Social Security Tax Considerations

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

The Time has Come: Revocation or Denial of U.S. Passports as IRS Begins Issuing Notices to U.S. citizens

At the end of 2015 (Dec. 9), I posted a description of what was then a new law, passed by Congress – Revocation or Denial of U.S. Passport: More on new section 7345 (Title 26/IRC) and USCs with “Seriously Delinquent Tax Debt”

At the time, it was clear that the IRS and the Department of Justice was going to take a substantial amount of time to actually implement what is a major change in the law. In short, the IRS has the power and obligation to notify the Secretary of State to (i) deny a U.S. citizen (the “Taxpayer”) a U.S. passport, or (ii) revoke or not renew a U.S. passport of the Taxpayer. The law is not clear as to what steps the Department of State will necessarily take in response to the notification.

At the time, it was clear that the IRS and the Department of Justice was going to take a substantial amount of time to actually implement what is a major change in the law. In short, the IRS has the power and obligation to notify the Secretary of State to (i) deny a U.S. citizen (the “Taxpayer”) a U.S. passport, or (ii) revoke or not renew a U.S. passport of the Taxpayer. The law is not clear as to what steps the Department of State will necessarily take in response to the notification.

Now the administrative machine is in full force as the IRS has begun issuing special notices to restrict or ban a U.S. passport of the Taxpayer. See, IRS Notice – Notice 2018–01 and a dedicated portion of the IRS website that focuses on Section 7345 titled Revocation or Denial of Passport in Case of Certain Unpaid Taxes.

The IRS has begun issuing notices required under the law for those  Taxpayers who the IRS asserts have “seriously delinquent tax debt” as defined in the law – Taxpayer Notification – Notices CP 508C.

Taxpayers who the IRS asserts have “seriously delinquent tax debt” as defined in the law – Taxpayer Notification – Notices CP 508C.

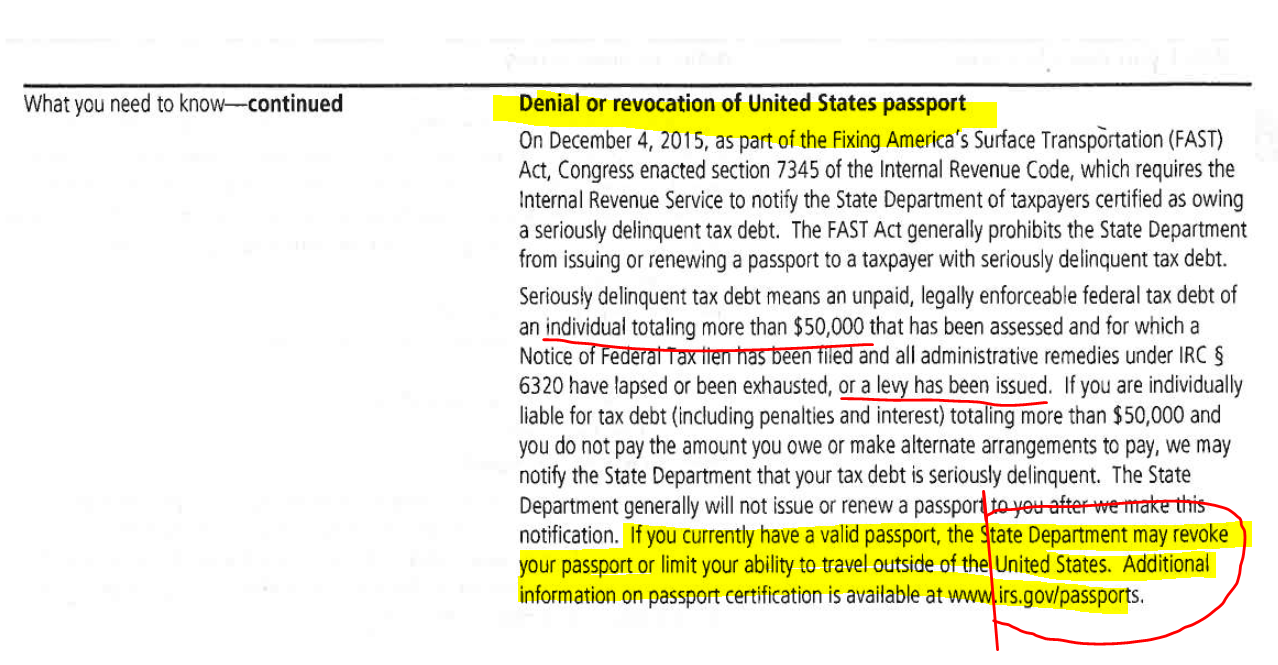

The Department of State’s website uses mandatory language regarding revoking, issuing or renewing a U.S. passport of U.S. citizens (“USCs”) once they have received certification from the Secretary of the Treasury –

If you have been certified to the Department of State by the Secretary of the Treasury as having a seriously delinquent tax debt, you cannot be issued a U.S. passport and your current U.S. passport may be revoked.

If you are overseas you may be eligible for a limited passport good for direct return to the United States.

We would suggest that if you have seriously delinquent tax debt, you contact the IRS to resolve your debt before applying for a passport. If you do not resolve your tax issues before applying for a passport, your application will be delayed or denied.

Indeed, a key representative from the IRS personally told me in Washington D.C. this May that the first batch of Notices CP 508C were issued as sort of a test batch of notices. Surely, Taxpayers will be forced to litigate and challenge the validity of these.

For those of us who have dedicated our professional lives to these issues, we see that probably more often than not, IRS notices of amount of taxes owing are erroneous. The IRS will use their own determinations of amount of taxes, penalties and interest owing, as in this example of a USC residing overseas:

There are two different judicial remedies a Taxpayer who is a USC can choose; file a suit in either U.S. Tax Court or a U.S. District Court to determine the validity or erroneous nature of any particular Notice CP 508C.

