Certification Requirement of Section 877(a)(2)(C)

More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. – -(What if there are No Records?)

The statutory rules of PFICs are set forth in 26 U.S. Code § 1297 – Passive foreign investment company. The U.S. Treasury and IRS also published new regulations in January 2014 on PFICs.

For an overview, see “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

United States Citizens living overseas, whether or not they are “Accidental Americans”, as well as lawful permanent  residents (LPRs) living outside the U.S. generally have the burden of proof under U.S. tax law to show they complied with U.S. law. Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

residents (LPRs) living outside the U.S. generally have the burden of proof under U.S. tax law to show they complied with U.S. law. Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

This presumption of correctness was confirmed by the U.S. Supreme Court and therefore imposes the burden on the taxpayer of proving that the assessment made by the IRS is erroneous. During my career, I have seen plenty of erroneous assessments made by the IRS, and an increasing number of assessments made against taxpayers residing in countries throughout the world, be it France, Australia, Canada, Russia, Germany, Mexico, Thailand, Japan, Hong Kong, etc.

Why is this presumption of correctness relevant, when PFICs are explained and discussed here? The law of PFICs is complex, to the point that very few IRS revenue agents really have any detailed understanding of how PFICs work, when they apply and how taxpayers are to report their investments in PFICs. Very few U.S. tax practitioners understand PFICs.

Accordingly, I regularly see errors made by the IRS in proposed tax assessments, including PFIC calculations. Unfortunately for the individual taxpayer, they must prove the IRS is wrong in its tax assessment.

PFICs create a real burden on individual taxpayers who have shares in a PFIC in different locations around the world, since it is rare that foreign companies, investment funds, mutual funds and the like ever provide any detailed accounting of (a) asset, or (b) income information (per U.S. tax rules) that are required to be reported by PFIC investors who are USCs or LPRs.

Unlike a controlled foreign corporation (CFC), a PFIC has no ownership threshold. If a USC owns just 1,000 shares/units out of 20M issued shares in a foreign mutual fund, the U.S. citizen will nevertheless need to report this 1,000 share/unit interest (even though this is only 0.0005% of the fund) on his or her individual income tax return if the foreign mutual fund meets – the income test or asset test. Virtually all mutual and investments funds will satisfy these tests, since by definition the funds are making investments in other companies or other passive income items, such as bonds, stocks, futures, ETFs, etc.

The income test is met when at least 75% of the income is passive income as defined under the law. The asset test is satisfied when at least 50% of the foreign corporation’s average assets produce such passive income.

The practical problem arises when the individual taxpayer needs information from the fund (or other foreign entity) that reflects information such as –

- the pro-rata share of the “ordinary” earnings (in the example above, just 1,000 share/20M shares – 0.0005% of the fund);

- the pro-rata share of the “net capital gain”;

- the total cash or property distributed;

- the total cash or property “deemed” distributed (which means there was actually no distribution – but the law “deems” there to have been a distribution); and

- many other complex calculations that require basic information to be provided by the PFIC in the first place.

What foreign fund or investment company around the world (located in whatever country – catering to customers commonly in their own country) even tracks or accounts for income and gains for U.S. tax law purposes; i.e. “ordinary” earnings versus “capital gains” – specifically including the netting of “capital gains” and “capital losses” as required by U.S. law? I certainly do not see such accounting records provided in the marketplace of investment funds, hedge funds and companies that cater to persons residing outside the U.S.

Most foreign companies around the world (unless they are controlled and managed by USCs who are aware of these U.S. tax obligations) never maintain such accounting records or the detailed information necessary to even provide it to their USC or LPR investors. Hence, USCs/LPR investors may never be able to accurate make these PFIC calculations.

Also, the ownership of shares/units of the fund might always be changing throughout the year. In other words, even if the “ordinary income” and “net capital gain” is available for a particular fund/PFIC, the total number of outstanding shares/units has to be stable or known for the USC or LPR to calculate their pro-rata share. In the above example, if there are 20M outstanding shares/units at the beginning of the year, but by the end of the year there are 22M outstanding shares/units, how is the USC or LPR investor ever going to be able to calculate their pro-rata share, assuming they have the “ordinary” earnings and “capital gains” amounts for the entire calendar year? Its not simply the “ordinary” earnings and “capital gains” multiplied by 0.0005%.

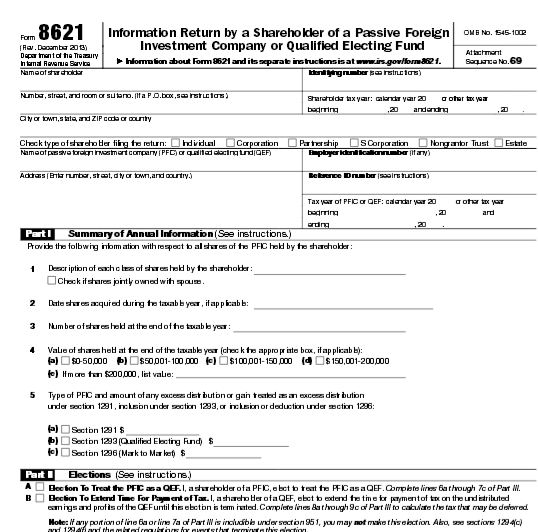

The only “good news” in this explanation of PFICs, is that there is not an automatic US$10,000 penalty for failure to file their investments in a PFIC on IRS Form 8621, Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund.

This is a departure from the normal rule of a minimum US$10,000 penalty for failure to file information returns regarding international (i.e., non-U.S. assets and investments). See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms.

All of these tax compliance rules begs a very important question for a USC who is considering renouncing their U.S. citizenship. The issue arises if they have had investments in PFICs during the last five years. If the USC has not been complying with IRC Section 1297 regarding PFICs, how can the taxpayer ever certify under penalty of perjury ” . . . that he has met the requirements of this title for the 5 preceding taxable years. . . [for purposes of Section 877(a)(2)(C)]”?

More details about PFICs to come in later posts.

IRS Sting Operation and Criminal Tax Indictments of Canadian Citizens – Investigations Overseas – Enabling U.S. Taxpayers with Offshore Accounts

The U.S. Department of Justice reported that two Canadian citizens along with a U.S. citizen were indicted for enabling tax evasion with offshore accounts. The press release from three months ago, 24 March 2014, can be reviewed here. Some highlights of the press release are below:

- According to the indictment, . . . Poulin, an attorney at a law firm based in Turks and Caicos, worked and resided in Canada and in the Turks and Caicos. His clientele also included numerous U.S. citizens.

- According to the indictment, Vandyk, St-Cyr and Poulin solicited U.S. citizens to use their services to hide assets from the U.S. government. Vandyk and St-Cyr directed the undercover agents posing as U.S. clients to create offshore foundations with the assistance of Poulin and others because they and the investment firm did not want to appear to deal with U.S. clients. Vandyk and St-Cyr used the offshore entities to move money into the Cayman Islands and used foreign attorneys as intermediaries for such transactions.

- According to the indictment, Poulin established an offshore foundation for the undercover agents posing as U.S. clients and served as a nominal board member in lieu of the clients.

The facts of this case will be interesting to cover, to see how and to what extent the IRS and Justice Department will be focusing on U.S. citizens residing overseas and their reporting (or failure to report) their “foreign” accounts; i.e., their financial accounts in their home countries of residence.

Since the withholding tax provisions under the Foreign Account Tax Compliance Act (“FATCA”) come into effect in a matter of days, it will be interesting to see if the government has more indictments along these lines planned for the summer of 2014.

U.S. citizens who are in the process of renouncing citizenship should be aware of each of the steps required as part of the process; both under U.S. federal tax law and immigration law.

Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute

People who cite to IRS forms, should have an appreciation that neither the form or its conditions may have the “force of law.” This is particularly important, when the statute itself, regarding the Certification Requirement of Section 877(a)(2)(C) does not specific whether the certification has to be made “prior to” (or after) the date of loss of nationality? See the relevant provision of the statute below – Section 877(a)(2)(C), which causes an individual to be a “covered expatriate” if::

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Consider the language of the instructions of IRS Form 8854, however, which expressly states that the certification must reflect you have ” . . . complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.”

Does this mean the IRS requires the compliance to have been satisfied prior to the expatriation/renunciation date? That is what the instructions say.

See the bottom of page 2 of the Form 8854 instructions –

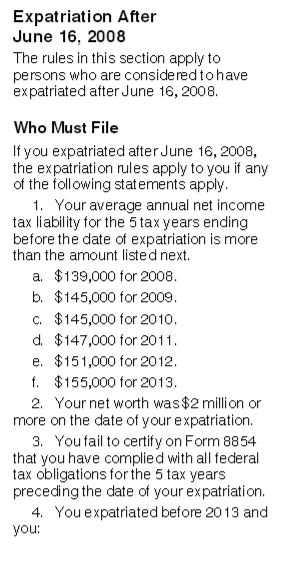

“If you expatriated after June 16, 2008, the expatriation rules apply to you if any of the following statements apply.

1. Your average annual net income tax liability for the 5 tax years ending before the date of your expatriation is more than the amount listed next . . .

2. Your net worth is $2 million or more on the date of your expatriation.

3. You fail to certify on Form 8854 that you have complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.”

In this case, the instructions to the form, say the former USC or LPR must ” . . . have complied with all of your federal tax obligations preceding the date of your expatriation. . . ”

If this statement were true, a taxpayer could not satisfy the rule by attempting to comply with all federal tax obligations after they have renounced their U.S. citizenship?

In other words, if such were true, attempting to comply with all provisions of the U.S. federal tax law for 5 years and then filing 8854, all after taking the oath of renunciation, would prohibit someone from avoiding “covered expatriate” status?

Importantly, the Treasury/IRS cannot create law by merely publishing a substantive rule in an IRS Form. Indeed, there are no regulations to date; that have been issued by the Treasury; only a few notices. See prior post, Does IRS Notice 2009-85 regarding expatriation have the “force of law”?

Of course, this does not mean the IRS will not challenge any former USC as not complying with Certification Requirement of Section 877(a)(2)(C) by not also complying with the condition set forth in the IRS own instructions?

This is an example of an important detail that any former USC will want to carefully consider prior to rushing off to take the oath of renunciation.

As always, see Limitations.

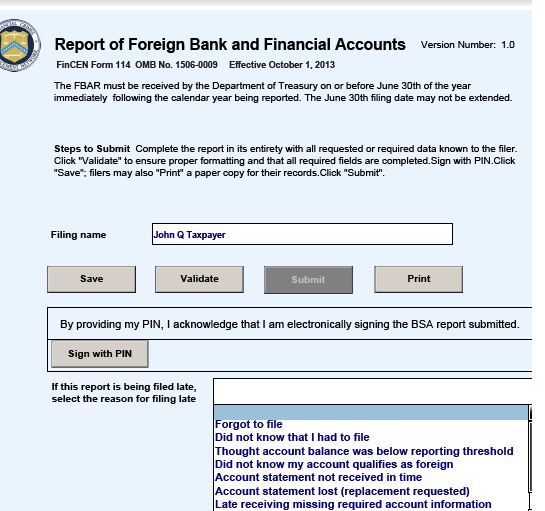

Why the FBAR (late filed or never filed) is not a requirement for the Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance)

Myths abound about how and when the certification requirements must be satisfied under Section 877(a)(2)(C), in order to avoid “covered expatriate” status. See a previous post, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

One common notion, is that if a USC or long-term LPR has not filed foreign bank account reports (“FBARs”) pursuant to Title 31, they will not be able to make the certification as required by the statute – Section 877(a)(2)(C), which causes an individual to be a “covered expatriate” if:

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Importantly, the statutory reference to “this title” is a reference only to “Title 26, Internal Revenue Code,” i.e. the federal tax laws. It is not a reference to any other “Title” of the federal laws. The federal statutory laws are organized by “Titles“; e.g., Title 8 is “Aliens and Nationality” (i.e., immigration law) and Title 7 is “Agriculture”, etc.

