International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

What Tax Forms Do US Citizens and Green Card Holders Living Abroad Need?

Living outside the United States does not eliminate your US tax obligations. US citizens and green card holders abroad must file a US tax return every year and may also need to file additional reports on foreign assets and accounts. Here is an overview of the key forms, what they cover, and how they interact.

Is my foreign income automatically exempt from US reporting?

No. A common misconception is that foreign income is exempt because it can be excluded. Foreign earned income is not exempt. You must report it on a US tax return, and you must be a qualifying individual to elect the exclusion.

What types of income qualify for the exclusion on Form 2555?

The exclusion is available only for “earned” income. It cannot be used for passive investment income such as dividends, interest, or capital gains.

Foreign Tax Credits (FTC)

How does a Foreign Tax Credit work?

A Foreign Tax Credit provides a dollar-for-dollar reduction, subject to limitations, of your US federal tax burden for income taxes you paid to another country on income sourced there. It is claimed on Form 1116.

Can I claim both the FEIE and the Foreign Tax Credit?

No. Once you choose to exclude foreign earned income or housing costs, you cannot take a foreign tax credit on that same income. If you do take the credit, your previous choice to exclude that income may be treated as revoked.

Are there different forms for lawful permanent residents (LPRs)?

US citizens and LPRs generally use Form 1040. However, LPRs residing in a country with a US income tax treaty may be eligible to file Form 1040NR as a non-resident.

Information Reporting and FBAR

What is Form 8938?

Form 8938 (Statement of Specified Foreign Financial Assets) is used to report specified foreign financial assets. It often overlaps with FBAR reporting and must be attached to your annual income tax return when filed with the IRS.

Who must file an FBAR (Form 114)?

US citizens and LPRs with a financial interest in or signature authority over foreign accounts must file a Foreign Bank Account Report (FBAR). The definitions of “ownership interest” and “signature authority” are interpreted very broadly under the regulations.

Where is the FBAR filed?

Unlike other tax forms, the FBAR is not filed with the IRS. You must file it electronically with FinCEN (the Financial Crimes Enforcement Network) through the BSA E-Filing System on Form 114.

What are the penalties for FBAR non-compliance?

The statutory penalty for failing to file, or filing late, is $10,000 per failure. If the failure to file was intentional, the penalty can increase to 50% of the account balances.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

Tax Preparation Software

Can I use standard tax software for these international forms?

Often, no. Most tax preparation software does not support Form 8938 or other forms related to non-US assets. These forms frequently require manual completion using an Adobe Acrobat version of the form.

Not everyone who renounces US citizenship faces the same tax consequences. People who qualify as “covered expatriates” face significant additional obligations. Here is what that means and how even modest individuals can end up in this category.

One of the greatest risks for anyone who wants to give up US citizenship is Section 877(a)(2)(C). Even the most economically modest individual, with little assets or income, can fall into this trap. No one at the US Department of State will provide tax advice or interpret Section 877(a)(2)(C) for you. The renunciation appointment itself is straightforward. The tax consequences are not.

What are the three tests for covered expatriate status?

Under Section 877(a)(2), you are a covered expatriate if any one of the following is true:

(A) Your average annual net income tax liability is greater than $124,000;

(B) Your net worth is $2,000,000 or more as of your expatriation date; or

(C) You fail to certify under penalty of perjury that you have met all US tax requirements for the 5 preceding taxable years, or fail to submit the required evidence of compliance.

Any individual who meets any one of these tests will be a covered expatriate and subject to the taxation and reporting requirements under Sections 877, 877A, and 2801.

What happens at the embassy or consulate?

When you take the renunciation oath at a US embassy or consulate, the Foreign Affairs Manual provides only standard overview language about “special tax consequences.” The consular officer will not explain the specific rules of Section 877(a)(2)(C) or tell you whether you will be a covered expatriate. This is worth understanding well before going to take the oath.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Why Long-Term Green Card Holders Cannot Escape the Exit Tax Rules

When long-term green card holders give up their green card, they face the same exit tax rules as US citizens who renounce citizenship. There is one exception in the law that allows certain dual citizens by birth to avoid covered expatriate status even if they meet the income or asset tests. Long-term green card holders cannot use it. Here is why.

When you give up your green card (or renounce US citizenship), the law determines whether you are a covered expatriate. You are a covered expatriate if you meet any one of three tests: an average annual income tax liability above an inflation-adjusted threshold, a net worth of $2 million or more on the date of expatriation, or a failure to certify 5 years of US tax compliance – where it is commonly certified on IRS Form 8854.

Meeting even one of these three tests makes you a covered expatriate. All three tests apply equally to US citizens who renounce and to long-term lawful permanent residents (LPRs) who give up their green card.

Is there an exception to the income and asset tests?

Yes, for some people. Under IRC Section 877A(g)(1)(B), certain individuals are exempt from the income and asset tests. If this exception applies to you, you can avoid covered expatriate status even if your net worth exceeds $2 million or your income exceeds the threshold. The certification requirement under Section 877(a)(2)(C) still applies to everyone, including those who qualify for this exception.

Who can use this exception?

The exception is narrow. Under the statute, it applies only to an individual who: became a citizen of the United States and a citizen of another country at birth; as of the date of expatriation, continues to be a citizen of and is taxed as a resident of that other country; and has been a US resident for no more than 10 taxable years during the 15-year period ending with the taxable year of expatriation. Only someone who acquired US citizenship automatically at birth, while also holding citizenship of another country from birth, can potentially qualify.

Why green card holders cannot use it

Lawful permanent residents are not US citizens. They hold a green card, which is a grant of permanent resident status, not citizenship. Because the exception in Section 877A(g)(1)(B) applies only to individuals who became US citizens at birth, long-term LPRs cannot satisfy this requirement by definition. The exception is simply not available to them.

What this means if you are a long-term green card holder

A long-term LPR who meets either the $2 million asset test or the income tax liability test will become a covered expatriate, even if they fully satisfy the 5-year certification requirement. Satisfying the certification requirement is necessary for everyone, but for long-term LPRs it is not sufficient on its own. If you also meet the income or asset test, you are a covered expatriate regardless.

The consequences include the mark-to-market exit tax on unrealized gains and the Section 2801 tax on covered gifts and bequests to US persons. These consequences can affect your US family members for decades. Understanding them well before you give up your green card, not after, is the only way to plan for them.

There are important unintended tax consequences that can befall individuals who have a green card depending upon their factual circumstances: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9):

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Green Card Holders (Abandonment) – so Many More than U.S. Citizens who Renounce: The Topsnik Problem(s)!

I have previously written (pre-Aroeste v. United States) about the thorny issues that LPRs face when spending substantial time outside the United States. See an earlier post titled:

I highlighted some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law and now the case law in Aroeste makes these risks clear as confirmed in the landmark case.

A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particular case.

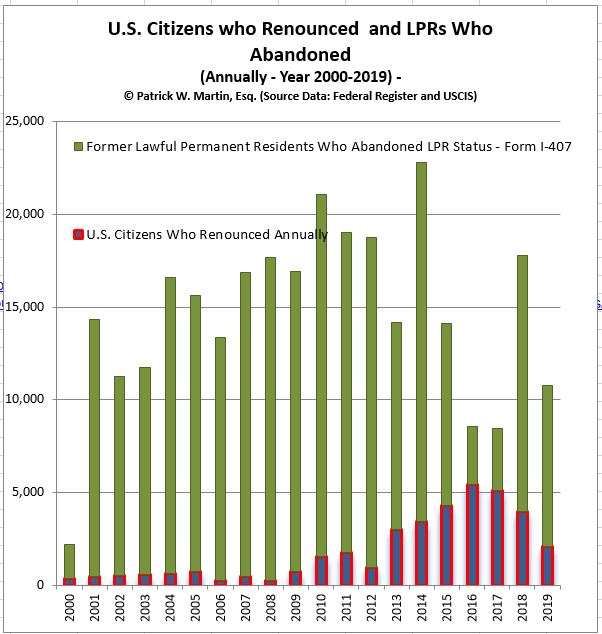

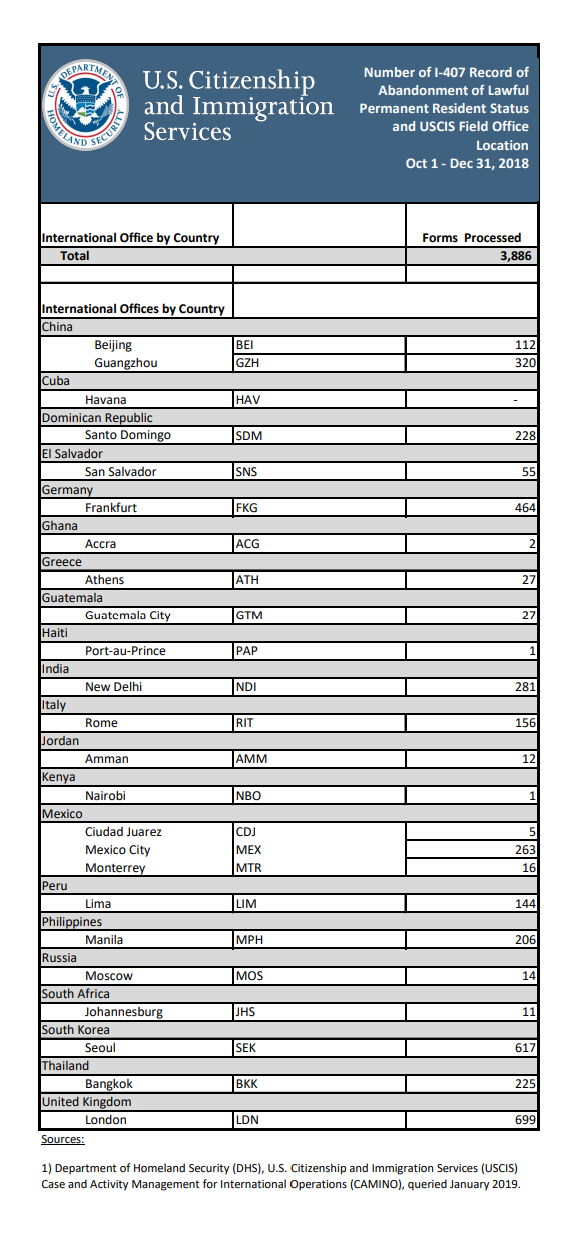

There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

* More Green Card Holders Abandon Status Than Citizens Renounce Citizenship

A frequently overlooked fact is that:

Formal Abandonment of LPR Status Is More Common Than Citizenship Renunciation

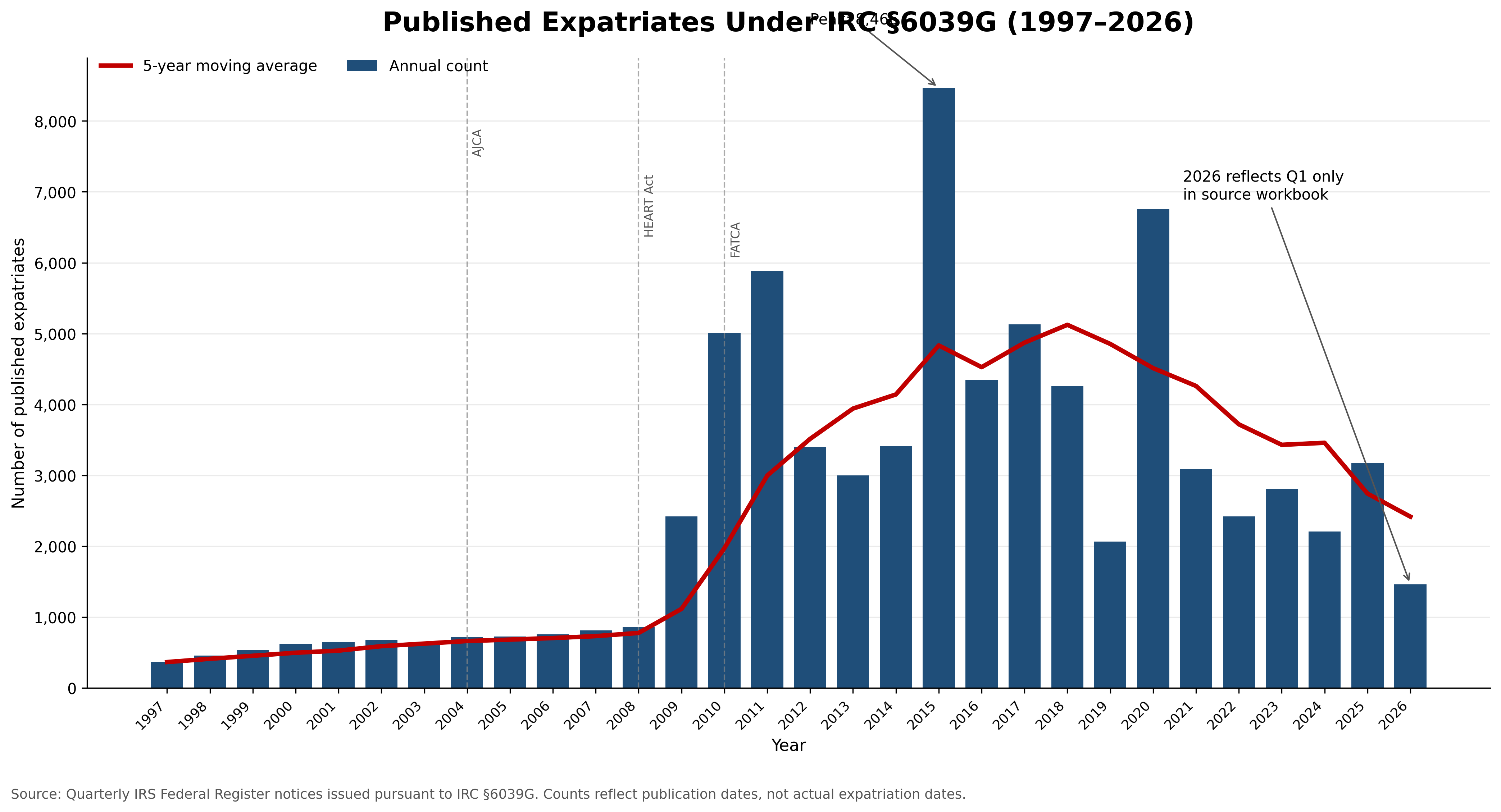

Each year, substantially more lawful permanent residents formally abandon their green cards than U.S. citizens formally renounce citizenship. The focus in the press and media is typically U.S. citizens who formally renounce. Here is my most recently compiled graph, the total number of U.S. citizens renouncing is typically in the thousands (few) each year. It has trended downward post-COVID.

However, with LPRs, formal recognition of abandonment by filing Form I-407 (not including informal abandonments which are multiple times greater) is multiple times greater.

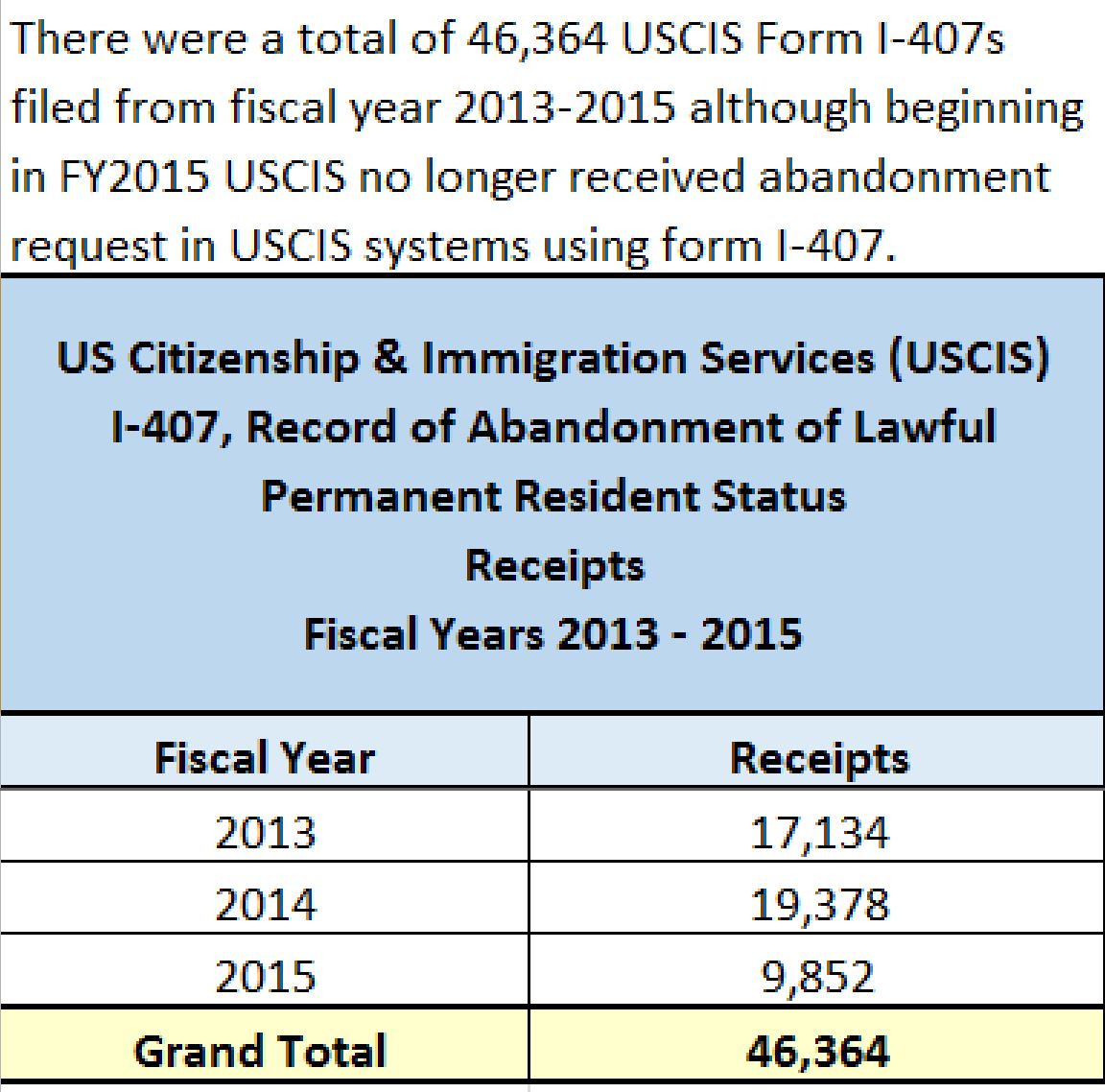

The graph I created several years ago, shows that formal LPR abandonments are mlutiple times greater than citizenship renunciation. I made a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

I have made a new FOIA request for more recent records, since this data is no longer public after the year 2019 year.

The statistics reflected above demonstrate that:

Formal green card abandonment significantly exceeds formal citizenship renunciations.

The population potentially affected by the expatriation rules is therefore much larger than many individuals around the world appreciate.

Lack of Control Over the Timing of Termination

One of the greatest risks for green card holders is that they often do not control the legal date on which their LPR status terminates, especially if they reside in a tax treaty country, per the analysis in the landmark case:

If abandonment is later determined by tax treaty law, effectively an CPB officer, the Executive Office for Immigration Review (EOIR) immigration court, the Board of Immigration Appeals (BIA)or a even a Federal District Court:

The taxpayer may not control the effective date of termination – “expatriation”.

If they are a “covered expatriate” or not.

The tax consequences may arise unexpectedly.

The timing can directly impact whether the tax expatriation rules apply and all of the potential consequences.

These timing issues become important when the IRS challenges tax positions taken on tax returns filed (or filed late) as was the case in Topsnik v. Commissioner (143 T.C. 240 (2014) – “Topsnik I”) and the subsequent case of Topsnik v. Commissioner (146 T.C. No. 1, 2016) – “Topsnik II”). In Topsnik II, Judge Kerrigan agreed with the IRS and ” . . . determined that P [taxpayer] was a “covered expatriate” who expatriated in 2010 and must recognize gain on the deemed sale of his installment obligation on the day before his expatriation under I.R.C. sec. 877A.” The U.S. Tax Court cited IRS Notice 2009-85 and explained it was not legally binding as follows:

We are not bound by Notice 2009-85, supra, see Compaq Computer Corp. v. Commissioner, 113 T.C. 363, 372 (1999), but it is an official statement of the Commissioner’s position and we may let it persuade us, see Nationalist Movement v. Commissioner, 102 T.C. 558, 583 (1994), aff’d, 37 F.3d 216 (5th Cir.1994).

The Tax Court went on to conclude these facts caused the court to conclude and uphold the IRS assessment of the “exit tax” on the German citizen Mr. Topsnik as a “covered expatriate” quoted as follows:

Notice 2009-85, sec. 8, 2009-45 I.R.B. at 611, explains that for purposes of certifying tax compliance for the five years before expatriation pursuant to section 877(a)(2)(C):

All U.S. citizens who relinquish their U.S. citizenship and all long-term residents who cease to be lawful permanent residents of the United States (within the meaning of section 7701(b)(6)) must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation. Individuals who fail to make such certification will be treated as covered expatriates within the meaning of section 877A(g) * * *

For the year of his expatriation petitioner failed to complete and file a Form 8854 certifying under penalties of perjury that he has complied with all of his U.S. Federal tax obligations for the five taxable years preceding the taxable year that includes his expatriation date. Respondent [IRS] has provided evidence that petitioner did not file all of his U.S. income tax returns before expatriatingand was not in payment compliance for taxes owed for the five years before expatriation in taxable year 2010. Thus petitioner could not have certified under penalties of perjury on a Form 8854 that he had been in tax compliance for the five years before expatriation. Consequently, because petitioner failed to certify tax compliance for the five years before expatriation, he is a “covered expatriate” as defined by section 877A(g)(1)(A).

Importantly, the court in Aroeste concluded IRS Form 8854 was not required to be filed (even though the DOJ attorney argued it was required – as set forth in the instructions to the form) as explained below:

C. Whether Aroeste Was Required to File Form 8854

The Government next argues that even if the IRS had accepted Aroeste’s amended

returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009- 85.(Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both

amended forms. (Id.)

Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply

with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley

Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under

the APA, agencies must follow a three-step procedure for “notice-and-comment”

rulemaking, but this requirement does not apply to “interpretive rules, general statements

of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In

Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found

that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure.

Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Both the Green Valley Investors LLC case and Mann Construction were 2022 cases, some 6 years after Topsnik II.

My law firm, Chamberlain Hrdlicka, successfully represented the taxpayers in Green Valley and of course in Aroeste.

Practical Lessons for Green Card Holders

The combined lessons from Aroeste, Topsnik I, and Topsnik II are significant.

Before Obtaining a Green Card

Individuals should understand:

The long-term resident rules and their U.S. tax obligations and reporting obligations;

The expatriation tax provisions and how they generally apply;

The “covered expatriate” tax regime and what steps to take;

The impact of income tax treaties with countries in the United States.

Before Formally Reporting the Abandonment (or Informally Abandoning) a Green Card

Individuals should carefully evaluate:

The date expatriation may occur;

Whether Form I-407 should be filed;

Tax compliance under U.S. tax laws (and what that means), including for the preceding five years to abandonment;

What notifications should be provided and when (not necessarily formal tax form filings);

Potential exit tax exposure – depending upon total assets, liabilities, type of assets and anticipated future income and gains;

Treaty residency positions and the particular facts of each case;

Reporting obligations, and which ones are mandatory or not – including IRS Forms 8833 and 8854.

Most Important Takeaway?

A green card holder does not necessarily need to spend seven or eight years physically living in the United States before becoming subject to the long-term resident and expatriation tax rules. The interaction of immigration law, tax law, treaty provisions, and reporting requirements can produce unexpected results. The recent landmark decision in Aroeste that I handled, confirms that these issues are not merely theoretical—they are increasingly becoming the subject of significant litigation and judicial scrutiny.

Quaint?: U.S. Treasury 1998 Report: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues (Part I of Part II)

This is a classic report that now reads quaintly.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties inUnited States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

What Questions Need to be Asked if You Live (with a “green card”) in one of the 67 Countries – with a U.S. Income Tax Treaty?

Depending upon the factual circumstances of each individual, they may be able to benefit from the international tax treaty law articulated by the U.S. Federal District Court in Aroeste v United States – Order (Nov 2023). Future posts will explore the legal relevance of some of the following questions to consider:

Has the individual filed any U.S. federal income tax returns since leaving the United States?

Was a professional tax return preparer hired or consulted about the filing of a federal income tax return (e.g., a certified public accountant, an enrolled agent, a full time tax return preparer, ta tax attorney, etc.)?

Has the individual been filing IRS Form 1040 Resident Tax Returns in the same way Mr. Aroeste was filing – based upon the advice (that turned out to be erroneous -although given in good faith) from their U.S. tax return preparer?

What steps if any have been taken to notify the U.S. federal government (irrespective of the agency) regarding their physical residency outside the United States?

This information is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

Countries From Which Viewers Read Posts – Tax-Expatriation.com – First Week of 2024 (Which Ones are Tax Treaty Countries?) – Applying the “Escape Hatch”

The whole idea of the “escape hatch” for tax treaties is an excellent way of explaining how and when tax treaty law applies in different circumstances. Importantly, the U.S. federal government cannot deny an individual (or presumably a company either) from properly applying the law of a tax treaty – even if they “gave [an] untimely notice of his treaty position “. See further comments at the end of this post and the District Court’s opinion here – Aroeste v United States – Order (Nov 2023). Meanwhile, see below the 22 countries from where global readers viewed Tax-Expatriation.comduring the first full week of 2024.

Below is the list of 22 countries (including the United States) from where readers hailed, who read Tax-Expatriation.comduring the first week of 2024. All, but Brazil, Croatia, Nigeria, the United Arab Emirates, Colombia, Kenya and Bermuda have income tax treaties with the United States.

This means that all other individuals are connected with the following 14 countries that have tax treaties with the United States:

Mexico

India

Canada

United Kingdom

Switzerland

Australia

China

Spain

Turkey

Germany

Japan

Romania

Portugal

Netherlands

Further, all individuals who might have never formally abandoned their lawful permanent residency (“green card”), maybe never filed specific IRS tax forms, and yet reside in one of these fourteen (14) treaty countries could be eligible for the application and the specific benefits of international income tax treaty law. This, along the lines of the decision in Aroeste v United States (Nov. 2023). In addition, there could be other tax treaty benefits applicable to those individuals in these fourteen countries depending upon where are their assets, what type of income they have, where does the income come from, and where do they reside.

The tax treaty rights discussed here are established by law, as elucidated by the Federal District Court in Aroeste v United States (Nov. 2023). The Court determined that the IRS cannot simply assert an individual’s ineligibility for treaty law provisions based solely on the failure to file specific IRS forms within the government-defined “timely” period. The Court emphasized that there is no automatic waiver of treaty benefits as a matter of law, while acknowledging: “. . . Aroeste gave untimely notice of his treaty position. . .” For specific excerpts from the opinion, please refer to the highlighted portions below. To access the complete opinion, please consult Aroeste v United States – Order (Nov 2023).

* * * * * * * * *

B. Whether Aroeste Did Not Waive the Benefits of the Treaty Applicable to Residents of Mexico and Notified the Secretary of Commencement of Such Treatment.

To establish Mexican residency under the Treaty, and thus avoid the reporting requirements of “United States persons,” Aroeste must have filed a timely income tax return as a non-resident (Form 1040NR) with a Form 8833, Treaty-Based Return Position Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2722 Page 8 of 17 9 22-cv-00682-AJB-KSC Disclosure Under Section 6114 or 7701(b). Indeed, Aroeste did not submit Form 8833 to notify the IRS of his desired treaty position for the years 2012 and 2013 until October 12, 2016, when he submitted an amended tax return for both years at issue. (Id.) The Government asserts that because Aroeste did not timely submit these forms, he cannot establish that he notified the IRS of his desire to be treated solely as a resident of Mexico and not waive the benefits of the Treaty. (Id. at 4.) The Government relies upon United States v. Little, 828 Fed. App’x 34 (2d Cir. 2020) (“Little II”), a criminal appeal in which the court held a lawful permanent resident of a foreign country was a “‘resident alien’ or ‘person subject to the jurisdiction of the United States’ with an obligation to file an FBAR.” Id. at 38 (quoting 31 C.F.R. § 1010.350(a), (b)(2)).

In response, Aroeste asserts that while he agrees with the Government that I.R.C. § 6114 requires disclosure of a treaty position, he disagrees as to the consequences for a taxpayer’s failure to timely file the disclosure. (Doc. No. 75-1 at 6.) While the Government asserts the failure to timely file Forms 1040NR and 8833 deprives individuals of the Treaty benefits provided, Aroeste argues instead that I.R.C. § 6712 provides explicit consequences for failure to comply with § 6114. Specifically, § 6712 states that “[i]f a taxpayer fails to meet the requirements of section 6114, there is hereby imposed a penalty equal to $1,000 . . . on each such failure.” I.R.C. § 6712(a). Based on the foregoing, Aroeste argues the taxpayer does not lose the benefits or application of the treaty law.1 (Doc. No. 75-1 at 6.) In United States v. Little, 12-cr-647 (PKC), 2017 WL 1743837, at *5 (S.D. N.Y. 1 Aroeste further asserts that published agency guidance, letter rulings, and technical advice support his position. (Doc. No. 75-1 at 7.) For example, in 2007, an IRS agent sought advice from IRS Counsel asking, “Do we have legal authority to deny a tax treaty because Form 8833 is not attached or the treaty is claimed on the wrong Form (1040EZ or 1040)?” Legal Advice Issued to Program Managers During 2007 Document Number 2007-01188, IRS. IRS Counsel responded, “No, you cannot deny treaty benefits if the taxpayer is entitled to them. You may impose a penalty of $1,000 under section 6712 of the Code on an individual who is obligated to file and does not.” Id. As to this, the Court finds it has no precedential value under I.R.C. § 6110(k)(3), which states that “a written determination may not be used or cited as precedent.” See Amtel, Inc. v. United States, 31 Fed. Cl. 598, 602 (1994) (“The [Internal Revenue] Code specifically precludes [plaintiff] and the court from using or citing a technical advice memorandum as precedent.”) Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2723 Page 9 of 17 10 22-cv-00682-AJB-KSC May 3, 2017) (“Little I”), a criminal case for the plaintiff’s willful failure to file tax returns, the court stated the plaintiff’s same argument “that the failure to take a Treaty position can result only in a financial penalty also lacks merit. 26 U.S.C. § 6712(c) expressly states that ‘[t]he penalty imposed by this section shall be in addition to any other penalty imposed by law.’” (emphasis added).

I have been consulted over the years by other taxpayers which are cited now as published decisions by the government and the Federal District Court (Southern District of California). These cases are referenced and cited in my own most recent case of Aroeste v United States (Nov. 2023).

However, in Little I, the plaintiff never attempted to take a treaty position. Next, in Shnier v. United States, 151 Fed. Cl. 1, 21 (2020), the court denied the plaintiffs’ claims for relief based on tax treaties because they failed to disclose a treaty based position on their tax returns pursuant to I.R.C. § 6114 “and did not attempt to cure this omission in their briefing[.]” Although the plaintiffs in Shnier were naturalized U.S. citizens who attempted to recover their income taxes under I.R.C § 1297, the court’s brief discussion of I.R.C. § 6114 in relation to a treaty-based position is instructive that an untimely notice of a treaty position does not bar the individual from taking such position. Moreover, in Pekar v. C.I.R., 113 T.C. 158 (1999), the court noted that a taxpayer who fails to disclose a treaty-based position as required by § 6114 is subject to the $1,000 penalty, but stated “there is no indication that this failure estops a taxpayer from taking such a position.” Id. at 161 n.5.2 The Court agrees with Aroeste.

Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

* * * * * * * * *

For individuals living in any of these 14 tax treaty countries (or any of the total 67 income tax treaty countries), the key takeaway is that, based on their specific circumstances, they might be eligible to leverage the international tax treaty principles outlined in the Aroeste v United States case (Nov. 2023). The forthcoming post will pose questions for consideration by the potentially millions of individuals affected by these rules of law.

Federal District Court Rules in Favor of Mexican Citizen – Aroeste vs. United States (LPR) – Tax Treaty Applies: Government’s Motion for Summary Judgment is Denied

Last week (Nov. 20, 2023), Judge Battaglia in the Southern District of California (San Diego) ruled in favor of our client Mr. Alberto Aroeste regarding the application of the U.S.-Mexico Tax Treaty. The DOJ, Tax Division arguments on behalf of the Internal Revenue Service in the case (and their Motion for Summary Judgment – MSJ) were largely rejected by the Court.

A thorough read of the Order from the Court is recommended to understand the substantial legal findings and legal analysis made by the Court relevant to those who possess a “green card” referred to as “lawfully admitted for permanent residence” in Title 8, § 1101(a)(13) [Immigration and Nationality Act]. Key to this case, Title 26, § 7701(b)(6) [Federal Tax Code] then rather contorts the concept by saying an individual is a “lawful permanent resident” in accordance with immigration laws; but then goes on to put conditions on who apparently is a “lawful permanent resident” for federal tax purposes. While immigration law requires the individual be ” . . . accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed”; the tax definition seems to ignore that status (i.e., has it changed and is the personal no longer accorded the privilege of residing permanently in the U.S.?).

The Board of Immigration Appeals (the “Board”), has long recognized that an alien’s status may change by operation of law, such that an alien may abandon his LPR status without a finding of removability (or, formerly, deportability or excludability) after a formal adjudicatory process. See United States v. Yakou, 428 F.3d 241, 247 (D.C. Cir. 2005); at 247-51 (discussing case law regarding abandonment and holding that an alien may abandon LPR status without formal administrative action); see also Matter of Quijencio, 15 I. & N. Dec. 95 (B.I.A. 1974); Matter of Kane, 15 I. & N. Dec. 258 (B.I.A. 1975); Matter of Muller, 16 I. & N. Dec. 637 (B.I.A. 1978); Matter of Abdoulin, 17 I. & N. Dec. 458, 460 (B.I.A. 1980); Matter of Huang, 19 I. & N. Dec. 749 (B.I.A. 1988).

The Court did not need to get into the nuances of immigration law to rule against the government in this case.

Some of the substantial takeaways from the decision are:

Waiver of the Tax Treaty: The government cannot assert an individual waived the treaty law because she initially filed the wrong IRS forms (1040) instead of the non-resident form (1040NR) and IRS Form 8833.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

Aroeste v United States – Order 20 Nov 2023 (p. 17)

Expatriation Tax form – IRS Form 8854: Validity and its Failure to Comply with the Administrative Procedure Act (“APA”)

C. Whether Aroeste Was Required to File Form 8854 The Government next argues that even if the IRS had accepted Aroeste’s amended returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009-85. (Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both amended forms. (Id.) Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does

not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Aroeste v United States – Order 20 Nov 2023 (p. 11)

Tax Treaty Law Applies – Article 4 Regarding Tax Residency

Various detailed analysis and discussions from the Court –

Aroeste v United States – Order 20 Nov 2023 (p. 11-14)

The Preamble to the FBAR Regulations is Not the Law –

. . . the Government points to the preamble to the 31 C.F.R. Part 1010 regulations, providing that “[a] legal permanent resident who elects under a tax treaty to be treated as a non-resident for tax purposes must still file the FBAR.” Amendment to the Bank Secrecy Act Regulations—Reports of Foreign Financial Accounts, 76 Fed. Reg. 10234-01 (Feb. 24, 2011). The Court finds this unavailing. The Government’s argument does not refute the plain language of the FBAR regulations, which explicitly invoke provisions of Title 26, including the provision that requires consideration of an individual’s status under an applicable tax treaty for the purpose of determining whether an individual is a “United States person” subject to FBAR filing. Specifically, Title 31 C.F.R. § 1010.350, which governs reporting of FBARs, subsection (b)(2) states that a “resident of the United States is an individual who is a resident alien under 26 U.S.C. 7701(b) and the regulations thereunder . . . .” The Government fails to cite to any case law or statue indicating otherwise, and the Court finds none. As such, because the Court finds the Treaty applicable to Aroeste, then the residence provisions of the Treaty, or the “tie breaker rules” dictates whether Aroeste may be treated as a nonresident alien.

Aroeste v United States – Order 20 Nov 2023 (p. 14)

This is the third court case (the other two were in U.S. Tax Court) I have had over the last several years where the IRS tried to assess substantial penalties and taxes against LPRs who resided substantially outside the United States. The other two cases were conceded by the IRS prior to going to trial. One case had over US$40M at stake as assessed by the IRS. This case, in federal district court, was pushed all the way to this favorable (to Mr. Aroeste and those around the world in similar circumstances) outcome by the government. We were successful with all of these non-U.S. citizen cases (two brothers from Mexico and an individual from Germany).

Three Precedent Setting Cases in International Information Reporting (“IIR”) in 6 Weeks: * Aroeste, * Bittner, and * Farhy: all Interconnected via Title 26, Title 31 and U.S. Income Tax Treaties

In just over six weeks, there have been three key judicial precedents favorable to international individuals. These cases have helped clarify the requirements of individuals and the limitations on the powers of the IRS in assessing IIR penalties. Please see the full article on tax notes. These IIR decisions relate to:

Title 31 penalties for Foreign Bank Account Reports (“FBARs”),

How these two federal statutory regimes of Title 31 and 26 crossover into international law as set forth in U.S. income tax treaties negotiated with different countries around the world.

Each of these three cases are interconnected and have significant impact to individuals with global lives, global assets, multi-national family members and those who have businesses or accounts in different parts of the world.

Aroeste v. United States

First, on February 13th, 2023, the Southern District of California District Court (the “District Court”) made a key determination in a Joint Discovery Motion decision in Aroeste.[2] The District Court concluded in Aroeste that the IRS/DOJ[3] could not ignore the U.S.-Mexico income tax treaty (“Treaty”) and its application to a Mexican national who has resided almost all of his life in Mexico City and has maintained a “green card” for immigration purposes in the United States. It is a non-willful FBAR case. The District Court applied the interconnected statutes and regulations of Titles 31 and 26 to help determine who qualifies as a “United States person”; specifically with reference to international law and obligations set forth in the Treaty. The key question in that case that remains to be answered is who (specifically Mr. Aroeste and by extension to a pool of millions of green card individuals residing outside the United States who are not citizens[4]) must file FBARs?

Second, on February 28th, 2023, the Supreme Court of the United States (“SCOTUS”) resolved in Bittner[5], that the applicable non-willful FBAR penalty is not measured by every foreign account of the individual as the Service has argued for years. That case also dealt with non-willful filing of FBARs and the SCOTUS concluded the IRS cannot impose penalties of $10,000 on each and every account held; but rather the penalty is “per report” that was not correctly filed. Hence, the total maximum penalty per year is $10,000. A maximum penalty of $50,000 (x5 years) applied per the SCOTUS versus the IRS determined amount of US$2.7M+.

Farhy v. Commissioner

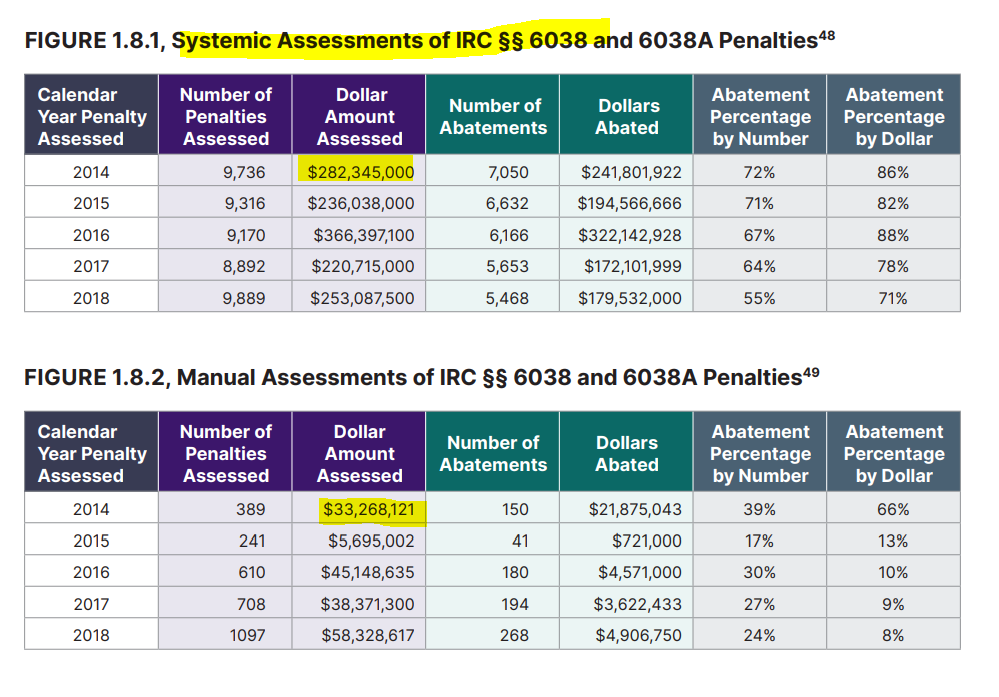

Lastly, on April 3rd, 2023, the United States Tax Court (the “Tax Court”) issued a decision in Farhy,[6] stating that the IRS does not have statutory authority to assess IIR penalties under section 6038(b). The IIR that is required by this statute is IRS Form 5471, which includes multiple filing categories. This has far reaching implications about how the government will be able to collect the IIR penalties the Service administratively determines are owed.[7] The Taxpayer Advocate previously issued a report on point titled: The IRS’s Assessment of International Penalties Under IRC §§ 6038 and 6038A Is Not Supported by Statute, and Systemic Assessments Burden Both Taxpayers and the IRS[8] In that report, the Taxpayer Advocate identified more than $310M of penalties just for the tax year 2014 the IRS “assessed” under Sections 6038 and 6038A.[9] We now know these “assessments” were invalid.

[1] See, footnote 19 regarding United States Tax Court’s Order in the case of Alberto Aroeste & Estela Aroeste vs. Commissioner.

[3] The “IRS” or the “Service” are used as shorthand for the Internal Revenue Service; and the Department of Justice; Tax Division is referred to as the “DOJ.”

[4] See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year and 4.8 million are estimated to have died and/or emigrated. The authors have extrapolated from these estimates in the report to conclude that more than 3 million of these individuals have emigrated and left the United States. The millions of individuals do not reside in the U.S. of which Mr. Aroeste is one of these individuals; although a tax treaty must exist in the country of residence for the analysis of the District Court in Aroeste v. United States to be applicable.

[5] No. 31—1195 (U.S. Feb. 28, 2023); 598 U. S. ____ (2023); The majority opinion by Justice Gorsuch cited to the ACTEC amicus brief (where Patrick W. Martin, the author of tax-expatriation.com and a fellow of ACTEC worked on the drafting of the brief) and concluded:

“Best read, the BSA treats the failure to file a legally compliant report as one violation carrying a maximum penalty of $10,000, not a cascade of such penalties calculated on a per-account basis.” The ACTEC brief was cited by the majority opinion- “ We see evidence, too, that the point of these reports is to supply the government with information potentially relevant to various kinds of investigations, criminal and civil alike. But what we do not see is any indication that Congress sought to maximize penalties for every nonwillful mistake (whether a late filing, a transposed account number, or an out-of-date bank address). See Brief for American College of Trust and Estate Counsel as Amicus Curiae 5–7.”

[7]See, Patrick W. Martin, Megan L. Brackney, Robert Horowitz, and Javier Diaz de Leon Galarza: Problems Facing Taxpayers with Foreign Information Return Penalties, November 12, 2020.

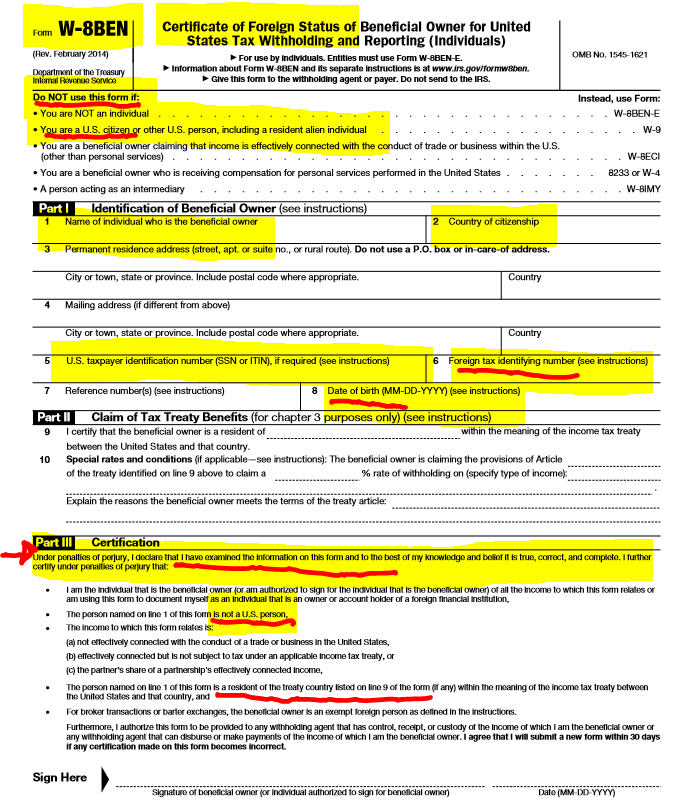

Individuals who do not specialize in U.S. federal tax law, often have little detailed understanding of the U.S. federal “Chapter 3” (long-standing law regarding withholding taxes on non-resident aliens and foreign corporations and foreign trusts) and “Chapter 4” (the relatively new withholding tax regime known as the “Foreign Account Tax Compliance Act”) rules.

Indeed, plenty of U.S. tax law professionals (CPAs, tax attorneys and enrolled agents) do not understand well the interplay between these two different withholding regimes –

Plus, the IRS forms have been significantly modified over the years; with increasing factual representations that must be made by individuals who sign the forms under penalty of perjury. They are complex and not well understood. For instance, the older 2006 IRS Form W-8BEN for companies was one page in length and required relatively little information be provided.

The entire form is reproduced here; indicating how foreign taxpayer information was optional and generally there was no requirement to obtain a U.S. taxpayer identification number. It was governed exclusively by Chapter 3 and the regulations that had been extensively produced back in the early 2000s.

The forms were even easier before those regulations (see old IRS Form 1001). No taxpayer identification numbers were ever required and virtually no supporting information regarding reduced tax treaty rates on U.S. sources of income.

Life was simple back then – compared to today!

The one thing all of these forms have in common is that all information was provided and certified under penalty of perjury. Current day IRS Forms W-8s can typically be completed accurately by experts who understand the complex web of rules. Plus, multiple versions of W-8s exist today; most running some 8+ pages in length.

Making certifications under penalty of perjury are more complex, the more and more factual information that is being certified. If I certify the dog I see in front of me is “white and black” that is not a complex certification, if I see the dog and see the “white and black”. If the dog also has some brown coloring, my certification would necessarily not be false.

However, if I have to certify as to the colors of each dog in a pack of 8 dogs (and each and every color that each dog is/was), that becomes a much more complicated certification.

That’s my analogy for the old IRS Forms W-8s and the current day IRS Forms W-8s.

Compare that form, of just 10 years ago, with what is required and must be certified to under current law. It can be daunting.

Now to the rub. Individuals who certify erroneously or falsely, can run a risk that the government asserts such signed certification was done intentionally. I have seen it happen in real cases; even though the individual layperson (particularly those who speak little to no English and live outside the U.S.) typically has little understanding of these rules. They typically sign the documents presented to them by the third party; usually the banks and other financial institutions.

The U.S. federal tax law has a specific crime, for making a false statement or signing a false tax return or other document – which is known as the perjury statute (IRC Section 7206(1)). This is a criminal statute, not civil. Some people are also under the misunderstanding that a false tax return needs to be filed. The statute is much broader and includes “. . . any statement . . . or other document . . . “.

(1) Declaration under penalties of perjury

Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that it is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; or . . .

Therefore, if a U.S. citizen living overseas (or anywhere) signs IRS Form W-8BEN (or the bank’s substitute form, which requests the same basic information), that signature under penalty of perjury will necessarily be a false statement, as a matter of law. Why? By definition, the statute says a U.S. citizen is a “United States person” as that technical term is defined in IRC Section 7701(a)(30)(A). Accordingly, IRS Form W-8BEN, must only be signed by an individual who is NOT a “United States person”; who necessarily cannot be a United States citizen. To repeat, a United States citizen is included in the definition of a “United States person.” Plus, the form itself, as highlighted at the beginning of the form, warns against any U.S. citizen signing such form.

Indeed, criminal cases are not simple, and I am not aware of any single criminal case that hinged exclusively on a false IRS Form W-8BEN. However, I have seen cases, where the government has alleged the U.S. born individual must have signed the form intentionally, knowing the information was false. It’s a question of proof and of course U.S. citizens wherever they reside, should take care to never sign an IRS Form W-8BEN as an individual certifying they are not a “United States person”; even if they think they are not a U.S. person

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

Compliance Act”) rules.

Compliance Act”) rules. extensively produced back in the early 2000s.

extensively produced back in the early 2000s.