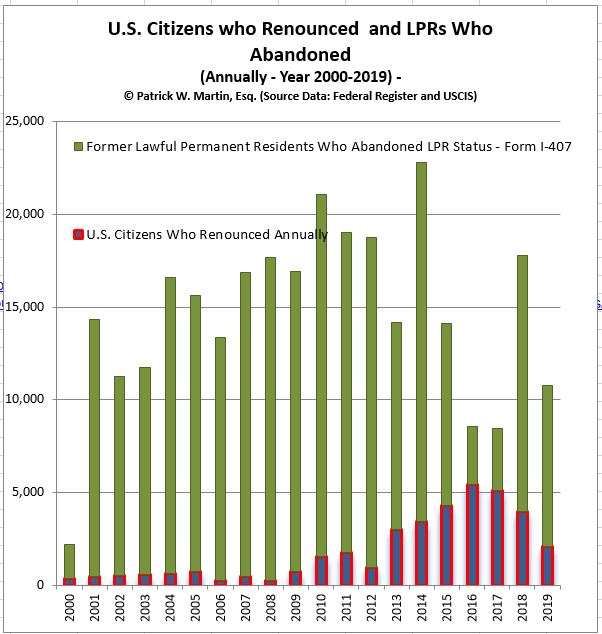

International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

EB-5 Visa – a common Path to a “Green Card” and then USC

Pathways to United States Citizenship – (USC): Focus on the EB-5

Every individual who ultimately becomes a naturalized U.S. citizen must first qualify for lawful permanent resident (“LPR”) status unless a narrow statutory exception applies. Although public attention frequently focuses on the EB-5 immigrant investor program, with the idea they are those with greater assets and income (contemplating taxes) EB-5 investors represent only a very small percentage of all individuals who become lawful permanent residents. Understanding the relative size of each immigration pathway is essential because every pathway ultimately raises many of the same U.S. tax issues—including worldwide income taxation, estate and gift taxation, and the tax consequences of later abandoning lawful permanent resident status or renouncing U.S. citizenship.

The EB-5 visa has been a fixture of U.S. law since the early 1990s. It was not until 2009 that a substantial number of EB-5 visas were issued in a given year, 4,218 to be exact. Statistically, the total EB-5 visa leading to LPR status is a fraction of the other categories as explained here. For an excellent overview of the law and categories, see the CRS report- Permanent Legal Immigration to the United States: Policy Overview (Updated November 4, 2024)

EB-5 Visa – to a “Green Card” then to United States Citizenship – (USC)

From the laws inception in 1992 through FY2004, there were only 6,024 EB-5 visas issued during that 12 year period. That is an annual average of only approximately 500 persons. See, the GAO Report on Immigrant Investors. As the program grew in popularity so too did the location of investors from around the world. It was not until 2009 when the total number of investors started growing substantially. Most significantly in 2009 when 4218 EB5 visas were issued, still less than 1/2 of the 10,000 allocated annually by the statute.

These numbers kept going at an annual pace especially starting in 2012, when 6,764 EB-5 visas were issued and then around 10K+/- annually for the last dozen years or so, up until the years that were impacted by a change in the law and a bit by COVID (2020 and 2021).

Chinese Investors Have Dominated the total Group of EB-5 Investors

The country-of-origin analysis is important because practitioners frequently advise clients from these jurisdictions regarding immigration planning, cross-border tax planning, and eventual expatriation planning with consequences in those countries.

I have compiled the total list of countries from which EB-5 visa investors came from as summarized in the Country of Origin global graphic for FYE 2024. There are over 100 countries from which these investors came from, but again, China is the dominant country, followed by Vietnam, India, Taiwan and then South Korea as the countries with the greatest number of investors. South Africa comes next, followed by Brazil and then Mexico, but each with less than 200 total investors, each country as follows:

China

9547

Vietnam

1533

India

1428

Taiwan

513

Korea, South

325

South Africa

158

Brazil

157

Mexico

128

Hong Kong S.A.R.

116

Venezuela

97

Canada

81

Great Britain & N. Ireland

63

Russia

58

Nigeria

52

Turkey

44

Colombia

44

France

38

United Arab Emirates

30

Germany

29

Japan

25

Singapore

23

Kazakhstan

21

Peru

20

Ukraine

17

Sweden

15

Argentina

15

Egypt

14

The importance of this analysis is to help individuals (and their advisors) who fit into these categories, e.g., who have a pathway to a green card and then on to become a naturalized U.S. citizen, understand the potential “tax expatriation” consequences of their decisions over the long-run.

What are the U.S. “tax expatriation” consequences to individuals who go down these pathways, including to their dependent children, or spouses or any future beneficiaries who are “United States person”?

What are the tax expatriation consequences if the individual later decides they do not want to be a green card holder or a U.S. citizen and later wishes to abandon their lawful permanent residency status or formally renounce their U.S. citizenship?

These and many other questions should be considered, especially for long-term family planning. Not just for the investor, but for their children and spouse, who may be eligible for the visa that can lead to LPR status and eventually to USC. Facilitating younger children (under 21 years of age) is a common driver for EB-5 investors for families who want the United States to be a pathway for their children’s’ future.

Why These Immigration Pathways Matter from a Tax Perspective

Every pathway leading to lawful permanent resident status almost always subjects the individual to the comprehensive U.S. federal income tax system. Depending upon the individual’s assets, family structure, treaty residence, and future living plans, obtaining a green card will also have significant implications for:

worldwide income taxation;

estate and gift taxation;

foreign trust reporting;

information reporting obligations under various laws;

controlled foreign corporation rules;

PFIC reporting;

exit tax planning; and

long-term succession planning.

Equally important, many lawful permanent residents eventually decide to return permanently to their country of origin or another foreign jurisdiction. Those individuals—and frequently their spouses and dependent children—must carefully consider the tax consequences of formally abandoning lawful permanent resident status or, after naturalization, renouncing U.S. citizenship. The sooner individuals and their advisors realize these consequences, the better they can plan for important life decisions.

Those tax consequences are collectively referred to as the U.S. tax expatriation rules, and they form the principal subject of this website.

The legal pathways towards lawful permanent residency status can be broken down into the following categories and the EB-5 category is a fraction (only about 1%) of the total pool leading to LPR status:

This category includes EB-1 through EB-5 categories that include individuals with extraordinary ability, certain professionals, other skilled workers. The chart I prepared here reflects the total number of EB-5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b).

EB-1, EB-2 and EB-3 represent the greatest group of individuals who obtained LPR status (e.g., approximately 5X, each category compared to the EB-5 category). See Yearbook of Immigration Statistics, Table 6.

For instance, annually the EB-1 through EB-3 categories are processing about 50K per year of each, and the EB-5 category is only 131K over most of its 25 year life (or about 10K per year – for more recent years). Approximately 16% of all green card holders come through these employment based preferences.

Table – Approximate Decade-Average Share by Category, FY2014–FY2023

Category

Approx. Share

Notes

Family-sponsored (total)

~64%

Immediate relatives + family preferences combined

— Immediate relatives

~46%

Spouses ~26%, parents ~14%, children ~6%

— Family preferences (F1–F4)

~18%

Numerically capped at 226,000

Employment-based (EB-1–EB-5)

~16%

Capped at 140,000; breached in COVID years

Refugees & asylees

~12%

Numerically unlimited; ceiling-driven volatility

Diversity

~4%

Statutory ceiling 55,000

All other / special

~4%

SIV, U/T victims, cancellation, registry, etc.

C. Diversity Immigrant Program

The annual diversity lottery, allocated by random selection, to natives of countries with historically low rates of immigration to the United States. See, 8 U.S. Code § 1153(c). The Attorney General plays a key role by statute in this determination. There is a statutory maximum of 55,000 and only represents about 4% of all LPRs compared to the larger pool. This program is on hold as of December 19, 2025 when the USCIS policy memorandum (PM-602-0193) directs officers to place an immediate hold on pending adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

D. Humanitarian and Special Pathways: Refugees/Asylees

Several routes proceed outside the preference system (the three categories above). Refugees and asylees adjust under a specific statutory regime; self-petitioning abused spouses and children proceed under other provisions; victims of qualifying crimes and of trafficking can adjust from U and T nonimmigrant status; and certain children subject to qualifying juvenile-court findings can qualify, among others. There are statutory limits placed on this group.