Specifically, Section 877(a)(2)(C) of the tax law, does not also require the individual to be able to certify his or her compliance with any other title for the preceding 5 years, such as Title 31 Money and Finance: Treasury.

Title 31 is the law that creates the FBAR filing requirements and is known as the “Money and Finance: Treasury.”

Accordingly, someone who has not filed FBARs, i.e., and not complied with Title 31 or Title 7 (e.g., regarding “Agriculture”) will not be barred from being able to comply with the tax requirements of Section 877(a)(2)(C), if they have complied with “Title 26, Internal Revenue Code, i.e. the federal tax laws. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

To put this into a concrete example, assume a USC living in Canada has filed complete and accurate U.S. federal income tax returns for the years 2008 through 2013; but never filed any FBARs regarding the Canadian corporate accounts over which the individual has had signature authority. Maybe this individual’s Canadian accounts also exceeded US$10,000 in at some point through the year? Nevertheless, if he or she renounces their U.S. citizenship in 2014, they should nevertheless, be able to avoid “covered expatriate” status by complying with Section 877(a)(2)(C), even though they failed to comply with Title 31 requirements.

As always, see Limitations.

Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Probably most “Accidental Americans” around the world do not and have not filed U.S. federal income tax returns during their lifetimes. A most important issue for these individuals who are considering renouncing their USC, is whether they can satisfy the statutory requirement (set out below) late; i.e., “after the fact” – if they have not previously filed tax returns?

See the relevant provision of the statute below:

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Can an “Accidental American” who has lived almost all of their lives outside the U.S., and who has never filed U.S. income tax returns satisfy the statutory language “. . . of the the requirements of this title [Title 26 – Federal Tax Laws] for the 5 preceding taxable years. . . “?

Some interpret the statute to say that filing late income tax returns (e.g., in 2014 for the years 2009 through 2013/2014) should be permissible, provided the former USC indeed satisfies all of the requirements set forth in the law at some later point in time.

Will the IRS argue late filings of tax returns means the taxpayer has not met the requirements of Title 26? Will they argue that a failure to file a timely return and violation of Section 6651 means such an individual did not meet the requirements of the law? See, § 6651 – Failure to file tax return or to pay tax, which provides in relevant part –

(1) to file any return required under authority of subchapter A of chapter 61. . . on the date prescribed therefor (determined with regard to any extension of time for filing), unless it is shown that such failure is due to reasonable cause and not due to willful neglect, . . .

Will the IRS or Tax Division, Justice Department lawyers argue that any federal tax returns that are not timely filed under Section 7502, means that a former USC cannot have satisfy the statutory language of “. . . the requirements of this title [Title 26 – Federal Tax Laws] for the 5 preceding taxable years. . . “?

Obviously, the stakes can be very high for any such former U.S. citizen (or LPR), due to the consequences of being deemed a “covered expatriate.” See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

The point of this post is to explain why “covered expatriate” status does matter, even for those with no assets. Most people in the world, probably think the tax expatriation provisions only are for the rich, wealthy and worldwide private jet owners. This is how the press (and members of Congress) typically portray those who renounce U.S. citizenship. The press articles typically cover the likes of Ms. Tina Turner and Mr. Eduardo Saverin, co-founder of Facebook. See,Tina Turner – Famous People Who Renounced U.S. Citizenship.

Most articles focus on the “net worth test” (US$2M) and the “income tax liability test” (“US$125K+/-). See, Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C).

Unfortunately, U.S. “expatriation tax law”, applies to the poorest former U.S. citizen (and certain long-term LPRs), wherever they reside if they do not comply with the certification requirements of Section 877(a)(2)(C). See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal, CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

So far so clear? But you are surely asking yourself, “this does not explain how this costs me any money or taxes, if I have no assets to begin with . . . “?

If the certification requirements are not satisfied, the individual with no assets should have no U.S. income tax to pay as he or she will have no unrealized gains. If there are no “unrealized gains”, there can be no tax base and hence no income tax caused by the “mark to market regime”.

However, there are two points of potential taxation under the law. First, when the USC or LPR leaves the U.S. (“expatriates”); which does not cause taxation in this example for the individual without “unrealized gains.” However, there is second point of taxation, under the law, which arises when a U.S. person receives a covered gift or bequest. IRC Section 2801. This might not happen until decades into the future, long after the expatriation event.

Incidentally, someone could have significant assets, without any unrealized gains. Both individuals (the rich and the poor) would be in the same position as they leave/expatriate from the U.S.; i.e., and have no U.S. income tax to pay. For instance, USC “A” with US$5,000 in total assets, would have the same income tax to pay ($0) as USC “B” with US$15M of cash in the bank; assuming no other assets. Neither would have unrealized gains upon which to cause any U.S. tax. This is because US dollars/”cash” have a tax basis – the same as the currency amount. Hence, there is no unrealized gains in US dollars-cash.

However, if in this case, assume both individuals (USC “A” and USC “B”) cannot satisfy the certification requirements of Section 877(a)(2)(C), and hence both would be “covered expatriates.” So what does that mean to them during their lifetimes (what U.S. tax might they have to pay)?

The potential U.S. tax created to both USC “A” and USC “B” in this circumstance, is IF AND WHEN, they were ever to make a future gift or bequest (directly or indirectly – e.g., through trust) to a U.S. person. At that point in time, the U.S. beneficiary will have to pay effectively a 40% tax on the fair market value of the property received. This tax is created under Internal Revenue Code Section 2801, that was passed in 2008. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” A common example is a child or sibling who is a dual national, who might inherit assets in the future.

The 40% tax is a lot of tax to pay – as there are virtually no deductions or exemptions from the amount of tax paid.

I have proposed a series of recommendations to the Treasury regarding concepts and provisions that hopefully will be incorporated into their propose regulation project under Section 2801. More to come on this important topic.

You might say – “I have no future U.S. beneficiaries and/or I have no assets. Why do I care?”

Very simply, you should care, if –

- You may grow your future assets (or inherit assets from others) while not being a U.S. citizen (post-expatriation). If that is your goal or your lot in life, you might end up with much more in assets than you have today (assuming you are the same as USC “A” in the example), while having virtually no assets today; and

- You may have family and friends who will become U.S. residents, even if none of them are today.

Assume USC “A” renounces citizenship and in 40 years leaves a bequest to a daughter of US$120,000; the daughter has moved to the U.S. In this case, the U.S. tax law would impose more than a US$40,000 tax on the daughter when she receives the inheritance. This is a very high tax burden to pay, on what is a relatively modest inheritance. This is one, of multiple scenarios of why “covered expatriate” status can be so important – over the long run.

In my practice, over the years, I have seen numerous cases where one single family member moves to the U.S. temporarily for work or study, e.g., graduate school, gets married and decides to stay on and live in the U.S., even for a while. Often times, they will have children, who will be U.S. citizens by birth in the U.S. Hence, a U.S. person is now part of the family tree.

How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854?

How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854?

Can this information be obtained directly from the IRS through a Freedom of Information Act (“FOIA”) request?

See, Does IRS Notice 2009-85 regarding expatriation have the “force of law”? Posted April 14, 2014.

Unfortunately, the law has left much confusion for USCs and LPRs living overseas who have –

- “relinquished” their citizenship many years ago (in the case of USCs), or

- terminated U.S. income tax residency by application of a U.S. income tax treaty (in the case of LPRs).

See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

The one certainty under the law, is that any former USC or LPR, regardless of their wealth or income, will necessarily be a “covered expatriate” if they do not file IRS Form 8854 and meet the certification requirements under the law.

This begs the question: how many have filed IRS Form 8854?

See, Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C). (Posted on April 16, 2014)

The List is Out – and Its 1,001 Former U.S. Citizens for the 1st Quarter 2014

The IRS published today the list of former U.S. citizens for the first quarter of 2014 and it can be reviewed here. It’s a record for any first quarter by 47%.

Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G

This is a record pace from any prior year, considering the entire year of 2013 had a record pace of 2,999 former U.S. citizens for the entire year. The 1,001 listed persons in the first quarter of 2014 is a 47% increase over the 679 former citizens published in the same period a year ago. No other first quarter list had more than 500.

There are a number of interesting questions that are created by this trend.

- Does the IRS have access to the data for former lawful permanent residents? That information is not published under the statute (Section 6039G), which only covers U.S. citizens. Does the Department of Homeland Security track former LPR – names, addresses, etc.?

- Will the IRS simply select the list of published former citizens for audits? The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

- Will the IRS try to locate former long-term lawful permanent residents (LPR) to select for audit? See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents? Posted on March 5, 2014.

- How many former citizens are not included in this quarterly list? The statute provides the names are compiled from data received from the U.S. Department of State and the federal agency principally responsible for immigration, among others..

- How many of these individuals met, or will meet, the certification requirements set forth in Section 877(a)(2)(C)? If the former citizen does not comply with this provision, they will necessarily be a “covered expatriate” with the accompanying adverse U.S. tax consequences. See,Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C). Posted on April 16, 2014

- Related to the above question: How many have filed (or will file) IRS Form 8854? See, Does IRS Notice 2009-85 regarding expatriation have the “force of law”? Posted April 14, 2014.

- How many of these former citizens will be subject to the US$10,000 penalty under Section 6039G(c)?

- How will the IRS collect tax and penalty assessments against individuals who live exclusively outside the U.S.?

There has been a clear trend of a growing list of former U.S. citizens. As more “Accidental Americans” learn they are U.S. tax residents by virtue of their U.S. citizenship, I think the trend will continue. The longer term consequences will be interesting as they unfold.

???????????????? ?Please click here to view the above in Chinese.?

More renounce US citizenship but deny stereotype

This article is quite consistent with the many multinational families I have come across in my practice and even person life. The article can be reviewed in its entirety here at More renounce US citizenship but deny stereotype.

The press and certainly Congress focuses on the handful of wealthy individuals who renounced citizenship to pay less U.S. income, estate and gift taxes. Little focus has been on the millions of middle income or even low income individuals who live around the world and are caught up in the complex U.S. tax (estate, income, gift and inheritance tax and reporting) and bank account reporting legal web.

Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C).

There are many unanswered questions about the tax consequences of Sections 877 and 877A. The language in the statute is not clear as to its meaning for those who file incomplete, fail to file, or fail to “timely file” IRS Form 8854. Be careful to understand the meaning and how the IRS interprets the law.

One of the greatest risks for anyone who thinks they will not be a “covered expatriate” because of the asset test or income tax liability test, is the certification requirements set forth in Section 877(a)(2)(C).

Anyone who renounces their citizenship at the Embassy or Consulate will find that process relatively easy. See forms. However, no one at the U.S. Department of State will provide tax advice or try to interpret the meaning of Section 877(a)(2)(C). Indeed, the Foreign Affairs Manual used to read to the person taking the oath, simply provides the standard overview language of “special tax consequences” arising form the renunciation.

Even the most economically modest individual, with little assets or income, can fall into this trap for the unwary – Section 877(a)(2)(C). The statute is spelled out below –

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

- Did not fully complete or file the information set forth in IRS Form 8854?

- Did not convert the values of the assets and liabilities from the foreign currency where they were held into U.S. dollars?

- What if the former USC or long-term resident does not file a dual-status return for the part of the taxable year that includes the day before the expatriation date?

- What if the tax returns (and hence IRS Form 8854) are filed beyond their normal filing dates required? See filing dates in –IRS Beats the Drums – Re: Foreign Assets, Just Days Before April 15 Posted on April 12, 2014

- What if the date of relinquishment (not renunciation) is a date prior to the year when the last tax return is required to be filed pursuant to IRS Notice 2009-85? For instance, what if the relinquishment date is October 1, 2009 (as reflected by the final Certificate of Loss of Nationality from the U.S. Department of State) and the former USC has to decide how and when to file in the year 2014?

- ← Previous

- 1

- …

- 3

- 4

- 5

- Next →