Not everyone who renounces US citizenship faces the same tax consequences. People who qualify as “covered expatriates” face significant additional obligations. Here is what that means and how even modest individuals can end up in this category.

One of the greatest risks for anyone who wants to give up US citizenship is Section 877(a)(2)(C). Even the most economically modest individual, with little assets or income, can fall into this trap. No one at the US Department of State will provide tax advice or interpret Section 877(a)(2)(C) for you. The renunciation appointment itself is straightforward. The tax consequences are not.

What are the three tests for covered expatriate status?

Under Section 877(a)(2), you are a covered expatriate if any one of the following is true:

(A) Your average annual net income tax liability is greater than $124,000;

(B) Your net worth is $2,000,000 or more as of your expatriation date; or

(C) You fail to certify under penalty of perjury that you have met all US tax requirements for the 5 preceding taxable years, or fail to submit the required evidence of compliance.

Any individual who meets any one of these tests will be a covered expatriate and subject to the taxation and reporting requirements under Sections 877, 877A, and 2801.

What happens at the embassy or consulate?

When you take the renunciation oath at a US embassy or consulate, the Foreign Affairs Manual provides only standard overview language about “special tax consequences.” The consular officer will not explain the specific rules of Section 877(a)(2)(C) or tell you whether you will be a covered expatriate. This is worth understanding well before going to take the oath.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Why Long-Term Green Card Holders Cannot Escape the Exit Tax Rules

When long-term green card holders give up their green card, they face the same exit tax rules as US citizens who renounce citizenship. There is one exception in the law that allows certain dual citizens by birth to avoid covered expatriate status even if they meet the income or asset tests. Long-term green card holders cannot use it. Here is why.

When you give up your green card (or renounce US citizenship), the law determines whether you are a covered expatriate. You are a covered expatriate if you meet any one of three tests: an average annual income tax liability above an inflation-adjusted threshold, a net worth of $2 million or more on the date of expatriation, or a failure to certify 5 years of US tax compliance on Form 8854.

Meeting even one of these three tests makes you a covered expatriate. All three tests apply equally to US citizens who renounce and to long-term lawful permanent residents (LPRs) who give up their green card.

Is there an exception to the income and asset tests?

Yes, for some people. Under IRC Section 877A(g)(1)(B), certain individuals are exempt from the income and asset tests. If this exception applies to you, you can avoid covered expatriate status even if your net worth exceeds $2 million or your income exceeds the threshold. The certification requirement under Section 877(a)(2)(C) still applies to everyone, including those who qualify for this exception.

Who can use this exception?

The exception is narrow. Under the statute, it applies only to an individual who: became a citizen of the United States and a citizen of another country at birth; as of the date of expatriation, continues to be a citizen of and is taxed as a resident of that other country; and has been a US resident for no more than 10 taxable years during the 15-year period ending with the taxable year of expatriation. Only someone who acquired US citizenship automatically at birth, while also holding citizenship of another country from birth, can potentially qualify.

Why green card holders cannot use it

Lawful permanent residents are not US citizens. They hold a green card, which is a grant of permanent resident status, not citizenship. Because the exception in Section 877A(g)(1)(B) applies only to individuals who became US citizens at birth, long-term LPRs cannot satisfy this requirement by definition. The exception is simply not available to them.

What this means if you are a long-term green card holder

A long-term LPR who meets either the $2 million asset test or the income tax liability test will become a covered expatriate, even if they fully satisfy the 5-year certification requirement. Satisfying the certification requirement is necessary for everyone, but for long-term LPRs it is not sufficient on its own. If you also meet the income or asset test, you are a covered expatriate regardless.

The consequences include the mark-to-market exit tax on unrealized gains and the Section 2801 tax on covered gifts and bequests to US persons. These consequences can affect your US family members for decades. Understanding them well before you give up your green card, not after, is the only way to plan for them.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Does TIGTA have the Answer: to the Question – How many former U.S. citizens and long-term lawful permanent residents have filed and should have filed IRS Form 8854?

The short answer to the question above – is NO!

The government does not know how many IRS Forms 8854 should have been filed.

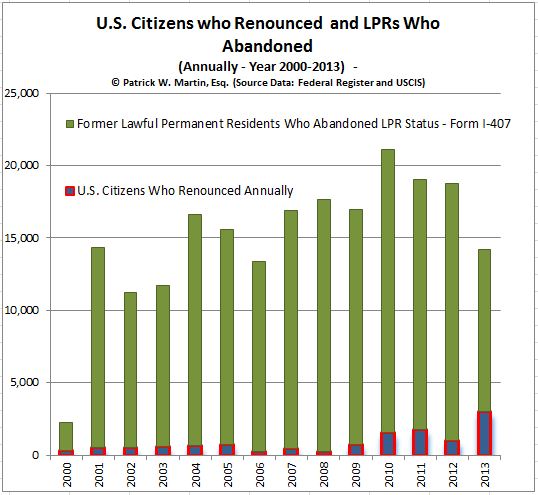

Note the total numbers of 8854 returns filed as reported in Figure 2 of the TIGTA Report were less than 25,000 during a ten year period. This report focuses really only on former U.S. citizens (“USC”) who have renounced their citizenship. Not on lawful permanent residents (“LPRs), which during that same ten year period there were around 200,000 who filed USCIS Form I-407.

* How Many Individuals Should have Filed Form 8854?

These regulations are extensive and provide an explanation of the purpose of these rules.

II. Purpose of Foreign Gift and Trust Provisions

During the mid- to late-1990s, abusive tax schemes, including offshore schemes involving foreign trusts, reemerged in the United States after reaching their last peak in the 1980s. GAO, Efforts to Identify and Combat Abusive Tax Schemes Have increased, but challenges remain, GAO–02–733 (Washington, DC: May 22, 2002). In these schemes, foreign trusts were used to transfer large amounts of assets abroad, where it was much more difficult for the IRS to identify whether U.S. persons owned a trust.

interest in such trusts, and whether such persons were reporting and paying the required taxes on their income from such trusts. Many of the foreign trusts were established in tax haven jurisdictions with bank secrecy laws. Before the 1996 Act amended sections 6048 and 6677, there was no Form 3520-A), which was limited to five percent of the transfer or corpus of the trust, as applicable, not to exceed $1,000. In light of this, it was difficult for the IRS to obtain information about income earned by U.S.-owned foreign trusts and distributions to U.S. beneficiaries from foreign trusts, and Sections 6048 and 6677 were generally ineffective in ensuring that U.S. persons provided this information. information. The result was “rampant tax evasion.” 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan). Requirement for U.S. Persons to Report Distributions from Foreign Trusts and the Penalty for Failure to Report Transfers to a Foreign Trust or an Annual Foreign Trust Information Statement (in Federal Register/Vol. 89, No. 90/Wednesday, May 8 of 2024/Proposed Rules and 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan).

“LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – BIG GAP with Actual Emigration of LPRs

Millions of lawful permanent residents (LPRs) who have left the U.S. and not “formally abandoned” their LPR status (by filing Form I-407, Record of Abandonment of Lawful Permanent Resident) typically remain in some kind of “LPR U.S. tax limbo.” How many individuals worldwide are in this LPR U.S. tax limbo?

Why are these numbers important for the tax-expatriation analysis? See, a recent post, Why Most LPRs Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets (Part I). Indeed, most individuals probably do not think they are a U.S. federal income tax resident when they leave the U.S. to reside overseas back to their home country. Why would they? There is no tax training manual provided to LPRs who leave the U.S. and no tax advisories – reflected on the card itself (unlike the last page of the U.S. passport, paragraph D). More precisely, most are probably not giving much, if any thought, to the complex U.S. federal tax residency rules and their extraterritorial application.

The “big gap” referred to above can be identified from the the Office of Immigration Statistics (OIS) report titled: Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year. Between naturalization, mortality and emigration the report shows that the LPR population, year over year, has remained stable. In 2019 the total number of LPRs per this report was 13.6 million, up from just 13.0 million in 2015.

The “gap” is the difference between the numbers of LPRs who have left-emigrated the U.S. (some 3+ million) compared to something like an annual average of 15-19 thousand who have filed Form I-407. The gap is in the millions of persons who are in LPR U.S. tax limbo.

Mexico

The report is also worth reading if you want to understand the demographics of the LPR population. Mexico has about 2.5 million (which is by far the greatest number) of the total 13+ million LPR population.

As the report points out there is no reliable direct measurements of LPR emigration. They do not exist. This lack of information is what drove me to file a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

The information I obtained in the FOIA response was surprising, since the government had records showing only 46,364 Forms I-407 were filed in the years 2013 through 2015, as follows:

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

This represents an average of only 15,455 individuals who formally abandoned their LPR status. Contrasted with more than 3.6 million estimated to have emigrated in 2019 per the DHS report leaves a massive gap of well over 3 million persons who held a “green card” and have left. They are now in LPR U.S. tax limbo.

What about the tax consequences? How many of these LPRs who left the U.S. know, understand or have any idea whatsoever of the federal tax filing obligations regarding their status?

What is the takeaway from the DHS report and LPR – I-407 information provided to me by the FOIA response? There is a discrepancy in the millions of people. Millions of individuals who actually leave or have left the U.S. to reside somewhere else around the world; compared to only some tens of thousands of individuals who have formally filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

What can these individuals do to get out of the LPR U.S. tax limbo?

Part II: Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

A post in August 2014 explained the basic rule of who is a “long-term resident” as that technical term is defined for tax purposes in IRC Section 877 (e)(2). There is much confusion about how the tax law defines a “lawful permanent resident” (“LPR”) versus how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

This follow-up comment is to highlight some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law.

A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particicular case.

There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

U.S citizens (USCs) and Lawful Permanent Residents (LPRs): Caution When Making Gifts. US Tax Court Recently Ruled a 1972 Gift by Sumner Redstone Still Open to IRS Challenge

Statute of Limitations

The statute of limitations is one of the most important considerations for any individual when considering what tax consequences the Internal Revenue Service (“IRS”) might argue they have for years past. This can occur many years into the future as explained further below.

Former USCs and LPRs can be in a particularly precarious position, as was recently demonstrated by a U.S. Tax Court case for a gift that was made decades ago in 1972. See, Redstone vs. Commissioner (TCM 2015-237). Although this U.S. Tax Court case involving Sumner Redstone had nothing to do with renunciation of citizenship, it shows how the IRS can reach back many years and even decades in assessing taxes it claims are owing. The newly (in year 2010) added IRC Section 6501(c)(8) makes this highly likely under current revised law.

Transfers to U.S. Beneficiaries (e.g., U.S. resident or citizen children or grandchildren who might receive gifts or bequests from a “Covered Expatriate” the former USCs or “long-term resident” – Green Card Holders)

2. There is fraud on the part of the taxpayer (e.g., the taxpayer intentionally does not report income). IRC Sections 6501(c)(1), (c)(2).

Missing Information on Tax Return Filed – re: International Matters

3. The USC or LPR fails to report certain foreign transactions, including inadvertently neglecting to report. IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act” which also created FATCA. The types of transactions set above in the table provides a brief summary of when transactions can give rise to an “open” statute of limitations period. In other words, as many years and decades can pass (see Redstone 1972 gift transaction) before the IRS ever has to make a proposed assessment of taxes and penalties. These include numerous ownership or economic interests in foreign (non-U.S.) companies, partnerships, foreign trusts, foreign investment accounts, among others.

For a more in depth review of the international (non-U.S.) transactions that give rise to this reporting, see IRS Forms 3520, 3520-A, 5471, 8865, 5472, 8938, 8858, 926 among others.

Denial of U.S. Passports: President Obama and Congress Pass Law that will Require Department of State to Deny a U.S. Passport for a “Seriously Delinquent Taxpayer”

Entry in and out of the U.S. has just gotten more problematic under a new law for those U.S. citizens who the IRS asserts owes taxes. A new statutory concept has been added to the tax law called “seriously delinquent tax debt”; which is defined by new IRC Section 7345 as a tax that has been assessed, is greater than US$50,000, and where a notice of lien has been filed or levy made.

The administration of passports is the responsibility of the Department of State. [“Passport Act of 1926,” 22 U.S.C. sec. 211a et seq.] The Secretary of State may refuse to issue or renew a passport if the applicant owes child support in excess of $2,500 or owes certain types of Federal debts. The scope of this authority does not extend to rejection or revocation of a passport on the basis of delinquent Federal taxes. Although issuance of a passport does not require a social security number or taxpayer identification number (“TIN”), the applicant is required under the Code to provide such number. Failure to provide a TIN is reported by the State Department to the Internal Revenue Service (“IRS”) and may result in a $500 fine.