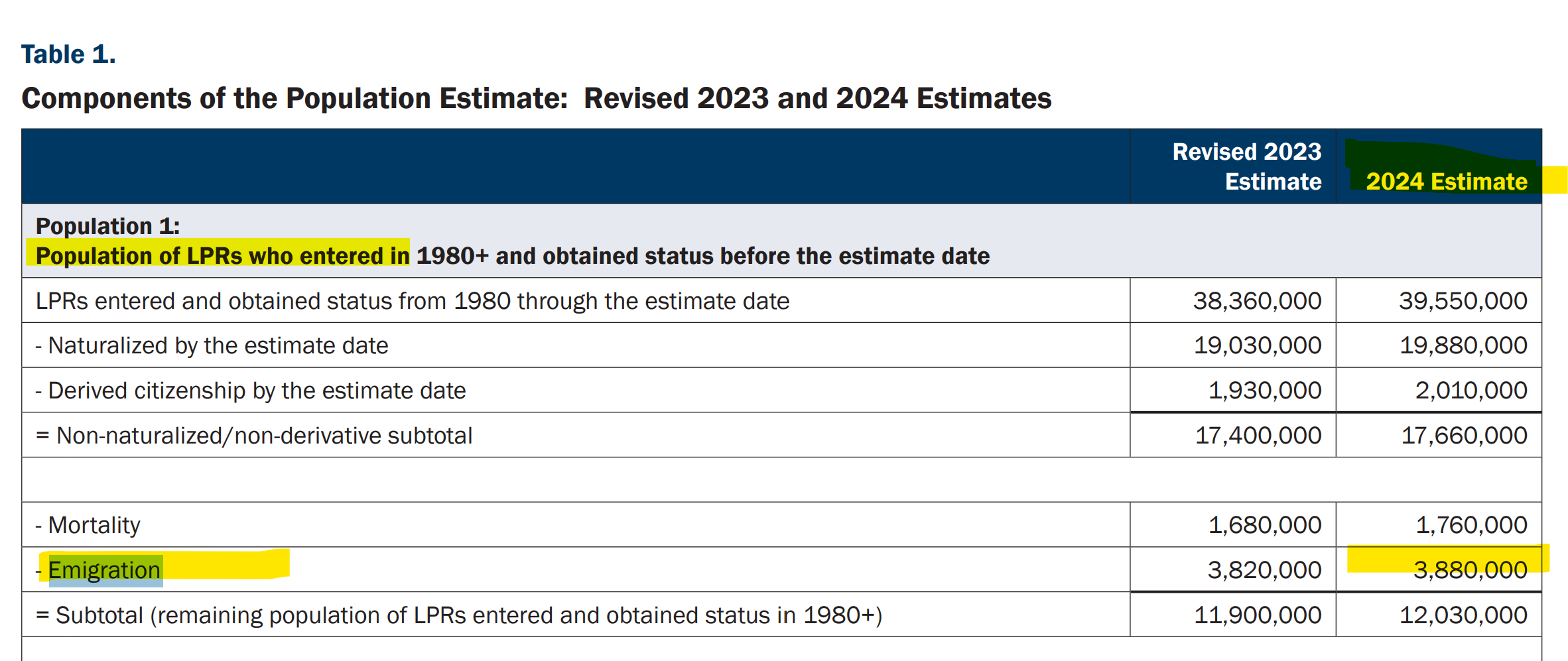

Whatever category one uses for LPR status, there will be important U.S. federal tax consequences to them and typically their family members. That’s the large part of the focus on this forum where the author has written about the subject of how it all ties to “tax expatriation”. As previously reported, there are 3.88 million “LPR” individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. See, Table 1 of the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023.

Is there a legal difference between “relinquishing” and “renouncing” U.S. citizenship for tax purposes?

For U.S. federal tax purposes, “relinquish” and “renounce” are in effect interchangeable. Many people assume the two words carry an important legal distinction. For federal tax purposes, they generally do not. This question was first taken up in an earlier post dated June 21, 2014. The expatriation tax statute, IRC Sections 877 and 877A (the U.S. tax rules that apply when a person gives up U.S. citizenship), uses both terms in the same breath. What drives the tax result is not which word applies but the “expatriation date.”

What date actually matters under the U.S. expatriation tax rules?

The key time reference is the “expatriation date.” Under IRC Sections 877 and 877A (the U.S. expatriation tax rules), this date is defined in Section 877A(g)(3). It focuses on specific dates tied to meetings or events with the U.S. Department of State. Because the tax outcome turns on this date, the choice between the words “relinquish” and “renounce” does not, by itself, change it.

Why don’t the words “relinquish” and “renounce” change the tax outcome?

Both words point to the same thing under the tax law. The expatriation tax statute, IRC Sections 877 and 877A, uses “renounce” and “relinquish” in the same breath. The result instead depends on the “expatriation date” defined in Section 877A(g)(3), which is tied to specific meetings or events with the U.S. Department of State. So the terminology a person uses does not, on its own, change the federal tax treatment.

Consult an experienced attorney about how these rules apply to a specific situation.

World Cup & Playing in the United States: Green Card Holders, the Treaty Tiebreaker, and the Global Athlete or Entertainer

As the world’s athletes have arrived to perform on U.S. soil, the U.S. tax system is a broad net. The 2026 FIFA World Cup—hosted across the United States, Mexico, and Canada—is a useful occasion to revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

This blog is dedicated to issues of “tax expatriation” which crosses into different professions and global lifestyles. See, for instance the following prior blogs:

There are of course many famous athletes who were not U.S. citizens and then became green card holders and oftentimes then became naturalized U.S. citizens. Since the Knicks just won the NBA championship after 53 years, one of their greatest, Patrick (mi tocayo) Ewing left Jamaica as a boy, became a green card holder and then a naturalized citizen. A 1985 New York Times article, A Favorite Son Goes Home, describes his first return to the island since a boy.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

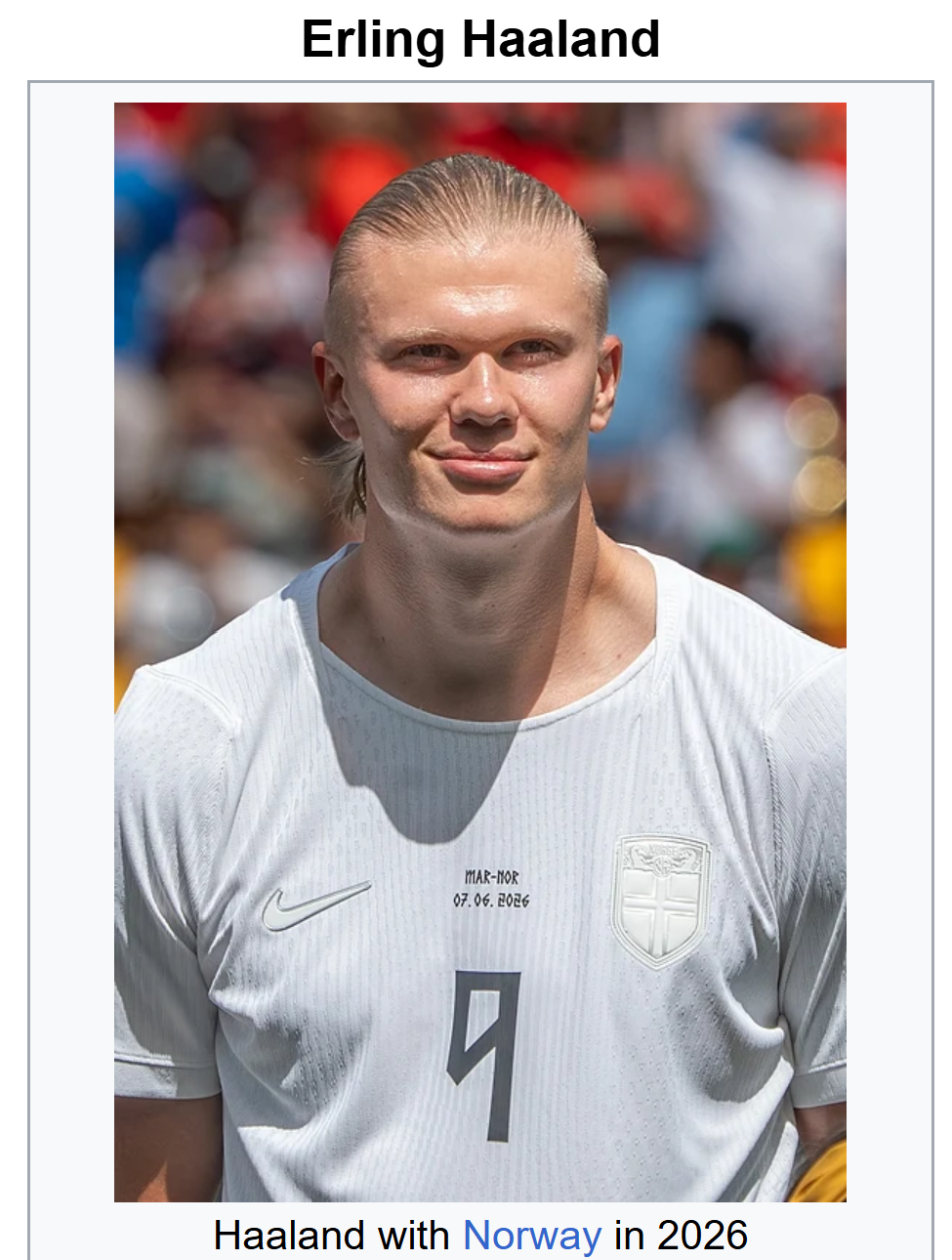

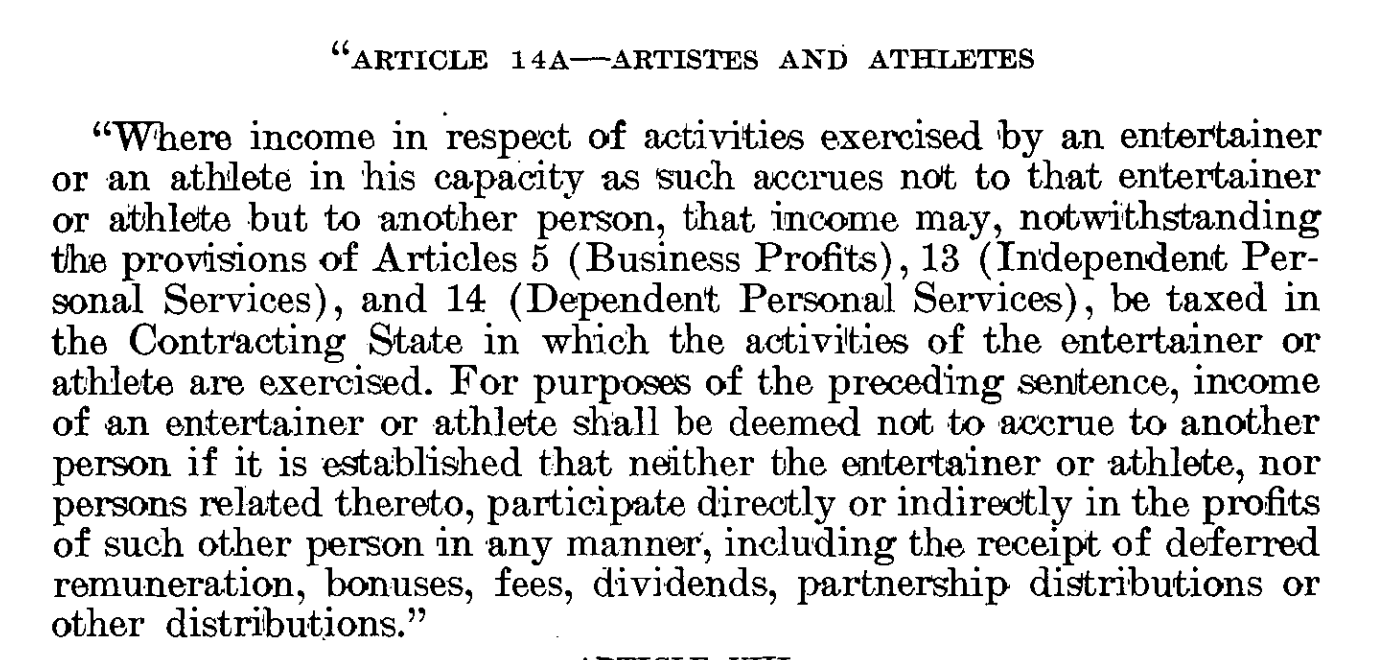

Athletes and entertainers are specially taxed in the U.S. in the sense they typically receive few benefits from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

A protocol to the treaty adopted in 1980 has a “new” article 14A specific to artists and athletes as reflected here in its entirety allowing the government to tax athletes and entertainers when they perform in the country (overriding other protective provisions of the treaty – e.g., Business Profits Art. 5, Independent Personal Services Art. 13 and Dependent Personal Services Art. 14):

The IRS also adopted a specific program, called the Central Withholding Agreement (“CWA”) program created by Revenue Procedure 89-47 specific to artists and athletes. I personally think it is a program that is not authorized by the statute and often applied by the IRS in a manner that violates the withholding tax regime we have in Chapter 3 of our statutory tax law, Subtitle A. In practice, third parties are subject to the 30% withholding tax on certain gross proceeds paid to companies other than the artist or athlete, if the athlete or artist doe not participate with the IRS in their CWA.

