IRS

A “Resident” is a “Resident” is a “Resident” – or Not?

Who is a “resident”? What is a “resident”? This sounds like such a basic question. It is not so simple for tax purposes; nor for other provisions of the law.

There is the colloquial meaning of resident. For instance, if Mr. Smith says, “I have been a resident of Montana on my ranch for 30 years”; to what does he refer? What if Mr. Smith has a house in California (which he has owned for 15 years) and another ranch in Alberta, Canada that he has owned for 45 years. Is he also a “resident” of Canada and California?

What if he is not a U.S. citizen but holds a particular type of visa, such as lawful permanent residency (an immigrant visa)? What if he has a non-immigrant visa, such as an E-2 visa? What if he only spends 4 months a year on his ranch in Montana, of where is he a “resident”?

Is he a “resident” in some or all of these scenarios? Why is this important in the context of “U.S. expatriation taxation”?

There are three sources of federal law where it becomes very important, which will be discussed in later posts:

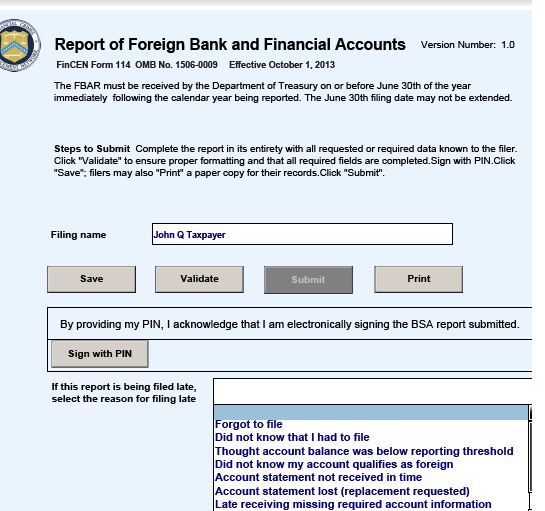

- Title 31 – which is the “bank secrecy” law that creates the “FBARs” – see a prior post, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

- Title 26 – federal tax law that has a myriad of definitions regarding “residents”; see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9.

- Title 8 – federal immigration law; see, Part II: Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

In addition, various states, such as California, Texas and Washington D.C. (actually not a state; but all places I happen to be licensed to practice law) have their own definitions of who are “residents” for income tax and other purposes.

Subsequent posts will discuss the importance of understanding who is a “resident” and the implications under these various laws.

Laymen regularly have an idea of where they are “resident” – but that idea is often very different from definitions of “resident” under federal Titles 31, 26 and 8 and state laws (e.g., Texas, D.C., Florida, California, New York, etc.).

Part I: New TIGTA Report to Congress (Sept 30) Has International Emphasis on Collecting Taxes Owed by “International Taxpayers”: Treasury Inspector General for Tax Administration (TIGTA)

TIGTA’s Semiannual Reports – Today’s Report with International Considerations – Part I

The Internal Revenue Service and U.S. Department of Justice (Tax Division) are the “soldiers” on the ground used to enforce U.S. federal tax law. They interpret the law, in no small part based upon the expertise and input of the myriad of experts in the U.S. Treasury, IRS and DOJ.

However, there are outside forces which oftentimes seem to have an “over-sized” influence on how, when and what priorities are identified in the IRS and DOJ. One of those powers of course is the Administration which makes up the Treasury Department and the very Department of Justice. The green book proposals of the Treasury and different policy proposals are an example. The other organization, within the Executive Branch is the Treasury Inspector General for Tax Administration (TIGTA).

TIGTA is the sort of “watch dog” over the IRS that independently reviews the work undertaken and often times questions that work and the IRS’ efforts. Per its own website it describes itself as:

The Treasury Inspector General for Tax Administration (TIGTA) was established in January 1999 in accordance with the Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) to provide independent oversight of Internal Revenue Service (IRS) activities. As mandated by RRA 98, TIGTA assumed most of the responsibilities of the IRS’ former Inspection Service.

TIGTA is separate and apart from the Taxpayer Advocate Service (“TAS”). See, excerpts of TAS reports here.

Another important influence is the Congress. See a prior post from September 2014 on this topic: How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior