A U.S. Immigration Officer Stops You at at the Airport – @ the Point of Entry (Demands your Green Card be Turned Over))

Being stopped, searched, interrogated or simply questioned by U.S. federal government agents can be intimidating. Especially, if you do not know your legal rights.

It can be more intimidating on your arrival to the U.S. airport, if the CBP officer (U.S. Customs and Border Protection) demands that you physically “return voluntarily” your green card. The consequences they tell you will be immediate deportation from the U.S.

- Removal from the U.S. – is it voluntary or not, under these circumstances?

- What are the U.S. federal tax consequences if you “return voluntarily” your green card?

- What if the CBP officer pulls out Forms W-8s you previously signed with your foreign financial institution and presents them to you in the airport and asks the following questions:

-

- Why did you certify “under penalty of perjury” you were not a United States person on your foreign bank produced documents (you received in France, Germany, the U.K., Canada, Mexico, Japan, Indonesia, Australia — or any other foreign country)?

-

- The officer then asks for all of the envelopes and papers in your luggage and opens the letters and files in your possession – See, the U.S. Supreme Court decision United States v. Ramsey, 431 U.S. 606 (1977).

-

Tax Problems that Turn Serious – can Cause a Green Card Holder to become a “Covered Expatriate”

In Kawashima v. Holder (565 U.S. 478 (2012), the United States Supreme Court held that certain tax offenses committed by lawful permanent residents constitute crimes involving “fraud or deceit” for purposes of the Immigration and Nationality Act (“INA”). Specifically, the Court concluded that lawful permanent residents (a husband and wife from Japan) who were convicted of filing false tax returns resulting in a tax loss exceeding $10,000 had been convicted of an “aggravated felony” within the meaning of the INA.

crimes involving “fraud or deceit” for purposes of the Immigration and Nationality Act (“INA”). Specifically, the Court concluded that lawful permanent residents (a husband and wife from Japan) who were convicted of filing false tax returns resulting in a tax loss exceeding $10,000 had been convicted of an “aggravated felony” within the meaning of the INA.

As a consequence, a conviction for such an aggravated felony renders a lawful permanent resident removable (deportable) from the United States under the immigration laws. Importantly, however, the criminal conviction itself does not automatically terminate lawful permanent resident status. Rather, it provides the legal basis for the Department of Homeland Security to initiate removal proceedings, after which an Immigration Judge may enter a final order of removal.

Once a final order of removal becomes effective, the individual’s lawful permanent resident status is considered to have been revoked. For U.S. federal income tax purposes, this generally results in the termination of lawful permanent resident status under 26 U.S.C. § 7701(b)(6)(B), which provides that an individual ceases to be a lawful permanent resident when “such status has been revoked or has been administratively or judicially determined to have been abandoned.” Accordingly, following a final order of removal, the individual is no longer treated as a lawful permanent resident for purposes of the tax law as summarized below:

| Stage |

Legal Effect |

| 1. Criminal conviction (including guilty plea) |

If the offense qualifies as an “aggravated felony” under INA §101(a)(43), the individual becomes deportable under 8 U.S.C. §1227(a)(2)(A)(iii). A guilty plea counts as a conviction for immigration purposes if the statutory definition of “conviction” is satisfied. |

| 2. DHS initiates removal proceedings |

DHS serves a Notice to Appear (NTA) charging removability before an Immigration Judge under 8 U.S.C. §1229a. |

| 3. Immigration Judge determines removability |

DHS bears the burden of proving deportability by clear and convincing evidence, typically through the certified judgment of conviction. |

| 4. Final order of removal |

If removability is sustained and no relief is available, the Immigration Judge orders removal. After appeals are exhausted (or waived), the removal order becomes final, and the person’s LPR status ends. |

The 2012 case involved Akio and Fusako Kawashima, Japanese citizens who had been lawful permanent residents since 1984. Mr. Kawashima pleaded guilty to willfully filing a false tax return under 26 U.S.C. § 7206(1), while Mrs. Kawashima pleaded guilty to aiding and assisting in the preparation of a false tax return under 26 U.S.C. § 7206(2). The immigration judge issued the order of removal. The Board of Immigration Appeals affirmed. Holding that convictions under 26 U. S. C. §§7206(1) and (2) in which the Government’s revenue loss exceeds $10,000 constituted aggravated felonies, the Ninth Circuit affirmed and ultimately so too did the SCOTUS in this decision.

