International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

Why Are Foreign Banks Closing Accounts for Americans Abroad?

Is it hype, or is it real? Many U.S. citizens and lawful permanent residents (green-card holders) living overseas have heard that foreign banks are closing their accounts. Here is what actually shows up in practice, and why so many people are moving their money home.

Are foreign banks really closing the accounts of Americans living overseas?

It is hard to know with certainty how accurate these claims are. If it has happened to you, of course you will know it. In practice, account closings have turned up in places such as Hong Kong, London, Geneva, and Zurich. But they do not appear to be a widespread practice, at least not anecdotally.

What have news reports said about banks cutting off American expats?

Several published reports have raised the issue, including:

The Wall Street Journal, “Expats Left Frustrated as Banks Cut Services Abroad” (11 Sept 2014).

The Wall Street Journal opinion piece by Colleen Graffy, “How to Lose Friends, Citizens and Influence.”

Time Magazine, “Swiss Banks Tell American Expats to Empty Their Accounts.”

The Huffington Post (Aug 2014), “Expatriate Tax Sense or Broad-Brush Overreach: The U.S. Foreign Account Tax Compliance Act (FATCA).”

The New York Times (April 2013), “Overseas Finances Can Trip Up Americans Abroad.”

The Association of Americans Resident Overseas, on Americans abroad being denied access to banking and investment opportunities.

American Citizens Abroad, which compiles various news accounts of accounts being closed.

Does the size of the account change how a foreign bank responds?

It appears to. For individuals with large investment accounts, for example greater than US$1 million, banks seem to accommodate them, or at least require them to move their assets to a U.S. affiliate or branch. Those with smaller accounts, for example less than US$100,000, appear to see a broader brush stroke of closures.

If foreign banks aren’t the main driver, who is closing these accounts?

Much of it is the individual’s own decision, not the bank’s. What has been widespread in practice is a plan by individuals to close foreign financial accounts and relocate the assets to a U.S. financial institution. This includes U.S. citizens and lawful permanent residents (green-card holders) living outside the U.S. The move is the individual’s choice, not the financial institution’s.

Why are U.S. citizens and green-card holders abroad choosing to close their foreign accounts?

The reason is generally not FATCA (the Foreign Account Tax Compliance Act) itself, but a desire to reduce the compliance costs of filing and reporting on foreign accounts. FATCA seeks to co-opt foreign banks as long-arm enforcement of U.S. tax law. Even so, the driver people cite is cost, not the statute. Multiple tiers of reporting of foreign assets is now required. It can cost a small fortune to retain a good international tax adviser who is aware of these reporting requirements.

What reporting makes holding foreign accounts so expensive?

Two main layers apply to U.S. citizens and lawful permanent residents living outside the U.S.: the FBAR (the Foreign Bank Account Report) and IRS Form 8938 (Specified Foreign Financial Assets). For those with significant assets and numerous accounts, the professional fees and costs of reporting these accounts accurately can become exorbitant. That is especially true when the risk of potentially devastating civil penalties is weighed into the mix.

What penalties are people worried about?

The IRS now regularly threatens large, multiple-year 50% willfulness penalties for those who did not file an FBAR. This risk is more than just perceived. The Zwerner FBAR case is one example, and it has been described as probably a Pyrrhic victory for the government for U.S. citizens and lawful permanent residents living outside the U.S. The combination of cost, compliance burden, and penalty risk is what drives many people to act.

Is it actually illegal for a U.S. person to hold a foreign bank account?

No. There is no legal restriction for a U.S. citizen to hold foreign accounts. A U.S. citizen or lawful permanent resident residing outside the U.S. will generally find it easier, from a lifestyle and personal financial management perspective, to have an account in their home country. The irony is that the practical effect pushes in the opposite direction.

Where are these assets ending up?

The practical effect, anecdotally, is that U.S. financial institutions are receiving these assets and investments. As individuals close foreign accounts to cut compliance costs and penalty risk, the money flows back into the U.S. rather than staying in their home country abroad.

The FBAR (the Foreign Bank Account Report) comes from a different law than the federal income tax. The income tax sits in Title 26 of the U.S. Code. The FBAR comes from the Bank Secrecy Act, which is Title 31. These two laws are very different, with very different obligations and rights. One of the important differences is the time frame in which the government can assess penalties for not complying.

Who has to file an FBAR?

By its expansive terms, which some would call extraterritorial, the FBAR law applies to U.S. citizens residing outside the U.S. It also applies to most LPRs (lawful permanent residents, or green card holders) residing outside the U.S. Many of these people are unaware the rules reach them.

