The President’s Proposal is NOT the Same as Current Law – Section 877A(g)(1)(B)

Some individuals are mistaken that the Obama proposal to exempt certain U.S. citizens from taxation (including the “mark to market” exit tax), is the same as the exception in IRC Section 877A(g)(1)(B).

It’s not. They are not the same, although they have some similar requirements (e.g., 5 years of certification of U.S. tax law compliance under penalty of perjury).

For a brief discussion on the President’s proposal, see –The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group

–

There are important differences. Most importantly, the I

RC Section 877A(g)(1)(B) exception requires the individual not only have been a dual citizen (of at least two or more countries) at birth, along with U.S. citizenship; but also continue to reside and be a tax resident of that country, i.e., the country of which they were also a citizen at the time of their birth. This tax residency/dual citizenship rule is necessarily required by I

RC Section 877A(g)(1)(B). If the person has moved to another country, they will not be eligible for this treatment and will be subject to the mark to market “exit tax” if they renounce their U.S. citizenship. Their U.S. heirs and beneficiaries will also be subject to the 40% (current tax rate) tax on “covered gifts” and “covered bequests.”

–

The President’s proposal (if it ever becomes law) will also apparently exempt all qualifying individuals from any type of U.S. taxation; other than tax that would apply to a “non-resident alien” (which would be no U.S. tax – if the individual had no U.S. source income). Not only would no “exit tax” apply, but so too would no U.S. income tax on their income from their country of residence or any other country outside the U.S. The President’s proposal would also exempt them from all U.S. tax filing requirements (other than the 5 years) and from FBAR filing requirements. See,

Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.–

–

What is the burden of proof for civil willful FBAR penalties? Government says – mere “preponderance of the evidence”?

A prior post took part of the government’s brief in the Zwerner case. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

A portion of the post and brief is set out below:

. . . another perplexing aspect of this case is that the government continues to persist in its argument that a mere preponderance of the evidence is the proof standard required. That will be left for another post and another discussion.

Here is that other post.

The reason this issue is so important for U.S. citizens and lawful permanent residents (LPRs) residing outside the U.S., is that few have historically filed FBARs. Few may have had little knowledge or understanding of what is an FBAR in years past. For more background on FBARs and how the government has assessed penalties as of late, see, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

Also, see a prior post entitled – Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S

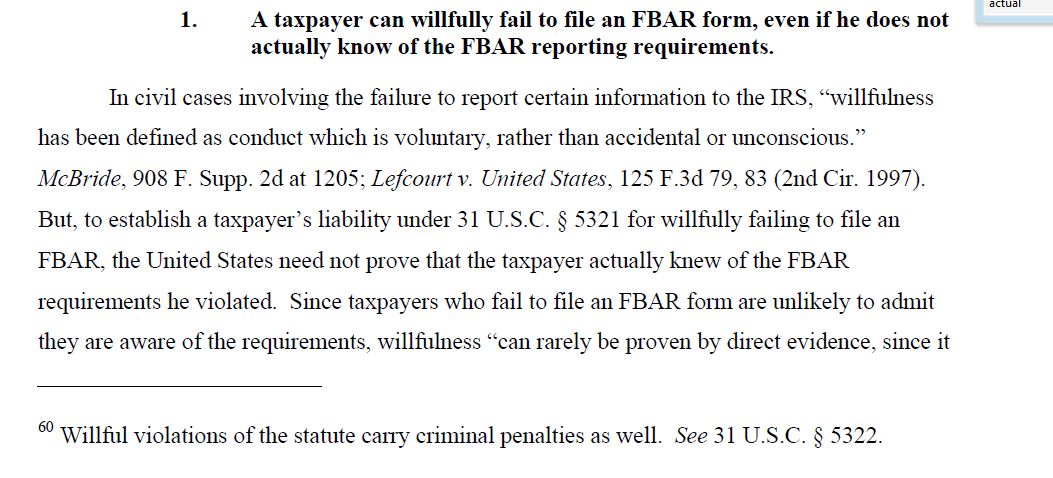

Back to the point at hand: can the government truly take the position that “. . . But to establish a taxpayer’s liability under 31 U.S.C. Section 5321 for willfully failing to file an FBAR, the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated. . . “?

This is a truly low bar and a low level of proof the government has, IF this is the law, particularly when the amounts of the penalties can exceed the value of the individual’s accounts in their country of residency. To date, no appeals court has ruled on the question.

The current state of the law, leaves taxpayers at a terrible disadvantage when the IRS assesses FBAR penalties which seem to have little correlation with their failure to file the form.

The position taken by the Tax Division, Department of Justice in the Zwerner case is also seems contrary to the Internal Revenue Service’s own Internal Revenue Manual, which provides as follows (with highlights in bold):

- The test for willfulness is whether there was a voluntary, intentional violation of a known legal duty.

