International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

World Cup & Playing in the United States: Green Card Holders, the Treaty Tiebreaker, and the Global Athlete or Entertainer

As the world’s athletes have arrived to perform on U.S. soil, the U.S. tax system is a broad net. The 2026 FIFA World Cup—hosted across the United States, Mexico, and Canada—is a useful occasion to revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

This blog is dedicated to issues of “tax expatriation” which crosses into different professions and global lifestyles. See, for instance the following prior blogs:

There are of course many famous athletes who were not U.S. citizens and then became green card holders and oftentimes then became naturalized U.S. citizens. Since the Knicks just won the NBA championship after 53 years, one of their greatest, Patrick (mi tocayo) Ewing left Jamaica as a boy, became a green card holder and then a naturalized citizen. A 1985 New York Times article, A Favorite Son Goes Home, describes his first return to the island since a boy.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

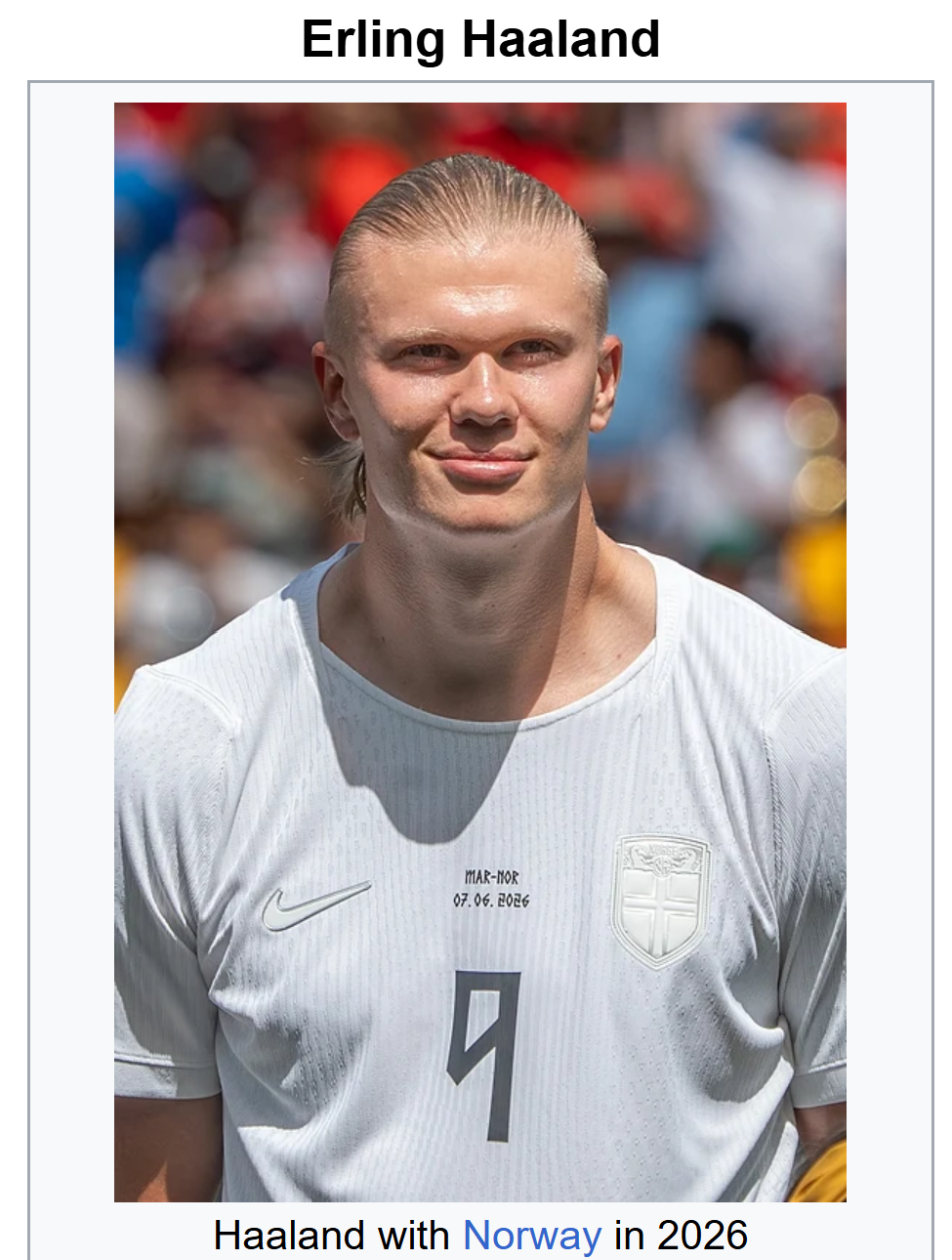

Athletes and entertainers are specially taxed in the U.S. in the sense they typically receive few benefits from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