Mexico

In the case of global soccer players, even one with a “lawful permanent resident” card (i.e., a “green card”) they may be subject to the Chapter 3 withholding tax rules if the athlete is like Mr. Aroeste (Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC)) holding a green card in his pocket, but not a U.S. income tax resident by application of the residency rules set forth in an income tax treaty. Will the soccer player become a “covered expatriate” and not even know it (oops)?! It can get tricky quickly.

Meanwhile, Mexico and the U.S. have both advanced to the knockout round.

Canada plays Switzerland and presumably has a 99% chance of advancing to the Round of 23.

How much does it cost to renounce U.S. citizenship?

The fee to process a Renunciation of U.S. Citizenship rose to US$2,350, up from US$450. That is an increase of more than 500%. The U.S. Department of State announced the change, and it applies to the consular service of accepting and adjudicating a renunciation.

Why did the State Department raise the renunciation fee so much?

The Department said the new fee reflects the true cost of providing the service. Documenting a renunciation is described as extremely costly, because U.S. consular officers overseas spend substantial time to accept, process, and adjudicate each case. The fee had previously been subsidized, and the Department said it seeks to recover the cost of consular services through the fees it collects. It reviews these costs regularly and adjusts fees to match the cost of service.

When did the higher renunciation fee take effect?

The new fee took effect on September 12, 2014. The Department announced the change from Mexico City on August 28, 2014, as part of a broader adjustment to processing fees for several consular services.

How long can it take to get an appointment to renounce?

At some consulate offices around the world, appointments for renunciations were reportedly not available until the year 2015. A person seeking to renounce may face a long wait, because demand for these appointments can exceed what a given consulate can schedule in the near term.

What other consular fees changed at the same time?

Most nonimmigrant visa processing fees stayed the same, but several other fees moved alongside the renunciation fee:

The fee for E visas (treaty-traders and treaty-investors) decreased.

The fee for K visas (for fiancé(e)s of U.S. citizens) increased.

The fee for Border Crossing Cards for Mexican citizen minor applicants under age 15 increased by $1.

For immigrant visas, the fee for family-sponsored immigrant visas increased, as did the fee for domestic review of an Affidavit of Support.

All other immigrant and special visa processing fees that changed decreased.

Where were the new fees published, and could the public comment?

The proposed fees were published in the Federal Register and took effect 15 days later. The change was issued as an interim final rule, viewable at http://www.regulations.gov. Comments were accepted until 60 days after publication, and the Department said it would consider the public comments and address them in the published final rule. Fee information may also be found on the Bureau of Consular Affairs website, travel.state.gov, and on the websites of U.S. embassies and consulates.

The Social Security Act regulations set specific rules for Social Security numbers (SSNs) at § 422.103, titled “Social security numbers.” These rules cover how a person applies for an SSN, how to obtain a replacement Social Security card, how SSNs are assigned, and how the Department of Homeland Security (DHS) can have an agreement with the Social Security Administration (SSA) on issuing SSNs to people who have immigrated to the United States.

Who is eligible for a Social Security number?

Form SS-5 explains the general requirements for an SSN as set forth in the law. To qualify for an SSN and a card, an individual must be one of the following:

a U.S. citizen,

a person with lawful, work-authorized immigration status, or

a person with a valid non-work reason for requesting an SSN and a card.

How do you apply for a Social Security number?

Applications for an SSN are completed on Form SS-5, which is located on the SSA’s website. Form SS-5 sets out the general requirements for an SSN as established in the law, including that the applicant be a U.S. citizen, have lawful work-authorized immigration status, or have a valid non-work reason for requesting a number and card.

How do immigrants get a Social Security number through the immigration process?

Under § 422.103(b)(3), the “Immigration form” rule, SSA may enter into an agreement with the Department of State (DOS) and the Department of Homeland Security (DHS) to collect enumeration data as part of the immigration process. Where such an agreement is in effect, an alien need not complete a Form SS-5 with SSA. Instead, the person may request, through DOS or DHS as part of the immigration process, that SSA assign a Social Security number and issue a card. These requests are made on forms provided by DOS and DHS.

How many replacement Social Security cards can a person get?

The regulations limit how many replacement Social Security cards a person may receive. An individual may obtain a maximum of 10 replacement cards over a lifetime.

Can you cancel or expunge your Social Security number after losing US citizenship or green card status?

There appears to be no statutory or regulatory rule in the law that allows an individual to “expunge” or otherwise terminate a Social Security number once it has been obtained. This appears to remain the case even after a person loses U.S. citizen (USC) or lawful permanent resident (LPR, or green card) status. The assigned number generally stays in place. Anyone weighing the tax or immigration consequences of giving up citizenship or a green card may want to consult an experienced attorney.

Can You Lose Your Green Card Just by Living Outside the United States?

Many green card holders who move abroad assume their permanent resident status is safe as long as they return to the United States occasionally. Under US immigration law, that assumption can be wrong. A green card can be abandoned automatically, without any formal filing, simply by how long you spend outside the United States.

A lawful permanent resident (LPR) can lose permanent resident status through removal (deportation) ordered by an immigration court, or through abandonment. Abandonment can happen formally, by filing Form I-407 (Abandonment of Lawful Permanent Resident Status), or automatically, by operation of law, when an LPR takes an action that constitutes abandonment under immigration law, such as departing the United States for more than a temporary visit abroad.

What triggers an automatic abandonment finding?

The Department of Homeland Security (DHS) will make an abandonment finding if an LPR takes a single trip outside the United States lasting more than one year. After a trip of more than one year, the LPR can only challenge the finding in removal proceedings. For a single trip lasting between 6 months and one year, DHS presumes the LPR intended to abandon their permanent resident status, but the LPR may rebut that presumption. Even for shorter trips, DHS may find abandonment if the LPR has spent a significant amount of time outside the United States on multiple trips.

What factors does DHS consider?

DHS and the immigration courts look at: the purpose and duration of the trip abroad; whether there was a specific event after which the LPR planned to return; and the LPR’s family ties, employment, property holdings, and business affiliations in the United States versus the foreign country.

How does filing a tax return as a non-resident affect your status?

Filing a US income tax return as a non-resident alien raises a rebuttable presumption of abandonment of LPR status for immigration purposes.

What can you do if you expect a long absence?

If an LPR knows they will need to spend significant time outside the United States, they should apply for a reentry permit before departing. A reentry permit alone does not guarantee readmission following a long absence, but it is evidence of the intent to return to the United States and maintain permanent resident status.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

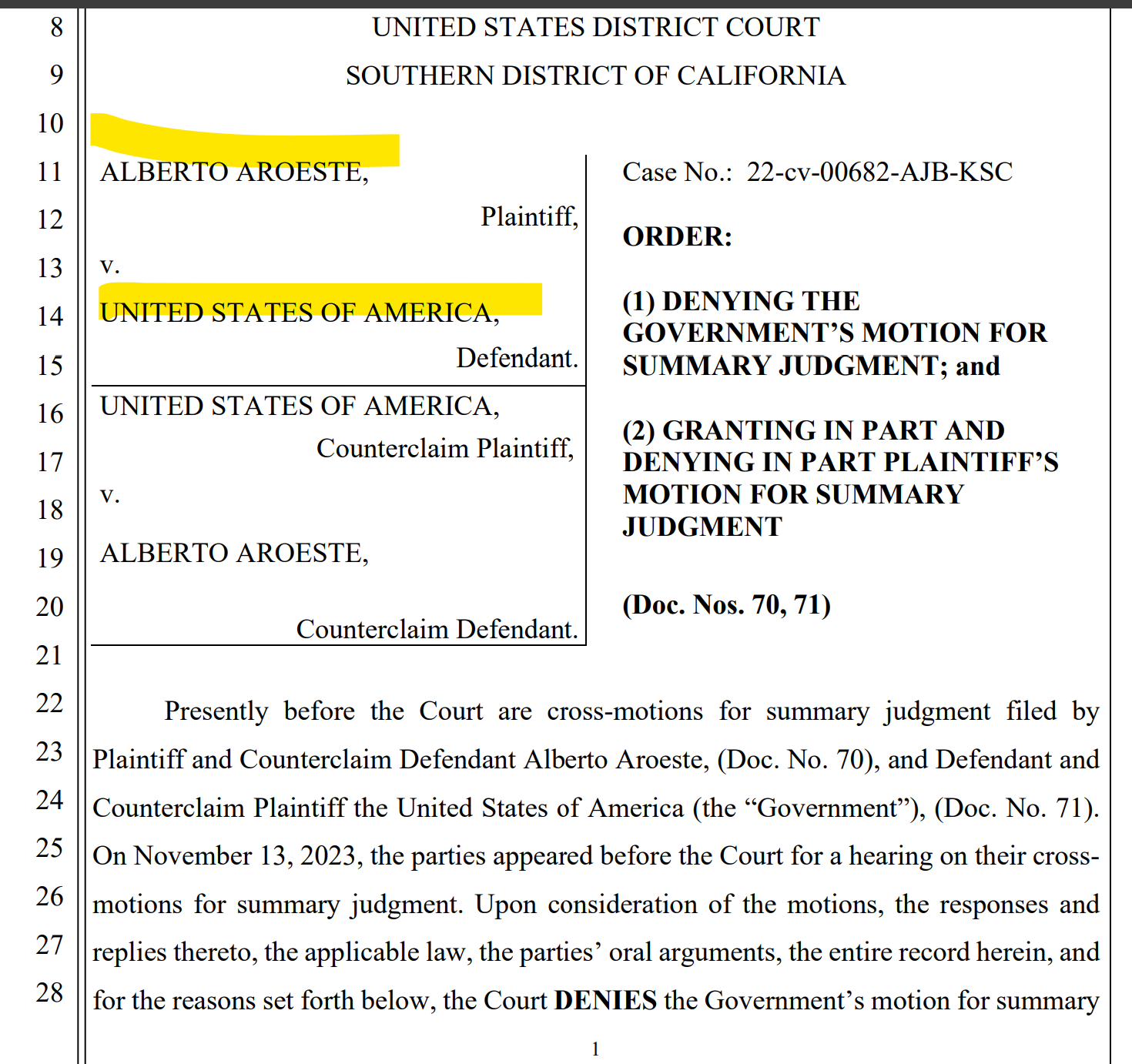

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

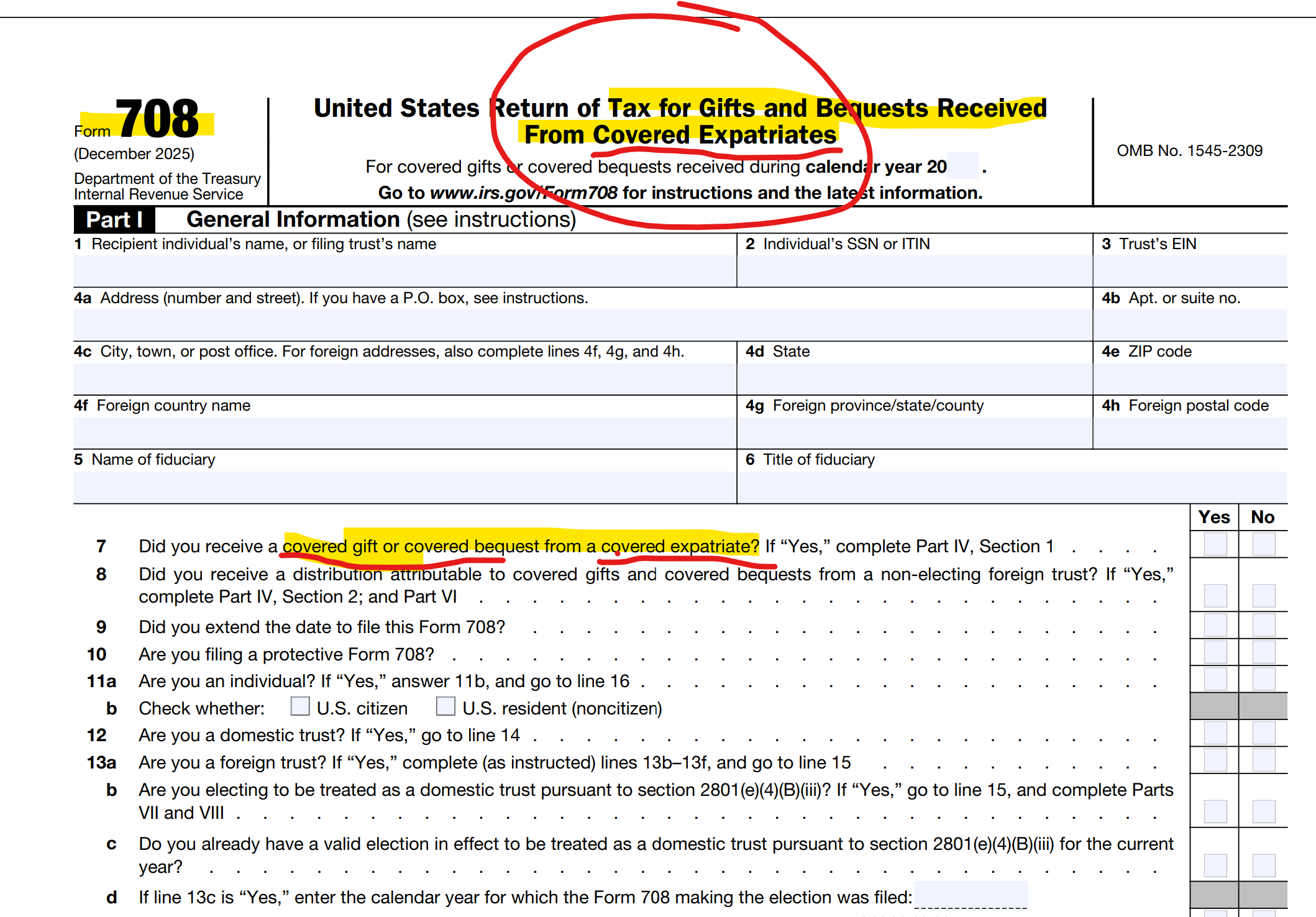

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Did USCs Born in the U.S. lately (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

Sec. 2. Policy. (a) It is the policy of the United States that no department or agency of the United States government shall issue documents recognizing United States citizenship, or accept documents issued by State, local, or other governments or authorities purporting to recognize United States citizenship, to persons: (1) when that person’s mother was unlawfully present in the United States and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth, or (2) when that person’s mother’s presence in the United States was lawful but temporary, and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth.

(b) Subsection (a) of this section shall apply only to persons who are born within the United States after 30 days from the date of this order.