What is a statute of limitations for these penalties?

A statute of limitations is the time frame in which the government has to assess penalties for not complying with the law. For foreign accounts, these time periods are not the same under Title 31 (the Bank Secrecy Act) as they are under Title 26 (the income tax law). The gap between the two is what makes this area confusing.

Is there a time limit for the IRS to assess income tax if a return was never filed?

No. When a U.S. citizen or LPR residing overseas fails to file an income tax return, the time period for the IRS to make tax assessments never lapses. There is effectively no statute of limitations against the IRS in that situation. The clock to assess does not start until a return is filed.

How long does the government have to assess civil FBAR penalties?

Title 31, the Bank Secrecy Act, is different. It does have a time period that runs against the U.S. federal government, even if the FBAR was never filed. For civil assessments of penalties, that time period is 6 years.

Can someone be criminally liable for not filing an FBAR?

Yes. A U.S. citizen or LPR living overseas could become criminally liable for willfully not filing the FBAR form. Criminal liability carries different legal consequences than a civil penalty. The key word is willfully, which separates a criminal matter from a civil one.

How is the FBAR filed now?

All FBARs must now be filed electronically. The form is not filed with the IRS. It is filed with FinCEN (the Financial Crimes Enforcement Network), on Form 114, Report of Foreign Bank and Financial Accounts, through the BSA E-Filing System website. The electronic Form 114 supersedes TD F 90-22.1, the paper FBAR form used in prior years.

Can the U.S. collect FBAR penalties in the filer’s home country?

Not always. The laws of many countries outside the U.S. often conclude that enforcing these FBAR penalties against a U.S. citizen, inside that person’s home country, violates the laws of that country. Canada is one example. Calgary based tax attorney Roy Berg has written on the question of whether the IRS can collect FBAR penalties under the Canada-US Treaty.

Is there a statute of limitations for criminal FBAR charges?

Yes, there are also statutes of limitations for criminal charges the government brings for FBAR violations. The law gets much more complex here, especially when the taxpayer is residing outside the U.S. In that situation, the time period can be tolled or suspended in favor of the government, which extends the window to bring charges. Jack Townsend has written on the statutes of limitations for FBAR noncompliance related to tax noncompliance.

What do “willful” and “non-willful” mean for US citizens and green-card holders living abroad who have not filed?

“Willful” and “non-willful” describe how a failure to file is characterized. For any US citizen (USC) or lawful permanent resident (LPR, a green-card holder) living outside the US who has not been filing US income tax returns or FBARs (the Foreign Bank Account Report), the willfulness question is one of the most important to understand. The IRS “streamlined” procedure requires a taxpayer to certify that the conduct was non-willful. The distinction shapes the options a person has for correcting past filings.

Why does the willful or non-willful question matter for a US citizen or green-card holder overseas?

The willful or non-willful question matters because it shapes what steps a US citizen or green-card holder living abroad needs to take about filing US income tax returns. The answer affects how a person who has not been filing may approach cleaning up past returns and FBAR filings.

Can a green-card holder living in a tax-treaty country clean up past US tax filings?

A green-card holder who lives predominantly in a country that has a US income tax treaty may be in the best position to clean up past US tax filings and return positions. The US has 68 income tax treaties. Under the “tie-breaker provisions” of such a treaty, typically Article 4, the person’s facts may allow them to file as a non-resident, and those filings may apply to several prior years.

When is a green-card holder no longer treated as a lawful permanent resident for US tax purposes?

A green-card holder is no longer treated as a lawful permanent resident for US federal tax purposes under IRC Section 7701(b)(6) when three tests are met:

the individual is treated as a resident of a foreign country under the provisions of a tax treaty;

the individual does not waive the benefits of the treaty; and

the individual notifies the Secretary of the commencement of such treatment.

When a green-card holder notifies the IRS that he or she is not a US resident under an applicable income tax treaty and files the treaty position accordingly, the issue of “expatriation” becomes front and center.

Can a green card be given up for tax purposes just by moving outside the US?

In some cases, yes. Since the 2008 tax law changes, lawful permanent resident status can be abandoned for tax purposes by merely leaving and moving outside the US.

Does giving up long-term green-card status trigger the US exit tax?

Giving up green-card status can trigger the US “exit tax” for a green-card holder treated as a “long-term resident.” A green-card holder who has held that status for 8 years or more is generally treated as a long-term resident and may be subject to the exit tax of IRC Sections 877 and 877A. A separate tax may also apply to future US persons who receive gifts or inheritances from such a former green-card holder under Section 2801.

