingly undertaking more sophisticated life and tax planning before “taking the plunge”!

Many (in my experience – all) of these “expatriates” eventually want to be able to visit the U.S. and in some cases possibly come back to live permanently. Many simply apply for and obtain a B1/B2 visa.

To appreciate how many more persons want to immigrate to the U.S. compared to emmigrate from it, see an earlier post: The Number of Citizens Leaving (Renouncing) Versus Coming (Naturalizing) is Just a Speck

This is the other “side of the coin” so to speak, since individuals contemplating coming to the U.S. often should undertake pre-immigration tax planning. One means for non-U.S. citizens to become LPRs and eventually U.S. citizens, is through the EB-5 visa program.

Immigration attorney Ms. Teodora Purcell has written prior guest posts, including: When is the loss of US nationality effective? [Guest Post from Immigration Lawyer]

The next post on this site will be a complete article by Ms. Teodora Purcell explaining in more detail the EB-5 visa program and recent developments.

As to the tax implications of immigration to the U.S. (as opposed to emigration from it), I wrote the tax chapter in the latest edition of the American Immigration Lawyers Association (“AILA’s) treatise – Immigration Options for Investors & Entrepreneurs US$199.

That treatise is heavily focused on “EB-5 investors” and the tax discussion is titled: Key U.S. Tax Considerations for EB-5 (& Other) Visa Applicants.

Ms. Teodora Purcell’s contact information is set out below:

Teodora Purcell | Attorney at Law

FRAGOMAN

11238 El Camino Real, Suite 100, San Diego, CA 92130, USA

Direct: +1 (858) 793-1600 ext. 52424 | Fax: +1 (858) 793-1600

TPurcell@Fragomen.com