The Supreme Court concluded that these tax offenses necessarily involve fraud or deceit and, because the tax loss exceeded the statutory $10,000 threshold, they constituted aggravated felonies under immigration law. The Supreme Court of the U.S. therefore upheld the government’s order (which had been upheld through the Ninth Circuit Court of Appeals) removing the Kawashimas to Japan.

This of course is important for U.S. “expatriation tax” purposes, since the “lawful permanent resident” status for tax purposes will necessarily terminate upon the final order of removal. Not before. Once LPR status terminates, the individuals will become covered expatriates, if they meet the time period under the statute to become “long term residents” as was the case for Mr. and Mrs. Kawashima and meet either of the three tests: the tax liability, net asset and certifications of compliance with the federal tax laws. See, Why a “long-term” LPR can NEVER avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B) if Asset or Tax Liability Test is Satisfied!

What Is the IRS Non-Filer Program and How Does It Affect Americans Abroad?

U.S. Citizens and Green-Card Holders Abroad: The IRS Non-Filer Program Explained

On this page:

Read the full analysis here.

What is U.S. citizenship-based taxation, and who does it reach?

The U.S. taxes based on citizenship, not just on where a person lives. A U.S. citizen who has spent nearly all of their life outside the U.S. can still fall within the U.S. tax system. Lawful permanent residents (green-card holders, also called LPRs) residing outside the U.S. can be reached as well. Many people in both groups are shocked to learn how broad this scope is.

Why does the IRS focus so heavily on accounts and assets outside the U.S.?

In recent years the IRS and the Tax Division of the Department of Justice (DOJ) have aggressively pursued assets and accounts located outside the U.S. That pursuit has put a keen focus on the offshore holdings of U.S. citizens and green-card holders who live abroad.

What are the “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers”?

In August the IRS articulated its position for U.S. citizens and lawful permanent residents residing outside the U.S. in a document titled “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers.” It sets out how the IRS approaches the filing obligations of those taxpayers.

What is the IRS non-filer program?

The IRS has had, for years, a specific program aimed at “non-filers,” meaning persons who do not file U.S. income tax returns. The program is detailed in the Internal Revenue Manual (IRM), the IRS’s internal handbook of procedures. It can apply to U.S. citizens and green-card holders living overseas who have not filed.

What can happen if a U.S. citizen or green-card holder living abroad never files a U.S. return?

When a taxpayer does not file, the IRS may prepare a “substitute return” on that person’s behalf. A substitute return is a return the IRS files for the taxpayer, rather than one the taxpayer files. This can apply to U.S. citizens and lawful permanent residents residing overseas who are non-filers. Anyone facing this situation may want to consult an experienced attorney.

Where is the non-filer program actually written down?

The non-filer program is laid out in the Internal Revenue Manual at section 4.19.17, the Non-Filer Program. Its subsections cover the full process:

- 4.19.17.1 — Non-Filer Program

- 4.19.17.2 — Non-Filer Strategy

- 4.19.17.3 — Non-Filer Processing

- 4.19.17.4 — Non-Filer Penalties

- 4.19.17.5 — Undelivered Mail

- 4.19.17.6 — Taxpayer Replies

- 4.19.17.7 — Closures, Non-Examined

Read the full analysis here.

What Are the Risks of Using the IRS Streamlined Filing Program?

On this page:

Read the full analysis here.

The IRS announced a new “streamlined” filing program in June 2014 for US citizens and lawful permanent residents with unreported foreign accounts. Here is how the program works and where its legal risks lie.

What is the IRS “streamlined” program for offshore accounts?

The streamlined program is an administrative procedure the IRS announced in June 2014 for US citizens (USCs) and lawful permanent residents (LPRs, or green-card holders) who did not file US tax returns, information returns, or FBARs (FinCEN Form 114, the Foreign Bank Account Report) covering their foreign accounts. An earlier version was announced in June 2012 and has since been removed from the IRS website. The program asks the taxpayer to file under a certification, and for US residents to pay a “5% miscellaneous offshore penalty.” It is an administrative procedure, not a change in the underlying law.

Does the streamlined program give any legal protection or finality?

No. Legally speaking, this administrative procedure provides no legal protection or finality to the taxpayer. It does not protect against penalties for failure to file tax returns, failure to file information returns, or failure to file FBAR forms. It also does not protect against IRS audits of prior years while the statute of limitations is still open. The IRS or the Justice Department can still fully pursue a US citizen or green-card holder who did not properly file US income tax returns, information returns on foreign assets, or FBARs for prior years, as provided under the law.

What is the “5% miscellaneous offshore penalty”?

For US residents using the streamlined program, the “5% miscellaneous offshore penalty” is an amount equal to 5% of the relevant foreign assets that the taxpayer agrees to pay in order to participate. It is not a penalty that exists under the law in the first place, and it may have no correlation with any income taxes actually owing. As a result, a good-faith taxpayer who made an inadvertent mistake about complex tax provisions can end up paying a portion of their principal assets, not just tax.

Can the IRS be required to refund the 5% penalty if you change your mind?

No. Under the terms of the Certification, the government will never be required to refund the 5% miscellaneous offshore penalty. The taxpayer waives “all defenses against and restrictions on the assessment and collection of the [5%] miscellaneous offshore penalty.” It is a one-way street. Once the money is paid it does not come back, even though the penalty is not something contemplated under Title 26.

What does the streamlined certification require, and who wrote it?

The certification is a statement the taxpayer signs under penalties of perjury. It is not drafted in the taxpayer’s own words; it is drafted by the US federal government. By signing, an individual may expose themselves to greater liability if the government later wants to challenge the certification. The certification turns on terms like “negligence,” “inadvertence,” and a “mistake” that is a “good faith misunderstanding” of the law. It is entirely unclear how the government will interpret these terms in any particular case.

Can the government challenge your certification after you file?

Yes. The IRS’s limited resources mean the vast majority of streamlined cases likely will not be challenged. Even so, there are many ways a certification can be challenged against a particular taxpayer. For example, if a taxpayer threw away the monthly bank statements for a foreign account for the year 2012, that may breach the Certification, and the terms seem to provide that all bets are off against the taxpayer. Signing under penalties of perjury is what creates this exposure.

Could the government later decide you belonged in the OVDP instead?

Yes. Some practitioners expect the government to selectively pursue taxpayers who entered the streamlined process when it believes they should have gone in under the Offshore Voluntary Disclosure Program (OVDP) instead. That determination is made by the government, not the individual taxpayer, and it can put the taxpayer in further jeopardy after they have already filed under streamlined.

Why is the FBAR described as a “trap”?

The FBAR has been used as a trap for the taxpayer. If an individual did not check the right box on Schedule B, Part III of their tax return, the government may argue they were “willfully blind” of the FBAR filing requirements, even if they genuinely did not know about them. The FBAR regulations are extremely complex. Few tax experts anywhere could pass a basic exam on what counts as a “financial interest in” or “signature authority over” an account under these regulations, with many scoring only around 75%, a C or maybe D grade.

Does the streamlined program apply to green-card holders as well as US citizens?

Yes. The same exposure applies to both US citizens (USCs) and lawful permanent residents (LPRs, or green-card holders) who did not properly file US income tax returns, information returns on foreign assets such as IRS Form 8938, or FBARs. Both groups face the same lack of protection from penalties and audits. Both can be pursued by the IRS or the Justice Department for prior years.

A concrete example: why might the program produce an unjust result?

Consider Pierre, who moved from France to the US about 10 years ago. He was an accountant in France, his English is poor, and he relies on an English-only return preparer who never asked whether he held non-US assets. Pierre inherited Swiss and French accounts worth about US$3M, plus real estate outside Paris worth about US$2.5M that generates monthly rent. His preparer always checked the “No” boxes on Schedule B, Part III and never filed FBARs or IRS Form 8938. His sophisticated French advisers told him those European assets were taxable only in France and Switzerland. Foreign taxes withheld there exceed his US tax, so after the US foreign tax credit he owes less than US$1,000 of federal income tax. To join the streamlined program, he would pay about US$325,000, which is 5% of US$6.5M.

Why would a good-faith taxpayer pay $325,000 to settle a $1,000 tax bill?

This is the core unfairness of the program for US residents. A taxpayer like Pierre may owe less than US$1,000 in federal income tax, yet the 5% miscellaneous offshore penalty would require paying about US$325,000, a large portion of a family inheritance, for an inadvertent mistake about very complex rules. That US$325,000 is not contemplated under Title 26. There is no clear legal basis for requiring a good-faith taxpayer to hand over part of their principal to the government for an honest misunderstanding.

What are the choices if you do not enter the streamlined program?

A taxpayer in Pierre’s position faces two hard choices. The first is to comply under Title 26 by filing amended returns, and risk that the IRS and Justice Department pursue multiple-year 50% willfulness penalties by arguing he was “willfully blind,” as in the Zwerner case, even though the penalty for failing to file IRS Form 8938 is generally limited to 3 years at $10,000 per year. The second is to be forced into the streamlined procedure and pay a large portion of his European family inheritance to the US, simply because he did not file IRS Form 8938 or FBARs. Both paths carry real risk.

Read the full analysis here.

When Does the IRS Have No Time Limit to Audit or Assess Taxes?

Table of contents

Read the full analysis here.

What is the statute of limitations on an IRS tax audit?

The statute of limitations is the time frame in which the government has to conduct an audit against a US taxpayer. Once that time frame lapses, the IRS cannot commence tax audits or assess taxes or tax penalties against a US citizen (USC) or lawful permanent resident (LPR, a green card holder) living overseas. In other words, the limitations period sets a fixed window, and after it closes the taxpayer generally has protection from new audits and assessments for that year.

In what situations is there no statute of limitations for a US citizen or green card holder abroad?

There are basically three ways a US citizen or green card holder living outside the US will have no protection of a statute of limitations against the IRS. In these scenarios the limitations period stays open, so there is no closing date on the government’s ability to audit or assess. The three basic scenarios are:

- The USC or LPR does not file a US income tax return (IRC Section 6501(c)(3)).

- There is fraud on the part of the taxpayer (IRC Sections 6501(c)(1), (c)(2)).

- The USC or LPR fails to report certain foreign transactions (IRC Section 6501(c)(8)).

What happens to the statute of limitations if you do not file a US income tax return?

If a US citizen or green card holder does not file a US income tax return, there is no statute of limitations for that year under IRC Section 6501(c)(3). Because the limitations clock generally starts when a return is filed, no return means the period never begins to run. The IRS may therefore audit or assess for that year without a fixed cutoff.

How does tax fraud affect the statute of limitations?

Where there is fraud on the part of the taxpayer, there is no statute of limitations under IRC Sections 6501(c)(1) and (c)(2). An example is a taxpayer who intentionally does not report income. In that situation the limitations period stays open, so the IRS may pursue an audit or assessment for that year without a closing date.

What happens if you fail to report certain foreign transactions?

If a US citizen or green card holder fails to report certain foreign transactions, there is no statute of limitations under IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act,” the same law that created FATCA (the Foreign Account Tax Compliance Act). The limitations period for the year can remain open until the required foreign-transaction reporting is made.