What does the IRS streamlined procedure require taxpayers to certify?

The IRS “streamlined” procedure, announced on June 18, 2014, has specific requirements that obligate the taxpayer to certify “non-willful” behavior. That certification is made under penalty of perjury. Where a green-card holder’s past failure to file US income tax returns was not non-willful, difficult legal questions arise about the consequences.

Understanding Your FBAR Obligations: A Guide for U.S. Citizens and Residents Abroad

If you are a U.S. citizen or a Green Card holder living overseas, you may have heard of the “FBAR.” While it sounds like a complex tax term, it is actually a financial reporting requirement that follows you no matter where you live in the world.

Here is a breakdown of what you need to know to stay compliant, explained in plain English but with a focus on the legal details.

The FBAR stands for the Report of Foreign Bank and Financial Accounts. Its official name is FinCEN Form 114.

Legally, this is not an income tax requirement. It is a mandatory report required under Title 31, Section 5314 of the U.S. Code. Because it falls under “Money and Finance” laws rather than the Internal Revenue Code, you do not file it with the IRS. Instead, you file it with FinCEN (the Financial Crimes Enforcement Network), a separate branch of the Treasury Department.

Who has to file?

The requirement applies to all U.S. Citizens (USCs) and Lawful Permanent Residents (LPRs), regardless of their physical location.

Global Reach: If you are a U.S. citizen living in France, you are required to report your French bank accounts, as well as any other accounts you might hold in places like London or Geneva.

Green Card Holders: Similarly, a Green Card holder living in Sao Paulo, Brazil, must report their Brazilian accounts and any accounts held in other countries, such as Uruguay.

Defining “Resident”: Interestingly, the law for FBARs uses the tax code’s definition (Internal Revenue Code Section 7701(b)) to determine who counts as a “resident,” even though the FBAR itself is not a tax form.

Note: While many resources mention a $10,000 threshold for filing, this specific dollar amount is not mentioned in the legal excerpts provided here; you should verify current filing thresholds independently.

What accounts are covered?

The law is broad and covers bank and financial accounts located outside of the United States. This includes accounts in your country of residence and any other foreign country. Currently, all FBARs must be submitted using the electronic Form 114, which replaced the old paper form known as TD F 90-22.1.

Is the FBAR the same as Form 8938?

No, though they are often confused because they involve duplicate reporting.

FBAR (Form 114): A financial report filed with FinCEN under Title 31.

Form 8938: A tax information return filed directly with your IRS tax return under Title 26.

A major legal distinction lies in the statute of limitations. The FBAR has a time limit after which the government can no longer assess penalties, even if you never filed the form. In contrast, if you fail to file Form 8938, there is no time limit for the IRS to come back and assess income taxes and penalties for that year.

The reality of FBAR penalties

The penalties for failing to file an FBAR are often discussed as being severe, but the law provides some unique protections.

Penalties are Elective: The law states the Secretary of the Treasury “may” (not “shall”) impose a penalty. This means the government has the discretion to decide whether or not to penalize a violation; it is not mandatory.

Limited Collection Powers: Unlike a standard tax debt, the government cannot simply place a tax lien or levy on your property to collect an FBAR penalty. Instead, the government typically must sue you in a judicial court action to enforce the penalty.

Expiration Dates: Because there is a statute of limitations, the government’s window to act is limited. For example, if a U.S. citizen missed a filing for the year 2006, the time for the government to assess a penalty has already lapsed.

How to file

Gone are the days of mailing paper forms. All FBARs must now be filed electronically through the BSA E-Filing System website.

Staying compliant is obligatory, but understanding these nuances can help you navigate the process with more confidence. If you have accounts abroad, ensuring your electronic Form 114 is submitted correctly is the best way to avoid the complications of a potential government investigation.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

