Certification Requirement of Section 877(a)(2)(C)

Does IRS Notice 2009-85 regarding expatriation have the “force of law”?

The above statement may sound quite provocative, until one explores in more detail some of the basic principles identified by the U.S. Supreme Court.

IRS Notice 2009-85 is the guidance issued by the IRS after Section 877A was adopted in 2008 and attempts to address a number of issues regarding the mark to market rules. This IRS Notice is a type of so-called “IRB” guidance (Internal Revenue Bulletin). Other IRS guidance that falls into this “IRB” guidance category includes revenue rulings and revenue procedures.

Two key Supreme Court cases, Mayo Clinic and Home Concrete and the 3rd Circuit Cohen decision, among many others, help articulate when such IRS authority is valid, and when it can be successfully challenged by taxpayers. A thoughtful law review article by Kristin Hickman, Unpacking the Force of Law, articulates in much detail the law in this regard and when IRS guidance, specifically including IRS Notices are subject to other U.S. laws, including the Administrative Procedures Act (“APA”).

Below is a list of some of the provisions of IRS Notice 2009-85 that seem to fall outside the language of the statute:

- A covered expatriate who is required to file Form 8854 for such taxable year will be considered to have timely filed Form 8854 if it is filed by the due date of the original Form 1040NR or Form 1040 (including extensions) for such taxable year. Covered expatriates who are U.S. citizens or long-term residents for only part of the taxable year that includes the day before the expatriation date must file a dual-status return.

-

D. Interaction with treaties

Section 877A(f)(4)(B) provides that a covered expatriate shall be treated as having waived any right to claim any reduction under any treaty with the United States in withholding on any distribution to which section 877A(f)(1)(A) applies unless the covered expatriate agrees to such other treatment as the Secretary determines appropriate.

What are the consequences if a former USC or LPR does not comply with one or more of the above requirements that are only set forth in a Notice and not the statute?

Can the IRS make a determination that the taxpayer is a “covered expatriate”, even if they otherwise do not meet the asset or tax liability thresholds?

There is no “timely filed” requirement in the statute or even an inference in it, as to the time and effective nature of notifying the IRS?

Can the IRS successfully argue that the certification requirement of Section 877(a)(2)(C) has not been satisfied and the individual is a “covered expatriate” if IRS Form 8854 is not “timely filed” as defined by the IRS in the Notice?

Must a taxpayer necessarily agree to “such other treatment as the Secretary determines” appropriate, even if such determination is contrary to the terms of an applicable income tax treaty? Can the Secretary unilaterally override the terms of an income tax treaty negotiated between two countries?

These and other questions remain as a result of IRS Notice 2009-85.

???????????????? ?Please click here to view the above in Chinese.?

Did she “relinquish” or “renounce” U.S. citizenship? – Tina Turner –

There are important legal differences between “renouncing” and “relinquishing” U.S. citizenship. Specifically, the federal tax consequences that follow from one versus the other can be quite important. The principle point is the “timing” of when USC status terminates.

The federal tax reporting can be quite different for those who “relinquish” or “renounce” U.S. citizenship. For related background information see the following:

*

Certifying Under Penalty of Perjury – Meeting the Requirements of Title 26 for Preceding 5 Taxable Years

*

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

*

What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

*

More posts to following regarding “relinquishing” or “renouncing” U.S. citizenship.

Certifying Under Penalty of Perjury – Meeting the Requirements of Title 26 for Preceding 5 Taxable Years

The statutory language of Section 877(a)(2)(C) provides that the individual will be a “covered expatriate” if he or she ” . . . fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The reference to “this title” is to Title 26, which is commonly known as the “Internal Revenue Code” and covers all provisions of federal tax law and taxes, including income, estate, gift, excise, employment, alcohol and tobacco, etc. The complexity of the law is discussed below at the bottom of this post.

This provision is commonly forgotten by two groups of individuals.

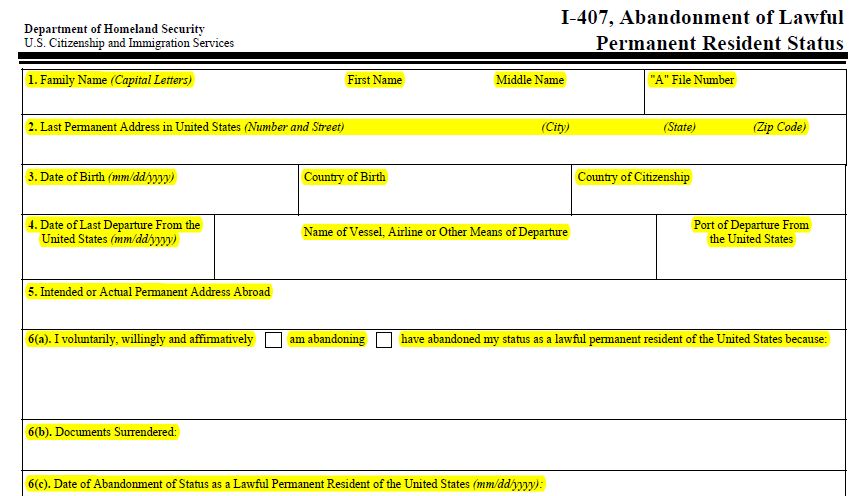

1. Lawful permanent residents (“LPRs”) who abandon their status formally by filing Form I-407 or

by application of a U.S. income tax treaty and IRC Section 7701(b)(6). See, U.S. TAX TREATIES AND SECTION 6114: WHY A TAXPAYER’S FAILURE TO “TAKE” A TREATY POSITION DOES NOT DENY TREATY BENEFITS

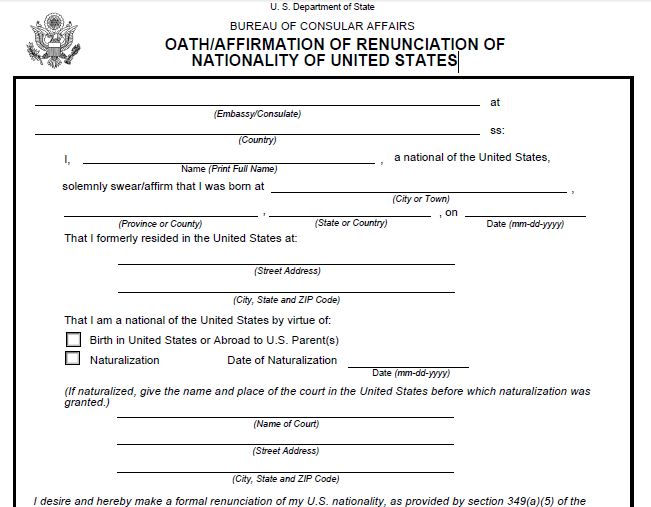

2. U.S. Citizens (“USCs”) who renounce or relinquish their U.S. citizenship status; via the U.S. Department of State.

Filing Form DS-4080, Oath of Renunciation of the Nationality of the United States is a requirement for renunciation.

Under current law, both of these groups of individuals need to certify they have “met the requirements” of the tax law for the five preceding years. How can any taxpayer feel comfortable they have met the requirements of such a complex law?

What steps does an individual in one of the above categories need to take to help assure they have met this requirement? See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms for a basic overview of the foreign earned income law and forms, foreign tax credit law and forms and information reporting requirements under Title 26.

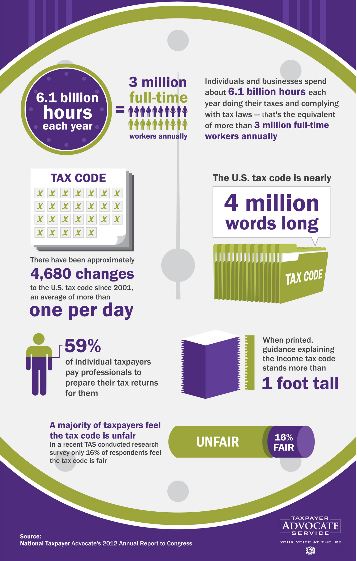

The Taxpayer Advocate Report identifies many of the complexities of this tax law, Title 26:

1. The Current Tax Code Imposes Huge Compliance Burdens on Individual

Taxpayers and Businesses.

Consider the following:

?? According to a TAS analysis of IRS data, individuals and businesses spend about 6.1 billion hours a year complying with the filing requirements of the Internal Revenue Code.7 And that figure does not include the millions of additional hours that taxpayers must spend when they are required to respond to IRS notices or audits.

?? If tax compliance were an industry, it would be one of the largest in the United States. To consume 6.1 billion hours, the “tax industry” requires the equivalent of more than three million full-time workers.8

?? Compliance costs are huge both in absolute terms and relative to the amount of tax revenue collected. Based on Bureau of Labor Statistics data on the hourly cost of an employee, TAS estimates that the costs of complying with the individual and corporate income tax requirements for 2010 amounted to $168 billion — or a staggering 15 percent of aggregate income tax receipts.9

?? According to a tally compiled by a leading publisher of tax information, there have been approximately 4,680 changes to the tax code since 2001, an average of more than one a day.10

?? The tax code has grown so long that it has become challenging even to figure out how long it is. A search of the Code conducted using the “word count” feature in Microsoft Word turned up nearly four million words.11

?? Individual taxpayers find return preparation so overwhelming that about 59 percent now pay preparers to do it for them.12 Among unincorporated business taxpayers, the figure rises to about 71 percent.13 An additional 30 percent of individual taxpayers use tax software to help them prepare their returns,14 with leading software packages costing $50 or more. For 2007, IRS researchers estimated that the monetary compliance burden of the median individual taxpayer (as measured by income) was $258.15

???????????????? ?Please click here to view the above in Chinese.?

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

Probably the most misunderstood concept in the U.S. tax expatriation law provisions is Section 877(a)(2)(C) for several reasons.

1. People of modest means with modest to little income and little to no assets can fall into this category.

2. Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45

3. Lawful permanent residents (“LPRs”) can inadvertently fall into this category without doing anything, other than living principally in a country outside the U.S., which has a U.S. income tax treaty. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9. At the end of this post is a list of the countries with U.S. income tax treaties.

4. Few individuals understand exactly what must be included and reported in IRS Form 8854 to be able to satisfy the certification requirement above. For more details, see What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

The relevant provisions of Section 877(a)(2)(C) are highlighted below:

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Failure to certify truthfully about compliance with U.S. tax law for 5 years, as set forth above in the statute, means the individual necessarily will be a “covered expatriate.” Does this mean that if a U.S. citizen who renounces citizenship or a LPR who abandons their green card, will necessarily be a “covered expatriate” if they fail to follow IRS Notice 2009-45 “Guidance for Expatriates Under Section 877A”?

What steps will the IRS take if someone intentionally does not comply with the certification requirement? Will they become a target of a criminal investigation, and under what circumstances? What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

There are many pending and open questions not answered by current law, as the U.S. Treasury has yet to publish regulations under Section 877A, 877 or 2801.

APPENDIX – Countries with Income Tax Treaties with the United States

Armenia

Australia

Azerbaiján

Bangladesh

Barbados

Belarus

Belgium

Bermuda

Canada

People’s Republic of China

Cyprus

the Czech Republic

Denmark

Egypt

Estonia

Finland

France

Germany

Georgia

Greece

Hungary

Iceland

India

Indonesia

Protocol

Ireland

Israel

Italy

Jamaica

Japan

Kazakhstan

Latvia

Lithuania

Luxembourg

Mexico

Morocco

Netherlands

New Zealand

Norway

Pakistan

Philippines

Poland

Portugal

Romania

Russia

Slovak Republic

South Africa

South Korea

Spain

Sir Lanka

Sweden

Switzerland

Thailand

Trinidad and Tobago

Tunisia

Turkey

Ukraine

United Kingdom

Venezuela

???????????????? ?Please click here to view the above in Chinese.?

What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

Many lay p ersons are stumped as they try to understand the tax consequences of Sections 877 and 877A. The language in the drafting of the statutes is not so clear. Be careful to understate the meaning and how the IRS interprets the law.

ersons are stumped as they try to understand the tax consequences of Sections 877 and 877A. The language in the drafting of the statutes is not so clear. Be careful to understate the meaning and how the IRS interprets the law.

One of the greatest risks for anyone who wants to self-diagnose their path towards becoming a former U.S. citizen, is Section 877(a)(2)(C). To be blunt, anyone who renounces their citizenship at the Embassy or Consulate will find that process relatively easy. However, no one at the U.S. Department of State will provide tax advice or try to interpret the meaning of Section 877(a)(2)(C). Indeed, the Foreign Affairs Manual used to read to the person taking the oath, simply provides the standard overview language of “special tax consequences” arising form the renunciation.

Even the most economically modest individual, with little assets or income, can fall into this trap for the unwary – Section 877(a)(2)(C). The statute is spelled out below –

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

One of the greatest traps for the unwarry is how Section 877(a)(2)(C) can cause even the most economically modest person to become a “covered expatriate” with the adverse tax and reporting requirements that follow.

One of the greatest traps for the unwary is how Section 877(a)(2)(C) can cause even the most economically modest person to become a “covered expatriate” with the adverse tax and reporting requirements that follow.

All individuals should have a clear understanding about how this specific code section can affect their personal taxes and the future taxes of any future gifts or bequests/inheritances to U.S. beneficiaries. All U.S. citizen or U.S. resident children, grandchildren and friends and family of the “expatriate” who fall into this “Section 877(a)(2)(C) trap” will likely be subject to the 40% tax on “covered gifts” or “covered bequests.” This can come as a real surprise years after the “renouncing” citizenship or “abandoning” lawful permanent residence status.

- ← Previous

- 1

- …

- 4

- 5