- A finding of willfulness under the BSA must be supported by evidence of willfulness.

- The burden of establishing willfulness is on the Service.

- If it is determined that the violation was due to reasonable cause, the willfulness penalty should not be asserted.

- Willfulness is shown by the person’s knowledge of the reporting requirements and the person’s conscious choice not to comply with the requirements. In the FBAR situation, the only thing that a person need know is that he has a reporting requirement. If a person has that knowledge, the only intent needed to constitute a willful violation of the requirement is a conscious choice not to file the FBAR.

- Under the concept of “willful blindness” , willfulness may be attributed to a person who has made a conscious effort to avoid learning about the FBAR reporting and recordkeeping requirements. An example that might involve willful blindness would be a person who admits knowledge of and fails to answer a question concerning signature authority at foreign banks on Schedule B of his income tax return. This section of the return refers taxpayers to the instructions for Schedule B that provide further guidance on their responsibilities for reporting foreign bank accounts and discusses the duty to file Form 90-22.1. These resources indicate that the person could have learned of the filing and recordkeeping requirements quite easily. It is reasonable to assume that a person who has foreign bank accounts should read the information specified by the government in tax forms. The failure to follow-up on this knowledge and learn of the further reporting requirement as suggested on Schedule B may provide some evidence of willful blindness on the part of the person. For example, the failure to learn of the filing requirements coupled with other factors, such as the efforts taken to conceal the existence of the accounts and the amounts involved may lead to a conclusion that the violation was due to willful blindness. The mere fact that a person checked the wrong box, or no box, on a Schedule B is not sufficient, by itself, to establish that the FBAR violation was attributable to willful blindness.

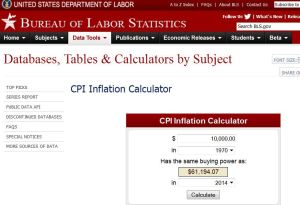

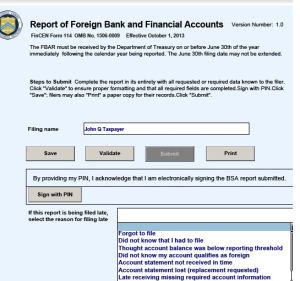

1970 Dollars: The Current Day US$10,000 FBAR Threshold Reporting Requirement (From Instructions Not Statute or Regulations)

The relevant statute that requires reporting of a so-called foreign bank account report (“FBAR”) is Section 5314 of Title 31 .  This is not a federal tax law provision from Title 26 (aka I.R.C. aka Internal Revenue Code.)

This is not a federal tax law provision from Title 26 (aka I.R.C. aka Internal Revenue Code.)

There have not been extensive revisions to this Section 5314 over the years and it remains largely as originally drafted and passed in the year 1970.

See, Currency and Foreign Transaction Reporting Act of 1970, P.L. No. 91-508, 84 Stat. 114 (1970).

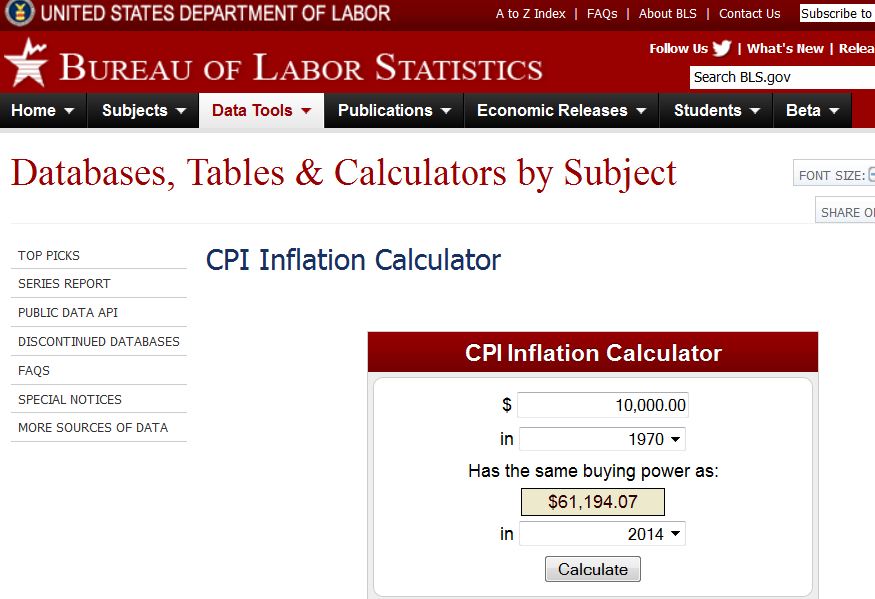

Curiously, the US$10,000 threshold amount is not reflected in the statutory language, nor in the regulations. Instead, this US$10,000 threshold is set forth in the instructions of the form. See page 4 of the FBAR electronic filing instructions.

This raises numerous legal questions that will be discussed in later posts.

The point of this post is twofold:

(1) the US$10,000 threshold amount is not part of the statutory or regulatory law; but rather is adopted in the instructions.

(2) US$10,000 in the year 1970 currently equals US$61,194 in inflation adjusted dollars (pursuant to the federal government’s CPI inflation calculator) which is a far different threshold for reporting

See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Most e-mailed Article from New York Times: “Why I’m Giving Up My Passport”

New York Times: “Why I’m Giving Up My Passport”

A relatively small percentage of the U.S. citizen population is aware of the complex requirements of the U.S. tax law and detailed financial reporting that is imposed under current law against individuals who reside outside the U.S. These same laws apply to both those USCs who live in and outside of the U.S. See, for instance, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

The December 7th Op-Ed article in the New York Times by Jonathan Tepper is now the most e-mailed of all NYTimes articles, as of today, which indicates the general public may now start to better understand the scope of U.S. tax and account reporting laws that are unique in the world.

He does summarize well, how the law works in practice:

The United States is an outlier: Its extraterritorial tax laws apply to American citizens and companies no matter where they are. We are the only country (except, arguably, Eritrea) that taxes all of its citizens on worldwide income rather than where the income is earned. Expatriate Americans have to pay taxes once, wherever they live, and then file again in the United States.

The I.R.S. doesn’t tax the first $97,600 of foreign earnings, and usually doesn’t double-tax the same income. So most expatriates owe no money to the I.R.S. each year — and yet many of us have to pay thousands of dollars to accountants because the rules are so hard to follow.

The extraterritorial reach of the income tax dates from the Civil War, . . .

These legal requirements also impose detailed reporting on all financial accounts in the country of residence that meet a modest threshold of US$10,000 at any time during the year. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

One of the consequences of the U.S. law, is that the Department of Justice argues (and has done so successfully at two different trial courts) that a USC does not need to actually know of the requirements of the FBAR law to still be liable for a civil willfulness penalty that can represent more than 300% of the value of all financial accounts of the individual. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

Many legal analysts would like to think Zwerner is just an outlier result that will not happen to most USCs residing outside the U.S. At the same time, most legal experts never thought the facts of the case in Zwerner would compel the government to assess what represented more than 200% of his foreign accounts as a civil penalty (i.e., a penalty of US$3.6M on an account of $1.69M).

The information reporting requirements are extensive and the government has argued the individual does not need to have actual knowledge of the law. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

In the government brief, they argue “ . . . the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated . . . ”

This puts a very low burden on the government when they pursue penalties that represent multiples of the amounts any individual has in their accounts.

Ironically, the facts of Boris Johnson, the mayor of London would indicate he has easily violated such laws (assuming he does not file his annual FBARs); by his statement that he will not pay the tax owing under U.S. federal tax laws. Surely, the U.S. government will be able to pursue him under the “willful blindness” theory they are using against other U.S. citizens who did not file FBARs. See, According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

For those practitioners who are handling cases before the IRS and Department of Justice on a regular basis, we understand well how the threat of ominous FBAR penalties can be bandied about against individuals to try to get them to settle on terms favorable to the government. See Mr. Zwerner, who indeed paid more than 100% of his entire foreign account (some US$1.69M) in settlement of his case.

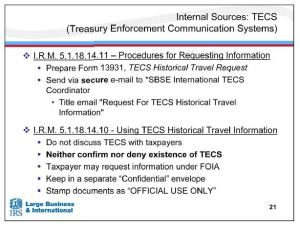

“Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –

There have been a series of previous posts that discussed the IRS and other government agencies ability to track taxpayers and their assets outside the U.S.

See for instance, the following posts: Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

and Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

Interestingly, the release of IRS internal training manuals and materials (which were obtained through a Freedom of Information Act – FOIA – request) and includes the Power Point slide in this post, describes the TECs database and how it can be used by IRS agents regarding foreign assets and individuals as follows:

The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. TECS contains historical travel information such as records of commercial airline flights, border crossings, and specific dates that individuals have traveled to and from the United States.

All this information could provide you with potential leads to pursue.

For example, the discovery of where the taxpayer may hold assets or accounts or where the taxpayer conducts business. It may also assist in determining taxpayer’s residency and the credibility of taxpayer testimony. TECS may have gaps in the information captured, caution is advised. For example, it might contain incomplete information about border crossings, private plane and private boat information. It does not contain enough stand alone data to determine residency. It should be used together with other sources of information.