***

Senate Amendment

Under the Senate Amendment, the Secretary of State is required to deny a passport (or renewal

of a passport) to a seriously delinquent taxpayer and is permitted to revoke any passport

previously issued to such person. In addition to the revocation or denial of passports to delinquent taxpayers, the Secretary of State is authorized to deny an application for a passport if the applicant fails to provide a social security number or provides an incorrect or invalid social security number. With respect to an incorrect or invalid number, the inclusion of an erroneous number is a basis for rejection of the application only if the erroneous number was provided willfully, intentionally, recklessly or negligently. Exceptions to these rules are permitted for emergency or humanitarian circumstances, including the issuance of a passport for short-term use to return to the United States by the delinquent taxpayer.

The provision authorizes limited sharing of information between the Secretary of State and

Secretary of the Treasury. If the Commissioner of Internal Revenue certifies to the Secretary of

the Treasury the identity of persons who have seriously delinquent Federal tax debts as defined

in this provision, the Secretary of the Treasury or his delegate is authorized to transmit such

certification to the Secretary of State for use in determining whether to issue, renew, or revoke a

passport. Applicants whose names are included on the certifications provided to the Secretary of

State are ineligible for a passport. The Secretary of State and Secretary of the Treasury are held

harmless with respect to any certification issued pursuant to this provision.

Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

This is Part II, a follow-on discussion of older U.S. case law and IRS rulings that address how and when individuals are subject to U.S. taxation before and after they assert they are no longer U.S. citizens.

I might point out that I am of the belief that we humans always like to hear the news we want to hear; and/or interpret it in the way we find most beneficial to us. Who doesn’t like good news versus bad news? Whether we (laypeople and tax lawyers alike) interpret Section 877A(g)(4) in any particular way; it is of no real consequence when it is the IRS that will enforce the law and ultimately the Department of Justice, Tax Division who will handle any such case interpreting this provision before a U.S. District Court or the Court of Federal Claims. For those who have not litigated before these Courts and seen how aggressive are the government lawyers in advocating for the government, the following discussion will hopefully be illustrative.

The question is what is the correct date of “relinquishment of citizenship” as defined in the statute; IRC Section 877A(g)(4)? Many argue the law cannot be applied retroactively?

Of course, the answer to this question helps determine if and when will the individual be subject to the federal tax laws of the U.S. on their worldwide income and global assets. In the case of Ms. Lucienne D’Hotelle (an interesting 1977 appellate opinion from the firs circuit) she had spent little time in the U.S. and had sent a letter in her native language French to the U.S. Department of State, which stated “I have never considered myself to be a citizen of the UnitedStates.” This is not unlike many individuals around the world today; at least as of late – in the era of FATCA, who assert they are not a U.S. citizen because they “relinquish[ed] it by the performance of certain expatriating acts with the required “intent” to give up the US citizenship” and did not notify the U.S. federal government.

The Court nevertheless found Ms. Lucienne D’Hotelle retroactively subject to U.S. income taxation on her non-U.S. source income (up until she received a certificate of loss of nationality from the Department of State); for specific years even when the immigration law provisions of the day said she was no longer a U.S. citizen during that same retroactive period.

There have been many contemporary commentators who argue an individual does not need to (i) have, (ii) do, or (iii) receive any of the following, and yet still should be able to successfully argue they have shed themselves of U.S. citizenship and hence the obligations of U.S. taxation and reporting on their worldwide income and global assets –

(i) receive a U.S. federal government issued document (e.g., a certificate of loss of nationality “CLN” per 877A(g)(4)(C)),

(ii) receive a cancelation of a naturalized citizen’s certificate of naturalization by a U.S. court (per 877A(g)(4)(D)),

(iii) provide a signed statement of voluntary relinquishment from the individual to the U.S. Department of State (per 877A(g)(4)(B)), or

(iv) provide proof of an in person renunciation before a diplomatic or consular officer of the U.S. (per paragraph (5) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481(a)(5)), in accordance with 877A(g)(4)(C)).

Some older tax cases that interpreted similar concepts are worthy of consideration. They will certainly be in any brief of the attorneys for the U.S. Department of Justice, Tax Division and/or Chief Counsel lawyers for the IRS in any case where the individual challenges that none of the above items are required in their particular case to avoid U.S. taxation and reporting requirements.

