Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking

At the end of 2012, the IRS announced a New Filing Compliance Procedures for Non-Resident U.S. Taxpayers.

This announcement is now talked about among many tax return preparers as if it creates some sort of special rights or benefits to a particular type of U.S. citizen residing overseas. The IRS announcement is neither the law, nor purports to be the law. It also does not modify the statute of limitations period or otherwise bar the IRS from commencing an audit against a USC residing overseas who has never filed U.S. income tax returns. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S. (Posted on March 24, 2014)

The “new filing compliance procedures” is simply a statement of what has always been the practice of the IRS. U.S. income tax returns that are filed are examined under whatever procedure the IRS chooses as part of its audit and review practices. Income tax returns with modest assets, modest income or little to no U.S. income tax liability garner less attention and resources of the IRS than those with lots of assets, lots of income, etc. See, IRS summary of IRS audits.

Some of the key concepts in the 2012 announcement are set out below:

- Compliance risk determination:

- The IRS will determine the level of compliance risk presented by the submission based on certain information provided on the returns filed, and based on certain additional information that will be required as part of the submission. Low risk will be predicated on simple returns with little or no U.S. tax due. Absent high risk factors, if the submitted returns and application show less than $1,500 in tax due in each of the years, they will be treated as low risk. In general, the risk level will rise as the income and assets of the taxpayer rise, if there are indications of sophisticated tax planning or avoidance, or if there is material economic activity in the United States.

* * *

- How taxpayers will be able to take advantage of the new procedure:

- Taxpayers wishing to use the new procedure will be required to submit: (1) delinquent tax returns, with appropriate related information returns, for the past three years, (2) delinquent FBARs for the past six years, and (3) any additional information regarding compliance risk factors required by future instructions. Payment of any federal tax and interest due must accompany the submission. More information about the application process including where submissions should be sent, will be provided prior to the effective date.

- Any taxpayer claiming reasonable cause for failure to file tax returns, information returns, or FBARs will be required to submit a dated statement, signed under penalties of perjury, explaining why there is reasonable cause for previous failures to file. See IRS Fact Sheet FS-2011-13 (December 2011) for examples of reasonable cause.

Does any of the above protect the USC residing outside the U.S. from an audit for any year a U.S. federal income tax return was not filed? The short answer is – NO!

Does any of the above statements in the IRS announcement mean that a USC residing overseas could not be subject to late payment or late filing penalties for not previously filing U.S. tax returns. The short answer is – NO!

Does any provision in the IRS announcement mean the FBAR penalties could not apply for failure to file. The short answer is – NO! See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

Does any of the above statements in the IRS announcement mean that a USC residing overseas can never be subject to penalties for not filing information returns regarding their non-U.S. international assets and “specified foreign financial assets”? The short answer is – NO! See, USCs and LPRs residing outside the U.S. – and IRS Form 8938

Why then, did the IRS issue such an announcement? Was it an attempt to present a softer message than the IRS announcement in 2011 ( IRS Fact Sheet FS-2011-13 – which enumerates various penalty concepts such as –2. Penalties imposed for failure to file income tax returns or to pay tax; 3. Possible additional penalties that may apply in particular cases; 6. Possible penalties for failure to file FBAR; etc.)?

This is another mixed message from the IRS, which is nothing more than how tax returns have been processed by the IRS over the decades; i.e., a taxpayer files a late tax return and it gets processed by the IRS (and the IRS may elect to audit any particular return, late filed or otherwise).

When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

There are basically three ways a U.S. citizen living outside the U.S. will have no protection of a statute of limitations vis–à–vis the IRS.

The statute of limitations is the time frame in which the government has to conduct an audit against a U.S. taxpayer. This is important, since once that time frame lapses (i.e., the statute of limitations period is over) the IRS cannot commence tax audits or assess taxes or tax penalties against the USC or LPR living overseas.

The three basic scenarios of when there is no statute of limitations for federal tax matters are as follows:

1. The USC or LPR does not file a U.S. income tax return. IRC Section 6501(c)(3).

2. There is fraud on the part of the taxpayer (e.g., the taxpayer intentionally does not report income). IRC Sections 6501(c)(1), (c)(2).

3. The USC or LPR fails to report certain foreign transactions. IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act” which also created FATCA. The following types of transactions and forms that give rise to an “open” statute of limitations period is set out below:

For an excellent overview of the statute of limitations periods, see the presentation – “Starting the Race Against the Tax Authority in the International Tax World – Statute of Limitations & Lack of Filings” by John C. McDougal, Special Trial Attorney – IRS, Jon P. Schimmer and Eric D. Swenson of Procopio.

One of the basic points to takeaway from the law, is that a USC or LPR is almost always better off by filing tax returns (complete and accurate), even when no tax is owing. This will help assure him or her of a fixed time frame during which the U.S. federal government can conduct tax audits and other related tax investigations.

???????????????? ?Please click here to view the above in Chinese.?

The Big Gap ? – How U.S. Citizens and LPRs Residing in the U.S. versus those Living Outside the U.S. File U.S. Tax Returns.

The U.S. worldwide taxation system of U.S. citizens and LPRs causes much confusion. It is unique in the world as most all other countries only impose worldwide taxation on their residents. See, . “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

These U.S. citizens and LPRs living outside the U.S. have (at least prior to FATCA) little third party reporting of income directly to the IRS. There are numerous government reports that demonstrate that when third parties (e.g., banks, tenants, securities brokers, credit card companies, real estate sales transactions, etc.) report the income of a particular transaction to the government, the voluntary compliance of taxpayers increases significantly. See, OECD FORUM ON TAX ADMINISTRATION: COMPLIANCE SUB GROUP

and the U.S. GAO-12-342SP: General government: 44. Internal Revenue Service Enforcement Efforts which highlights that the ” . . . where IRS can improve its programs which can help it collect billions in tax revenue, facilitate voluntary compliance, or reduce IRS’s costs. These include pursuing stronger enforcement through increasing third-party information reporting . . . Expanding third-party information reporting improves taxpayer compliance and enhances IRS’s enforcement capabilities. The tax gap is due predominantly to taxpayer underreporting and underpayment of taxes owed. At the same time, taxpayers are much more likely to report their income accurately when the income is also reported to IRS by a third party. By matching information received from third-party payers with what payees report on their tax returns, IRS can detect income underreporting, including the failure to file a tax return.”

The current trend of worldwide reporting of assets and income via FATCA and the OECD programs is designed to accomplish just this; increase information reporting by third party payers (e.g., principally from foreign financial institutions) directly to the IRS and tax revenue authorities around the world to deter U.S. citizens and LPRs living outside the U.S. from under-reporting or not reporting at all their income on their U.S. income tax returns.

Traditionally, there were limits on the law and the jurisdictional authority the U.S. government had to require non-U.S. institutions to report non-U.S. source income directly to the IRS. This has changed significantly now with FATCA, which started in earnest this year, in 1 January 2014. See,

Here is where there appears to be a “Big Gap”? Not necessarily a gap in the amount of tax dollars collected among USC and LPR living in the U.S. versus those living outside the U.S.; but at least an apparent gap in the number of tax returns filed by overseas residents. The level of over-all tax compliance by U.S. citizens and LPRs residing overseas is not clear, since only 334,851 total individual tax returns were filed in 2006 which incorporated the foreign earned income exclusion (IRS Form 2555) by non-resident U.S. taxpayers.27 If there are approximately 5-7 million U.S. citizens residing overseas28 (not even including LPRs who reside overseas) and 142 million total individual income tax returns filed annually29 such a small number (i.e., 334,851) indicates that only a fraction of the total returns filed are filed by persons residing overseas; i.e., only about 2 tenths of one percent (0.24%) of the total income tax returns filed were by those residing overseas with the foreign earned income exclusion.

Will the government see this as a tax gap?

These numbers for the year 2006 are even more interesting when one analyzes the foreign earned income exclusion taken.

Canada had 30,067 returns filed versus Mexico with only 6,112 for the year 2006. It seems that Mexico should at a minimum have more returns filed than Canada – or at least about the same, since the State Department estimates that more U.S. citizens (approximately 1+/- million live in that country). Both seem very low, if it is true that there are probably close to 1.5 to 2 million total U.S. citizens living in these two countries.

28. See, p. 130 and footnote 11 of Taxpayer Advocate Report referenced in footnote 29 above – “Cf. IRS website, Reaching Out to Americans Abroad (Apr. 2009), and W&I Research Study Report, Understanding the International Taxpayer Experience: Service Awareness, Use, Preferences, and Filing Behaviors (Feb. 2010) (citing U.S. Department of State data). This number does not include U.S. troops stationed abroad.”

In 2006, there were a total of 138 million total individual income tax returns filed.

Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs

The IRS, U.S. Treasury and Congress have been troubled for a very long time by tax issues regarding U.S. citizens and LPRs who reside outside the U.S. In 1998, an excellent U.S. Treasury report explains well the state of the tax law at that time and can be read here: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues.

The tax law discussed in that report is largely the same today, except for the expatriation provisions (IRC Sections 877, 877A, 2801 and 7701(b)(6)).

The tax law discussed in that report is largely the same today, except for the expatriation provisions (IRC Sections 877, 877A, 2801 and 7701(b)(6)).

What has changed is the sharing and exchange of information within the government and among foreign governments.

The report which is now over 15 years old, portended the future we have today with FATCA and the multi-prong efforts to ensure that U.S. citizens and LPRs residing overseas comply with U.S. tax law –

???????????????? ?Please click here to view the above in Chinese.?

Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?

Senators on the Permanent Subcommittee on Investigations have recently focused extensively on U.S. nationals living outside the U.S. who have Swiss accounts. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

There are millions of U.S. citizens living in all parts of the world, many of whom I have identified as “Accidental Americans.” See the detailed tax article Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45; Martin, P.

During the past century U.S. Citizens living permanently or nearly permanently outside the U.S. have been “de facto” non-residents for U.S. income tax purposes. Not because the law provided they were not residents, but simply because there was little awareness of the unique system of U.S. citizenship based taxation (or those cases where individuals purposefully chose not to comply with U.S. tax laws). The U.S. Supreme Court in Cook vs. Tait found it Constitutional nearly 100 years ago. See . “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

This “de facto” non-residency for U.S. citizens is rapidly changing for several reasons:

First, the UBS scandal of U.S. citizens with undeclared accounts broke in 2008 and 2009.

Second the legal struggle between the U.S. Justice Department and the Swiss government and Swiss financial institutions during these past years.

Third, the adoption of FATCA by the Congress and President Obama in 2010.

Fourth, the current day technology which makes collecting, sending, sorting and identifying taxpayers and their assets through the worldwide financial sector now feasible.

Fifth, the implementation of FATCA by the U.S. in 2014 and the 20 plus FATCA Intergovernmental Agreements entered into with various countries.

Sixth, the OECD plan for a worldwide multilateral FATCA like system to be implemented shortly.

Seventh, the high profile IRS offshore voluntarily disclosure programs in 2009, 2011 and the current program launched in 2012.

Eighth, the on-going deferred prosecution agreements that have been entered into with more than 100 Swiss banks and the U.S. Justice Department.

Ninth, on-going criminal indictments by the U.S. Justice department of various taxpayers, foreign bankers, foreign lawyers and other so-called enablers for tax evasion, filing fraudulent documents and aiding and abetting the same.

Tenth, the Senate bi-partisan hearings that have and keep focusing and pushing these issues publicly at multiple levels.

Eleventh, the internet and current methods of communications and intern ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

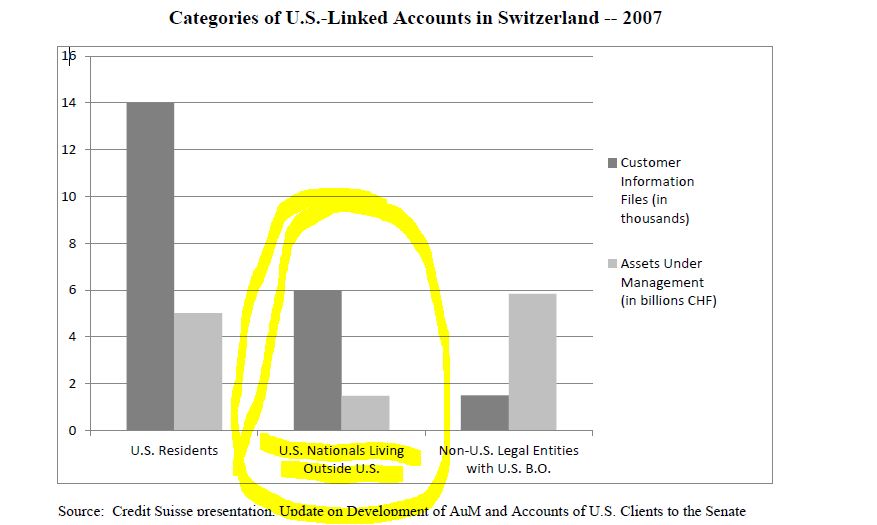

A large portion of the Senate committee report is dedicated to U.S. citizens who live outside the U.S. and are not compliant with U.S. tax laws. The following chart from the report highlights this focus as to the approximately 6,000 U.S. citizen accounts at Credit Suisse who were/do not live in the U.S:

For further observations on this topic, see an earlier post – Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.; Posted on March 4, 2014

???????????????? ?Please click here to view the above in Chinese.?

What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Below is a fairly detailed summary of the type of tax crimes that are commonly investigated by IRS Criminal Investigation (“CI”) agents.

As has already been noted, TaxAnalysts reporter Jaime Arora reported in the 3 March 2014, Worldwide Tax Daily certain comments made by Mr. Jeffrey Cooper, who is the deputy director of the IRS Criminal Investigation division’s international operations. It was reported that IRS CI is looking into why people are making the choice to shed their U.S. citizenship; whether it is related to any particular laws. Cooper was quoted at the Federal Bar Association’s Section on Taxation’s 38th Annual Tax Law Conference held on February 28, 2014.

TaxAnalysts journalist Arora quoted Cooper as identifying why people are making the choice and “If we find something, we do; if not, we just move on,” he said.

It is common policy for the IRS CI not to provide information on how they commence taxpayer investigations, including how they obtain U.S. citizenship renunciation referrals or documents. There could be a number of ways these investigations are commenced. It may be as simple as taking the list from the Quarterly Publication of Individuals, Who Have Chosen to Expatriate – Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G and start reviewing their tax return files (IRS Forms 1040, 8854, etc.) along with FBAR filings.

IRS CI tax investigations generally focus on false documents or false statements, evasion of taxation, aiding and abetting of the above along with other related tax and Bank secrecy (Title 31) crimes.

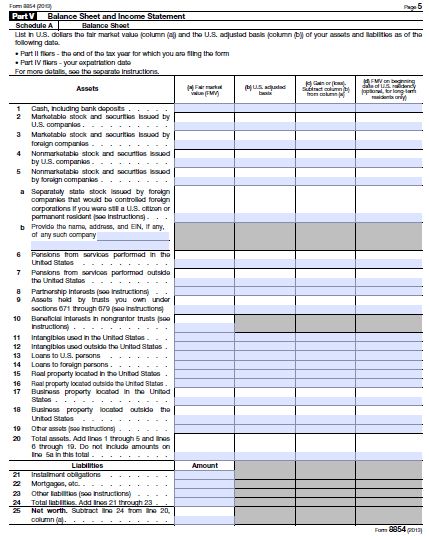

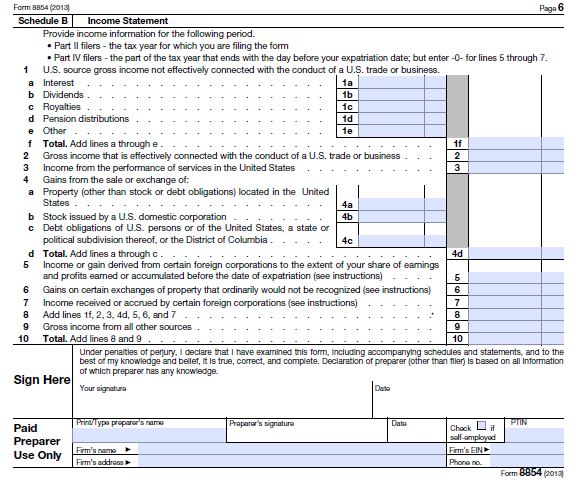

The tax reporting process for expatriates is extensive, including the basic requirement of signing IRS Form 8854 under penalty of perjury, which provides as follows on the last page of the form:

There are a host of reporting requirements and factual information that must be provided under Sections 877 and 877A, for all persons (including those with little to no assets), specifically including filing IRS Form 8854 which asks for a “boat load” of asset, income, liability and tax information. A former U.S. citizen or LPR always needs to be careful that the information provided is true, accurate and complete. See Part V of the form.

A summary of these crimes is set out below:

1. Criminal Offenses under Title 26 (Federal Tax Law)

a. Tax Evasion (IRC Section 7201)

b. Filing a False Return or Other Document – Perjury (IRC Section 7206(1) )

(i) Aiding or assisting in the perpetration of a false or fraudulent document (26 U.S.C. § 7206(2))

(ii) Removal or concealment with intent to defraud, commonly related to untaxed liquor (26 U.S.C. § 7206(4))

(iii) Compromises and closing agreements involving fraud or concealment (26 U.S.C. § 7206(5))

c. Failure to File Return, Supply Information, or Pay Tax – (IRC § 7203 – Misdemeanor – up to 12 months imprisonment)

d. Fraudulent Returns, Statements, or Other Documents (IRC § 7207)

e. “Structuring” Transactions to Evade Cash Reporting (IRC § 6050I)

In addition to these tax specific crimes, other key crimes commonly used by IRS CI agents in tax cases, particularly international cases, include:

2. Tax Related Criminal Offenses under Titles 18 and 31 (Not Tax Law Specific)

a. Conspiracy (Section 371 of Title 18)

(i) Elements of the Offense

(ii) Penalties and Statute of Limitations

b. False Statements (Title 18 U.S.C. § 1001)

(i) Penalties and Statute of Limitations

c. Perjury

d. Mail fraud

e. Principals and those Who Aid and Abet (Title 18)

f. Accessory After the Fact

Finally, it is worth noting that the government regularly collects information from internet resources, such as blogs and e-mails as they build a case for criminal prosecution. A former head of the Tax Division at the U.S. Department of Justice once told me that “e-mails and internet communications was God’s gift to prosecutors”.

???????????????? ?Please click here to view the above in Chinese.?

Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

Instead of the government finding U.S. citizens living outside of the United States, as a low priority, the Senate Permanent Subcommittee on Investigations focused extensively on Swiss accounts opened by these individuals. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

Some key excerpts of that report are as follows (at page 4):

. . . focused primarily on Swiss accounts held by U.S. residents, ignoring the over 6,000 accounts opened by U.S. nationals living outside of the United States. . . . It was not until 2012, that the bank expanded the Exit Projects to include a review of the thousands of Swiss accounts opened by U.S. nationals living outside of the United States.. . .

In addition, the report is replete with statistical data of accounts held by U.S. nationals living outside the U.S., such as the following:

Instead of concluding that the complex U.S. laws are leading to non-compliance by U.S. citizens residing outside the U.S. (per the Taxpayer’s Advocate Report), it seems to conclude to the contrary and the report highlights the virtues of the OVD program in non-compliance as generally willful with millions of U.S. citizens living outside the U.S. who are not in compliance, per the following statement (at page 22):

“The OVDP continues to provide valuable information for the United States in its efforts

to combat offshore tax abuse, although it is far from clear that effective use is being made of the

information generated. For taxpayers, it continues to offer a useful alternative to report

undeclared offshore accounts that, potentially, number in the millions. According to the Taxpayer Advocate, “While 7.6 million U.S. citizens reside abroad and many more U.S. residents have FBAR filing requirements, the IRS received only 807,040 FBAR submissions in 2012,” signaling “significant information reporting noncompliance.”69 2013 Annual Report to Congress — Volume One, Taxpayer Advocate Service, “OFFSHORE VOLUNTARY DISCLOSURE: The IRS Offshore Voluntary Disclosure Program Disproportionately Burdens Those Who Made Honest Mistakes,” at 229.

