Month: September 2018

Taxpayer’s Advocate (TAS) and Passport Revocations – Unconstitutional Restriction on Right to Travel Internationally?

As the State Department starts rolling out more letters denying U.S. passport renewals and initial applications on the backs of IRS Notices CP 508C to U.S. citizens (USCs); USC taxpayers are highly motivated to  address their “seriously delinquent tax debts.” What rights do USCs have vis-a-vis these government allegations in their tax certifications?

address their “seriously delinquent tax debts.” What rights do USCs have vis-a-vis these government allegations in their tax certifications?

For a deep dive into a range of issues that USCs need to consider, if they find themselves on the side of an unfortunate IRS Notices CP 508C – see the TAS’s excellent Interim Guidance Memorandum dated April 26, 2018. One key point made by the TAS memo is:

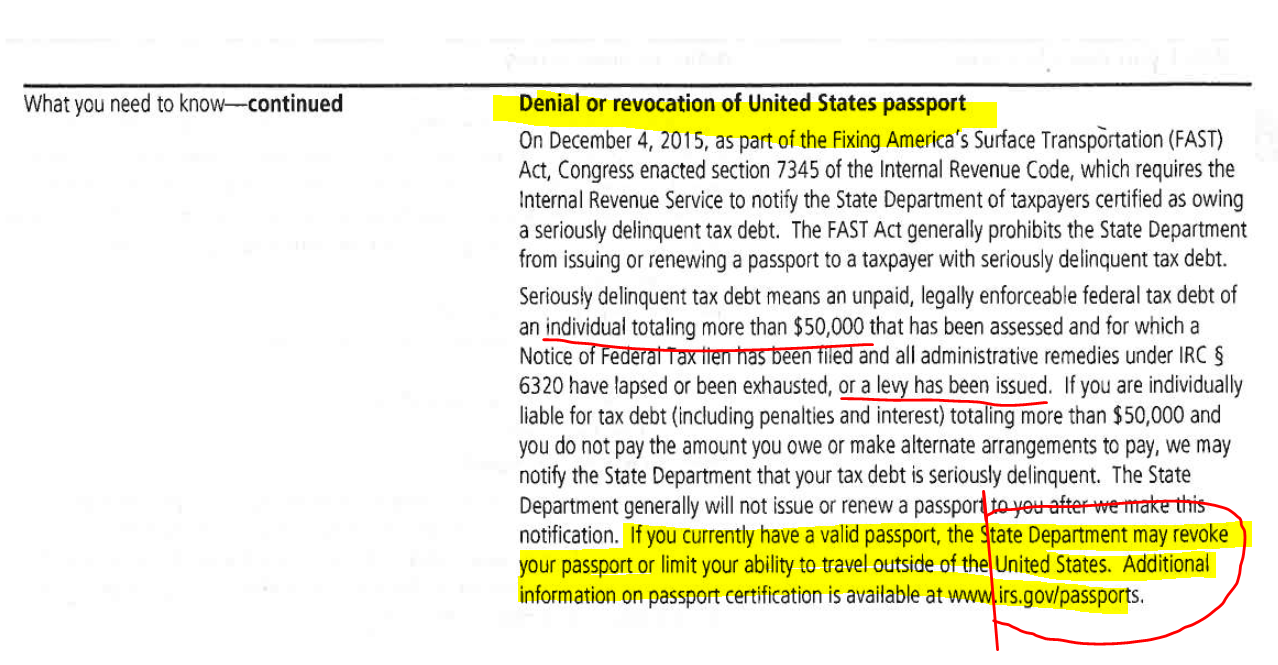

The right to travel internationally is a fundamental right, protected by the Due Process Clause of the Constitution. Under the Universal Declaration of Human Rights, adopted in 1948 by the United Nations after a unanimous vote (including the United States) “[e]veryone has the right to leave any country, including his own, and to return to his country.” The National Taxpayer Advocate expressed concerns that the IRS’s implementation of the passport program fails to protect taxpayers’ right to travel as well as their rights promised under the Taxpayer Bill of Rights. See the National Taxpayer Advocate’s blog and the Fiscal Year 2018 Objectives Report to Congress.

The U.S. Supreme Court, in an opinion penned by retired Justice Souter in Sosa v. Alvarez-Machain (2004), has some interesting observations about the Universal Declaration of Human Rights (which is cited above by the Taxpayer Advocate) limiting its application in the Alvarez-Machain case. This is a fascinating case to read, as it arises out of the tragic torture and murder of a DEA agent, Enrique Camarena-Salazar in 1985 in Mexico. Physician Alvarez-Machain was subsequently indicted in the U.S. as part of the torture and murder scheme and the DEA hired private Mexican nationals to seize  Alvarez and bring him to the United States in a private plane to stand trial.

