Month: September 2015

Part I: New TIGTA Report to Congress (Sept 30) Has International Emphasis on Collecting Taxes Owed by “International Taxpayers”: Treasury Inspector General for Tax Administration (TIGTA)

TIGTA’s Semiannual Reports – Today’s Report with International Considerations – Part I

The Internal Revenue Service and U.S. Department of Justice (Tax Division) are the “soldiers” on the ground used to enforce U.S. federal tax law. They interpret the law, in no small part based upon the expertise and input of the myriad of experts in the U.S. Treasury, IRS and DOJ.

However, there are outside forces which oftentimes seem to have an “over-sized” influence on how, when and what priorities are identified in the IRS and DOJ. One of those powers of course is the Administration which makes up the Treasury Department and the very Department of Justice. The green book proposals of the Treasury and different policy proposals are an example. The other organization, within the Executive Branch is the Treasury Inspector General for Tax Administration (TIGTA).

TIGTA is the sort of “watch dog” over the IRS that independently reviews the work undertaken and often times questions that work and the IRS’ efforts. Per its own website it describes itself as:

The Treasury Inspector General for Tax Administration (TIGTA) was established in January 1999 in accordance with the Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) to provide independent oversight of Internal Revenue Service (IRS) activities. As mandated by RRA 98, TIGTA assumed most of the responsibilities of the IRS’ former Inspection Service.

TIGTA is separate and apart from the Taxpayer Advocate Service (“TAS”). See, excerpts of TAS reports here.

Another important influence is the Congress. See a prior post from September 2014 on this topic: How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

Tax Expatriation: The Numbers Affected Are Far Greater for Lawful Permanent Residents vs. Citizens

The last post discusses a scenario where an individual can be forced into “tax expatriation” by a third-party; i.e., the government, if a criminal tax investigation were to be pursued successfully. See, Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

We can call this “forced expatriation”; when the government takes investigative action to deport a lawful permanent resident (“LPR); i.e., cause a forced tax expatriation where an individual files a false return, provides false information or otherwise submits a false document to the government.

Other posts have discussed the role of U.S. income tax treaties in accidental “expatriation” for lawful permanent residents. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?), posted April 29,. 2014 and The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C), posted March 9, 2014.

We can call this “inadvertent expatriation”; when the individual themselves who is a LPR inadvertently causes a tax expatriation by operation of law.

There are other data points and relevant government operations of importance to LPRs. For instance, see, Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?, posted April 11, 2015. See, More Inforation and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The point of this post is to highlight a point previously made:

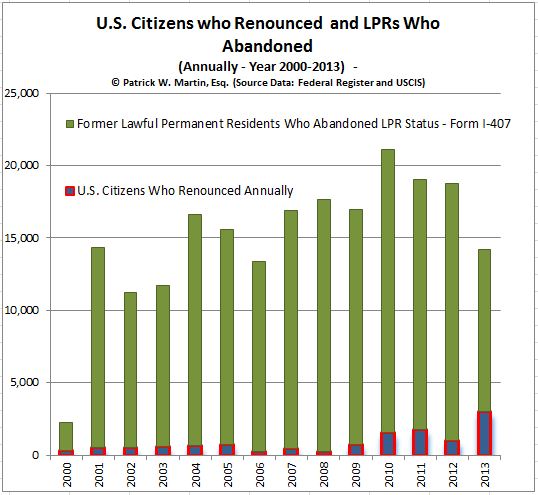

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

See, The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service, Posted on April 4, 2015

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency, Posted on April 3, 2015

The U.S. Customs and Immigration Service (USCIS) announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement,

Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

One sure way to “get expatriated” as a lawful permanent resident (even if that was not the plan) is to file a false federal tax return, statement or provide false information to the government. U.S. citizens cannot be deported for filing false tax returns, due to Constitutional rights.

Kawashima vs. Holder, (2012), is a story of a Japanese family that lived legally in the U.S. with lawful permanent residency status. According to the L.A. Times,

“Akio and Fukado Kawashima came to Southern California in 1984 as lawful Japanese immigrants determined to succeed in business. They operated popular sushi restaurants in Thousand Oaks and Tarzana and recently opened a new eatery in Encino.

But after they underreported their business income in 1991, they paid a hefty price. The Internal Revenue Service hit them with $245,000 in taxes and penalties. The couple pleaded guilty and paid in full. A decade later, the Immigration and Naturalization Service decided to deport them. . . “

The crucial mistake was the filing of a false return as defined under IRC Section 7206(1):

“(1) Declaration under penalties of perjury . . . Willfully makes and subscribes any return, statement, or other document . . . made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter . . . “

The Supreme Court ruled in this case that the false return that generated a revenue loss of at least US$10,000 for the government was properly classified by the government as an “aggravated felony.” In other words, the tax returns were materially false (which the taxpayers had plead to previously) and created an unpaid tax liability of at least US$10,000. The Supreme Court cited the immigration law (Title 8) and found such an offense to be a violation of Section 1227(a)(2)(A)(iii) as an:

“(iii) Aggravated felony

Any alien who is convicted of an aggravated felony at any time after admission is deportable.

The false tax return which created a tax liability of a relatively low threshold of US$10,000 therefore carries potentially sever consequences.

See a prior post that briefly discusses IRC Section 7206(1), see, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

While most USCs residing overseas will never be concerned about deportation (which should generally not be available to the government, due to constitutional rights of the U.S. citizen) LPRs filing tax returns will indeed want to consider carefully the implications of ” . . . any [and all tax and other] return[s], statement[s], or other document[s] . . . ” submitted to the federal government.

Also, prior posts discussed the law and risks associated with filing or sending false documents, information or returns to the Internal Revenue Service (“IRS”) –

See,Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer, posted July 19, 2014;

*Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?* posted March 6, 2014, Will the Justice Department and Criminal Investigation Division of the IRS Turn Their Sights on USCs or LPRs living Overseas? posted March 19, 2014,

The relevance of the Kawashima case to readers of this blog, is how a “long-term resident” may inadvertently find they will trigger the “mark-to-market” tax on their worldwide assets and later cause their U.S. beneficiaries to be subject to what is currently a 40% tax on the receipt of certain gifts and inheritances. See, prior posts on LPR status – Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?, posted August 19, 2014.

Some prior news coverage of the Kawashima v. Holder case here:

Legal immigrants face deportation for filing false tax return

The Supreme Court rules against a couple who pleaded guilty and paid in full, saying the crime was an ‘aggravated felony’ subject to automatic deportation. Tax lawyers say the decision is ominous.

Taxpayer’s Burden of Proving the Impossible (?) – Chapter 3 and Chapter 4 (FATCA) Withholding Taxes Paid by Third Parties

The IRS has issued a Notice (Notice 2015-10) this year announcing its intention to modify the Treasury Regulations regarding tax refunds. This new series of rules, Guidance on Refunds and Credits Under Chapter 3, Chapter 4, and Related Withholding Provisions will complicate the lives of taxpayers significantly.

Indeed, I have already seen and handled cases where the IRS asserts the taxpayer is not entitled to a tax refund, unless and until they can prove the third party who withheld and paid over the tax (issuing IRS Forms 1042 to all parties, including the IRS and the taxpayer) actually issued and deposited those payments.

These cases are like “proving a negative” since the withholding agent (typically a bank) who made and paid over the deposit, almost never makes single identifying payments for each amount of tax withheld. Typically, there are multiple taxpayers where the withholding tax was made and a single deposit made to the IRS. Those are indeed the specific rules set forth by the IRS. See, IRS Publication 515, withholding of tax on nonresidents

It gets even worse in Qualified Intermediary (“QI”) cases, where a large pool of withholding taxes are made. Typically, I have found the financial institution keeps detailed records of the payments and deposits (along with IRS Forms 1042s), but never has a payment specific to a particular taxpayer, as the deposit payments correspond to multiple taxpayers at once. Indeed, the IRS has acknowledged this treatment in this notice when it states:

Under the existing information reporting, withholding, and deposit procedures, a withholding agent does not indicate to which beneficial owner the deposit of tax relates, and such information is not reported on Form 1042 or 1042-S. Under the existing procedures, therefore, an amount deducted by the withholding agent with respect to a payment to the beneficial owner cannot be matched with an amount of tax deposited in the withholding agent’s Form 1042 account.

See page 5 of (Notice 2015-10).

There is a huge incentive for withholding agents to timely pay and deposit the taxes. There are harsh penalties levied against the withholding agent if they do not timely deposit and pay over the taxes, as follows:

Penalty rate. If the deposit is:

- 1 to 5 days late, the penalty is 2% of the underpayment,

- 6 to 15 days late, the penalty is 5%, or

- 16 or more days late, the penalty is 10%.

However, if the deposit is not made within 10 days after the IRS issues the first notice demanding payment, the penalty is 15%.

In short, the proposal in the form of modifying the regulations puts the burden on the nonresident taxpayer to prove the tax was withheld, before he or she will be entitled to a refund.

This is a new development in a series of developments where the IRS and Treasury simply issue regulations in areas of the law they do not seem to like. Further, it puts an unrealistic burden on nonresident taxpayers who are relying upon the third party withholding agent who makes the payment of taxes.

