Month: August 2020

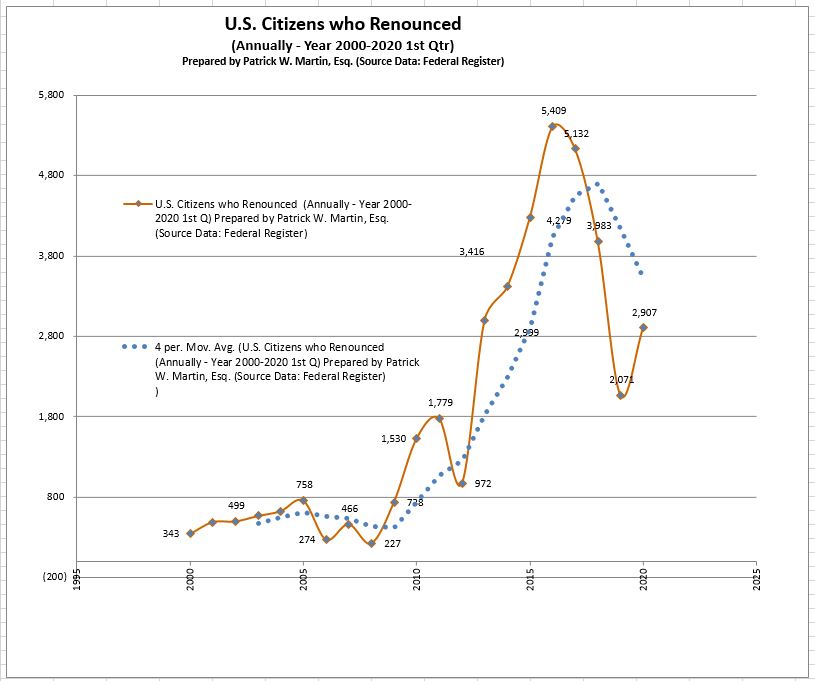

USC Renunciations: Ski Slope Upward – Ski Slope Downward

The federal tax law has a very transparent system of reporting and identifying former U.S. citizens who have renounced their citizenship. The data with the names of each individual are published quarterly on the federal government’s website as Required by Section 6039G. The complete set of lists including thousands of names of former U.S. citizens going back to the mid-1990s can be reviewed here. Quarterly Publications. Quarterly Publication of Individuals, Who Have Chosen to Expatriate.

See previous posts regarding the numbers of USCs who were renouncing at an increasingly rapid pace starting at just around and just before the year 2010. The FATCA transparency laws were passed in 2010 and so too were more international information reporting requirements (IRC 6038D) and strong enforcement efforts overseas by the IRS and DOJ Tax Division; which could be part of a cause and effect consequence? See, CHAPTER 4—TAXES TO ENFORCE REPORTING ON CERTAIN FOREIGN ACCOUNTS (§§ 1471 – 1474)

Why have U.S. Citizenship Renunciation Numbers Plateaued?

Posted on : The current renunciations and now steep decline starting in 2018 may be temporary or part of a trend?

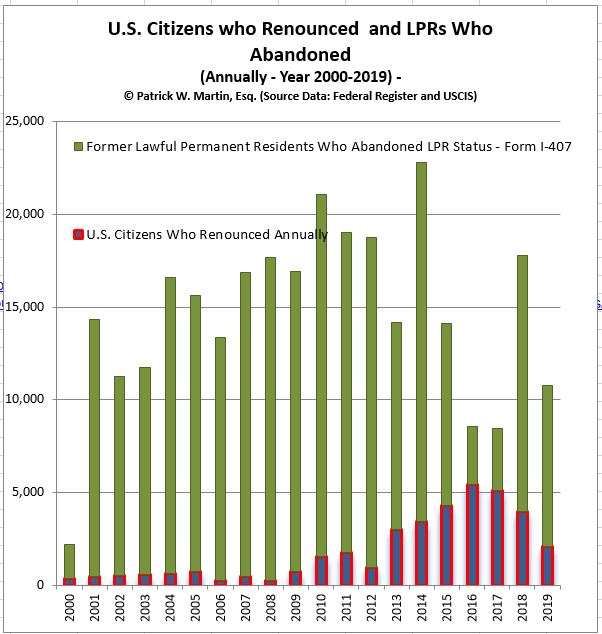

Subsequent posts will discuss the new trend of how relatively fewer lawful permanent residents (“LPRs”) are formally abandoning their status compared to USCs who formally renounce. This is true even though the number of USCs renouncing is in decline.

The expatriation laws were modified substantially in 2008 per the “HEART” Act, as part of a trend of changes in the expatriation tax law during a dozen year time frame. See prior post, Timeline Summary of Changes in Tax Expatriation Provisions Since 1996

There have been no substantial modifications to the law since 2008 when the “mark to market” rules were adopted. Importantly, expatriates often must concern themselves The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” These new taxes on “covered gifts” or “covered bequests” (currently taxed at 40% of the value of the property received) were adopted in 2008, but have yet to go into force. They can be particularly troublesome for LPRs – See, What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment? and “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – BIG GAP with Actual Emigration of LPRs