In addition, the IRS training materials demonstrates the secrecy of the TECs database and what steps the IRS tells their agents to take regarding the TECs database. The following excerpt directly from the IRS “Matrix Application Training International Individual Compliance: Basic Structures Part II: Pre-Audit, Investigative Techniques & Statutes”

• IRM 5.1.18.14.10 – Covers using TECS Historical Travel Information

First and foremost, do not discuss the existence of TECS with the taxpayers. We must neither confirm nor deny the existence of TECS data.

USCs and LPRs Who Are Having Their Non-U.S. Accounts Closed: Is it hype or is it real?

Is it hype or is it real?

It’s difficult to know with certainty how accurate are the various claims that U.S. citizens overseas are having their accounts closed by foreign financial institutions. If it has happened to you, of course you will know it. See for instance the following reports, just to name a few:

Wall Street Journal: Expats Left Frustrated as Banks Cut Services Abroad Americans Overseas Struggle With Implications of Crackdown on Money Laundering and Tax Evasion (11 Sept 2014)

Wall Street Journal – Opinion (Colleen Graffy): How to Lose Friends, Citizens and Influence; The U.S. Foreign Account Tax Compliance Act seeks to co-opt foreign banks as long-arm enforcement

Association of Americans Resident Overseas: Americans Abroad are Denied Access to Banking and Investment Opportunities

Time Magazine: Swiss Banks Tell American Expats to Empty Their Accounts

The Huffington Post (Aug 2014) – Expatriate Tax Sense or Broad-Brush Overreach: The U.S. Foreign Account Tax Compliance Act (FATCA)

The New York Times (April 2013) Overseas Finances Can Trip Up Americans Abroad

and

American Citizens Abroad which compiles various news accounts of accounts being closed.

Anecdotally, I have certainly seen it in my practice, in places such as Hong Kong, London, Geneva and Zurich, but I can’t say I have seen it as a widespread practice. Indeed, for those individuals with large investment accounts (e.g., greater than US$1M, the banks seem to accommodate, or at least require them to move their assets to their U.S. affiliate or branch). I suspect those with smaller accounts of less than US$100,000, are seeing a broader brush stroke closing these accounts.

For good practical advice about maintaining or opening foreign accounts, I recommend you read:

**

I can say that what I have seen in practice is a widespread plan by individuals to close foreign financial accounts and relocate the assets to a U.S. financial institution. This is not the decision of the financial institution, but rather the individual. The reason is not FATCA, per se, but a desire to reduce the compliance costs of filing and reporting on these foreign accounts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Multiple tiers of reporting of foreign assets is now required and it can cost a small fortune to have a good international tax adviser who is aware of these reporting requirements. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938 [Specified Foreign Financial Assets]

For those with significant assets and numerous accounts, the professional fees and costs of reporting accurately these accounts can become exorbitant (especially when the risks of potentially devastating civil penalties are weighed into the mix). See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

At the end of the day, the practical affect I have seen (anecdotally) is a widespread desire to close foreign accounts and move them to the U.S.; not because of FATCA, but because of the costs and compliance and risk (more than just perceived – considering the IRS now regularly threatens large multiple year 50% willfulness penalties for those who did not file an FBAR) of being penalized by the IRS.

I find this ironic, since there is no legal restriction for a USC to hold foreign accounts and indeed a USC or LPR residing outside the U.S., will generally find it easier from a lifestyle and personal financial management perspective to have an account in their home country. The affect, however, is that U.S. financial institutions are receiving these assets and investments.

I will post a survey this week to ask individuals if they have had their non-U.S. bank accounts closed.

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

Probably the most misunderstood concept in the U.S. tax expatriation law provisions is Section 877(a)(2)(C) for several reasons.

1. People of modest means with modest to little income and little to no assets can fall into this category.

2. Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45

3. Lawful permanent residents (“LPRs”) can inadvertently fall into this category without doing anything, other than living principally in a country outside the U.S., which has a U.S. income tax treaty. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9. At the end of this post is a list of the countries with U.S. income tax treaties.

4. Few individuals understand exactly what must be included and reported in IRS Form 8854 to be able to satisfy the certification requirement above. For more details, see What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

The relevant provisions of Section 877(a)(2)(C) are highlighted below:

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Failure to certify truthfully about compliance with U.S. tax law for 5 years, as set forth above in the statute, means the individual necessarily will be a “covered expatriate.” Does this mean that if a U.S. citizen who renounces citizenship or a LPR who abandons their green card, will necessarily be a “covered expatriate” if they fail to follow IRS Notice 2009-45 “Guidance for Expatriates Under Section 877A”?

What steps will the IRS take if someone intentionally does not comply with the certification requirement? Will they become a target of a criminal investigation, and under what circumstances? What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

There are many pending and open questions not answered by current law, as the U.S. Treasury has yet to publish regulations under Section 877A, 877 or 2801.

APPENDIX – Countries with Income Tax Treaties with the United States