Alvarez and bring him to the United States in a private plane to stand trial.

Alvarez-Machain was ultimately granted motion for a judgement of acquittal on the criminal charges.

In response, Alvarez-Machain then sued the federal government under the Federal Tort Claims Act and the Alien Tort Statute.

The Supreme Court opined (on these tort action claims and the application of international law as to U.S. federal tort statutes) as follows:

. . . To begin with, Alvarez cites two well-known international agreements that, despite their moral authority, have little utility under the standard set out in this opinion. He says that his abduction by Sosa was an “arbitrary arrest” within the meaning of the Universal Declaration of Human Rights (Declaration), G. A. Res. 217A (III), U. N. Doc. A/810 (1948). And he traces the rule against arbitrary arrest not only to the Declaration, but also to article nine of the International Covenant on Civil and Political Rights (Covenant), Dec. 19, 1996, 999 U. N. T. S. 171,22 to which the United States is a party, and to various other conventions to which it is not. But the Declaration does not of its own force impose obligations as a matter of international law. See Humphrey, The UN Charter and the Universal Declaration of Human Rights, in The International Protection of Human Rights 39, 50 (E. Luard ed. 1967) (quoting Eleanor Roosevelt calling the Declaration “ ‘a statement of principles … setting up a common standard of achievement for all peoples and all nations’ ” and “ ‘not a treaty or international agreement … impos[ing] legal obligations’ ”).23 And, although the Covenant does bind the United States as a matter of international law, the United States ratified the Covenant on the express understanding that it was not self-executing and so did not itself create obligations enforceable in the federal courts. . . [emphasis added]

Section 7345(e) provides for judicial review of the IRS’s certifications of “seriously delinquent tax debts” as follows:

(e)Judicial review of certification

After the Commissioner notifies an individual under subsection (d), the taxpayer may bring a civil action against the United States in a district court of the United States or the Tax Court to determine whether the certification was erroneous or whether the Commissioner has failed to reverse the certification.

Surely, the U.S. Tax Court and Federal District Courts will have much more to say about the rights of USCs who have their U.S. passports revoked or renewals denied by application of 26 U.S.C. 7345. Will the Universal Declaration of Human Rights be meaningful to the Courts applying Section 7345?

How many errors will the IRS make in issuing certifications of “seriously delinquent tax debts” to USCs around the world?

22. Article nine provides that “[n]o one shall be subjected to arbitrary arrest or detention,” that “[n]o one shall be deprived of his liberty except on such grounds and in accordance with such procedure as are established by law,” and that “[a]nyone who has been the victim of unlawful arrest or detention shall have an enforceable right to compensation.” 999 U. N. T. S., at 175—176.

23. It has nevertheless had substantial indirect effect on international law. See Brownlie, supra, at 535 (calling the Declaration a “good example of an informal prescription given legal significance by the actions of authoritative decision-makers”).

Part II: Example of United States Department of State – Letter Denying Passport Renewal – The Time has Really Come: Revocation or Denial of U.S. Passports as IRS Begins Issuing Notices to U.S. citizens

Earlier posts have addressed Section 7345 of Title 26 and how the U.S. Department of State (DOS) will deny the renewal of passports.

See, The Time has Come: Revocation or Denial of U.S. Passports as IRS Begins Issuing Notices to U.S. citizens and Revocation or Denial of U.S. Passport: More on new section 7345 (Title 26/IRC) and USCs with “Seriously Delinquent Tax Debt”

The IRS has purportedly issued tens of thousands of IRS Notices CP 508C to U.S. citizen (USC) taxpayers during the first part of this year, 2018.

We have now started seeing examples of the letters issued by the DOS. They are harsh and direct.

See here such a letter, with identifying information redacted.

The letter from the DOS says it is obliged to comply with the letter from the Department of Treasury’s Internal Revenue Service (IRS) certifying the USC has a “seriously delinquent tax debt.” The letter goes on to say that it has no actual information concerning the “seriously delinquent tax debt” and it is the IRS who must be contacted.

The DOS essentially “washes its hands” of this legal issue, by simply saying the USC taxpayer must resolve the issue within ninety days directly with the IRS.

Only after “”these arrangements” have been made with the IRS, can the USC taxpayer contact the National Passport Information Center according to the letter.

There are a host of legal issues and practical problems that USC taxpayers face in these circumstances. Many of these will be covered in later posts.

. . . more to come . . .

Is it too late to comply with the “965 Hammer” (aka the “Transition” or “Repatriation” Tax) for USCs Residing Overseas?

For more background on how Section 965 works, please see, The “965 Hammer” (aka the “Transition” or “Repatriation” Tax) for USCs Residing Overseas, which explains how U.S. citizens (USC) residing overseas may owe U.S. federal income tax on “phantom income”.  I call it phantom income as it does not need to be received (nor does the USC) need to have any right to it for it to be taxed.

I call it phantom income as it does not need to be received (nor does the USC) need to have any right to it for it to be taxed.

The tax is calculated with reference to (1) the type of assets held in the USC’s foreign corporation (cash or not), and (2) the previously un-taxed earnings of the foreign corporation owned by the USC.

The IRS has a dedicated page on their website to the Section 965 Transition Tax that provides a basic overview. The rules are complex and the IRS addressed a set of Q&As to help taxpayers understand how they must report on their tax return; see, Questions and Answers about Reporting Related to Section 965 on 2017 Tax Returns

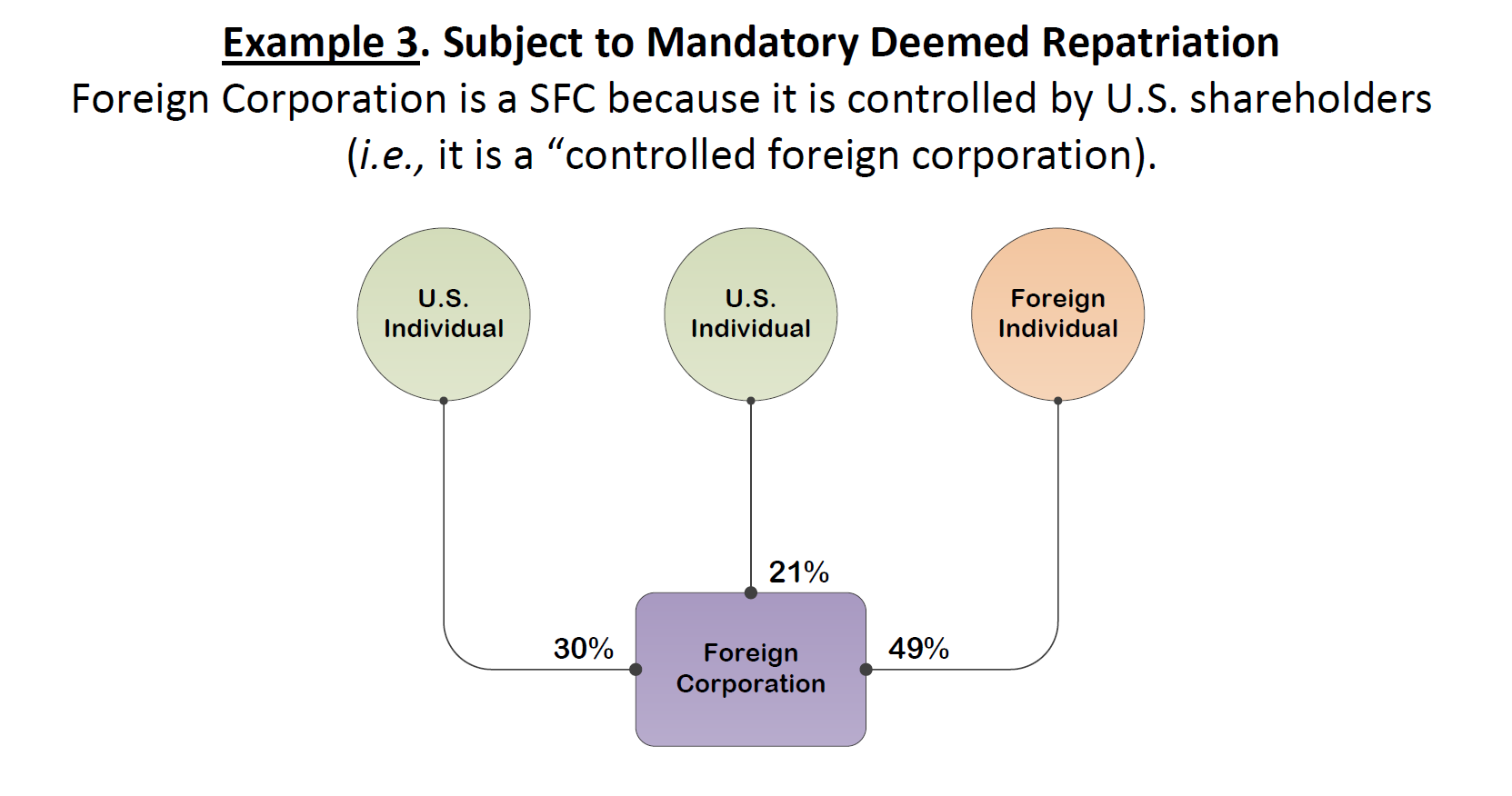

Normally, USCs combined with other “U.S. persons” need to have greater than 50% of the shares of the foreign corporation to be subject to the 965 Hammer/Repatriation tax.  The following example shows how U.S. individuals combined to own 51% cause the foreign corporation to be a “controlled foreign corporation” (CFC) and therefore a “specified foreign corporation” (SFC) that causes the USCs to be subject to the tax on “phantom income” to the extent the company has previously un-taxed earnings.

The following example shows how U.S. individuals combined to own 51% cause the foreign corporation to be a “controlled foreign corporation” (CFC) and therefore a “specified foreign corporation” (SFC) that causes the USCs to be subject to the tax on “phantom income” to the extent the company has previously un-taxed earnings.

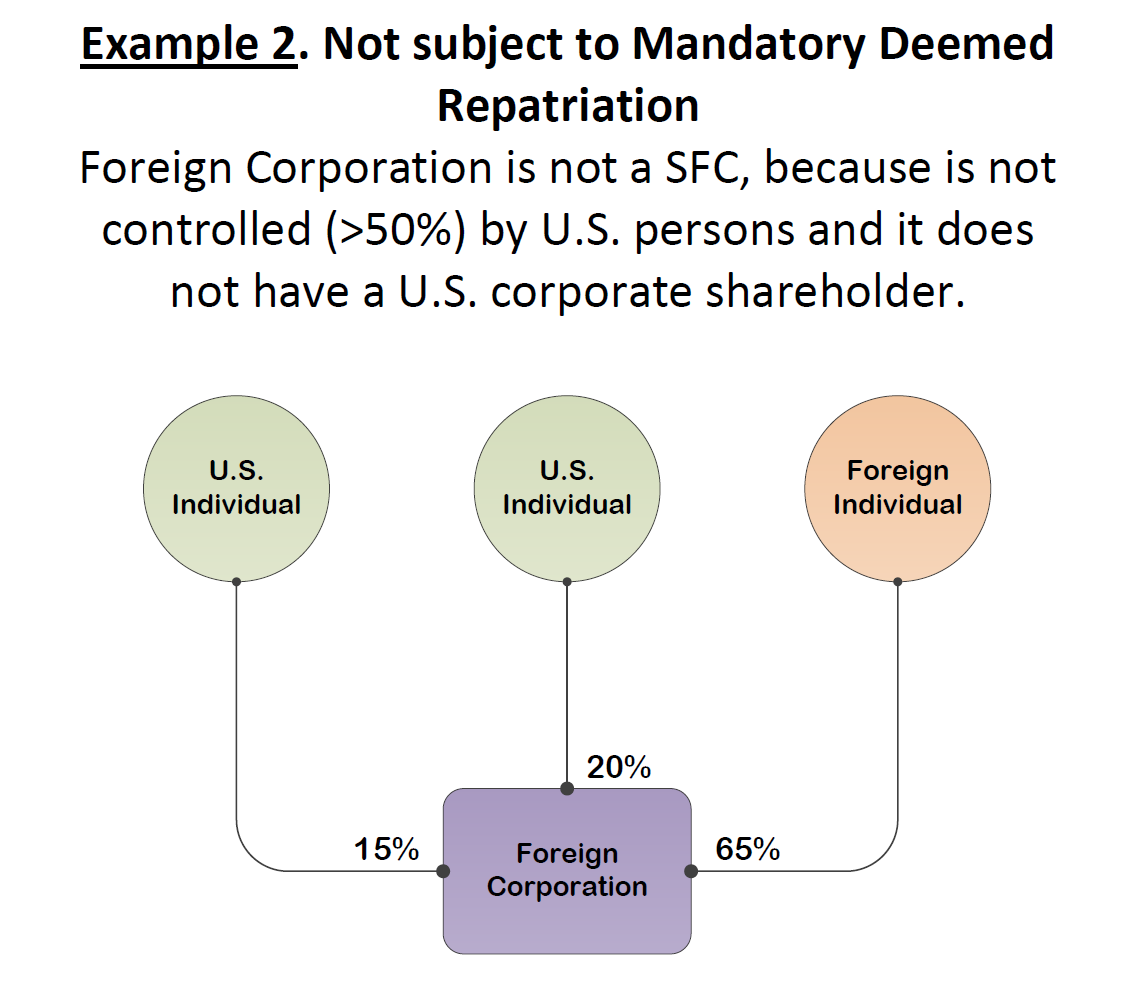

In contrast, a USC that owns 10% (or 21% or 30%) should not be subject to this tax, as long as the foreign corporation is not a CFC and/or there is no U.S. corporate shareholder that owns 10% or more of the foreign corporation. The following example (Example 2) shows how a USC that owns 15% and another USC who owns 20% of a foreign corporation, will not be subject to the 965 Hammer, since it is neither a CFC or a SFC.

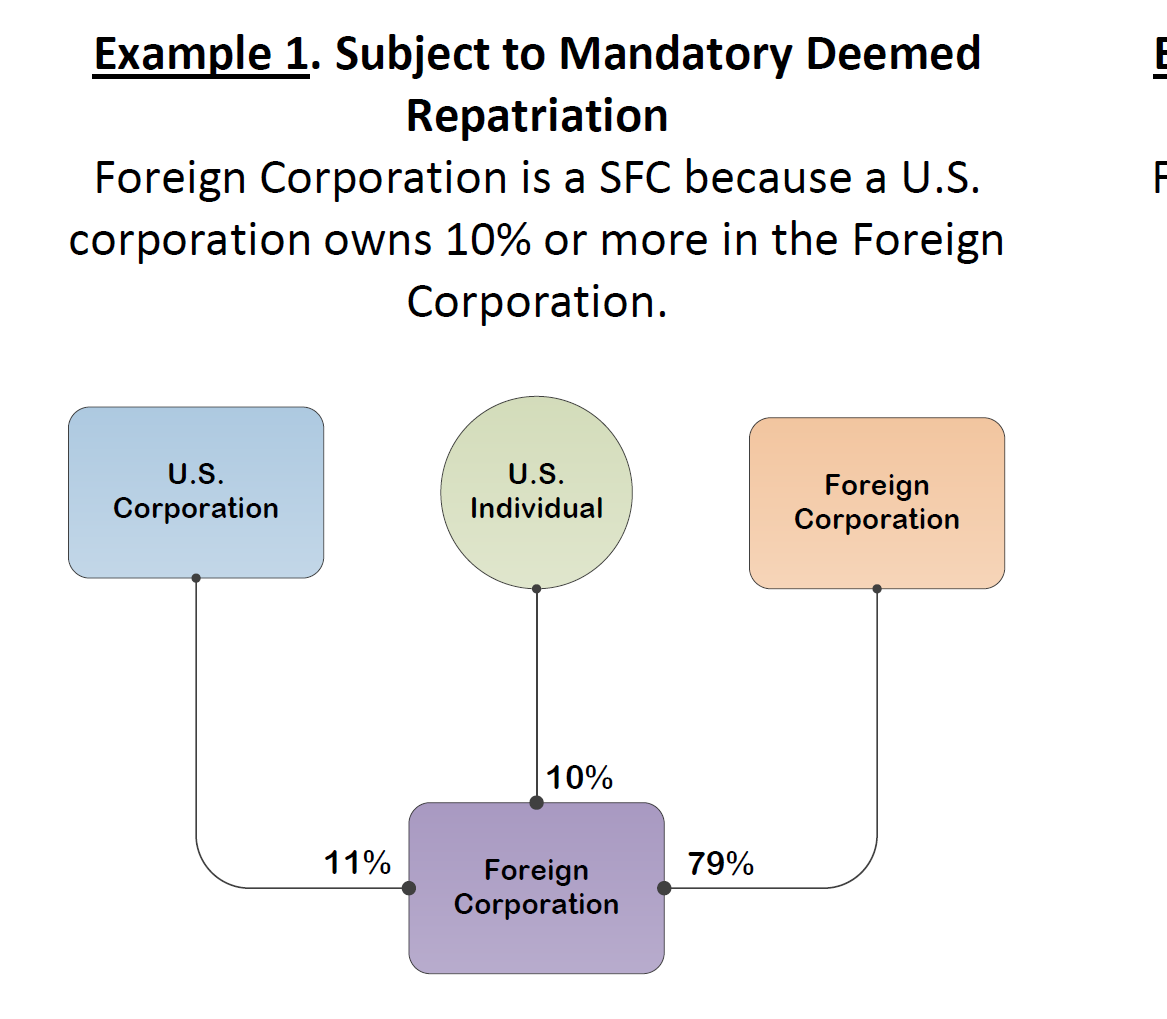

Compare that scenario to the following example (Example 1) that shows the somewhat “capricious” nature of how a USC that only owns 10% in a different fact pattern of ownership, can still be subject to the 965 Hammer repatriation tax. This is true, even when other U.S. owners have a mere 11% ownership (but in this case it is a U.S. corporate owner with >=10%), causing it to be a SFC and therefore triggering the 965 Hammer/repatriation tax:

In this last example, the USC owns only 10% of the shares of the foreign corporation, but since a U.S. corporate shareholder owns at least 10% of the shares of the same foreign corporation, all U.S. shareholders are subject to the 965 Hammer/repatriation tax.

There are some silver linings to this tax.

First, the tax rate applicable (8% in the case of non-cash assets) can be much lower than the normal statutory rate on dividend distributions.

Second, since the tax is mandatory (hopefully at a lower rate as cash and cash equivalents carry out a 15.5% higher tax rate), it can provide an opportunity to restructure and/or repatriate profits of the foreign corporation. This can give liquidity in the hands of the USC shareholder who was otherwise deterred from making actual dividend distributions or investing in U.S. property (which is in itself normally deemed a dividend to the USC shareholder) for foreign corporations that are “CFCs.”

Maybe USCs residing overseas will want to restructure their business operations to obtain specific tax advantages from the federal tax reform (e.g., 21% or 13.25% corporate tax rates that can be applicable for U.S. corporate taxpayers)?

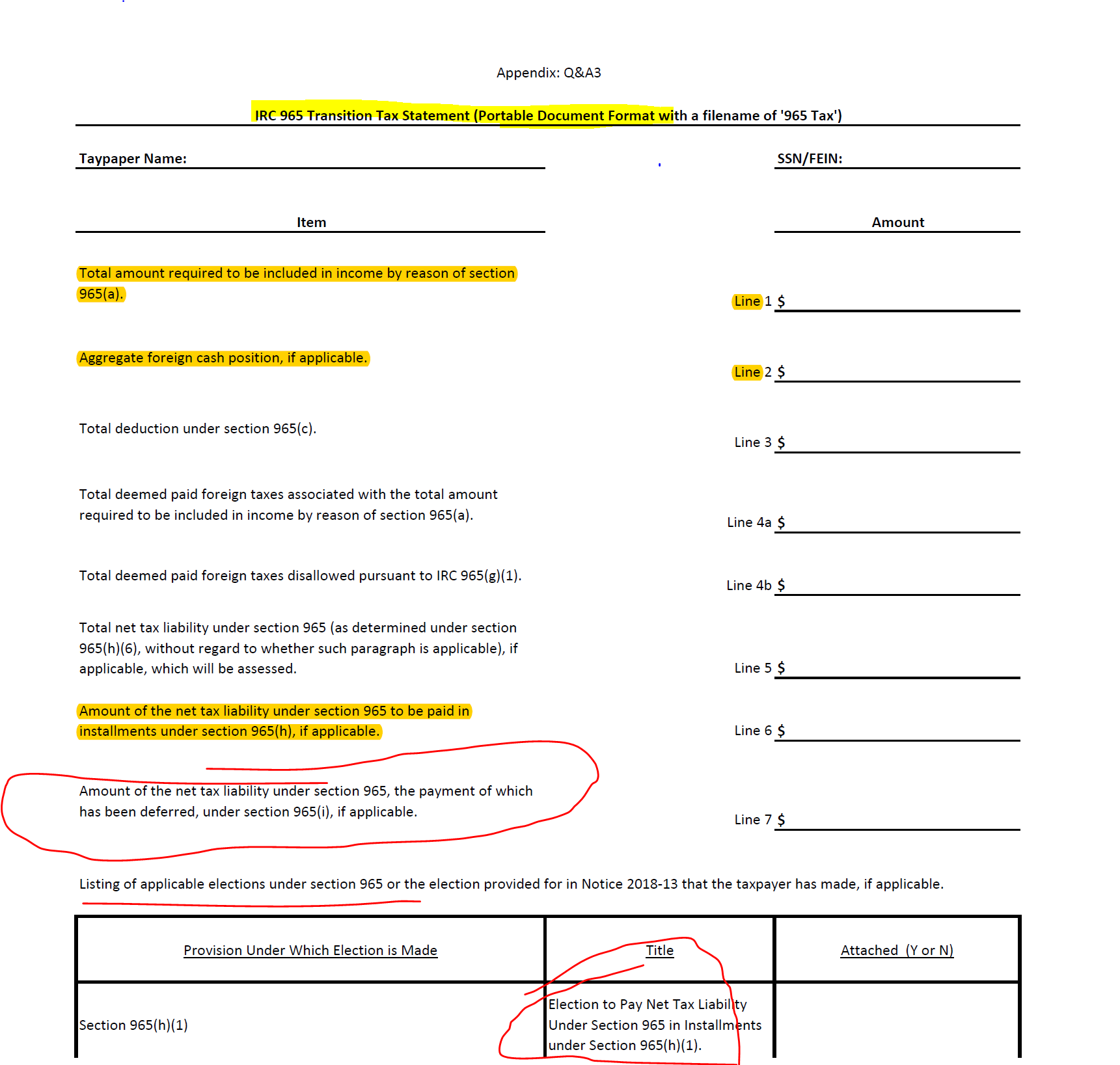

Third, the statute allows the taxpayer to make a timely election (under Section 965(h)(1)) to defer the payment of the tax over many an eight (8) year period as follows:

There are no circumstances where a USC would not want to defer the payment of the tax over time? Why pay for something today, when you can pay it tomorrow without an interest carrying charge?

For instance, if the total 965 Hammer/repatriation tax is US$200,000 for a USC, why would she not want to pay only 8% or US$16,000 in 2017/2018 and defer the rest of the US$200,000 tax payments over time?

The payments are “back-loaded” in later years and do not carry an interest charge.

Also, the IRS granted further relief for individuals who owe less than US$1M of 965 Hammer/repatriation tax. This relief allows the payment/deferral of the first installment otherwise due in 2017 until 2018 (and will not trigger the full amount immediately due), provided all of the following are satisfied:

- a timely election under Section 965(h)(1) needs to have been made, which is typically extends the return due date until October 15, 2018 (USCs residing outside the U.S., the extension due date was June 15th, 2018 and requires the filing of a specific automatic extension form (IRS Form 4868) by that date); and

- pays the first installment by the due date of of the 2017 tax return, without regard to extensions (which will typically be June 15th, 2018 provided the USC is residing overseas).

Bottom line: a USC who has timely filed an extension to file their IRS Form 1040 individual income tax return by June 15th, still has time to timely file the election under Section 965(h)(1) to defer the payment of the 965 Hammer/repatriation tax.

Incidentally, the Treasury published proposed regulations at the beginning of last month on Section 965 – Treasury Announces Guidance on One-Time Repatriation Tax on Foreign Earnings

The “965 Hammer” (aka the “Transition” or “Repatriation” Tax) for USCs Residing Overseas

Small businesses around the world commonly operate through companies established in their country of operation. According to the U.S. Tax Foundation, with admittedly outdated information from the year 2014, there were 1.7 million traditional C corporations, compared to 7.4 million partnerships and S corporations; even more sole proprietorships operating in the U.S.

I could not find similar data for other countries around the world, which is where Section 965 takes us.

USCs who live outside the U.S. and operate a business through a corporate entity in their country of residence (e.g., Canada, Mexico, UK, France, South Africa, Japan, Brazil, Hong Kong, Sweden, etc.) can be shocked when they learn how the new tax provision of IRC Section 965 works.

People read about the Administration and Congress’s goal to tax mega-technology companies such as Google, FaceBook, Microsoft and the like on their accumulated overseas profits in low tax jurisdictions. See, for instance, U.S. companies will pay billions in tax on offshore cash piles from CNN Money (by Alanna Petroff) and Apple Leads These Companies With Massive Overseas Cash Repatriation Tax Bills from FORTUNE (by Lisa Marie Segarra, January 18, 2018).

Hence, new IRC Section 965 imposes a one-time mandatory repatriation tax on accumulated earnings and profits of foreign corporations. The tax is paid by the U.S. shareholder. This makes policy sense, if the goal is to tax U.S. based taxpayers, especially mega companies with billions or 100s of millions of dollars of offshore un-taxed cash. In the past, much of these offshore profits could avoid U.S. taxation indefinitely as long as they were not actually repatriated in the form of dividends to the U.S. shareholder(s).

However, most people at the time were not expecting that this same repatriation tax would befall USCs living overseas arising from their local business operations.

Probably Congress and the Administration did not contemplate the fallout to these USC taxpayers. They were focusing on a different group of taxpayer. Nevertheless, Section 965 imposes immediate U.S. individual taxation on the “phantom income” (i.e., when no dividends are distributed to the USC shareholder) of the USC shareholder.

The next few posts will be dedicated to trying to explain in plain English how the “965 Hammer” (as I am affectionately calling it) applies to USCs residing in their home country with a business or investment assets held in a corporation.

The due date under the statute for paying this 965 tax has “come and past”; however, the IRS has granted certain extensions of time. These will be discussed in subsequent posts.

Importantly, a timely election under Section 965(h)(1) must be made by the due date (including extensions) for filing the return for the relevant year. For USCs residing outside the U.S., that due date was June 15th, 2018 and hopefully all USCs filed an automatic extension (IRS Form 4868) by that date, which would extend your due date to October 15, 2018 and the time to file the 965(h)(1) election.

Q&A 16 of the IRS website (Questions and Answers about Reporting Related to Section 965 on 2017 Tax Returns) addresses key provisions here –

Q16: If an individual fails to timely pay his or her first installment of tax due under section 965(h), will the IRS assess an addition to tax for failure to pay? Will the taxpayer’s requirement to pay all subsequent installments be accelerated under section 965(h)(3)?

. . . However, the IRS has determined that, if an individual’s net tax liability under section 965 in the individual’s 2017 taxable year is less than $1 million, the individual makes a timely election under section 965(h), and the individual did not pay the full amount of the first installment by the due date under section 965(h)(2), the failure to make the payment will not result in an acceleration event under section 965(h)(3) so long as the individual pays the full amount of the first installment (and its second installment) by the due date for its 2018 return (determined without regard to extensions). . .

A USC’s extensions and elections are very important here. A later post will explain how a USC residing outside the U.S. can obtain an additional extension at the discretion of the IRS. This can extend the due date of the 2017 income tax returns (IRS Form 1040) from the extended October 15th date to a further extended date of December 15th, 2018; for which the 965 election must be correctly made by the USC individual shareholder of a non-U.S. corporation.

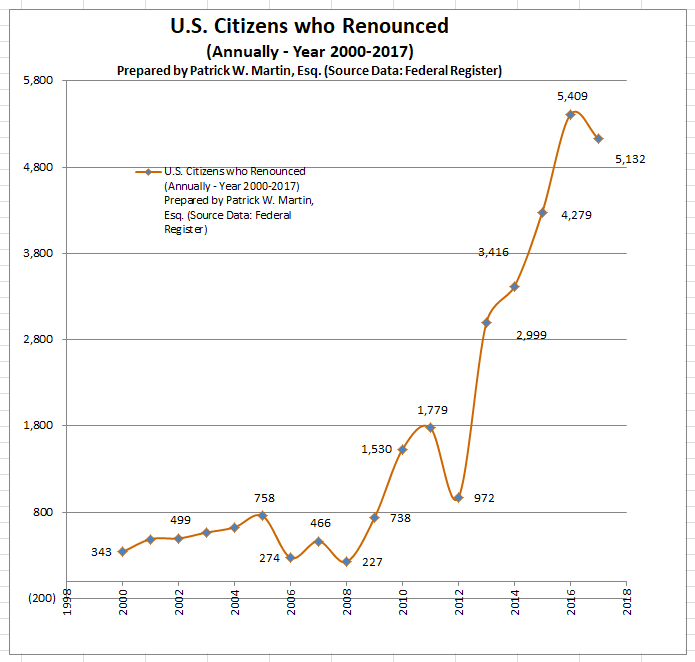

Why have U.S. Citizenship Renunciation Numbers Plateaued?

The number of U.S. citizens who have renounced has plateaued starting in 2016. That was the peak year with 5,409 renunciations followed by a similar number of 5,132 in 2017. See an older 2014 post that highlighted the then record of 2,999 for the entire year.

2017. See an older 2014 post that highlighted the then record of 2,999 for the entire year.

The 2014 Third Quarter Renunciations Is probably the New Norm –

The data used for these running compilations, with the individuals names published can be reviewed on the federal government’s website. The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications. Quarterly Publication of Individuals, Who Have Chosen to Expatriate

The total number of renunciations for the first two quarters of 2018 was 2,185.

None of this answers why these numbers have stopped increasing in a ski slope fashion?