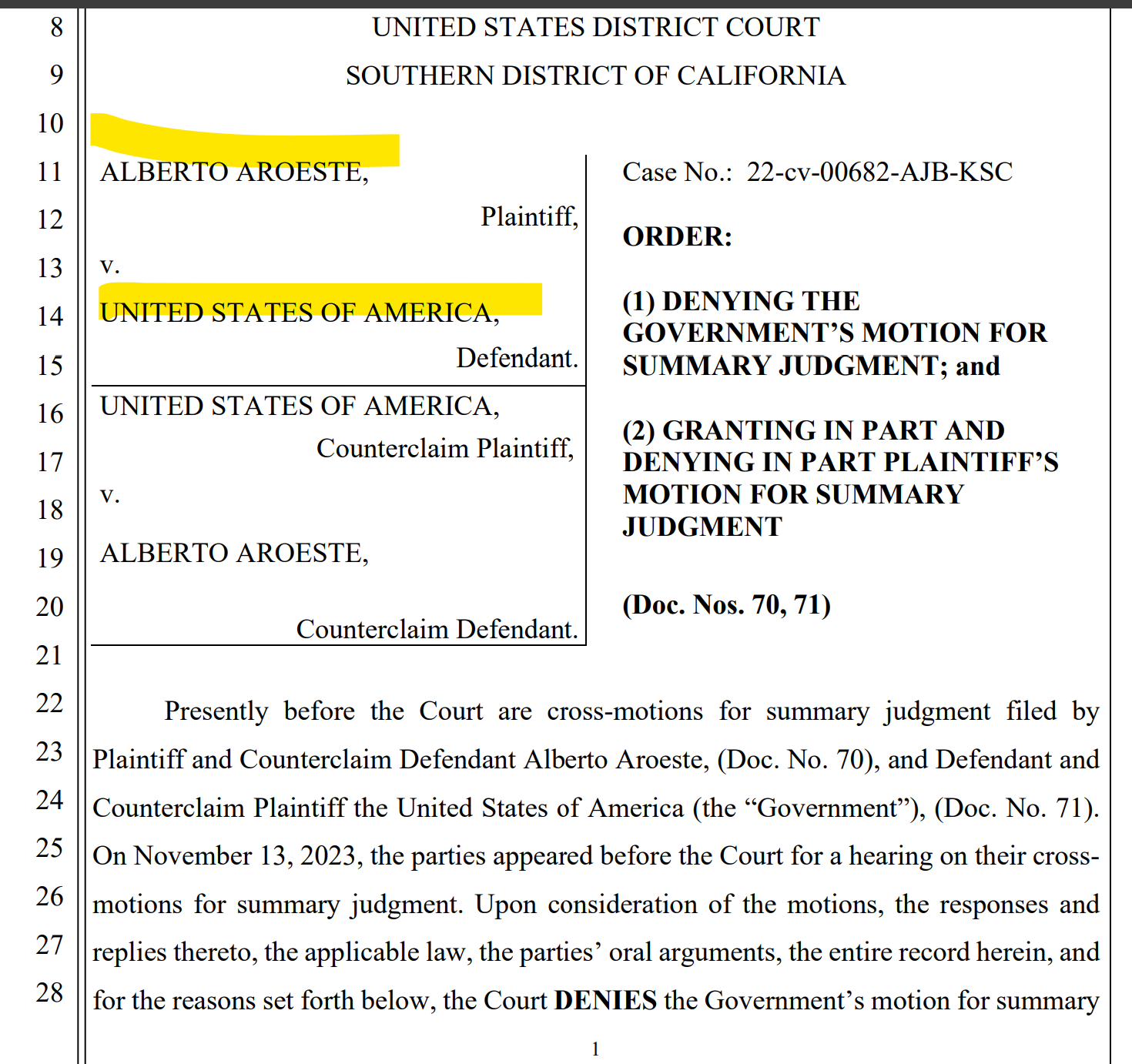

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

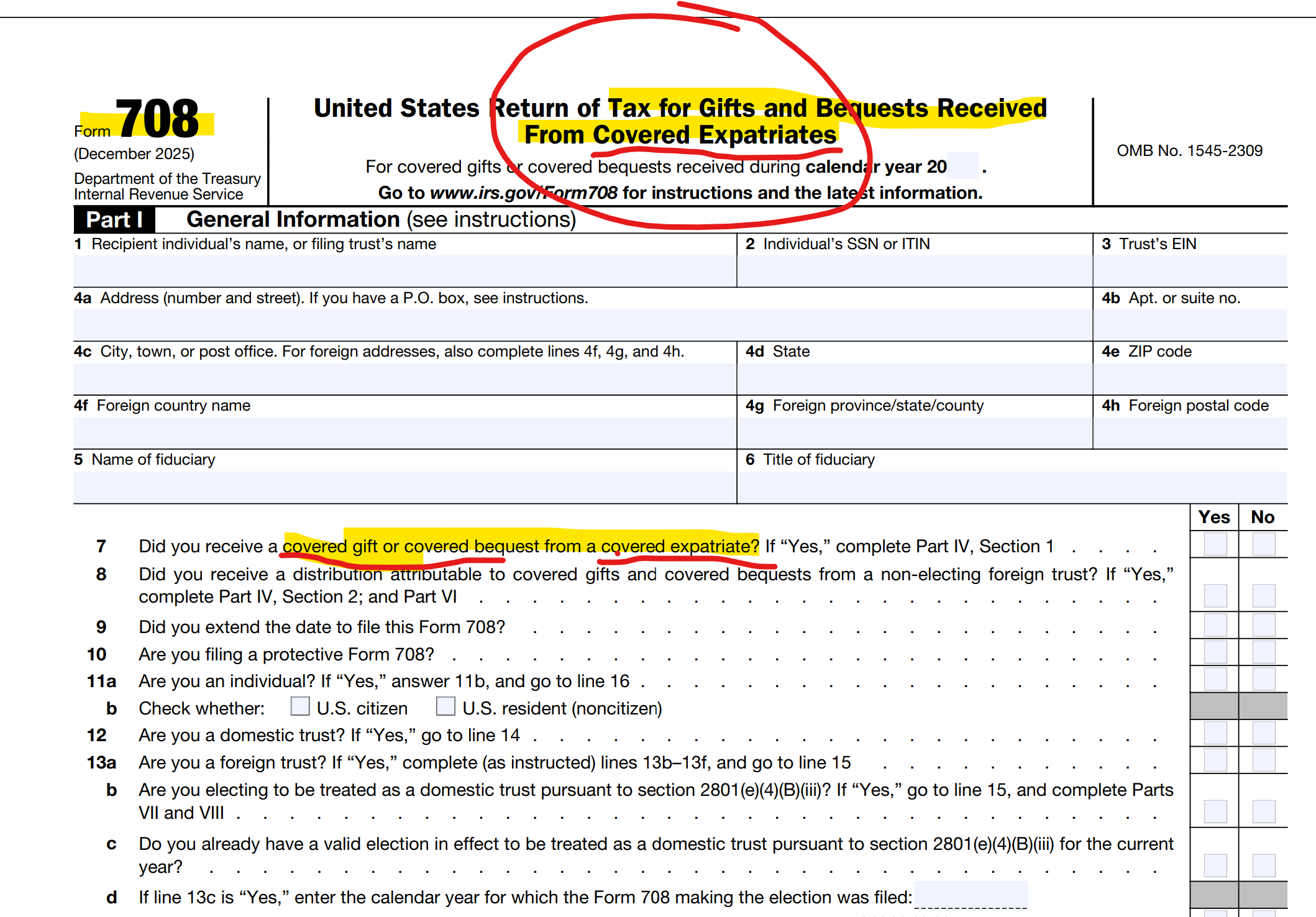

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

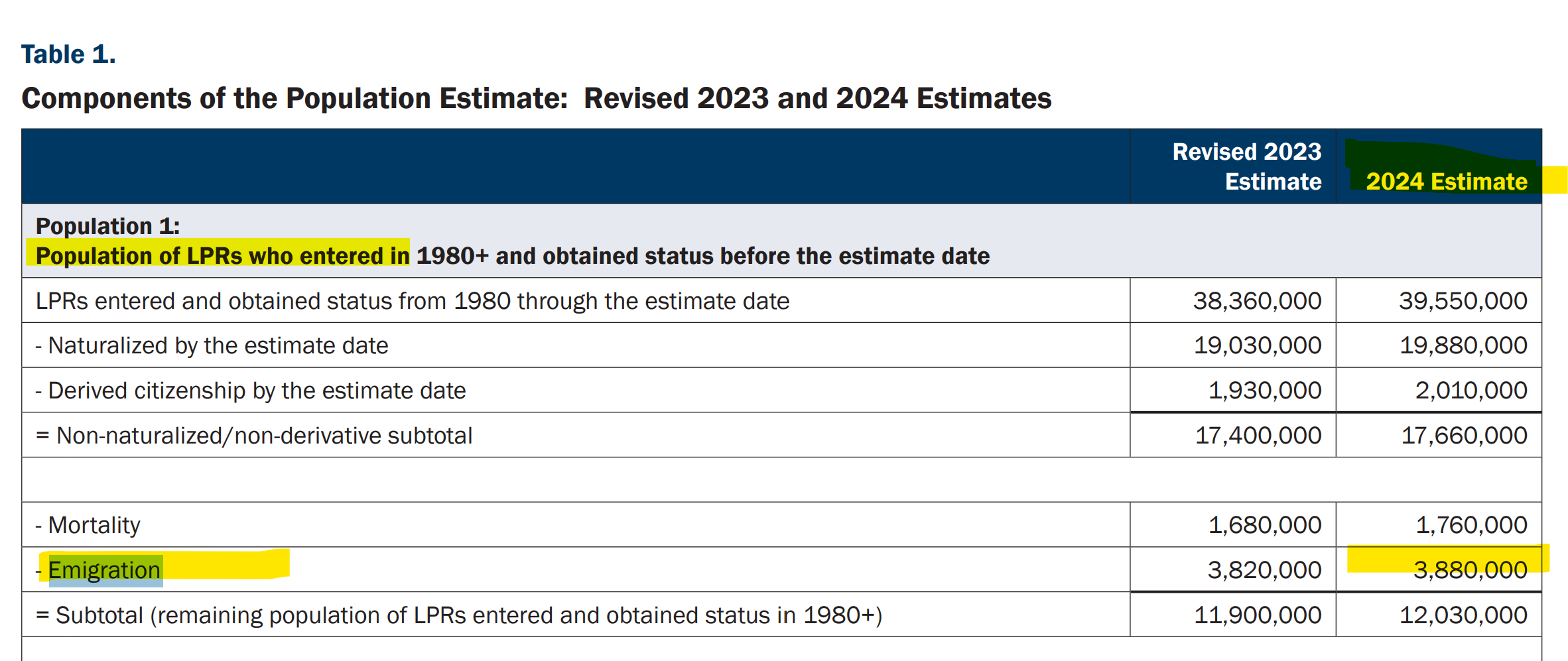

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Quaint?: U.S. Treasury 1998 Report: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues (Part I of Part II)

This is a classic report that now reads quaintly.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties inUnited States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

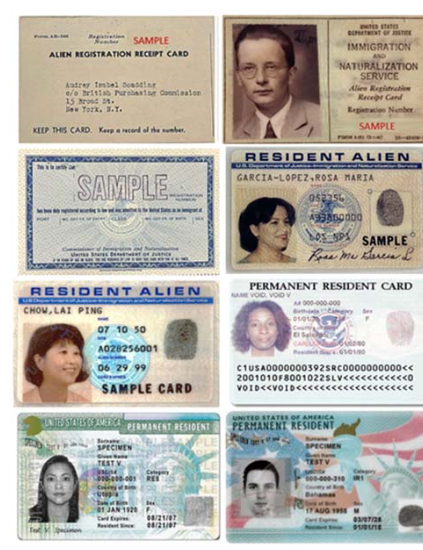

Immigration Forms, I-407; I-485, Application to Register Permanent Residence or Adjust Status & Tax Forms, 1040, 1040NR, 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114, etc. etc. (Part I of III)

The U.S. tax law is complex, including when an individual (i) becomes and (ii) ceases to be, a U.S. income tax resident (USITR). USITR is not a technical term used under the tax law. The U.S. tax and information reporting requirements are very different depending the status of an individual. Anyone who is not a United States citizen, is either a –

