Certification Requirement of Section 877(a)(2)(C)

Part II: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

· More Myths – about Renouncing U.S. Citizenship

There are many misunderstandings of how the law works when someone renounces U.S. citizenship. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

The author regularly hears a range of myths that will befall an “Accidental American” when and if, they renounce. These “myths” include the following:

- Myth 5: There is no requirement to file U.S. income tax returns if the individual has few assets, little income or has otherwise lived outside the U.S. for almost all of their lives.

- Fact: The old tax law from 1996 and the modifications in 2004 had a 10 year period of taxation concept after “expatriation.” There is no longer such a 10 year period of taxation for those persons who renounce on or after June 17, 2008. However, any former U.S. citizen will necessarily be a “covered expatriate” if they cannot meet the certification requirement of Section 877(a)(2)(C); one of which includes 5 years of compliance with the U.S. tax law. See prior posts explain in more detail – Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the StatuteSee also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

- Myth 6: There is somehow some “magical difference” under the law, for those who “renounce” citizenship (currently) versus those who “relinquished” citizenship (some time in the past) and the U.S. Department of State should recognize this “magical difference”. Such a difference will create a different U.S. tax result.

- Fact: The tax law nor immigration law makes such a distinction, even though this seems to be a common myth frequently spread throughout the Internet.

- Myth 7 : Former U.S. citizens who are “covered expatriates” can gift assets to their U.S. citizen children and friends without U.S. tax costs to them.

- Fact: This is true, i.e., there is no restriction or tax that is levied against the former U.S. citizen who makes the gift. The problem is for the recipient U.S. citizen or other “U.S. person” children or friends who will become subject to tax upon such gifts at the highest estate and gift ta rate (currently 40%).

- Myth 8: Former U.S. citizens should not worry about the IRS and its ability to collect taxes owing for the “mark-to-market” gains tax on expatriation (or on covered gifts and covered bequests) against assets located outside the U.S.?

- Fact: This depends on the particularl factual circumstances of each former U.S. citizen. Where are their assets? Do they (or will they) travel to and from the U.S.? In what country do they regularly reside? See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations and How will the IRS collect tax and penalty assessments against former USCs and LPRs who live exclusively outside the U.S.?

These are just some of the myths commonly floated. There are yet more myths which will be discussed in a later post.

What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

A prior post identified the number of lawful permanent residents (LPRs) who file Form I-407 to formally abandon their lawful permanent residency. See, The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

These numbers of I-407 forms filed annually were obtained through a freedom of Information Act (“FOIA”) request and provided by the USCIS. See tabl:

Of course, this statistic does NOT identify the number of the approximate 13.3+ million LPRs who leave the U.S. to live elsewhere in another country without completing Form I-407 and formally abandoning. The estimated number of LPRs was 13.3 million for the year 2012 as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012.

Maybe the number of individuals who fall into this latter category (i.e., moving out of the U.S. without filing Form I-407) is several hundred of thousands of individuals annually?

Importantly, from a taxation perspective, anyone who moves and lives in a country with a U.S. income tax treaty (the list of these countries is set out below – from the IRS website), needs to be careful not to be deemed to be a “covered expatriate” due to the application of IRS Form 7701(b)(6). See, IRS Notice 2009-85.

See, the following posts with further explanation of the tax law for LPRs who move and live in one of the countries listed below. Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

See also, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Becoming a “covered expatriate” has U.S. tax consequences not just to the “former long-term LPR”, but also to their family and friends who are “U.S. persons” (as defined under Section 7701. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

A

Armenia

Australia

Austria

Azerbaijan

B

Bangladesh

Barbados

Belarus

Belgium

Bulgaria

C

Canada

China

Cyprus

Czech Republic

D

E

F

G

H

I

Iceland

India

Indonesia

Ireland

Israel

Italy

J

K

L

M

N

Netherlands

New Zealand

Norway

O

P

Pakistan

Philippines

Poland

Portugal

Q

R

S

Slovak Republic

Slovenia

South Africa

Spain

Sri Lanka

Sweden

Switzerland

T

Tajikistan

Thailand

Trinidad

Tunisia

Turkey

Turkmenistan

U

Ukraine

Union of Soviet Socialist Republics (USSR)

United Kingdom

United States Model

Uzbekistan

V

“Covered Expatriate” Status is a “Scarlet Letter”

Throughout Tax-Expatriation, I have tried to emphasize the importance of avoiding “covered expatriate” status, if at all possible – and at all costs. It is a technical term defined in the tax law.

“Covered Expatriate” status is a “Scarlet Letter”.

There is much misunderstanding about how the tax expatriation provisions of the law apply. Many people think they only apply to wealthy individuals. This is not the case.

See various posts explaining the importance of the Certification Requirement of Section 877(a)(2)(C):

Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)

Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

As explained throughout, there are many ways for individuals to fall into the “covered expatriate” category. I liken it here to the “Scarlet Letter”. The fictional protagonist in Nathaniel Hawthorne book, could never shed herself of the consequences of her infidelity and wore the Scarlet Letter for life. It had devastating consequences to her, her loved ones around her and especially her daughter.

This is also true for “covered expatriate” status; but it is not fictional. Covered expatriate status can never be shed and can have disastrous consequences not only for the former USC or LPR; but also to the friends and family of the individual who carries around the “covered expatriate” status for life. See, The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

In the book, the protagonist took the Scarlet Letter to her grave and had it on her tombstone. “Covered expatriate” status extends beyond the grave and beyond the tombstone. Any loved one who is a U.S. person of a “covered expatriate” who receives a gift or inheritance, will be subject to a tax; even if the inheritance occurs many years after the death of the covered expatriate. In this case, the Scarlet Letter transfers to the loved one who receives property in the future and continues on for another generation. At least in Nathaniel Hawthorne’s book, the daughter Pearl received an inheritance not tainted by the Scarlet Letter.

The Importance of Planning – PRIOR to Renouncing, Relinquishing or Abandoning

International tax law experts who specialize in a particular area of the law, have a fairly good understanding of the importance of tax planning. The reason is simple. The law is complex and without planning, laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

“Tax expatriation” in the U.S. is particular complex for several reasons:

1. The general rule is that there is an immediate income tax payable from the “mark to market” taxation rules on unrealized gains. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

2. If a tax is recognized under the U.S. tax law, the only way to discharge the liability with the U.S. federal government is to pay the tax owing. The IRS generally can collect an income tax owing against a taxpayer who lives outside the U.S. indefinitely, as the 10 year collection statute does not apply when the individual outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). More on this topic in another post. In other words, the IRS can “forever” pursue the collection of the “expatriation tax” against USCs and LPRs living outside the U.S.

3. It is easy to fall into the general rule of expatriation, even if the taxpayer would not otherwise be subject to income taxation. See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

4. The friends and family of the “covered expatriate” – i.e., the former U.S. citizen and long-term lawful permanent resident can be subject to U.S. taxation during their lifetimes, even if they also live outside the U.S. See also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Each of these points help demonstrate the need for planning prior to running to the U.S. Department of State and completing and filing the following forms when you take the oath of renunciation:

See, Documents to Request the Consular Officer When Renouncing U.S. Citizenship

At the end of the day, if the individual lives outside the U.S. and does not travel to and from the U.S., it may be very difficult (at least practically speaking) for the IRS to collect on the tax judgment owing, if the individual has no assets in the U.S. There are legal means and steps the IRS can take in an attempt to try to collect U.S. taxes on overseas assets.

For a further discussion on collection of taxes overseas:

See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations, and

Ideally, a former U.S. citizen or long-term lawful permanent resident will wish to avoid all of the potential tax and collection issues, by engaging in thoughtful and strategic planning prior to their renunciation of U.S. citizenship or abandonment of lawful permanent residency.

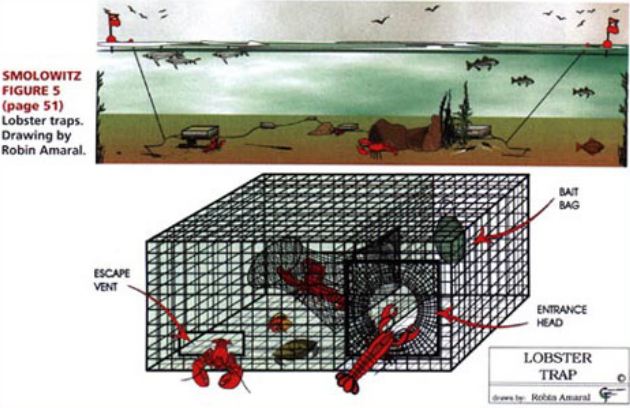

Avoiding the Lobster Pot: Why becoming a Naturalized Citizen or LPR can be the proverbial “Lobster [Tax] Pot”

Two famous tax professors coined a wonderful analogy that can largely be applicable to any non-U.S. citizen who is considering either becoming a (1) lawful permanent resident (LPR), or (2) a naturalized citizen.

Tax professors Boris I. Bittker (Yale) and James S. Eustice (NYU), both of whom are now deceased, wrote –

- “[Under the tax laws] a corporation is like a lobster pot: it is easy to enter, difficult to live in, and painful to get out of.”

I think the same analogy is very much appropriate to a non-U.S. citizen who becomes a LPR or a naturalized citizen, without fully understanding the U.S. federal tax consequences of such a decision. The word “corporation” merely should be changed with “lawful permanent resident” or “naturalized citizen” in the quote from Bittker and Eustice when considering the potential long-term application of the “expatriation tax” rules.

The analogy is particularly applicable for two reasons. First, individuals are usually less sophisticated and, often times, simply unaware of complex tax laws. Corporate taxpayers often can have a better understanding of complex U.S. tax laws – i.e., the “lobster trap” via sophisticated tax advisers.

Second, some lobster traps have an “escape vent” for small lobsters. Similarly, the tax laws on expatriation can treat individuals with smaller amounts of assets or U.S. tax liabilities, very differently and more favorably under the law. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute,

Non-U.S. citizens who are not certain they will spend the rest of their lives in the U.S., should carefully consider if they indeed wish to obtain LPR or become a naturalized citizen. This is because of the long-term tax consequences of Sections 877, 877A, 2801, etc. for those who later abandon their LPR status or renounce their U.S. citizenship.

Of course, this blog, is dedicated to shedding light on the income tax, estate and gift tax, and “covered gift” and “covered” inheritance tax consequences to those who enter the “lobster trap.”

Many more may wish to simply shy far away from the lobster trap to begin with.

Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)

A previous post explained why lawful permanent residents (LPRs) can never satisfy this exception in the law to avoid “covered expatriate status.” See, Why a “long-term” LPR can NEVER avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B) if Asset or Tax Liability Test is Satisfied!

For the same reasons, a naturalized citizen cannot satisfy the statutory requirement since they will never be able to meet the IRC Section 877A(g)(1)(B)(i)(I) requirement of becoming ” . . . at birth a citizen of the United States . . . ”

See the relevant provisions of the statute as follows:

(B) Exceptions

Of course a naturalized United States citizen by definition was not a citizen at birth and only became one upon completing the lengthy legal requirements of naturalization. See, USCIS website – Citizenship Through Naturalization

Posted on May 19, 2014

.

529 College Plans – Funded by Former USCs and LPRs (“Long-Term” LPRs)

There is a basic tax planning opportunity for U.S. taxpayers who wish to fund the costs of higher education for family or friends. These are referred to as “529 Plans” with reference to the tax code section – IRC Section 529. In short, a 529 trust is established and funded with contributions for the benefit of named beneficiaries.

The principle benefit of a 529 plan, is that the income earned from the investments inside the 529 trust fund are exempt from U.S. income taxation.

There are multiple plans that are operated by various institutions, principally in conjunction with various States in the United States. Qualifying higher education expenses also apply to about 350 non-U.S. institutions that currently qualify for distributions out of a 529 Plan; e.g., University of Cambridge, University of Dublin Trinity College, University of Edinburgh, University of Oslo, The University of York, University of Wollongong, etc.

Unfortunately, non-U.S. citizens who are not resident in the U.S. generally are not eligible to establish and form a new 529 plan.

These “529 Plans” fall expressly into the category of a “specified tax deferred account” under the law. See, IRC Section 877A(e)(2).

In short, the law causes the entire amount in the 529 Plan to be treated as distributed to the “covered expatriate” the day before the expatriation date, although no early distribution tax will apply. If a 529 Plan has $500,000, that will represent taxable income to the “covered expatriate” to the extent of the tax-free growth in the plan. For instance, if the individual funded $200,000 into this plan, in this example, and he or she is subject to the 39.6% tax rate upon “expatriation”, this means there will be US$118,800 less to pay for college and universities (i.e., $500,000 less the $200,000 invested; leaving $300,000 X 39.6% = US$118,800 of tax).

This is yet another example, of how and why it is so important to avoid “covered expatriate” status; if permitted by the law in any particular circumstances. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute, also see Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Careful thought should be taken for the range of considerations and U.S. tax consequences that can befall a former USC or long-term LPR.

Ineligibeility for a SSN after Taking Oath of Renunciation – TINs, ITINs, EINs, etc.

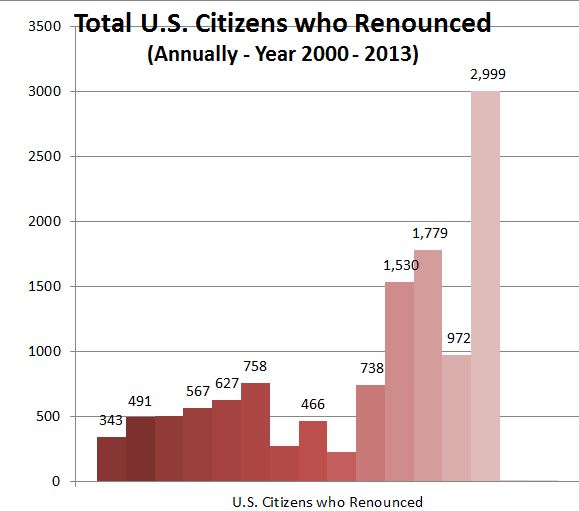

USCs and LPRs residing outside the U.S. have been increasingly renouncing their citizenship and abandoning their lawful permanently residency status, respectively. In some cases, individuals who have lived virtually all (or all) of their lives in a country other than the U.S. are a lmost making a “knee jerk” decision to renounce.

lmost making a “knee jerk” decision to renounce.

The statistics as to the absolute number and relative increases are astonishing. See, Wow, the number of 2,999 U.S. citizens who renounced in the year 2013 shattered the prior record set in 2011 of 1,782 renunciations. Why so many renunciations?

There is a practical problem for an individual who has renounced his or her U.S. citizenship prior to obtaining a Social Security Number (“SSN”). The individual will NOT be able to obtain a SSN once they have taken the oath of renunciation. See, *Why the Oath of Renunciation is Not the Opposite of the Oath of Allegiance

Of course, as prior posts have explained, an individual must have a “taxpayer identifying number” which must be a SSN for a U.S. citizen. However, the Social Security Administration will not allow an individual who has taken the oath of renunciation to apply for a SSN. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs

Also, see, Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The only way an individual can avoid becoming a “covered expatriate” is by filing U.S. federal income tax returns and being able to satisfy the certification requirement of Section 877(a)(2)(C). Accordingly, if a SSN is not available, the former citizen will need to file for an ITIN, as explained in previous posts.

IRA Distributions – (Counter-intuitive Results) U.S. Tax Consequences to Former USCs and Long Term Residents (LPRs)

IRA Distributions – (Counter-intuitive Results) U.S. Tax Consequences to Former USCs and Long Term Residents (LPRs)

Those USCs who have renounced citizenship (or who are contemplating renunciation) and those LPRs who (were/are/will) fall into the category of “long-term residents” who have qualified retirement accounts, known as “Individual Retirement Arrangement” (“IRAs”) have special considerations to consider under IRC Sections 877, et. seq. For more details on how IRAs work and the deduction limits, see the IRS website explanation.

In short, if an individual is a “covered expatriate” upon renunciation (or LPR abandonment), they will generally be subject to U.S. income taxation on the entire amount of the IRA (along with all other assets with unrealized gains), reduced by the exemption amount (currently US$680,000 for the year 2014).

Unfortunately, it is fairly easy to become a “covered expatriate” even if the asset or tax liability tests are not satisfied, simply if the individual fails to satisfy the certification requirement under Section 877(a)(2)(C). There are multiple posts that address this important certification requirement of Section 877(a)(2)(C), irrespective of how poor or how few of assets might be held by the individual. See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute, also see Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Plus, the topic is covered yet further in More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

Generally “covered expatriate” status is to be avoided, give the various adverse tax consequences. See, for instance, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

However, since the U.S. tax law is complex and oftentimes full of unintended consequences, there may be times when “covered expatriate” status is desirable in any particular circumstance. I have seen and advised on several; including scenarios, where some planning steps can help get a much better U.S. tax result in various cases.

Assume a former USC does not meet the certification requirement (e.g., since they neglected to properly file a complete and accurate IRS Form 8854, or they otherwise did not comply with Title 26 for one or more of the five years preceding the renunciation/abandonment). Further, let us assume, she has an IRA with a total value of US$1.4M and all of her other assets have no unrealized gain (e.g., Euros in a bank in Europe and an apartment she purchased in her country of residence in Europe that continues to have depressed real estate prices). These other assets, the apartment and Euros are US$500,000 in value; hence, less than the US$2M net worth threshold. However, we will assume she did not timely comply with the certification requirements under the law.

In such an “unfortunate” case, she would have to accelerate all of the income (gain) from her IRA in the year she has her “date of expatriation”. This would cause a U.S. federal income tax liability of about US$260,000 that would become immediately due and payable. This amount is calculated as follows: US$1.4M total IRA, less the $680,000 exclusion amount, for a total taxable income of about $720,000 (which will generate an approximate US$260,000 income tax for someone who is not married filing jointly. This represents an effective tax rate of approximately 36% on the taxable income portion (US$260,000/US$720,000). Remember, however, $680,000 escapes taxation under the exclusion amount. Hence, the effective tax rate on the entire IRA portion is actually only about 18.6% in this case. This amount is calculated as total IRA income of US$1.4M against tax of US$260,000 (i.e., $260,000/$1.4M= 18.6%).

An 18.6% tax rate is generally a very “attractive” U.S. individual income tax rate for those who have high amounts of income, as is this case with US$1.4M.

If instead, she is not a “covered expatriate” at the time she renounces her citizenship in 2014 (as she did comply with the certification requirements and otherwise would not meet the $2M net worth and her average annual net income tax liability for the preceding 5 years did not exceed $157,000) she would have a very different tax result. In short, she would not have to accelerate the entire tax liability. That sounds like good news, until one considers the U.S. tax rate on future IRA distributions to her after she ceases to be a U.S. citizen. Absent, an income tax treaty, she would have a 30% tax withheld at source (i.e., by the U.S. payer – trustee of the IRA) on each distribution made. If all US$1.4M is distributed out in one lump sum, there will be a tax of US$420,00 (US$1.4M X 30%); much more than the $260,000 for the “covered expatriate” scenario above. See calculations in this table:

Also, if she prefers to defer the IRA distributions (e.g., to make 14 annual distributions of US$100,000), she will have the same 30% tax withheld on each payment; hence, a total tax of US$420,00.

Obviously, a 30% tax is much worse than an 18.6% tax. Accordingly, this is a scenario where an individual may prefer to be a “covered expatriate” as opposed to avoiding such status. A bunch of factual analysis and strategic considerations would need to be considered in her case (e..g, where are her future heirs, what other income might she receive, will she receive any future gifts of inheritances herself, etc. etc.?).

Indeed, in this particular case, I can imagine a scenario (if accompanied by some focused tax planning), she could pay no more than a total effective tax rate of 12.2% on her income. Of course, 12.2% is better than 18.6% and 30%.

Finally, there is one more important wrinkle that can modify these results yet further; a particular income tax treaty with the U.S. that has a specific tax result that is better than the statutory 30% rate on distributions from an IRA to a non-resident alien. The U.S. has numerous income tax treaties with numerous countries, almost all of which have different terms and conditions. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

Li Lianjie – Famous Former U.S. Citizens – Born in Beijing, China (“Jet Li”)

The Chinese actor Li Lianjie, who is better known by his stage name Jet Li, was born in Beijing. He was born in 1963 and his father died when he was just 2 years old and he “. . . was from a very poor family and . . . didn’t have enough money for a good school, so sports-school was good . . . ”

He was born in 1963 and his father died when he was just 2 years old and he “. . . was from a very poor family and . . . didn’t have enough money for a good school, so sports-school was good . . . ”

He is a huge star in China and throughout Asia and became famous in Hollywood.

As a teenager he became a master at Wushu, the full-contact sport from Chinese martial arts. His martial arts fame led to acting, first in China and also in the United States. His film debut Shaolin Temple (1982), helped make him a star.

He apparently became a naturalized citizen of the United States while working in Hollywood.

He apparently has also become a naturalized citizen of Singapore.

He is often highlighted by government officials of China as a model citizen and success story.

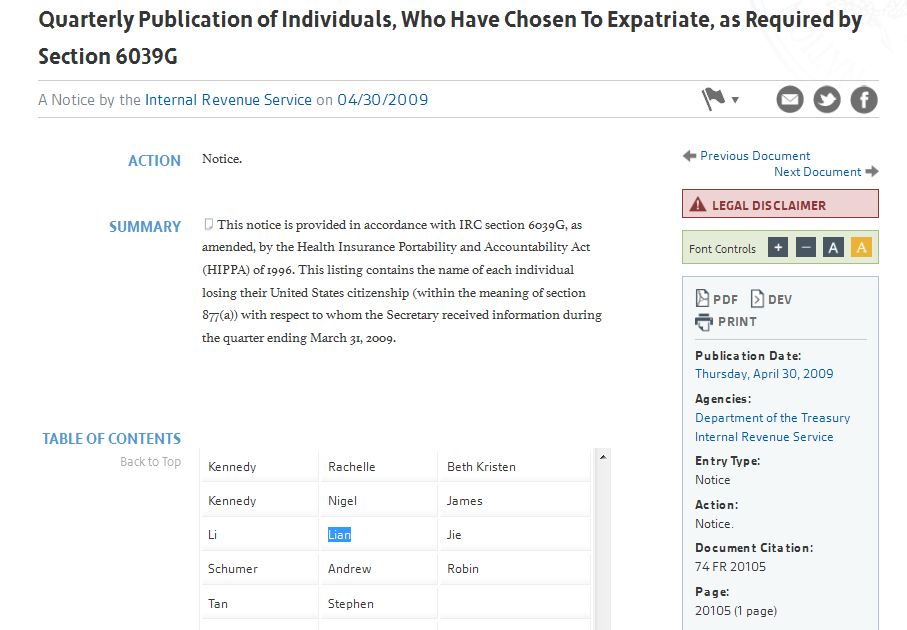

By the year 2009 he renounced his U.S. citizenship as listed in the U.S. federal government’s “Quarterly Publications of Individuals, Who Have Chosen to Expatriate, as Required by Section 6039G“

See here the list for the first quarter of 2009, where Li Lianjie is in the 2009 first quarter list of expatriates.

Presumably, Jet Li solicited timely and filed for a Certificate of Loss of Nationality (“CLN”) timely so he was not subject to the rules of 7701(a)(50) that went into effect in 2008 – See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

Finally, the certification requirement that is available to those individuals who are born with dual national citizenship to avoid “covered expatriate” status, was presumably not available for Li Lianjie, since he was not born a U.S. citizen. Presumably, he could not satisfy each of the requirements of IRC Section 877A(g)(1)(B).