Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

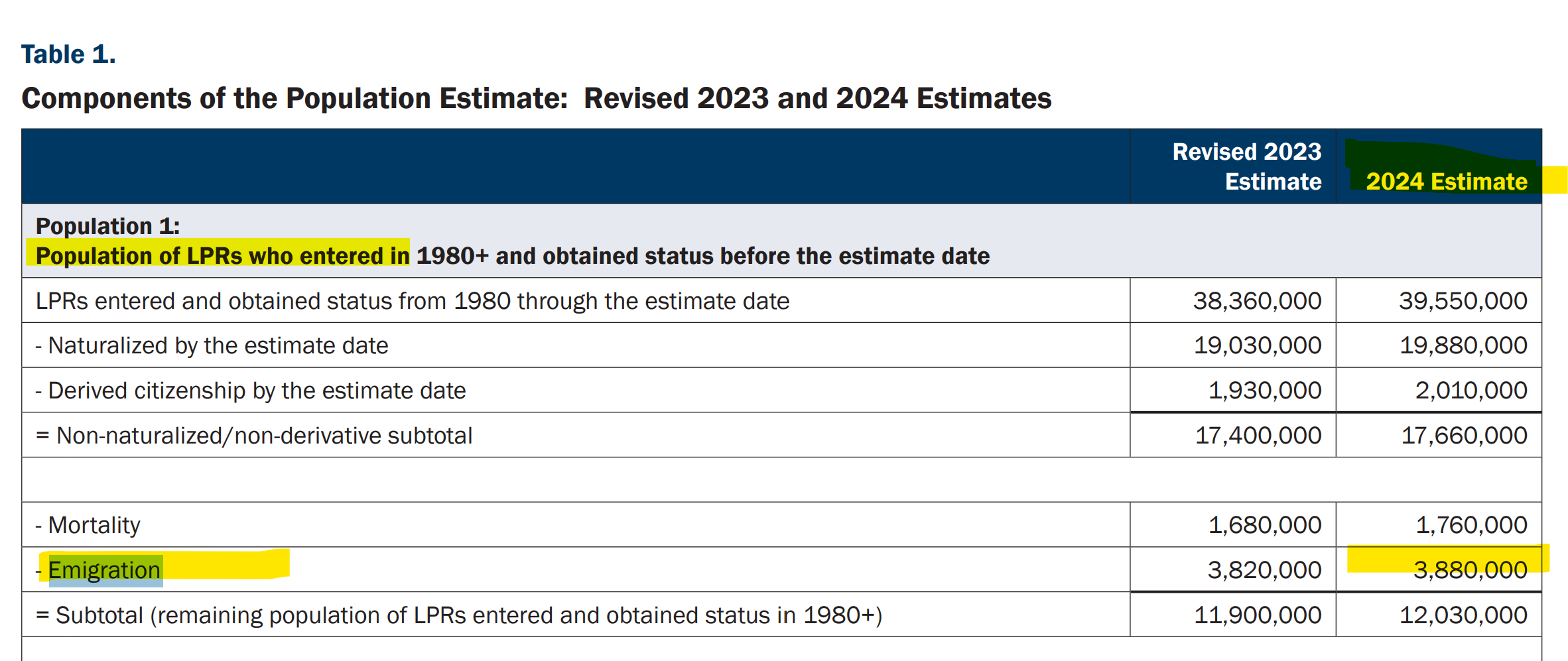

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

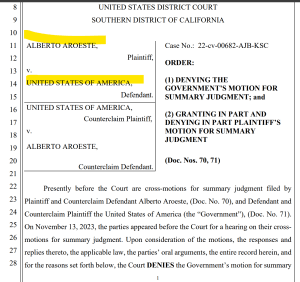

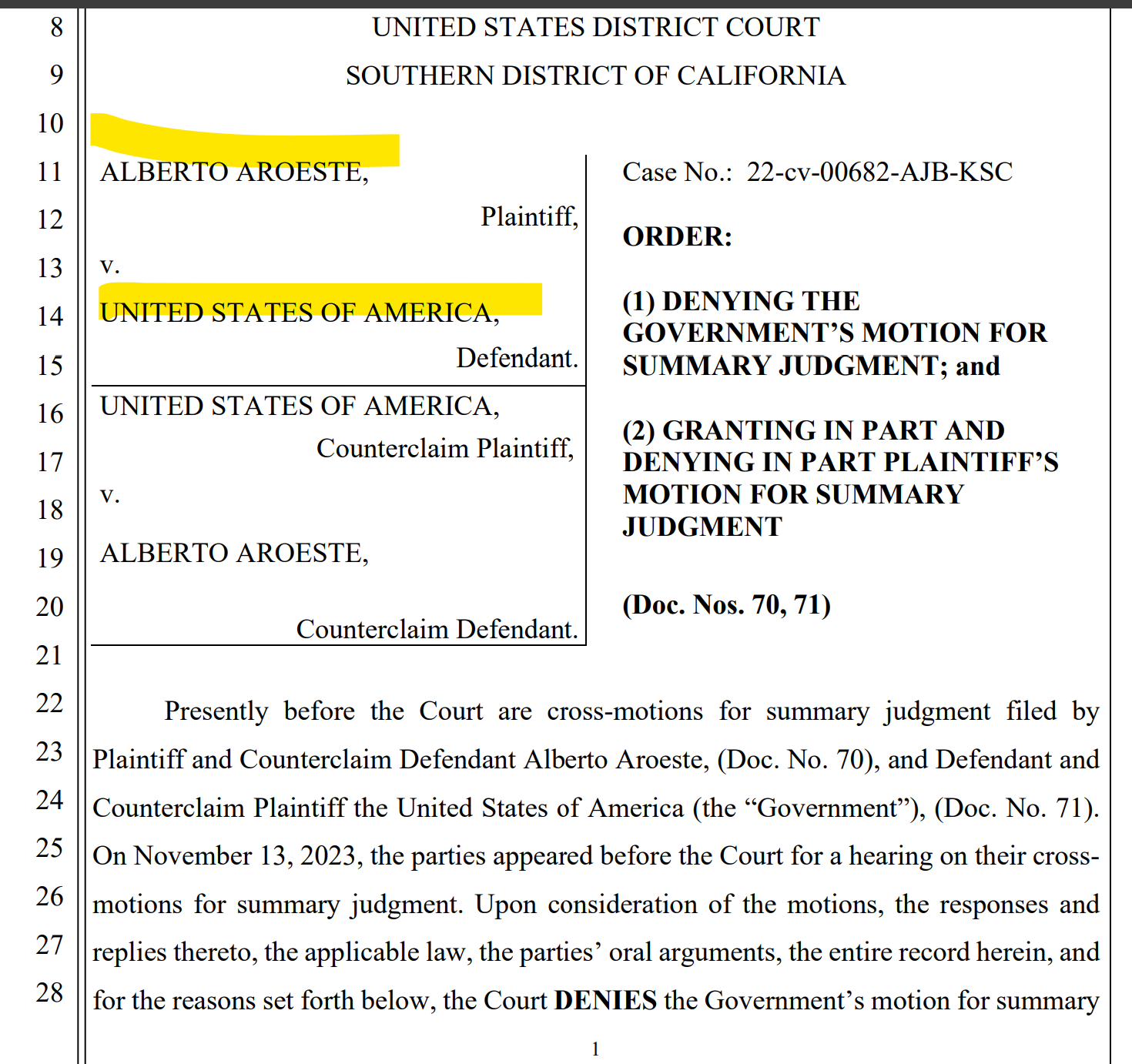

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Does TIGTA have the Answer: to the Question – How many former U.S. citizens and long-term lawful permanent residents have filed and should have filed IRS Form 8854?

The short answer to the question above – is NO!

The government does not know how many IRS Forms 8854 should have been filed.

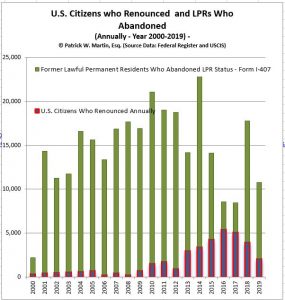

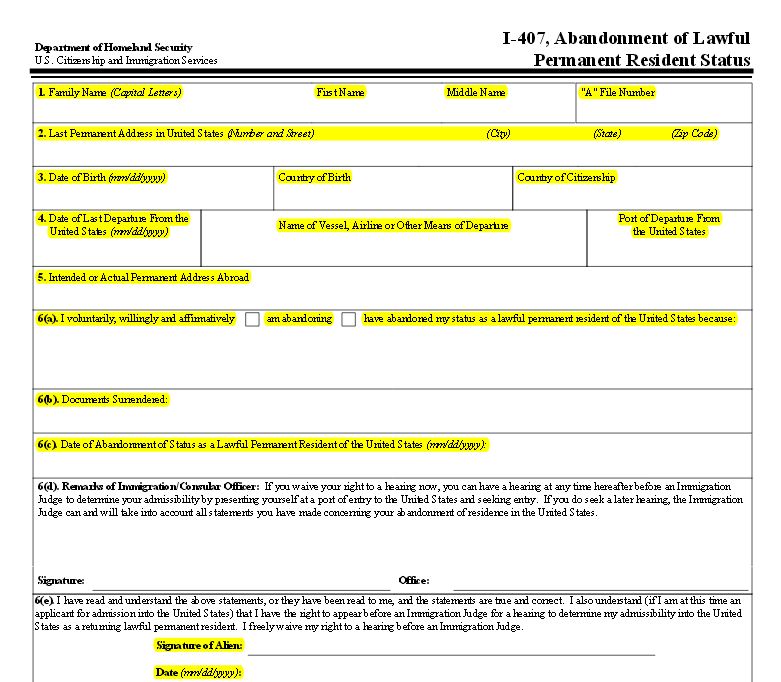

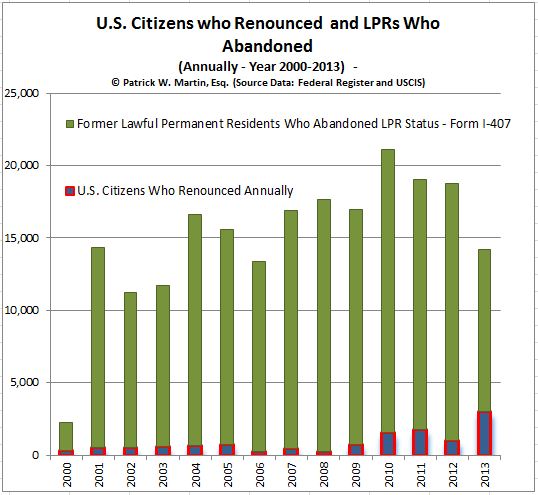

Note the total numbers of 8854 returns filed as reported in Figure 2 of the TIGTA Report were less than 25,000 during a ten year period. This report focuses really only on former U.S. citizens (“USC”) who have renounced their citizenship. Not on lawful permanent residents (“LPRs), which during that same ten year period there were around 200,000 who filed USCIS Form I-407.

* How Many Individuals Should have Filed Form 8854?

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

“LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – BIG GAP with Actual Emigration of LPRs

Millions of lawful permanent residents (LPRs) who have left the U.S. and not “formally abandoned” their LPR status (by filing Form I-407, Record of Abandonment of Lawful Permanent Resident) typically remain in some kind of “LPR U.S. tax limbo.” How many individuals worldwide are in this LPR U.S. tax limbo?

Why are these numbers important for the tax-expatriation analysis? See, a recent post, Why Most LPRs Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets (Part I). Indeed, most individuals probably do not think they are a U.S. federal income tax resident when they leave the U.S. to reside overseas back to their home country. Why would they? There is no tax training manual provided to LPRs who leave the U.S. and no tax advisories – reflected on the card itself (unlike the last page of the U.S. passport, paragraph D). More precisely, most are probably not giving much, if any thought, to the complex U.S. federal tax residency rules and their extraterritorial application.

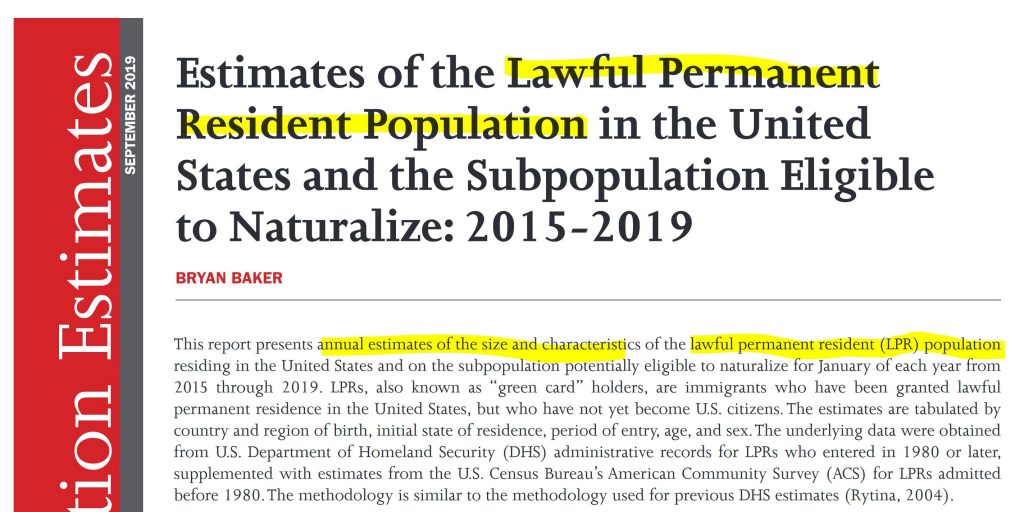

The “big gap” referred to above can be identified from the the Office of Immigration Statistics (OIS) report titled: Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year. Between naturalization, mortality and emigration the report shows that the LPR population, year over year, has remained stable. In 2019 the total number of LPRs per this report was 13.6 million, up from just 13.0 million in 2015.

The “gap” is the difference between the numbers of LPRs who have left-emigrated the U.S. (some 3+ million) compared to something like an annual average of 15-19 thousand who have filed Form I-407. The gap is in the millions of persons who are in LPR U.S. tax limbo.

Mexico

The report is also worth reading if you want to understand the demographics of the LPR population. Mexico has about 2.5 million (which is by far the greatest number) of the total 13+ million LPR population.

As the report points out there is no reliable direct measurements of LPR emigration. They do not exist. This lack of information is what drove me to file a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

The information I obtained in the FOIA response was surprising, since the government had records showing only 46,364 Forms I-407 were filed in the years 2013 through 2015, as follows:

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

This represents an average of only 15,455 individuals who formally abandoned their LPR status. Contrasted with more than 3.6 million estimated to have emigrated in 2019 per the DHS report leaves a massive gap of well over 3 million persons who held a “green card” and have left. They are now in LPR U.S. tax limbo.

What about the tax consequences? How many of these LPRs who left the U.S. know, understand or have any idea whatsoever of the federal tax filing obligations regarding their status?

What is the takeaway from the DHS report and LPR – I-407 information provided to me by the FOIA response? There is a discrepancy in the millions of people. Millions of individuals who actually leave or have left the U.S. to reside somewhere else around the world; compared to only some tens of thousands of individuals who have formally filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

What can these individuals do to get out of the LPR U.S. tax limbo?

The automatic exchange of bank and financial information is driven by the U.S. Treasury driven Intergovernmental Agreement (IGA).

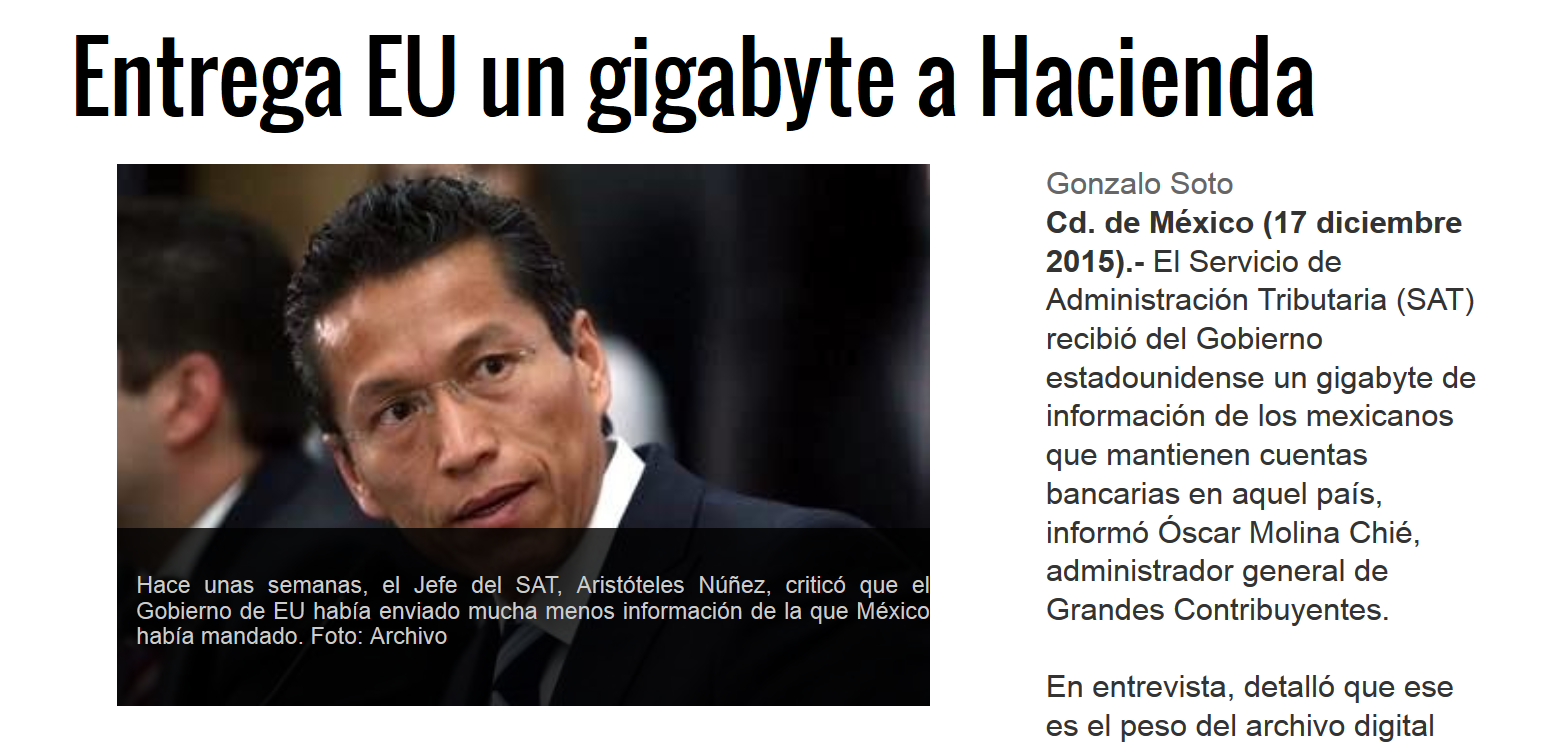

As a follow-up, the Mexican newspaper Reformareported on the 17th of December that the U.S. just provided Mexico’s treasury with a gigabyte of Mexican taxpayer information regarding U.S. financial and bank accounts. See, Entrega EU un gigabyte a Hacienda, dated Dec 17, 2015.

This news comes on the heals of the earlier criticism by the Commissioner of the Mexican IRS (SAT – Servicio de Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reformaarticle quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Finally, the article emphasized that Mexico has sent the IRS information regarding Mexican bank accounts of U.S. citizens.

No one knows for certain if the IRS (including the IRS per some of my conversations) is getting complete data from the Department of State regarding each name and individual.

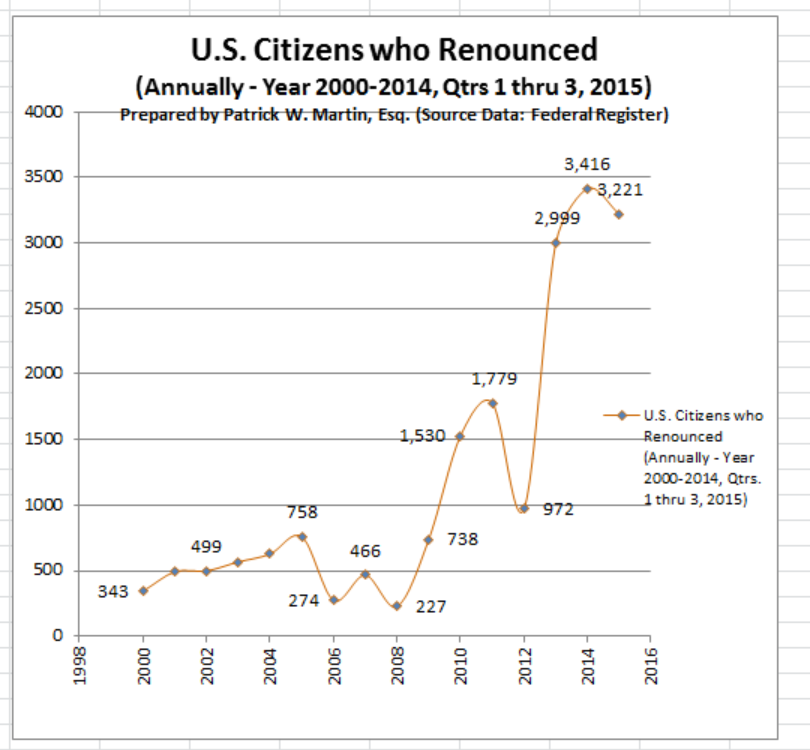

The graph I have prepared shows the number of names reported quarterly as I track all reported names quarterly that related to clients and non-clients. The latest cumulative amounts for 2015 (which does not include the 4th quarter) shows 3,221 thus far in the year. If there is close to 1,400 as was the case for the last quarter, the total will be a record – by a bunch; i.e., close to 5,000 renunciations for the year.

None of this answers the question of whether there is under-reporting of the names? Indeed, the question will likely not be answered without more information provided by the U.S. Department of State and the U.S. Treasury (i.e., the IRS officers responsible for issuing the names and report in the Federal Register).

The government is also likely to reject issuing information on these details to individuals and their advisers as part of a Freedom of Information Act (“FOIA”) request. I have had similar requests rejected by the government under the so called “Exemption 7(E)” of FOIA. See,

In addition, the second quarter saw a total of 460, for a cumulative total for the year (mid way through the year of 1,795). At this pace, the year 2015 could be a slight record of U.S. citizenship renunciations compared to the record year of 2014.

The names of each citizen can be located in the list published in the Federal Register.

There are a number of key considerations and strategic decisions that most all U.S. citizens need to consider prior to renouncing citizenship. See, for instance –

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms are set forth here. The new form requires the address overseas of the individual.

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

“mark to market” taxation on their worldwide assets,

40% inheritance tax to U.S. beneficiaries,

40% tax on gifts to U.S. beneficiaries,

etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”

Ms. Saunders writes thoughtfully on the subject of taxation and U.S. citizens who have renounced citizenship.

*

Her most recent article has a number of excellent observations, including the following regarding an academic study of those citizens living abroad:

According to a recent survey of 1,546 U.S. citizens and former citizens living abroad, 31% of participants have actively considered renouncing their U.S. citizenship and 3% are in the process of doing so. Many who were considering the move cited increasingly onerous and intrusive financial reporting requirements. The survey was conducted between Dec. 5 and Jan. 20 by Amanda Klekowski von Koppenfels, a researcher at the University of Kent in the U.K.

For other articles written by Ms. Laura Saunders, on this related subject, see the Media: News & Articles section –

The Number of Citizens Leaving (Renouncing) Versus Coming (Naturalizing) is Just a Speck

Much has been made about the number of citizens who have been renouncing their U.S. citizenship over the last few years. In historical terms, it is a relative explosion. See, earlier post – The 2014 Third Quarter Renunciations Is probably the New Norm –

However, the number of individuals who wish to come to the U.S. to become citizens is far in excess of the number who are renouncing their citizenship. According to the USCIS, there are about 700,000 individuals annually who become naturalized citizens. In the year 2008, there were more than 1 million naturalized citizens. See table:

Compare these numbers to just about 3,000 annually of individual who are renouncing their citizenship.

Of course, everyone has their own story and reasons for either coming or going, but in relative terms, those who find it desirous to renounce citizenship (at least in absolute numbers and relative terms) represent a small speck (less than 1/2 of 1 percent), compared to those who are becoming naturalized citizens.