“Resident alien“, or a

“Nonresident alien” as the tax law defines both of these categories.

You can’t be both.

“Resident aliens” are generally also “United States persons” (both technical terms in the federal tax law).

“Non-resident aliens” as defined are necessarily not “United States persons.”

Being one versus the other has huge U.S. tax and reporting consequences.

An individual who is a “lawful permanent resident” as referenced in the tax law (Section 7701(b)(6)) cross-references the U.S. immigration law. The first requirement of that statutory tax rule in § 7701(b)(6)(A)) is that “(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws [such status not having changed]. . .[emphasis added]” This means the tax definition is dependent upon the immigration laws, which are found in Title 8, Immigration and Nationality Act. Importantly, the last part of that sentence (i.e., [such status not having changed] is a requirement in the immigration law (Title 8), but does not appear in the tax definition.

The term “lawful permanent resident” cannot be found in Title 8 as a noun or object (i.e., the individual). Instead, the immigration law defines the status of a person in 8 U.S. Code § 1101(a) as follows:- “. . . (20) The term “lawfully admitted for permanent residence” means the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed.“

This analysis is fundamental to be able to determine whether an individual who holds a “green card” in their pocket even has the status of being “lawfully admitted for permanent residence. . . such status not having changed.” It’s a fundamental legal question under immigration law that must be answered first, to then be able to answer the tax question.

Each form an individual files or does not file (e.g., IRS tax form 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114; and immigration forms, e.g., I-485, I-407, etc.) can have a potential impact on the tax residency status of an individual.

The immigration law and when forms, such as Form I-485, Application to Register Permanent Residence or Adjust Status are submitted to the U.S. federal government can have an impact on this determination. The government can use it against the individual as they did unsuccessfully in Aroeste (see below – Pages 9 and 11 of 17); asserting that Mr. Aroeste waived the treaty by not submitting certain forms.