In addition, the IRS is now warning Taxpayers they may lose their passport in Notices of Intent to Levy. The following is sample text from  a recent Notice from the IRS to a USC residing outside the U.S.

a recent Notice from the IRS to a USC residing outside the U.S.

It has been reported that tens of thousands of IRS Notices CP 508C have been issued to Taxpayers during 2018. It remains to be seen the actual numbers of U.S. passports that will be revoked or denied by the Department of State upon receiving notice from the Secretary of Treasury (which notice is certified by the Commissioner of the Internal Revenue Service).

Generally, it will be the IRS Chief Counsel lawyers who litigate these issues before the U.S. Tax Court and the Department of Justice, Tax Division lawyers who litigate before the U.S. District Courts.

How the U.S. imposes income taxes on Social Security retirement benefits on former USCs and LPRs who reside outside the U.S.

Previous posts have explained how the Social Security Law and the U.S. federal tax law are different bodies of laws that have different rules for U.S. citizens who renounce and LPRs who formally abandon their permanent residency status.

This post explains the unique U.S. federal income tax treatment of social security retirement benefits. The tax treatment is different for USCs and former USCs who reside outside the United States.

- Former U.S. Citizens (25.5% Withholding Tax on All Amounts) – NO Graduated Tax Rates

Former USCs who reside outside the U.S. become “nonresident aliens” and hence are subject to a withholding tax that reduces the net Social Security benefits. The U.S. federal government withholds the tax immediately on all Social Security retirement payments to nonresident aliens at a 25.5% rate (calculated under the statute as 85% of the normal 30% statutory rate). See, IRC Section 871(a)(3).

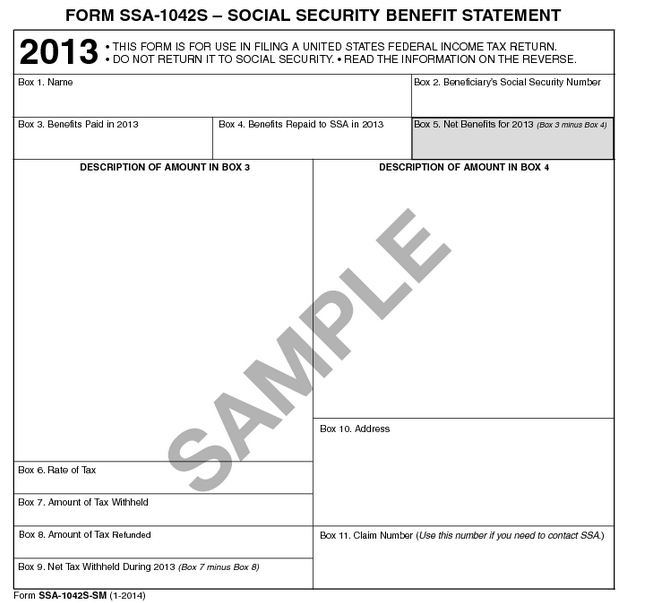

The IRS form used for withholding is SSA-1042S – Social Security Benefit Statement.

For instance if a monthly Social Security retirement payment is US$2,000 (gross), the tax withholding of 25.5%. creates a total tax withholding of US$510 (25.5% x US$2,000). This leaves a net retirement payment of US$1,490 that will be received by the former U.S. citizen. In relative terms, this is a very high effective tax rate, i.e., 25.5%, particularly considering in this example the former USC has only US$24,000 of annual Social Security retirement payments.

The same withholding tax rate applies if the former USC has millions of dollars of annual income, or no other sources of income; 25.5% – period.

- Current U.S. Citizens (0% Withholding Tax) – May or May Not be Taxable Depending Upon Total Income

There is no withholding tax imposed upon current USCs on Social Security retirement payments. However, there is an income tax that may be levied on a portion of the Social Security retirement payments, depending upon the total income of the individual. Basically, a USC needs to have more than US$25,000 of income annually, for any of the Social Security retirement income to be subject to U.S. income taxation. There are important detailed rules, where “modified adjusted gross income” is used to help make this determination of the so-called “base amount.”

See, IRC Section 86 for the specific statutory rules which provide that 50% of the Social Security retirement income is subject to taxation if the individual has an “adjusted base amount” of US$25,000 or more ($32,000 in case of a joint return).

The Social Security website describes this statutory rule in layman’s terms –

- Some people have to pay federal income taxes on their Social Security benefits. This usually happens only if you have other substantial income (such as wages, self-employment, interest, dividends and other taxable income that must be reported on your tax return) in addition to your benefits.

Once the “adjusted base amount” exceeds US$34,000 or more, then 85% of the Social Security retirement income is subject to taxation ($44,000 in the case of a joint return).

In the example used above of the US$24,000 of annual Social Security retirement payments, this income level will create no U.S. federal income taxation to a USC (not a former USC) if he or she has no other income.

In contrast, the former USC will have had indirectly paid (via the tax withheld), a total annual federal income tax of US$6,120 on the same amount of Social Security retirement benefits; US$24,000.

For the discussion of the IRS, explaining these rules, see Publication 915.

Finally, and most importantly for residents of certain countries (e.g., Canada), an income tax treaty with a specific provision can modify these rules in certain circumstances. Later posts will be dedicated to how these rules can be modified by an income tax treaty provision. Income tax treaties are not to be confused with Social Security Totalization Agreements. See, Social Security Retirement Benefits – for former USCs and LPRs (Intersection of U.S. Tax and Social Security Law)