Month: September 2023

Tax Notes International: Article by Robert Goulder: FBAR Madness: We need to Chat About Aroeste

On Monday 11 Sept 2023, Robert Goulder wrote a detailed article about the implications of what he calls “The Green Card From Hell”! His article can be reviewed in its entirety through the subscription service provided by Tax Notes International – FBAR Madness: We Need to Chat About Aroeste.

Goulder made some key observations that are worth repeating for anyone who has been a green card holder for basically more than seven years. That can trigger the “expatriation” tax provisions – the focus of this blog.

The facts of the case of Mr. Alberto Aroeste are covered extensively and accurately in Goulder’s article.

He noted:

This week’s article concentrates on the novel FBAR issue that will be decided in Aroeste v. United States, an illegal exaction suit before the U.S. District Court for the Southern District of California.7 The case has garnered attention for good reason. It pushes back against the government’s dubious policy of requiring individuals treated as nonresidents under a U.S. tax treaty to provide FBAR filings. Let’s note the futility of the financial information which the government seeks from these folks. It concurrently exempts treaty nonresidents from the need to file IRS Form 8938 (“Statement of Specified Foreign Financial Assets”), the tax code’s counterpart to the FBAR.8 It remains problematic that the government should demand reporting from treaty nonresidents as if they were residents.9

Goulder – FBAR Madness: We Need to Chat About Aroeste.

The one issue not explained well relates to how and when lawful permanent residency (i.e. a “green card”) under Title 8 is even valid in the first place. Goulder’s article explains some of the rights of lawful permanent residency status, but also addresses some key areas of the immigration law the same as most tax law experts cover a different area of the law. See, SCOTUS’ observations of the law in this context: Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

For instance, Goulder claims green card holders cannot be deported as long as the immigration status remains valid. True – but what is not explained is how easy it is to cease to have a valid one in the first place. What he doesn’t explain is how and when an individual can “abandon” or “relinquish” the status as a green card holder (as a matter of law) by not residing permanently in the United States. See, Fundamentals of Immigration Law, written by Charles A. Wiegand, III, Former Immigration Judge, Oakdale, Louisiana. The law is complex as described by Wiegand.

Goulder does not seem to find the government’s arguments persuasive (“ain’t buying it“!):

For Aroeste, there seems to be little doubt his closer personal and economic ties are with Mexico. The IRS knows this. An analysis conducted by an IRS agent concluded that he spent no more than 67 days in the United States during 2012 and 57 days in the United States in 2013, with three-quarters of the remaining time spent in Mexico.

Goulder –

The IRS doesn’t care where Aroeste had closer personal and economic ties. That’s because it doesn’t care about the tiebreaker. As the government sees it, the treaty is a distraction that has no meaningful role to play in this litigation. The plaintiff’s immigration status is conclusive, end of story. His green card settles the matter, such that all further inquiries are superfluous and should cease.

Id.

What bothers me about that argument is how the government’s position selectively wishes away the existence of the U.S. tax treaty network — but only for application of the FBAR regime. The Mexico treaty would still mean something in another context, but not on the pivotal issue of Aroeste’s status as a U.S. person for FBAR purposes. Sorry, I ain’t buying it.

Id.

The government argues the treaty is only relevant for income and excise tax purposes, and what we have here are penalties based on violations of the Bank Secrecy Act — not the Internal Revenue Code. As the government sees it, no plaintiff can successfully challenge penalties authorized by Title 31 with legal remedies based on Title 26. I’m still not buying it.

Id, Goulder

I would recommend you take a read through his article that also addresses a discussion on how the government prefers to keep internal memoranda from the eyes of the public. He discusses at some length – Tax Analysts and Coastal States. How the Court in Aroeste took an approach different from the D.C. Circuit in articulating 9th Circuit law regarding attorney client privileged documents in the possession of the government.

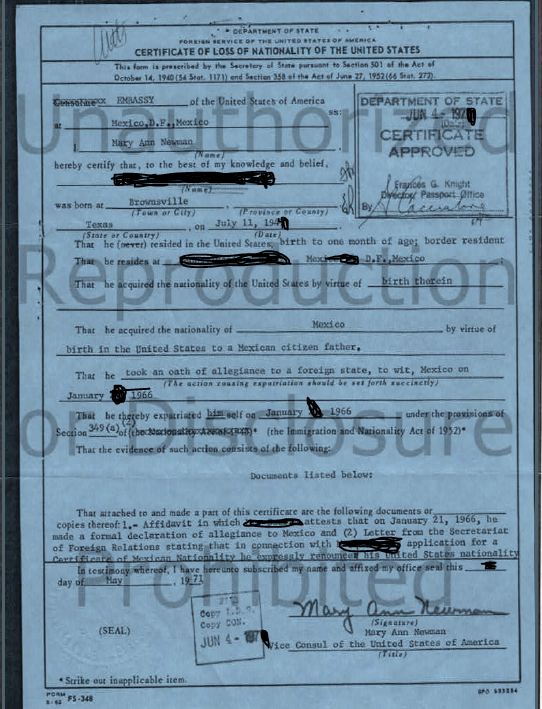

Short Window of Wait Times for CLN: One Month to 6 Weeks?

The wait times for the State Department to issue a Certificate of Loss of Nationality (“CLNs”) used to be quite long, based upon the author’s experience with various clients. That has all changed since about the beginning of this year 2023. The author has seen cases that are taking less than 6 weeks from the date of the meeting to take the oath of renunciation before a consular officer.

See a prior post back in 2014: Wide Window of Wait Times for CLN: One Month to 9 Months (or More?)

See another of the author’s posts regarding the CLN (2014): The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act.

Also, in a prior post back in 2014, this author discussed the importance of IRC Section 7701(a)(50): Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

These issues all relate to important timing considerations under the law which can be impacted by how long it takes to receive the CLN:

- When can an individual who has taken the oath of renunciation be able to file IRS Form 8854, Initial and Annual Expatriation Statement?

- When do you measure the values of the assets/liabilities for determining whether the former citizen was a “covered expatriate”?

- What will be the date as set forth in the statute (877A) for calculating the “mark to market” taxable gain (if any):?

- All property of a covered expatriate shall be treated as sold on the day before the expatriation date for its fair market value. (877A(a)(1))