The long term affect of this rule, will be to force more taxpayers to file suits for refund in the Court of Federal Claims or U.S. District Court, which is necessarily complicated and costly.

More posts to come on this Notice 2015-10 and amendments to the Chapter 3 and Chapter 4 (FATCA) withholding tax regulations.

Finally – Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

The U.S. Treasury department has issued proposed regulations implementing the tax on “covered gifts” and “covered bequests.” There have been numerous posts about this tax that was first created in 2008 by new IRC Section 2801 (which has it’s own chapter in Title 26 – aka the Internal Revenue Code or “IRC”: Chapter 15, Gifts and Bequests from Expatriates). The regulations can be reviewed here – Guidance under Section 2801 Regarding the Imposition of Tax on Certain Gifts and Bequests from Covered Expatriates

See prior posts, When does “Covered Expatriate” Status -NOT- matter?, (May 2015); See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” (April 2014) and Proposal to U.S. Treasury and IRS: awaits Final Regulations on “Covered Gifts” and “Covered Bequests” (December 2014).

The tax is levied currently at 40% and can be a big surprise to U.S. beneficiaries who receive so-called “covered gifts” and “covered bequests.” The actual implementation of the tax and its enforcement was suspended until Treasury issued regulations. That day has now come and final regulations will follow shortly.

The proposed regulations create an ingenious mechanism by which assets that are received from foreign trusts (which make an election to be taxed as domestic trusts) cannot escape the 40% taxation. Specifically, there was concern expressed to me by Treasury officials drafting the regulations, when I had submitted a proposal to the U.S. Treasury on the subject in May of 2014. See, COVERED GIFTS & BEQUESTS: THE NEED FOR GUIDANCE (5+ YEARS OUT)

* * *

There was concern by the U.S. Treasury that U.S. persons could escape the tax when assets are received by foreign trusts which elect to be taxed as domestic trusts. In those cases, the statute imposes the tax liability on the trust and not the U.S. beneficiary. Hence, the concern expressed by some of the key drafters at U.S. Treasury of the regulations, was that a foreign trust would make the election and purposefully NOT pay the tax imposed by the statute, since the trustee would be outside the U.S. and largely outside the jurisdiction of the IRS.

The proposed regulations create a mechanism by which the trustee cannot slip away so easily, as they will NOT be treated as a domestic trust (versus a foreign trust) in such circumstances where the tax is not actually paid. In those cases, the U.S. beneficiary will be liable for the tax.

It also has some unique concepts that are not necessarily intuitive under the law. For instance, those individuals who are not U.S. citizens, yet live in the U.S. on a nearly full time basis, might still be able to avoid the application of the tax (at least in certain circumstances) if they are not “domiciled” in the U.S. The term “domicile” is a key estate and gift tax term of tax residency, that is not tied to the number of days an individual spend in the U.S. Rather, it is tied to the subjective intention of whether they expect to spend the rest of their lives in the U.S. See, Section 28.2801-2(b) of the proposed regulations which defines residents as those under “Chapter 11” and “Chapter 12”; which are the rules of “domicile” for transfer tax purposes. These are different from the rules of income tax residency found in IRC Section 7701.

The operative definition is found in (b)(1) of the Regulations: 26 CFR 20.0-1 – Introduction.:

“A person acquires a domicile in a place by living there, for even a brief period of time, with no definite present intention of later removing therefrom. Residence without the requisite intention to remain indefinitely will not suffice to constitute domicile, nor will intention to change domicile effect such a change unless accompanied by actual removal.”

Notice, there is no reference to the number of days physically spent in the U.S.

More to be discussed on the proposed regulations in later posts.

CORRECTION TO A PRIOR POST – How Many of the 5,211 Former U.S. Citizens (who Renounced in 2014 and 2015) are Still U.S. Taxpayers?

My goal is to provide useful information on U.S. federal tax law provisions for U.S. citizens who renounce. As this blog provides, it does not provide legal advice specific to any individual circumstances.

A prior post (How Many of the 5,211 Former U.S. Citizens (who Renounced in 2014 and 2015) are Still U.S. Taxpayers?) erroneously indicated that many of these individuals continue to be U.S. persons for federal income tax purposes.

This is not necessarily the case, depending upon when the U.S. citizenship terminated; i.e., when was the “expatriation date” as provided for in the statute. It is very possible that individuals who have renounced citizenship and did not certify under Section 877(a)(2)(C) are “covered expatriates” with all of the adverse tax consequences that befall that status (including to any future U.S. beneficiaries).

They will not necessarily continue to be “U.S. persons” for other purposes of Title 26.

I will run a series of posts over the next month or so that will discuss some of the vexing timing issues in the statute in this regard.