SCOTUS Announced it Will Hear Arguments on May 15, 2025

The Congressional Research Service has an excellent summary article it prepared in 2018, titled – The Citizenship Clause and “Birthright Citizenship”: A Brief Legal Overview (1 Nov. 2018). This report was drafted when President Trump during his first term questioned the validity of “birthright citizenship”. Below is an excerpt from that 2018 article, relevant to the:

Under federal law, nearly all people born in the United States become citizens at birth. This rule is known as “birthright citizenship,” and it derives from both the Constitution and complementary statutes and regulations. The Citizenship Clause of the Fourteenth Amendment states that “[a]ll persons born or naturalized in the United States, and subject to the jurisdiction thereof, are citizens of the United States and of the State wherein they reside.” The Immigration and Nationality Act (INA), in turn, declares certain persons to be U.S. citizens and nationals at birth. INA § 301(a) more or less tracks the Citizenship Clause in stating that “a person born in the United States, and subject to the jurisdiction thereof” is a “national[] and citizen[] of the United States at birth.” (The INA also extends citizenship at birth to various persons not protected by the Citizenship Clause, such as those born abroad to some U.S. citizen parents.) Federal regulations—including those that govern the issuance of passports and access to certain benefits—implement the INA by providing that a person is a U.S. citizen if he or she was born in the United States, so long as the parent was not a “foreign diplomatic officer” at the time of the birth.

The report goes on to explain –

The weight of current legal authority suggests that these executive and legislative proposals to restrict birthright citizenship would contravene the Citizenship Clause. At least since the Supreme Court’s decision in the 1898 case United States v. Wong Kim Ark, the prevailing view has been that all persons born in the United States are constitutionally guaranteed citizenship at birth unless their parents are us born individuals foreign diplomats, members of occupying foreign forces, or members of Indian tribes. In Wong Kim Ark, the Court held that a man born in the United States in 1873 to parents who were Chinese nationals acquired citizenship at birth under the Fourteenth Amendment. The parents were ineligible to naturalize under the law of the time, but they had established “permanent domicile and residence in the United States.” The Court reasoned that the Citizenship Clause should be “interpret[ed] in light of the common law” and grounded its holding in the common law principle of jus soli or “right of the soil.” Pursuant to that principle, “every child born in England of alien parents was a natural-born subject, unless the child of an ambassador or other diplomatic agent of a foreign state, or of an alien enemy in hostile occupation of the place where the child was born.”

Tax Expatriation Consequences –

As to “tax expatriation” – of these individuals? I suspect these babies (i.e., those born after 30 days from the executive order; on or after February 19, 2025) will have bigger issues to worry about other than their U.S. tax issues if SCOTUS rules against them.

Did USCs Born in the U.S. (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

Part I of Part II: The Gold Card – “It’s like the green card, but better and more sophisticated.”

Will the “gold card” sell to ultra high net worth investors around the world who want U.S. citizenship (“USC”)? What are the tax costs of USC? * About the Author: Patrick W. Martin

President Trump again announced on April 3, aboard Air Force One his plan:

Whether the U.S. adopts a new “Gold Card” “For $5 million [that] we will allow the most successful job-creating people from all over the world to buy a path to U.S. citizenship,” is up to the U.S. government.

Congress can amend Title 8 and include a new “Gold Card” option.

Current law provides the EB-5 visa as one path towards a “green card” that ultimately can lead to U.S. citizenship through naturalization.

President Trump presented at his March 4th speech to a joint session of Congress, explaining the concept: “It’s like the green card, but better and more sophisticated. And these people will have to pay tax in our country.”

Sounds like a panacea to help the U.S. federal deficit problem? If 100,000 of these “Gold Cards” were sold for $5M each, and these funds were paid directly over to the federal government, that would raise $500 billion dollars. If 1 million were sold, that would be $5 trillion dollars to use to pay down the deficit (running annually at far greater than $1 trillion dollars since 2019).

To put that into perspective, the EB-5 visa that also leads to a “green card” that can further lead to U.S. citizenship through naturalization has an annual visa limit of about 10,000. See, USCIS’s article – (16 Aug 2024) – Annual Limit Reached in the EB-5 Unreserved Category There have been multiple years where the annual visa limit was not met. Prior to 2015, the 10,000 visa limit was never met and in several years there were less than 500 EB-5 visas issued annually.

There have been less than 150,000 EB-5 visas issued over the last 35 years since its adoption in 1990. Is it realistic to be able to “sell” even ten thousand $5M gold visas annually, when the “green EB-5 visa” costs $800,000 and has had less than 150,000 issued in nearly 35 years?

Equity Investment for EB-5 visa – $800,000 (Does NOT go to the Government)

The total required equity investment amount for an EB-5 visa in the qualifying project, is only $800,000 (if in a “TEA”). See, EB-5 Immigrant Investor Program, as published by the U.S. Citizenship and Immigration Services (USCIS). See, USCIS’s Chapter 2 – Immigrant Petition Eligibility Requirements. It used to be only $500,000 (1/10th of $5M). A TEA is a targeted employment area (“TEA”) that meets specific requirements under the law. If the capital investment is not in a TEA, the required minimal capital investment amount is $1,050,000 that increases in January 1, 2027 and each 5 years thereafter. Still about 1/5th the cost of a “gold visa”.

U.S. Estate and Gift Tax Consequences for U.S. Citizens and those with a Green Card (“Gold Card”?)

Finally, maybe the biggest impact on who wants an investor visa that leads to U.S. citizenship depends largely upon the U.S. income tax and U.S. estate and gift tax consequences. There are many tax implications. See, my case Aroeste v United States – Order Nov 2023, that was appealed to the 9th Circuit by the Office of Solicitor General (DOJ). U.S. District Court ruled in favor of green card holder.

which has a chart reflecting the total Chinese investors as a percentage of total – Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

which has a chart reflecting the total Chinese investors as a percentage of total – Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b).

5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b). adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —