Fidelity knows there is concern among investors about the U.S. Passive Foreign Investment Company (PFIC) rules. These rules could significantly affect “U.S. persons” who hold Canadian mutual funds, so we are providing you with information about these complex rules. . .

Month: May 2016

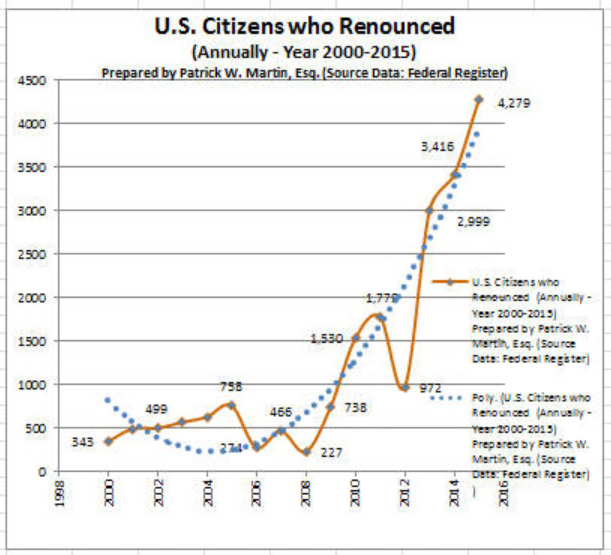

Trendlines Show United States Citizens Renouncing at Historical Levels

Graphs and charts are a nice way to show key pieces of information quickly. The charts I create showing the numbers of U.S. citizens (“USCs”) who have renounced their citizenship help me better understand and track the detailed data behind the graphs.

In this vein, I have added trend-lines to two of the graphs that reflect the total annual and quarterly numbers of individuals who have renounced over the last few years.

The trend-lines are the blue dotted lines in each chart. The first chart reflects annual renunciations over a longer period of time, which is compressed much more along the “x axis” – i.e., the horizontal axis. The trend of USCs who are renouncing looks quite dramatic in this chart; a giant ski slope heading upwards fast.

The next chart includes many more data points along the “x axis” spread out over a shorter period of time, which is also reflected by the dotted blue trend-line. Accordingly, the trend-line appears to be a more gradual increase of USC renunciations.

Nevertheless, both show the trend over time as increasing substantially over time.

As has been explained in prior posts, those U.S. citizens who are considering renouncing U.S. citizenship should not take the decision lightly unless they want to be a “covered expatriate” with various adverse U.S. tax and legal consequences.

See, for instance the following prior blogs, Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C).

The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

1st Qtr 2016 Renunciations – New Normal

The number of U.S. citizens who are reported to have renounced U.S. citizenship was 1,158 for the 1st quarter of 2016.  I keep and track all names of USCs who are reported by the U.S. Treasury in the Federal Register. The data tracking reflects a significant increase in quarterly renunciations since 2008. That is the general trend. There is no direct quarter to quarter trend, as my graph above reflects (where 1,158 is the latest number of USC renunciations).

I keep and track all names of USCs who are reported by the U.S. Treasury in the Federal Register. The data tracking reflects a significant increase in quarterly renunciations since 2008. That is the general trend. There is no direct quarter to quarter trend, as my graph above reflects (where 1,158 is the latest number of USC renunciations).

For some historical references, see, New Record of U.S. Citizens Renouncing – The New Normal, 11 Feb, 2015.

There are several strategic decisions that most all U.S. citizens need to consider prior to renouncing citizenship. See, for instance – Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4)) Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

Can the U.S. Federal Government Bar Entry into the U.S. to a U.S. Citizen without a U.S. Passport?

Global Entry, SENTRI and NEXUS after Renouncing – the “Trusted Traveler Programs” – SAFE TRAVELS!

The “Dirty Secret” of U.S. FATCA IGAs

The world is starting to wake up to better understand how the U.S. Treasury negotiated so-called “bilateral” FATCA Intergovernmental Agreements (“IGAs”) with some 113 countries around the world.  The list of all countries can be found here at the Treasury website – Foreign Account Tax Compliance Act (FATCA)

The list of all countries can be found here at the Treasury website – Foreign Account Tax Compliance Act (FATCA)

Not all of these countries have actually signed the IGAs. Many of them have what the U.S. Treasury calls an “agreement in substance.”

How does this impact USCs and LPRs residing outside the U.S.? Many ways.

First, extensive information is being collected by foreign financial institutions (FFIs – non-U.S. financial institutions) throughout the world to identify “U.S. Persons” and “Substantial U.S. Owners.” The IGAs use the term “Specified U.S. Person” with respect to what are defined as “U.S. Reportable Accounts.” See as an example, the Treasury FATCA IGA with Colombia, which is largely identical in form to almost all other IGAs.

Second, many FFIs have adopted a policy to no longer accept or retain U.S. accounts, due to the cost of compliance associated with U.S. citizens and lawful permanent residents. Also, many FFIs simply want to avoid the risk of being penalized heavily by the U.S. federal  government for having U.S. taxpayers and being charged with some type of wrongdoing; namely aiding and abetting U.S. taxpayers to evade U.S. tax obligations. See, Jack Townsend’s thoughtful website Federal Tax Crimes that reviews in detail the various cases with foreign banks, with a particular focus on Swiss banks, U.S. DOJ Program for Swiss Banks .

government for having U.S. taxpayers and being charged with some type of wrongdoing; namely aiding and abetting U.S. taxpayers to evade U.S. tax obligations. See, Jack Townsend’s thoughtful website Federal Tax Crimes that reviews in detail the various cases with foreign banks, with a particular focus on Swiss banks, U.S. DOJ Program for Swiss Banks .

Now to the “dirty little secret” of FATCA IGAs. They are not bilateral in the sense that U.S. banks do not need to provide the same detailed information on their non-U.S. clients (e.g., UK, French, Canadian, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, residents, etc.) as do FFIs regarding “U.S. accounts.” This is no real secret, since a simple reading of the FATCA IGAs will get you to this conclusion by simply understanding the difference between what is defined as a “U.S. Reportable Account” (which is extraordinarily broad) compared to “Country X Reportable Account.” The latter definition, e.g., a Colombian Reportable Account, only obligates U.S. banks to send information of individual residents on U.S. source income under chapter 3 and certain accounts of Colombian entities.

Hence, all non-U.S. source income to a Colombia resident individual is not subject to reporting by the U.S. financial institution. She could have a portfolio of US$150M in non-U.S. mutual funds, ADRs traded on the NYSE and have no reporting of all of her income going back to the Colombian government. Also, stock sales of U.S. corporations (e.g., Apple, Ford or Microsoft) is not treated as “U.S. source income” defined under chapter 3. Plus, a Colombian resident who has an offshore corporation (e.g., a BVI company) that owns the investments, NO reporting is required of the U.S. financial institution; even if the entire US$150M portfolio were invested in U.S. stocks, U.S. treasuries, and other American made financial investments.

Contrast that with what is defined as a “U.S. Reportable Account” that would include a U.S. Person that is a “Controlling Person” of a “Non-U.S. Entity.” Take the same example in reverse; a Colombian bank must identify all of its clients with Non-U.S. Entities (undertake an expensive due diligence process) to then identify whether such entities (e.g., a BVI company) has a “Specified U.S. Person”. Plus, it does not matter if the income is from Colombian sources or non-Colombian sources. Income is income and must be reported by the FFI.

Accordingly, Banks around the world in at least 113 countries (e.g., UK, French, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, Cayman, Singapore, Guatemala, Hong Kong, etc.) are required to drill down and collect detailed information on beneficial owners of basically all companies, trusts and other legal entities. This work is required, so as to identify who are “U.S. persons” to identify “substantial U.S. owners” as that term is defined in the FATCA regulations. The IGAs call these essentially “U.S. Reportable Accounts.” In the case of FFIs, U.S. taxpayers cannot hide behind offshore opaque legal entities (e.g., which would generally be illegal for USCs to form and hold assets in a foreign corporation and not report the assets, activities and earnings of the foreign corporation, which would generally be a CFC or possibly a PFIC).  See prior post: March 30, 2015, The Problem with PFICs! “Avoid PFICs Like the Plague”

See prior post: March 30, 2015, The Problem with PFICs! “Avoid PFICs Like the Plague”

The FATCA IGAs, require these FFIs to provide extensive information on all income on these “U.S. Reportable Account” to the IRS, either directly or indirectly through their own governments.