The entire case from the Federal District Court can be read here: Aroeste v. United States, 22-cv-00682-AJB-KSC (20 Nov. 2023):

The tax residency analysis for those who have kept their “green card” in their pocket, can be even more complex as was analyzed by the Court. There are additional provisions of the law that must be considered including old Treasury Regulations that pre-date many provisions of various U.S. income tax treaties.

For instance, each of the following federal tax statutory rules, which will be considered in more detail in later posts (II and III):

Additional posts will review the impact of these provisions in the law and how various immigration forms (including I-485 and I-407, Record of Abandonment of Lawful Permanent Resident Status) and tax forms (including 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858) and FinCEN form 114, can impact the determination of whether someone who has a “green card” in their pocket is or is not a United States person.

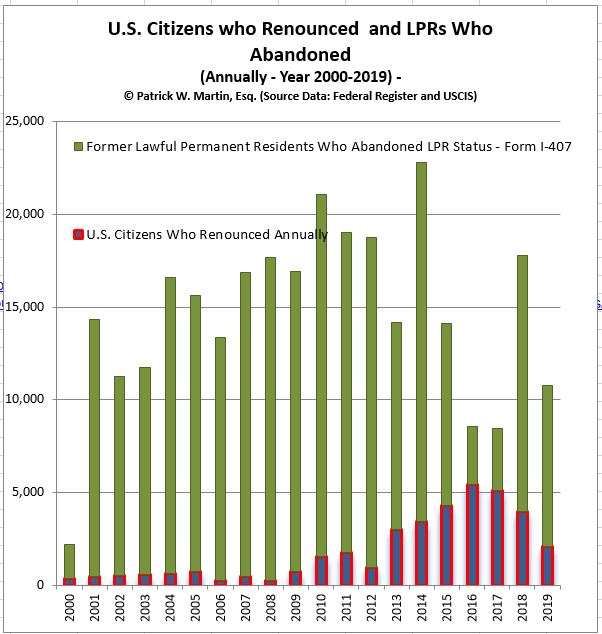

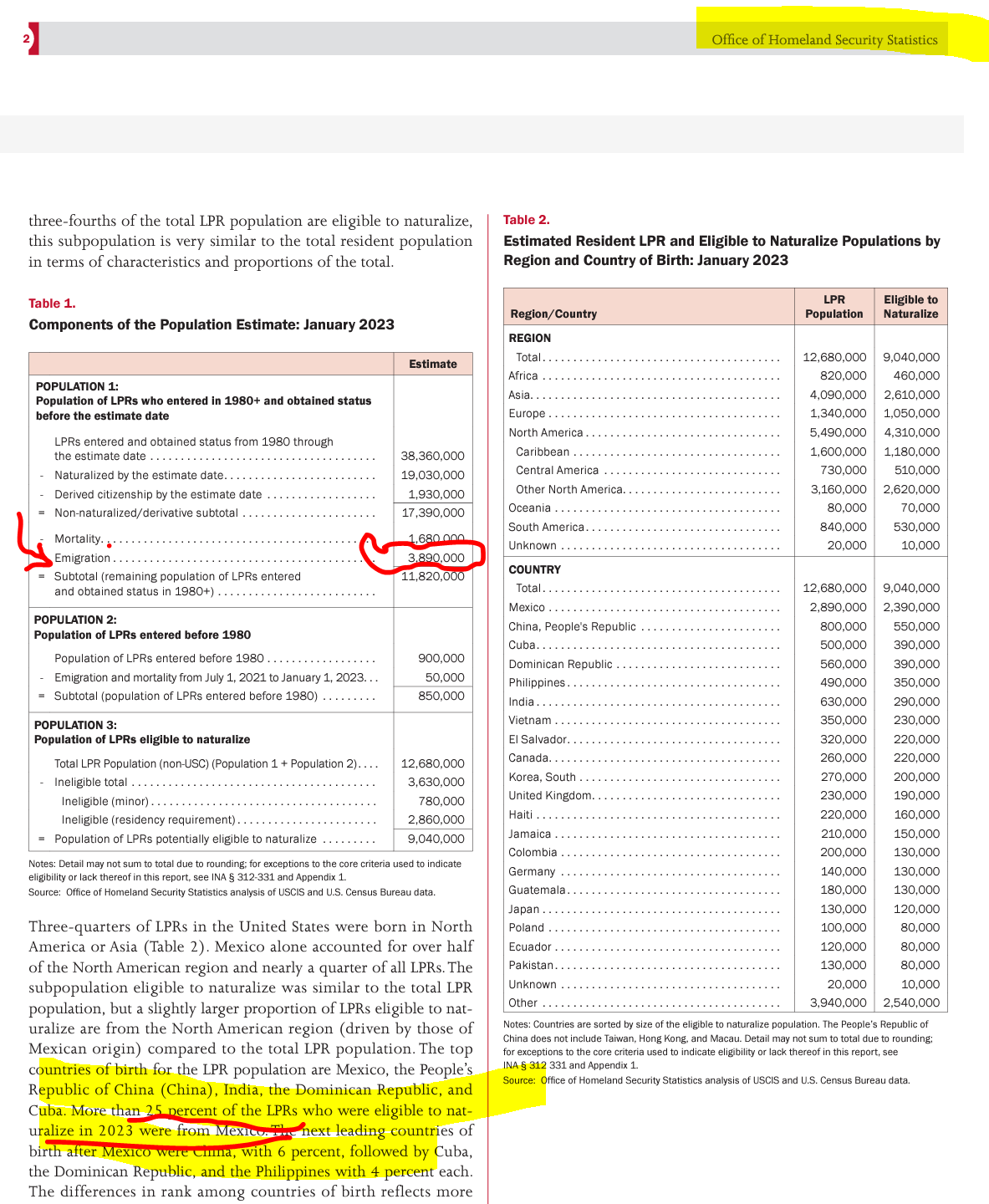

DHS Report: 3.89M Emigrated LPRs — Who Falls Under the Tax Treaty Escape Hatch?

Clear U.S. tax and legal relief now exists for a significant portion of the 3.89 million Lawful Permanent Residents (LPRs) who never formally abandoned their U.S. immigration status. This relief stems from two sources in the law:

(i) Tax treaty laws that apply to individuals residing in one of the 67 income tax treaty countries with the United States, recently including Chile.

(ii) Legal principles, recently confirmed by the Federal Court in Aroeste v. United States, that establish that individuals can apply tax treaty laws (when applicable) even if they missed certain filing deadlines set by the Internal Revenue Service. The Court termed this provision an “escape hatch,” allowing individuals, depending on specific circumstances, to be considered non-residents of the United States (not “United States persons”). This can be true under the relevant treaty, even if they never formally abandoned their LPR status.

The 2023 DHS report estimates that nearly 4 million individuals have emigrated from and left the United States and are now living somewhere around the world. Notably, Mexico constitutes the largest share at about 25% of the total LPR population who have left the United States.

The DHS report allows the reader to extrapolate that around 1 million individuals, similar to Mr. Aroeste, are living in Mexico and did not formally abandon their LPR status by filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