Why file a complete and accurate return even when no tax is owed?

One basic point from the law is that a US citizen or green card holder is almost always better off filing tax returns that are complete and accurate, even when no tax is owing. Filing this way helps assure a fixed time frame during which the US federal government can conduct tax audits and other related tax investigations. Without that fixed window, the limitations period may stay open. Anyone weighing their own situation may want to consult an experienced tax attorney.

Where can you read more about international tax statute of limitations issues?

For an overview of the statute of limitations periods, see the presentation “Starting the Race Against the Tax Authority in the International Tax World – Statute of Limitations & Lack of Filings” by John C. McDougal, Special Trial Attorney at the IRS, and Jon P. Schimmer and Eric D. Swenson of Procopio.

Read the full analysis here.

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

The Life Insurance “Gotcha Tax” – IRS Assesses Excise Tax on Normal Life & Other Insurance Policies

The information featured on this blog is designed to orient U.S. citizens (“USCs”) and U.S. lawful permanent residents, i.e., “green card” holders  (“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

(“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

There are many complex federal tax rules that are often overlooked in the international area. One of those is the excise tax that is payable by the USC or LPR individual, not the non-U.S. insurance company, when premiums are paid to an insurance company. The IRS takes the position that the ” . . . the Service will generally seek payment of the excise tax from the U.S. person making the premium payment . . .” See, IRS Foreign Insurance Excise Tax- Audit Technique Guide.

This is a 1% excise tax on the premiums paid for each life insurance, sickness or accident insurance or contracts. See, IRC Section 4371. If you reside in London and buy life insurance with a UK life insurance carrier (or Paris with a French insurance company, Toronto with a Canadian insurance company, etc.) in your home country, you are probably not thinking that you need to pay Uncle Sam a tax on what you perceive as a “run of the mill” insurance coverage.

Indeed your life insurance company in your country of residence will not be advising that as a USC or LPR, you should be paying Uncle Sam.

If the insurance contract is a casualty policy, the excise tax is 400% greater than the 1% tax on life insurance premiums; i.e., a 4% excise tax. The payment of the tax is made on IRS Form 720, Federal Excise Tax Return.

In my experience, I never find that any individuals who are USCs and LPRs living around the world are aware of this obscure tax. When the tax is not paid the IRS has unlimited time to assess tax and penalties, including late payment penalties, late filing penalties and negligence penalties. Plus, interest that accrues on the unpaid tax and penalties can grow the amounts owing over time. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S., posted March 24, 2014.

The excise tax amount may not seem too significant. However, if it is not timely paid, there will be late payment and late filing penalties (e.g., for failure to file the excise tax return). This 1% or 4% excise tax is on the gross premium payment. This tax amount can certainly add up when insurance premiums are paid annually and over many decades.

Finally, be aware that the IRS is focusing on this excise tax on insurance contracts, at least within its OVDP program where IRS revenue agents are asserting that 25%, 27.5% or 50% of the value of the entire asset (e.g., the cash surrender value of the insurance policy) is subject to the “in lieu of penalty”.

U.S. Citizens Overseas are Often Ill Advised to go into the (1) OVDP and sometimes even the (2) the Streamlined Filing Procedure

There have been prior posts discussing what is referred to as the offshore voluntary disclosure program (“OVDP”) and what the IRS later created – the so-called “streamlined program” filing procedure.

For more background, see, GAO Yr2014 Report on Offshore Voluntary Disclosure Program Indicates Less Than 4% of Taxpayers Lived Outside the U.S., posted March 11, 2014.

Importantly, these OVDP and streamlined programs created by the IRS are not creatures of any statutory law, for instance Title 26 (the Internal Revenue Code) or Title 31 (the so-called Bank Secrecy Act); or any law for that matter. There are no court cases or Treasury Regulations that spell out the terms of these programs as part of any legal framework.

I like to say they are similar to the Hasbro rules of “Monopoly”; a game I was fond of as a child. The IRS is like Hasbro in that they can change the rules of the game as they wish, and often do in the form of publicized frequently asked questions (“FAQs”). The IRS submits these rules of their game and ask, encourage and in some cases (in my view) browbeat taxpayers, often times through their advisers, into participating. See some of the various rule changes below –

The above reflect just some of the modifications and rules the IRS has made, and keeps making to their rules of their proposed OVDP structure; which again, I repeat, is not part of the law.

Many taxpayers and their advisers, in my view have not thought carefully about the law and its application; but rather have focused on the “Monopoly” rules. They cite and read the FAQs if that is somehow the law! See How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Similarly, the streamlined filing procedures is not part of the law, and also has been modified several times by the IRS. Fortunately, the IRS realized that U.S. taxpayers residing outside the U.S. are not the same as those who reside in the U.S. when they created two separate programs last year in 2014.

See, U.S. Taxpayers Residing Outside the United States: The following streamlined procedures are referred to as the Streamlined Foreign Offshore Procedures. Eligibility for the Streamlined Foreign Offshore Procedures

The point of this post is that I have seen numerous cases where U.S. citizens residing around the world were ill advised to participate in the OVDP. In short, if an individual has no criminal tax liability, I think there is little purpose or reason for almost all USC overseas to participate into the OVDP. Analyzing thoughtfully the facts of each case and the law (not the Monopoly rules) is what is important for each individual.

Finally, a clear understanding of what are the Monopoly rules compared to the law is crucial when advising USCs residing overseas. Sometimes, filing through the streamlined procedure might be well advised for a particular taxpayer; e.g., if they would otherwise have substantial late payment and late filing penalties. However, there are plenty of cases where simply filing tax returns pursuant to the law will be preferable in a particular case. This is a process that needs to be thoughtfully considered in each case with a clear understanding of the law – not just the Monopoly rules.

For some related commentary on this topic, see the following posts:

Part I: New TIGTA Report to Congress (Sept 30) Has International Emphasis on Collecting Taxes Owed by “International Taxpayers”: Treasury Inspector General for Tax Administration (TIGTA)

TIGTA’s Semiannual Reports – Today’s Report with International Considerations – Part I

The Internal Revenue Service and U.S. Department of Justice (Tax Division) are the “soldiers” on the ground used to enforce U.S. federal tax law. They interpret the law, in no small part based upon the expertise and input of the myriad of experts in the U.S. Treasury, IRS and DOJ.

However, there are outside forces which oftentimes seem to have an “over-sized” influence on how, when and what priorities are identified in the IRS and DOJ. One of those powers of course is the Administration which makes up the Treasury Department and the very Department of Justice. The green book proposals of the Treasury and different policy proposals are an example. The other organization, within the Executive Branch is the Treasury Inspector General for Tax Administration (TIGTA).

TIGTA is the sort of “watch dog” over the IRS that independently reviews the work undertaken and often times questions that work and the IRS’ efforts. Per its own website it describes itself as:

The Treasury Inspector General for Tax Administration (TIGTA) was established in January 1999 in accordance with the Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) to provide independent oversight of Internal Revenue Service (IRS) activities. As mandated by RRA 98, TIGTA assumed most of the responsibilities of the IRS’ former Inspection Service.

TIGTA is separate and apart from the Taxpayer Advocate Service (“TAS”). See, excerpts of TAS reports here.

Another important influence is the Congress. See a prior post from September 2014 on this topic: How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

*

The Internal Revenue Service Needs to Enhance Its International Collection

Efforts

*

International tax noncompliance remains a significant area of concern for the IRS. The IRS’s collection efforts need to be enhanced to ensure that delinquent international taxpayers become compliant with their U.S. tax obligations. Our review found that the IRS has not provided effective management oversight to international collection, contributing to several control weaknesses in the program. Most notably, international

collection does not have:

*

• Adequate policies and procedures, position descriptions,or the training needed to ensure that international revenue officers can properly work international collection cases;

*

• A specific inventory selection process that ensures that the international collection cases with the highest risk are worked;

*

• Performance measures and enforcement results reported separately from domestic collection; and

*

• A process to measure the effectiveness of the Customs Hold as an enforcement tool.

*

Customs Hold: A notification to the Department of Homeland Security that, according to IRS records, a taxpayer owes Federal taxes. If the taxpayer should return to the United States or Commonwealth Territories without having paid the total amount due, he or she could be interviewed by a Customs and Border Protection Officer at the time of entry. The IRS will then be advised of the taxpayer’s arrival and will be provided with information enabling it to contact the taxpayer regarding payment of his or her outstanding tax liability.

*

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

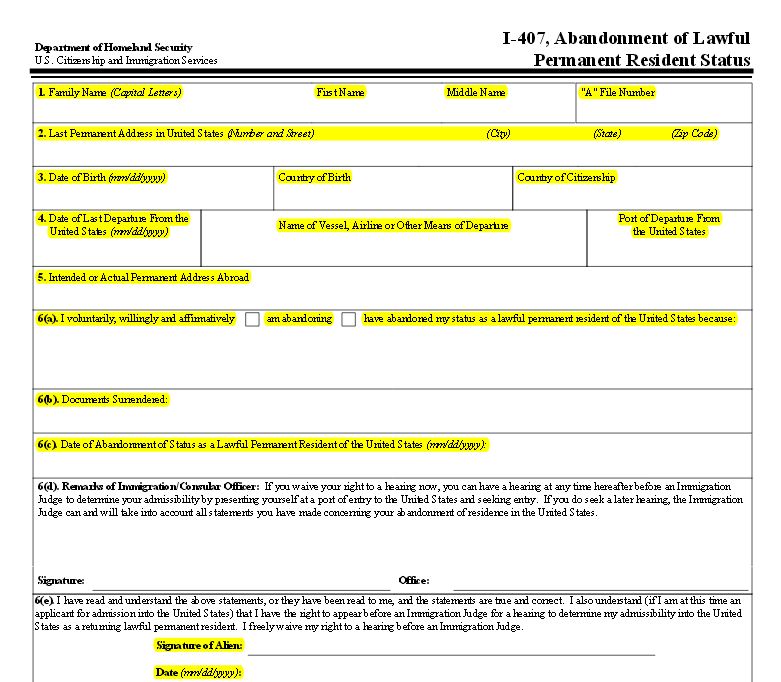

A prior post discussed the newly published USCIS immigration form I-407 for LPRs who must now use it when formally abandoning LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms  are set forth here. The new form requires the address overseas of the individual.

are set forth here. The new form requires the address overseas of the individual.

As readers here know, the names of former U.S. citizens are published quarterly by the U.S. federal government for the world to see. See a prior post, The 2014 Third Quarter Renunciations Is probably the New Norm –

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

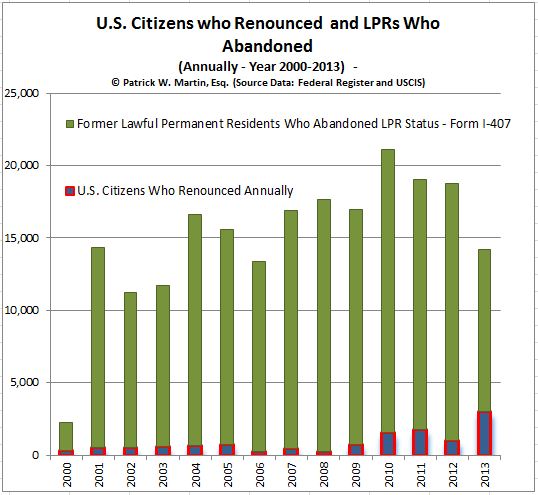

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

- “mark to market” taxation on their worldwide assets,

- 40% inheritance tax to U.S. beneficiaries,

- 40% tax on gifts to U.S. beneficiaries,

- etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”