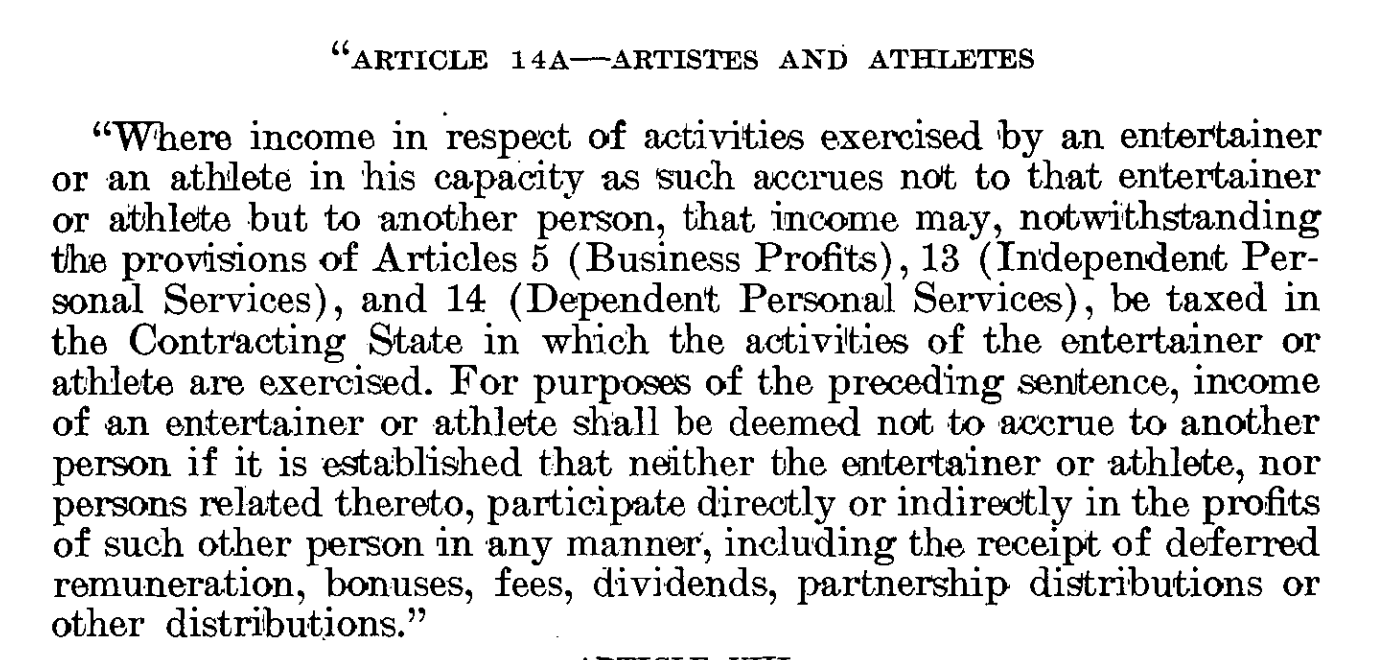

A protocol to the treaty adopted in 1980 has a “new” article 14A specific to artists and athletes as reflected here in its entirety allowing the government to tax athletes and entertainers when they perform in the country (overriding other protective provisions of the treaty – e.g., Business Profits Art. 5, Independent Personal Services Art. 13 and Dependent Personal Services Art. 14):

The IRS also adopted a specific program, called the Central Withholding Agreement (“CWA”) program created by Revenue Procedure 89-47 specific to artists and athletes. I personally think it is a program that is not authorized by the statute and often applied by the IRS in a manner that violates the withholding tax regime we have in Chapter 3 of our statutory tax law, Subtitle A. In practice, third parties are subject to the 30% withholding tax on certain gross proceeds paid to companies other than the artist or athlete, if the athlete or artist doe not participate with the IRS in their CWA.

Mexico

In the case of global soccer players, even one with a “lawful permanent resident” card (i.e., a “green card”) they may be subject to the Chapter 3 withholding tax rules if the athlete is like Mr. Aroeste (Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC)) holding a green card in his pocket, but not a U.S. income tax resident by application of the residency rules set forth in an income tax treaty. Will the soccer player become a “covered expatriate” and not even know it (oops)?! It can get tricky quickly. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

Meanwhile, Mexico and the U.S. have both advanced to the knockout round.

Canada plays Switzerland and presumably has a 99% chance of advancing to the Round of 23.

Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

This post is written simply because so many U.S. citizens residing overseas are reasonably confused about the complexity of U.S. tax law. The mere requirement to file U.S. income tax returns for those overseas often comes as a great surprise. My non-U.S. born wife is an exception (as she also lives outside the U.S.) simply because I have repeatedly told her for our 20 some years of marriage.

Some in the IRS erroneously think U.S. citizens residing overseas do and should understand U.S. tax law. I posed one simple scenario to a very sophisticated IRS attorney not very long ago who specializes in the FATCA rules.

Her view is (hopefully was) that U.S. citizens throughout the world know or should know the U.S. tax laws because the instructions to IRS Form 1040 are clear.

This thought knocked me off my figurative chair onto the floor! Smack.

My surprise is based upon my own experience working with individuals and families throughout the world, in numerous countries. I have noticed a number of notions, based upon these andectodal experiences as follows:

A minority of U.S. citizens (unless they lived most of their lives in the U.S. and recently moved overseas as an “expatriate”) have no real basic idea of how the U.S. federal tax laws work; let alone to their assets and income in their country of residence. See USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

There are indeed plenty of immigrant U.S. residents (certainly less than 50% by my own experience – especially when concepts of PFICs and foreign tax credits start being discussed) who even understand the basics of U.S. international tax law.

Even those in English speaking countries that have less historical or family ties to the U.S. have a lesser understanding (e.g., New Zealand, Australia, Kenya, South Africa, India, etc.).

Those who do not speak English know even less about U.S. tax laws and how they apply to them.

Many individuals who learn of these requirements overseas are sometimes driven to great despair. The message they receive is not a correct one under the law in my view: as they read IRS materials (for instance, see FAQs 5, 6 and and former 51.2 from the Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers 2014) and come to the conclusion they will soon be going to jail, criminally prosecuted or otherwise be subject to tens of thousands of dollars worth of penalties for their failure to file a range of tax forms.

Individuals around the world (even tax professionals) and certainly laypeople, are not commonly reading TaxAnalysts (nor would they subscribe) or other tax professional publications that explain many of the intricacies of U.S. tax laws.

Learning and understanding U.S. tax laws, including just the basics, requires a great deal of time, aptitude for nuances and details, literacy, patience and a level of aptitude for such matters that simply escape many people around the world (most I would say). see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. I can relate to this personally, as I am an international tax professional (indeed I even studied a post graduate law course outside the U.S. in a non-English language), have spent my entire professional career of more than 25 years in the area, and yet only generally have a very superficial understanding of tax laws throughout the countries where I am dealing with clients. I don’t try to understand the details of those laws.

Back to the intelligent IRS tax attorney. My question to her was: “Why would you, as a U.S. born individual not be reviewing the tax laws, tax forms and tax instructions of the country where your parents were born prior to immigrating to the U.S.?” I asked: “Are you not reviewing those laws in the original language of your parents (not English, but the other language of your parent’s country) to understand what tax forms and returns you should be filing?”

The IRS attorney’s response was: “What: of course, I am not reviewing such tax forms or filing information or tax laws, as I would have no tax obligations in that foreign country where I have no income, no assets or no bank or financial accounts!”

My follow-up question was a simple one: “Don’t you realize that U.S. federal tax law (Title 26) and financial bank reporting laws (Title 31) do just that!”

“Hmm she paused: how can that be?” I don’t recall if she said this out loud, or just said it with her puzzled expression.

Here is the big disconnect. It’s not just among the ill-informed or those lesser educated on the fine points of law. I had the pleasure this week along with my wife to host two educated, worldly and engaging individuals who have been married some 20 years together. They are well read and highly educated. Both are lawyers by training, one practices law that often pushes him fairly deeply into the tax law and his wife is a wonderful and experienced judge in the California state courts.

All of it was a great surprise to them! They were in utter shock and both are residents in the U.S., highly educated in the law and are like the vast majority of the world, including U.S. citizens who reside outside the U.S.

This is the common response for many U.S. citizens residing overseas.