This report seems to get off track by not distinguishing between normal U.S. citizens who are living out their lives in their country of residence, as opposed to U.S. nationals who are intentionally attempting to evade taxes, filing false documents, not filing returns, or otherwise intentionally violating U.S. law. All of these 7.6 million U.S. nationals living around the world are being lumped together by the government with U.S. resident citizens, irrespective of the facts of each individual and family.

This is a bit of a Bombshell – If the IRS Criminal Investigation (“CI”) is investigating U.S. citizens renouncing their citizenship?

It is reported the IRS CI is interested in the reasons that U.S. citizens renounce their citizenship. Jaime Arora, IRS Criminal Investigation Division Looking Into U.S. Citizenship Renunciations, 2014 TNT 41-8 (3/3/14). The article is nonspecific about what the IRS is looking for and the consequences might be if they found something.

Still, there are tax requirements for renouncing citizenship in certain cases. I won’t go into them now, but link to blogs on the subject here.

I can imagine that mishandling the various forms and representations required for renunciation, including the tax forms and representations, could be a crime under various federal statutes — tax and nontax — and, at last if something was done wrong related to taxes, conceivably the renunciation conduct could refresh statutes of limitations for tax crimes that might have otherwise expired.

Importantly, why someone renounces their U.S. citizenship under the current tax law (IRC Section 877A) is not relevant as to the tax consequences to the individual who renounced. This is very different from the law that was passed in 1996. These rules changed in 2004 and yet again in 2008 to create an objective set of taxation rules. For this reason, it would be very odd for the IRS CI to be investigating (at least recent expatriates) former U.S. citizens to determine why, i.e., the reasons, they renounced U.S. citizenship.

???????????????? ?Please click here to view the above in Chinese.?

Hearings – Permanent Subcommittee on Investigations – re: Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts – February 26, 2014

Will the IRS be assisting the Justice Department to prosecute U.S. citizens who have lived abroad most (if not all) of their lives?

Will the IRS be assisting the Justice Department to prosecute U.S. citizens who have lived abroad most (if not all) of their lives?

**

The on-going focus of of the government, including the purported “Billions in Hidden Offshore Accounts” by the Permanent Subcommittee on Investigations, begs the questions, where are these billions of assets by U.S. taxpayers?

**

Will this be the premiss used by the IRS and Justice Department to try to prosecute U.S. citizens residing overseas?

Law abiding U.S. citizens who have spent most (if not all) of their lives overseas are put in an untenable position vis–à–vis the U.S. federal government regarding U.S. tax and tax filing obligations.

**

See what the government has to say

**

Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

The Treasury Inspector General wrote the following in a 2009 report (of which none of these numbers have seriously been questioned, supported or analyzed) – – titled

A Combination of Legislative Actions and Increased IRS Capability and Capacity Are Required to Reduce the Multi-Billion Dollar U.S. International Tax Gap

Synopsis

The IRS estimated that the entire tax gap for Tax Year 2001 was $345 billion. However, the IRS has not developed an estimate for the international tax gap. Non-IRS estimates of the international tax gap range from $40 billion to $123 billion. While there might be overlap between the IRS tax gap estimate and the international tax gap, it is doubtful that the $345 billion estimate includes the entire international tax gap.

The primary reason for this conclusion is that identifying hidden income within international activity is very difficult and time–consuming.[4] Furthermore, the IRS did not measure for the international tax gap component in the Individual National Research Project (NRP) estimate for the Tax Year 2001 tax gap. Therefore, it is unlikely that hidden offshore income is comprehensively included in the IRS tax gap estimates. In fact, the IRS’s Research, Analysis and Statistics (RAS) organization reasoned that because of cost, staffing, and technical limitations, an NRP type of direct measurement is unfeasible. However, in an attempt to learn more, the IRS has other initiatives underway.

???????????????? ?Please click here to view the above in Chinese.?