In contrast, individuals resident in any foreign country (e.g., UK, French, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, Belgium, Guatemala, Luxembourg, etc.) can generally hold their ownership interests of U.S. investment assets in U.S. banks and financial institutions through opaque legal structures and hide behind the entity without worrying that a U.S. financial institution has any duty to identify and disclose who are the beneficial owners to the tax authorities of those residents. See Colombian individual scenario above with a BVI company.

- Why did the Treasury purposefully create this limited reporting obligations for U.S. financial institutions while creating extensive and detailed reporting obligations for FFIs?

- Why are U.S. financial institutions not required under FATCA IGAs to identify the beneficial owners of opaque legal structures to report the income and gains to foreign tax authorities?

- Why are U.S. financial institutions not required under FATCA IGAs to identify the and report non-U.S. source income in their U.S. accounts?

- Why has the U.S. refused to participate in the OECD common reporting standards?

- Why did the U.S. federal government wait until just this month of May 2016, to say it will start increasing the ” . . . transparency [of] the “beneficial ownership” of companies formed in the United States by requiring that companies know and report their true owners . . . “?

- Why is the White House just now saying it is going to be “Closing a Loophole that Enables Foreigners to Hide Behind Anonymous Entities Formed in the United States” when from inception, starting in 2012 all of the FATCA IGAs (which were drafted and negotiated exclusively by the U.S. Treasury) have always allowed foreigners with accounts and investments in the U.S. to hide behind anonymous entities?

New Proposed Treasury Regulations Will Not Affect USCs But Will Affect some LPRs

United States Citizens (“USCs”) and lawful permanent residents (“LPRs”) who live largely outside the U.S. must generally be aware of U.S. federal tax laws and how they apply to them. USCs and LPRs “expats” (living outside the U.S.) are of course constantly being required to understand U.S. tax law and comply with its provisions.

Recently, the U.S. Treasury proposed new regulations requiring certain foreign owned single member U.S. limited liability companies and grantor trusts to report information.

The preamble to the proposed regulations (which are titled – Treatment of Certain Domestic Entities Disregarded as Separate From Their Owners as Corporations for Purposes of Section 6038A) note that:

- Some disregarded entities are not obligated to file a return or obtain an employer identification number (“EIN”). In the absence of a return filing obligation (and associated record maintenance requirements) or the identification of a responsible party as required in applying for an EIN, it is difficult for the United States to carry out the obligations it has undertaken in its tax treaties, tax information exchange agreements and similar international agreements to provide other jurisdictions with relevant information on U.S. entities with owners that are tax resident in the partner jurisdiction or otherwise have a tax nexus with respect to the partner jurisdiction. . . . a disregarded entity is not subject to a separate income or information return filing requirement. Its owner is treated as owning directly the entity’s assets and liabilities, and the information available with respect to the disregarded entity depends on the owner’s own return filings, if any are required.

For those LPRs residing outside the U.S. who are not U.S. taxpayers by virtue of an applicable income tax treaty (i.e., by application of the treaty tie-breaker rules, typically Article 4), it appears these newly proposed regulations could be applicable to their single member LLCs or grantor trusts. USCs will not be effected, since the proposed regulations impose this reporting requirement when there is “(2) One foreign person [who] has direct or indirect sole ownership of the entity.” A USC cannot be a “foreign person”; which is not a defined term in the current statute or regulation. A “United States person” is a defined term and so is a “nonresident alien”; but not a “foreign person.”

Curiously, the Treasury is using IRC Section 6038A as the authority to issue such regulations. That statute only references “a corporation” which is a technically defined term under IRC Section 7701(a)(3), (a)(4) and (a)(30)(C). Section 6038A makes no reference to a”disregarded entity” a “grantor trust” or any other company or entity that are not “corporations.” Therefore, it is difficult to imagine how the Treasury has the statutory authority to issue this proposed regulation without legislative authority?

Part I: PFIC Minutiae – Why the Devil is in the Details

Previous posts have briefly discussed passive foreign investment companies (PFICs”). See, – “PFICs” – What is a PFIC – and their  Complications for USCs and LPRs Living Outside the U.S. (28 March 2014)

Complications for USCs and LPRs Living Outside the U.S. (28 March 2014)

and

The Problem with PFICs! “Avoid PFICs Like the Plague” (30 March 2015).

This discussion will be the first part of a series of key points that will delve into some of the important details.

To begin with, it is important to note the following “new” requirements, if you have an investment that falls into the category of a “PFIC.”

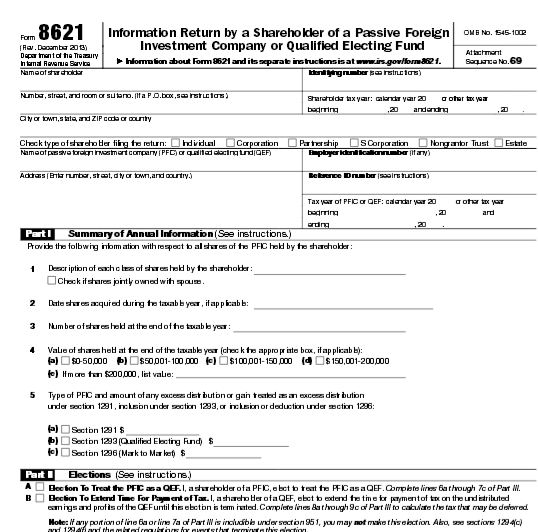

- Annual reporting of PFICs is now required under the new regulations. See, Regulations §1.1291–0T, et. seq.

- The regulations require the “. . . United States person must file a separate IRS Form 8621 for each PFIC . . .” investment. See, Treas. Reg. §1.1298–1T(e) –(e) Separate annual report for each PFIC—(1) General rule. If a United States person is required under section 1298(f) and these regulations to file Form 8621 (or successor form) with respect to more than one PFIC, the United States person must file a separate Form 8621 (or successor form) for each PFIC.

** This means that if the individual has a portfolio of 14 different mutual funds that are PFICs, the taxpayer has to prepare 14 different IRS Forms 8621.

Various financial institutions are just now starting to advise their clients who are U.S. citizens (commonly residing outside the U.S.) of these complex reporting rules. See for instance, Fidelity’s website; Passive Foreign Investment Company, Fidelity is helping investors comply with U.S. PFIC tax rules

The Life Insurance “Gotcha Tax” – IRS Assesses Excise Tax on Normal Life & Other Insurance Policies

The information featured on this blog is designed to orient U.S. citizens (“USCs”) and U.S. lawful permanent residents, i.e., “green card” holders  (“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

(“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

There are many complex federal tax rules that are often overlooked in the international area. One of those is the excise tax that is payable by the USC or LPR individual, not the non-U.S. insurance company, when premiums are paid to an insurance company. The IRS takes the position that the ” . . . the Service will generally seek payment of the excise tax from the U.S. person making the premium payment . . .” See, IRS Foreign Insurance Excise Tax- Audit Technique Guide.

This is a 1% excise tax on the premiums paid for each life insurance, sickness or accident insurance or contracts. See, IRC Section 4371. If you reside in London and buy life insurance with a UK life insurance carrier (or Paris with a French insurance company, Toronto with a Canadian insurance company, etc.) in your home country, you are probably not thinking that you need to pay Uncle Sam a tax on what you perceive as a “run of the mill” insurance coverage.

Indeed your life insurance company in your country of residence will not be advising that as a USC or LPR, you should be paying Uncle Sam.

If the insurance contract is a casualty policy, the excise tax is 400% greater than the 1% tax on life insurance premiums; i.e., a 4% excise tax. The payment of the tax is made on IRS Form 720, Federal Excise Tax Return.

In my experience, I never find that any individuals who are USCs and LPRs living around the world are aware of this obscure tax. When the tax is not paid the IRS has unlimited time to assess tax and penalties, including late payment penalties, late filing penalties and negligence penalties. Plus, interest that accrues on the unpaid tax and penalties can grow the amounts owing over time. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S., posted March 24, 2014.

The excise tax amount may not seem too significant. However, if it is not timely paid, there will be late payment and late filing penalties (e.g., for failure to file the excise tax return). This 1% or 4% excise tax is on the gross premium payment. This tax amount can certainly add up when insurance premiums are paid annually and over many decades.

Finally, be aware that the IRS is focusing on this excise tax on insurance contracts, at least within its OVDP program where IRS revenue agents are asserting that 25%, 27.5% or 50% of the value of the entire asset (e.g., the cash surrender value of the insurance policy) is subject to the “in lieu of penalty”.