The D’Hotelle case is illustrative of the efforts taken by the Department of Justice, Tax Division in collecting U.S. income tax on a naturalized citizen. You will notice they did not take a sympathetic approach to her case. Ms. Lucienne D’Hotelle was born in France in 1909 and died in 1968 in France, yet the U.S. government continued to pursue collection of U.S. income taxation on her foreign source income from the Dominican Republic, France and apparently Puerto Rico even after her death during a period of time when she used a U.S. passport. Lucienne D’Hotelle de Benitez Rexach, 558 F.2d 37 (1st Cir.1977). She, not unlike many individuals today, claimed she was not a U.S. citizen – or at least stated “I have never considered myself to be a citizen of the UnitedStates.”

Some of the particularly interesting facts relevant to Ms. D’Hotelle, a naturalized citizen, which are relevant to the question of U.S. taxation of citizens, were set forth in the appellate court’s decision as follows:

Lucienne D’Hotelle was born in France in 1909. She became Lucienne D’HotelledeBenitezRexach upon her marriage to Felix in San Juan, Puerto Rico in 1928. She was naturalized as a UnitedStates citizen on December 7, 1942. The couple spent some time in the Dominican Republic, where Felix engaged in harbor construction projects. Lucienne established a residence in her native France on November 10, 1946 and remained a resident until May 20, 1952. During that time s 404(b) of the Nationality Act of 19402 provided that naturalized citizens who returned to their country of birth and resided there for three years lost their American citizenship. On November 10, 1947, after Lucienne had been in France for one year, the American Embassy in Paris issued her a UnitedStates passport valid through November 9, 1949. Soon after its expiration Lucienne applied in Puerto Rico for a renewal. By this time she had resided in France for three years.

* * *

On May 20, 1952, the Vice-Consul there signed a Certificate of Loss of Nationality, citing Lucienne’s continuous residence in France as having automatically divested her of citizenship under s 404(b). Her passport . . . was confiscated, cancelled and never returned to her. The State Department approved the certificate on December 23, 1952. Lucienne made no attempt to regain her American citizenship; neither did she affirmatively renounce it.

* * *

Predictably, the UnitedStates eventually sought to tax Lucienne for her half of that income. Whether by accident or design, the government’s efforts began in earnest shortly after the Supreme Court invalidated *40 the successor statute4 to s 404(b). In in Schneider v. Rusk, 377 U.S. 163 (1964), the Court held that the distinction drawn by the statute between naturalized and native-born Americans was so discriminatory as to violate due process. In January 1965, about two months after this suit was filed, the State Department notified Lucienne by letter that her expatriation was void under Schneider and that the State Department considered her a citizen. Lucienne replied that she had accepted her denaturalization without protest and had thereafter considered herself not to be an American citizen.

There are other facts that make clear the government was not fond of her husband, the income that he earned and how he managed his and his wife’s assets during and after her death. The Court also discusses at length the fact that she had used a U.S. passport during the years when she alleges she was not a U.S. citizen. The Court goes on to analyze her U.S. citizenship, and the following discussions are illustrative of the ultimate tax consequences.

LUCIENNE’S CITIZENSHIP

The government contends that Lucienne was still an American citizen from her third anniversary as a French resident until the day the Certificate of Loss of Nationality was issued in Nice. This case presents a curious situation, since usually it is the individual who claims citizenship and the government which denies it. But pocketbook considerations occasionally reverse the roles. UnitedStates v. Matheson, 532 F.2d 809 (2nd Cir.), cert. denied 429 U.S. 823, 97 S.Ct. 75, 50 L.Ed.2d 85 (1976). The government’s position is that under either Schneider v. Rusk, supra, or Afroyim v. Rusk, 387 U.S. 253, 87 S.Ct. 1660, 18 L.Ed.2d 757 (1967), the statute by which Lucienne was denaturalized is unconstitutional and its prior effects should be wiped out. Afroyim held that Congress lacks the power to strip persons of citizenship merely *41 because they have voted in a foreign election. The cornerstone of the decision is the proposition that intent to relinquish citizenship is a prerequisite to expatriation.

12 Section 404(b) would have been declared unconstitutional under either Schneider or Afroyim. The statute is practically identical to its successor, which Schneider condemned as discriminatory. Section 404(b) would have been invalid under Afroyim as a congressional attempt to expatriate regardless of intent. Likewise it is clear that the determination of the Vice-Consul and the State Department in 1952 would have been upheld under then prevailing case law, even though Lucienne had manifested no intent to renounce her citizenship. Mackenzie v. Hare, 239 U.S. 299, 36 S.Ct. 106, 60 L.Ed. 297 (1915). Accord, Savorgnan v. UnitedStates, 338 U.S. 491, 70 S.Ct. 292, 94 L.Ed. 287 (1950). See also Perez v. Brownell, 356 U.S. 44, 78 S.Ct. 568, 2 L.Ed.2d 603 (1958), overruled, Afroyim v. Rusk, supra.

411 F.Supp. at 1293. However, the district court went too far in viewing the equities as between Lucienne and the government in strict isolation from broad policy considerations which argue for a generally retrospective application of Afroyim and Schneider to the entire class of persons invalidly expatriated. Cf. Linkletter v. Walker, supra. The rights stemming from American citizenship are so important that, absent special circumstances, they must be recognized even for years past.Unless held to have been citizens without interruption, persons wrongfully expatriated as well as their offspring might be permanently and unreasonably barred from important benefits.6 Application of Afroyim or Schneider is generally appropriate.* * *

During the interval from late 1949 to mid-1952, Lucienne was unaware that she had been automatically denaturalized.

* * *

Fairness dictates that the UnitedStates recover income taxes for the period November 10, 1949 to May 20, 1952. Lucienne was privileged to travel on a UnitedStates passport; she received the protection of its government.

_

It’s quite interesting that the Court uses and focuses on fairness as to the U.S. government, more than a discussion of “fairness” to the individual. The use of the passport seems to be an integral fact. Here, the Court determined she was retroactively a U.S. citizen and hence subject to taxation on her worldwide income during those crucial periods (1949 through 1952) even though (1) the U.S. Department of State said she was not a U.S. citizen during that time, and (2) she stated “I have never considered myself to be a citizen of the UnitedStates.”

_

101112 Although the government has not appealed the decision with respect to taxes from mid-1952 through 1958, the district court was presented with the issue. We wish to explain why the government should be allowed to collect taxes for the two and one-half year interval but not for the subsequent period. The letter from Lucienne to the Department of State official in 1965, which appears in English translation in the record, states that after the Certificate of Loss of Nationality, “I have never considered myself to be a citizen of the UnitedStates.” We think that in this case this letter can be construed as an acceptance and voluntary relinquishment of citizenship. We also find that in this particular case estoppel would have been proper against the UnitedStates. Although estoppel is rarely a proper defense against the government, there are instances where it would be unconscionable to allow the government to reverse an earlier position. Schuster v. Commissioner of Internal Revenue, 312 F.2d 311, 317 (9th Cir. 1962). This is one of those instances. Lucienne cannot be dunned for taxes to support the UnitedStates government during the years in which she was denied its protection. In Peignand v. Immigration and Naturalization Service, 440 F.2d 757 (1st Cir. 1971), this court refused to decide whether estoppel could apply against the government. A decision on the question was unnecessary, since the petitioner had not been led to take a course of action he would not otherwise have taken. Id. at 761. Here, Lucienne severed her ties to this country at the direction of the State Department. The right hand will not be permitted to demand payment for something which the left hand has taken away. However, until her citizenship was snatched from her, Lucienne should have expected to honor her 1952 declaration that she was a taxpayer.

_

Of particular note, the Court highlighted that the Department of State (one hand) cannot take away citizenship, the individual’s passport and issue a certificate of loss of nationality (“CLN”), and the IRS (on the other hand) impose taxation for the time period after the CNL was issued.

–

One point of emphasis by the Court was how U.S. citizenship rights are a highly protected right; as articulated by the U.S. Supreme Court. That high protection granted, serves to aid those individuals who defend against a government arguing they somehow ceased to be a U.S. citizen. Of course, for those trying to escape U.S. taxation, the result is not a desired one “. . . a curious situation, since usually it is the individual who claims citizenship and the government which denies it. . . “

In addition, the second quarter saw a total of 460, for a cumulative total for the year (mid way through the year of 1,795). At this pace, the year 2015 could be a slight record of U.S. citizenship renunciations compared to the record year of 2014.

The names of each citizen can be located in the list published in the Federal Register.

There are a number of key considerations and strategic decisions that most all U.S. citizens need to consider prior to renouncing citizenship. See, for instance –

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).