12 Year Old (and Older) U.S. Citizens Residing Outside the U.S. Must Have An “In-Person” Interview in a U.S. Embassy or Consulate for SSN Application in 1 of Just 17 Posts Worldwide

This dilemma affects numerous USCs throughout the world, which is now compounded by the certification and reporting requirements of USCs and third parties, such as FFIs and NFFEs[2] under the Foreign Account Tax Compliance Act (“FATCA”).

* * *

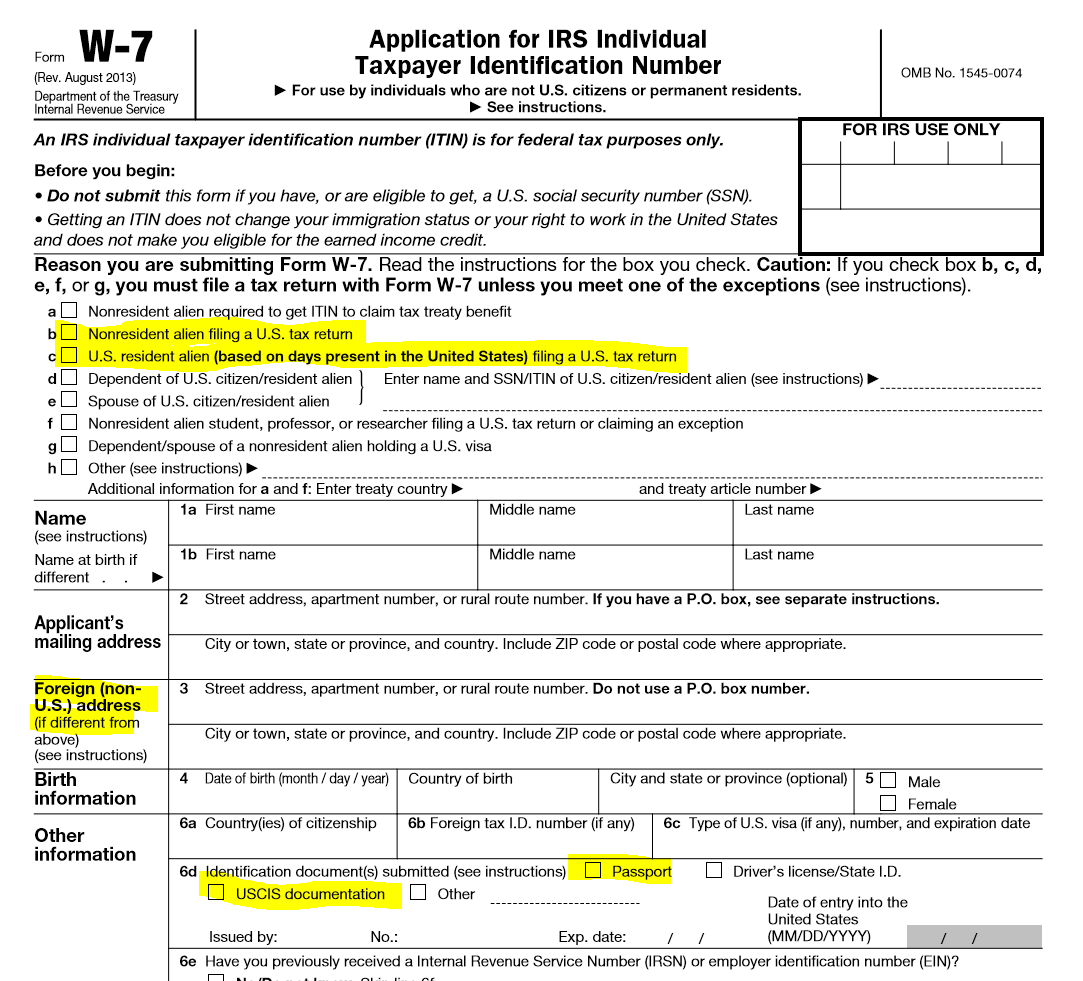

The regulations provide the specific rule that all USCs must have a SSN[1] as their TIN. There are no general exceptions in the regulations to the requirement that a USC must have a SSN as their TIN.

This regulatory requirement specifically directs the USC to the forms that must be completed and filed with the SSA, in order to obtain a SSN, as follows:[2]

(1) Social security number. Any individual required to furnish a social security number pursuant to paragraph (b) of this section shall apply for one, if he has not done so previously, on Form SS-5, which may be obtained from any Social Security Administration or Internal Revenue Service office. He shall make such application far enough in advance of the first required use of such number to permit issuance of the number in time for compliance with such requirement. The form, together with any supplementary statement, shall be prepared and filed in accordance with the form, instructions, and regulations applicable thereto, and shall set forth fully and clearly the data therein called for. Individuals who are ineligible for or do not wish to participate in the benefits of the social security program shall nevertheless obtain a social security number if they are required to furnish such a number pursuant to paragraph (b) of this section. [emphasis added]

These Title 26 regulations discuss individuals requesting forms from “any Social Security Administration or Internal Revenue Service office” which clearly implies that the SSA and the IRS have offices overseas.

Unfortunately, this is not the case, as the IRS recently announced it is closing its full-time walk-in offices in London, Frankfurt and Paris, as the office in Beijing, China was closed in 2014.[3] Similarly, the SSA has no overseas offices, but does have limited field office operations in Canada, the British Virgin Islands and Samoa.[4]

Therefore, it is clear that the above regulations are speaking to individuals who reside and live in the U.S., and not USCs residing overseas when it requires USCs to “ . . . make such application far enough in advance of the first required use of such number to permit issuance of the number in time for compliance with such requirement.[5]

These Title 26 regulations require the application be made well in advance of any tax filing requirements are not realistic for USCs residing overseas as is explained herein. This author has seen the issuance of SSNs take more than 6 months, even when the USC could have an interview in their country of residence.

More importantly, there are very few countries (only 17) where in-person interviews can even be held. See, discussion below.

USCs who have lived most, if not all of their lives outside the U.S., commonly do not have a SSN. The procedural requirements imposed by the SSA to obtain a SSN in these cases are complicated and unrealistic for USCs living overseas.[6] This author has seen cases where USCs residing overseas have even spent the money and resources and time to travel to the U.S. to apply for a SSN, yet were turned away by the SSA, due to various procedural requirements which were not satisfied.

Often times obtaining a SSN overseas is nearly impossible, depending upon which country and where within that country the USC resides.

A. Obtaining a SSN Outside the US by a USC – Much More than Just Filing SSA Form SS-5

The SSA does not have offices outside the U.S. although they have a so-called “Office of International Operations.”[7] The focus of OIO is the administration of social security benefits, not obtaining SSNs for USCs residing overseas. Since the SSA is assisted by the U.S. Department of State (who are not SSN experts), USCs have to rely upon various U.S. embassies and consulate offices around the world, as they try to obtain a SSN.

B. Tax Return Filing Requirements – Minimum Gross Income

Any USC individual is obligated under the U.S. federal tax law to file a federal income tax return IRS Form 1040 if they meet minimum thresholds of income. For the tax year 2015, the thresholds are low, and are reached once the gross income is at least the sum of (i) the “exemption” amount (currently $4,000) and (ii) the “standard deduction” amount (currently $6,300 for single and married filing jointly and $12,600 for married couples filing jointly).[8]

This is true, even if all of the income is earned income and eligible for the foreign earned income exclusion, which is $100,800 for the tax year 2015.[9]

Additionally, USCs living overseas necessarily have a U.S. tax return filing requirement, when they meet these low thresholds of gross income. In these cases, tax returns that are not filed by the 15th of June are not considered timely filed.[10]

II. The Social Security Administration Rules Make it Nearly Impossible for Many USCs Overseas to Reasonably Obtain a SSN

The policy and procedures of the SSA regarding issuing SSNs have changed significantly over the years.[11] The Social Security Administration (SSA) provides a detailed chronology of the major changes in policy and procedures regarding filing for and obtaining a SSN.[12] One of the most significant revisions in the last decade came from The Intelligence Reform and Terrorism Prevention Act of 2004 (P.L. 108-458), which imposes various standards for the verification of documents or records submitted by an individual.

A. Only a Few Countries Around the World have Personnel at U.S. Embassies or Consulate Offices that Can Process SSN Applications – SSA Form SS-5-FS

Applying for SSNs overseas is severely restricted compared to an application in the U.S.

According to the U.S. Department of State, Foreign Affairs Manual (“FAM”), only certain “Claims-Taking Posts” in specific countries “may” include “processing applications for Social Security Numbers.” [13]

These 17 countries (and a city in the case of Jerusalem) with Claims-Taking Posts include:

“Austria, Argentina, Costa Rica, Dominican Republic, France, Germany, Greece, Ireland, Italy, Japan, Jerusalem, Mexico, Norway, Philippines, Poland, Portugal, Spain, and the United Kingdom.”

Noticeably absent are many Western European countries, virtually all of Latin America, virtually all of Asia, virtually all of Eastern Europe, all of the Middle East (except Jerusalem), all of the African continent, all of the Australian continent and surrounding island countries and Russia, among many other significant countries, including OECD member countries.[14]

Nothing in the FAM requires any of these “Claims-Taking Posts” to actually process applications for a SSN. Plus, there are of course hundreds of other countries throughout the world, not listed above, which do not have such a U.S. Department of State Post. For these reasons, USCs in countries such as China must travel to a U.S. Department of State Post (e.g., the Philippines) which is able to process applications for SSNs.

B. In Person Interview Required for Individuals Older than 11 Years Old

Individuals who are older than 11 years old must personally go to the U.S. Embassy or Consulate with a Claims-Taking Post. See 7 FAM 530, pages 7, 12, 13 and 7 FAM EXHIBIT 530(D) Mandatory In-Person Interview Worksheet SSN Applicant Age 12 or Older – Original SSN * * *

All of these rules makes you wonder whether foreign born individuals, such as actress Kim Cattrall from Sex & the City fame would have ever obtained a social security number overseas while she lived in Canada or the UK.

[3]See, Bloomberg article, 14 January 2015 by Kocieniewski, IRS Will Shut Last Overseas Taxpayer-Assistance Centers: “After budget reductions over the last four consecutive years, the IRS is forced to make tough choices during this period of fiscal austerity and these closures have relatively little impact on taxpayers and treaty partners,” said Julianne Breitbeil, an IRS spokeswoman. Also, see IRS website that still reflects the London and Paris offices as open http://www.irs.gov/uac/Contact-My-Local-Office-Internationally.

[6] See discussion below, regarding requirements to obtain a SSN. I.II, I.I,The Social Security Administration Rules Make it Nearly Impossible for Many USCs Overseas to Reasonably Obtain a SSN

[7] See SSA website, “Office of International Operations” – http://www.ssa.gov/foreign/ “Service Around the World – Welcome to SSA’s Office of International Operations (OIO) home page. The purpose of this site is to assist Social Security customers who are outside the U.S. or planning to leave the U.S. OIO is responsible for administering the Social Security program outside the U.S. and for the implementation of the benefit provisions of international agreements. Since SSA has no offices outside the U.S., OIO is assisted by the Department of State’s embassies and consulates throughout the world.”

[8]See, IR-2014-104, Oct. 30, 2014 and IRS Publication 501.

[12]See, SSA website, Significant Milestones in Social Security Number Policy. A detailed chronology of the major changes in policy and procedures. http://www.ssa.gov/history/ssn/ssnchron.html.

[14] In contrast to these 17 countries (and one city – Jerusalem) where a USC residing overseas must travel to apply for a SSN, the Treasury Department has announced it has around 100 countries that have signed, or “have reached agreements in substance” a FATCA IGA. USCs throughout the world are required by the Foreign Account Tax Compliance Act (“FACTA”) to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . .”

This article reported that his U.S. tax bill was at issue – :

In case you missed it: London Mayor Boris Johnson has said he will renounce his U.S. citizenship following a high-decibel tax squabble with his country of birth. At issue: a tax bill U.S. tax authorities claimed he owed on some London property. The mayor will (of course) keep his citizenship in the U.K. as his political ambitions continue to play out.

Surely, he will be careful and thoughtful about the steps he is taking as part of his U.S. citizenship renunciation. His reported response to the news reporter last year could prove risky under U.S. law, to the extent he intentionally refuses to file U.S. income tax returns and pay taxes. The following line of questions and answers could be quite damning for him:

Presenter Susan Page then pressed him whether he would pay the bill, to which he said: “I think it’s outrageous.

“Well, I’m – no is the answer. Why should I? I haven’t lived in the United States for, you know, well, since I was five years old.

“I could but I pay – I pay the lion’s share of my tax, I pay my taxes to the full in the United Kingdom where I live and work.”

Here, the London Mayor has indicated he is not filing tax returns, yet knows he has a legal duty to file them and pay a tax owing under U.S. law. He goes further to say “I could . . . pay . . .” While rarely used standing alone by prosecutors (without other criminal claims brought), it is a crime that carries up to a 12 month prison sentence, to not file a U.S. return, supply information or pay tax; see, IRC § 7203. The relevant language of the statute is as follows:

Any person required under this title to pay any estimated tax or tax, or required by this title or by regulations made under authority thereof to make a return, keep any records, or supply any information, who willfully fails to pay such estimated tax or tax, make such return, keep such records, or supply such information, at the time or times required by law or regulations, shall, in addition to other penalties provided by law, be guilty of a misdemeanor and, upon conviction thereof, shall be fined not more than $25,000 ($100,000 in the case of a corporation), or imprisoned not more than 1 year, or both, together with the costs of prosecution.

Here, the government has yet another stick it can pull from its bag of sticks to be used against current and former U.S. citizens residing outside the U.S. It is of course, very common, that individuals who have spent most of their lives outside the U.S. have not filed any U.S. tax returns nor paid any U.S. income taxes. At what point, might these individuals have U.S. civil tax liability and what facts are necessary to give rise to criminal tax liability?

The vast majority of U.S. citizens residing overseas owe little to no U.S. income taxes because (i) modest income amounts and the impact of the “foreign earned income exclusion” or (ii) they reside in a country with higher taxes and tax rates than the U.S. because of the “foreign tax credit”. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

A couple observations about London Mayor Boris Johnson. First, he would be well advised not to make public statements about filing [or not] U.S. tax returns or paying [or not] U.S. taxes. Second, he will want to carefully consider completing and filing accurate U.S. tax returns as part of his formal renunciation process; particularly for the year in which he sold his London home tax free under UK laws. Third, he will want to understand carefully, the details of what is and should be filed on IRS Form 8854, after he has visited the U.S. embassy and files his Form DS-4080, Oath of Renunciation of the Nationality of the United States.

Finally, the case could present a unique international political and public relations nightmare for the U.S. Department of Justice, if they decided to bring any sort of criminal tax charges against the London Mayor. It would seem highly unlikely in my opinion.

“. . . The Assistant Attorney General, Tax Division . . . must approve any and all criminal charges that a United States Attorney intends to bring against a defendant in connection with conduct arising under the internal revenue laws, regardless of which criminal statute(s) the United States Attorney proposes to use in charging the defendant. See 28 C.F.R. § 0.70.

Also, only the Tax Division can authorize warrants of public officials, which presumably would extend to London Mayor Boris Johnson. See, See, 6-4.130, Search Warrants.

Li Lianjie – Famous Former U.S. Citizens – Born in Beijing, China (“Jet Li”)

The Chinese actor Li Lianjie, who is better known by his stage name Jet Li, was born in Beijing. He was born in 1963 and his father died when he was just 2 years old and he “. . . was from a very poor family and . . . didn’t have enough money for a good school, so sports-school was good . . . ”

He is a huge star in China and throughout Asia and became famous in Hollywood.

As a teenager he became a master at Wushu, the full-contact sport from Chinese martial arts. His martial arts fame led to acting, first in China and also in the United States. His film debut Shaolin Temple (1982), helped make him a star.

He apparently became a naturalized citizen of the United States while working in Hollywood.

He apparently has also become a naturalized citizen of Singapore.

He is often highlighted by government officials of China as a model citizen and success story.

Finally, the certification requirement that is available to those individuals who are born with dual national citizenship to avoid “covered expatriate” status, was presumably not available for Li Lianjie, since he was not born a U.S. citizen. Presumably, he could not satisfy each of the requirements of IRC Section 877A(g)(1)(B).

Famous Former U.S. Citizens – Oscar-winning actor Yul Brynner (Tax Rates Then and Now)

Yul Brynner was born as Yuliy Borisovich Briner in 1920 in Russia.

He won an Academy Award for best actor and two Tony Awards for the King and I. He also played the Egyptian king Ramses II in The Ten Commandments.

He started the process for naturalization of U.S. citizenship in 1943 according to the document, Declaration of Intention, filed with the U.S. federal district court in the Southern District of New York.

Note the photograph and prior residence identified as Dairem South Manchuria,

as his last place of foreign residency; which is a major port city located in China in the Liaodong peninsula. Apparently, Dairem is popular with Russian tourists. He was Russian.

This is particularly interesting, since Yul Brynner was Russian and apparently moved to what was then known as “South Manchuria”?

He renounced citizenship in 1965 in Bern, Switzerland, apparently for tax reasons according to a biography about his life.

The highest U.S. federal income tax rate in 1965 was 70% (compared to today’s 39.6% rate). See, Personal Exemptions and Individual Income Tax Rates, 1913-2002. The income tax rate was substantially higher then, compared with the current rate, although it is a bit like comparing “apples” and “oranges”; since the tax deductions, exemptions and credits that existed in 1965, look little like the current law.

Social security taxes in 1965 were about 1/2 the tax rate as today, but it only applied to the first US$4,800 of income (which represents about $36,125 in inflation adjusted dollars today). Current social security rates apply to the first $117,000 of income, without limits on the Medicare portion of 2.8%. For historical social security rates, see,

T.S. Eliot – Famous Former U.S. Citizens (Tax Rates Then & Now)

Thomas Stearns Eliot, who was better known as “T.S. Eliot” left the U.S. in the 1920s. He was recognized as one of the great writers of the early and middle 1900s. He published poetry, wrote plays and literature and was a social critic of his time.

T.S. Eliot received the Nobel Price for Literature.

He follows the lines of many other famous former U.S. citizens, in that he was not born on either the East Coast or West Coast of the U.S. He was born and raised in St. Louis, Missouri. Josephine Baker was also born in St. Louis, Missouri and Tina Turner in Tennessee, both famous individuals who shed their U.S. citizenship.

He either relinquished or renounced his U.S. citizenship as he became a naturalized British citizen in 1927. At the time, there were no adverse U.S. tax consequences for shedding U.S. citizenship. The first “expatriation tax” law was not adopted until 1966 as part of the The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of U.S. Tax Expatriation Law (Posted on April 6, 2014)

The highest U.S. federal income tax rate in 1927 was 25%. See, Personal Exemptions and Individual Income Tax Rates, 1913-2002. There was no Social Security tax at that time, as the Social Security programs were enacted in the Social Security Act of 1935.

Today’s highest marginal income tax rate is 39.6%, and the combined employer/employee portion of federal social security and medicare tax is 15.3%.

?????????????????Please clickhere to view the above in Chinese.?

Famous Former Citizens – Supreme Court Justice of Israel

Prof. Daphne Barak-Erez was born in the U.S. and hence became a U.S. citizen by virtue of her birth in the United States pursuant to the 14th Amendment (Section 1) of the U.S. Constitution. She was appointed in 2012 to the Supreme Court in Israel. The Tel Aviv University website provides a summary of her impressive CV as follows:

Prof. Daphne Barak-Erez recently left the Faculty of Law after being appointed to the Supreme Court of Israel. She was the Stewart and Judy Colton professor of law and held the chair of law and security.

She is a three time graduate of Tel-Aviv University: LL.B. (summa cum laude) 1988; LL.M. (summa cum laude) 1991, and J.S.D, 1993 (recipient of the Colton Fellowship). She was a visiting researcher at Harvard Law School, a visiting fellow at the Max-Planck Institute of Public Law, Heidelberg, an Honorary Research Fellow at University College London, a Visiting Researcher at the Swiss Institute of Comparative Law in Lausanne, a Visiting Researcher at the Jawarlal Nehru University in Delhi and a Visiting Fellow at the Schell Center at Yale Law School. . . . She was awarded several prizes, including the Rector’s Prize for Excellence in Teaching (three times), the Zeltner Prize, the Heshin Prize, the Woman of the City Award (by the City of Tel-Aviv) and the Women in Law Award (by the Israeli Bar). She is the author and editor of several books and of many articles in Israel, England, Canada and the United States.

?????????????????Please click here to view the above in Chinese.?

Did she “relinquish” or “renounce” U.S. citizenship? – Tina Turner –

There are important legal differences between “renouncing” and “relinquishing” U.S. citizenship. Specifically, the federal tax consequences that follow from one versus the other can be quite important. The principle point is the “timing” of when USC status terminates.

The federal tax reporting can be quite different for those who “relinquish” or “renounce” U.S. citizenship. For related background information see the following:

Tina Turner – Famous People Who Renounced U.S. Citizenship.

Proud Mary and the “keep on burning” lyrics is one of many mega hits of Tina Turner who was born a U.S. citizen in Tennessee.

Her fame spans multiple decades that continues today.

According to The Washington Post, she became a naturalized Swiss citizen in April 2013 and then “relinquished” (not renounced) her U.S. citizenship in 2013 (and is married to a German citizen):

revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card? Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute. from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

expatriate” and not even know it (oops)?! It can get tricky quickly. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

expatriate” and not even know it (oops)?! It can get tricky quickly. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).