Aroeste v. United States is the third case I’ve litigated, examining whether individuals with a “green card” residing outside the United States in a tax treaty country are considered U.S. income tax residents. The previous two cases (involving Mexican and German citizens) didn’t progress to the oral argument stage; as the government conceded both before trial. See, IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

A FOIA response yielded surprising information; the government records indicate that only 46,364 Forms I-407 were filed from 2013 to 2015.

(Source: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ)

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

What can we glean from the DHS report and the LPR – I-407 information obtained through the FOIA response? There is a substantial gap in the millions; millions of individuals who have physically left the U.S. to reside elsewhere globally, compared to the relatively smaller number of tens of thousands who have officially filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

Conclusion

Importantly, now under the legal principles established in Aroeste v. United States, individuals residing in one of the 67 countries covered by an income tax treaty have specific legal relief from the worldwide reporting of income to the United States government.

Mérida – the Place to be in February (19th and 20th)

The implications of the Aroeste v United States – Order (Nov 2023) particularly for millions of taxpayers globally and “U.S.” taxpayers affected by pertinent tax treaty provisions, will be a focal point of discussion at the upcoming international tax conference in February.

The University of San Diego School of Law – Chamberlain International Tax Institute will take place on February 19th and 20th, 2024, at the International Convention Center in Mérida, Yucatán, México. You can register for the conference – HERE –

Among the courses offered, there will be a detailed examination of- Aroeste v. the United States: Limits on Government Authority Re: Tax Treaty Law ++– along with other international tax topics and sessions featuring much Moore:

United States Supreme Court – Tax Decisions & Moore

International Tax Reporting: New Reporting of International Partnerships – K-2s & K-3s

United States-based Cross-Border Real Estate Investments (Advanced)

U.S. Investor Visa Options and Limitations

California, Texas & Florida Probate Proceedings of Cross-Border Estates

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —