The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

Categories of records in this system include:

A. The hardcopy paper A-File, which contains the official record material about each individual for whom DHS has created a record under the INA such as: naturalization certificates; various documents and attachments (e.g., birth and marriage certificates); applications and petitions for benefits under the immigration and nationality laws; reports of arrests and investigations; statements; other reports; records of proceedings before or filings made with the U.S. immigration courts and any administrative or federal district court or court of appeal; correspondence; and memoranda. Specific data elements may include:

- Alien Registration Number(s) (A-Numbers);

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

? Document type,

? issuing organization,

? document number, and

? expiration date;

- Military membership;

- Arrival/Departure information (record number, expiration date, class of admission, etc.);

- Federal Bureau of Investigation (FBI) Identification Number;

- Fingerprint Identification Number;

- Immigration enforcement history, including arrests and charges, immigration proceedings and appeals, and dispositions including removals or voluntary departures;

- Immigration status;

- Family history;

- Travel history;

- Education history;

- Employment history;

- Criminal history;

- Professional accreditation information;

- Medical information relevant to an individual’s application for benefits under the INA before DHS or the immigration court, an individual’s removability from and/or admissibility to the United States, or an individual’s competency before the immigration court;

- Specific benefit eligibility information as required by the benefit being sought; and

- Video or transcript of immigration interview

Subsequent posts will discuss how and when the law allows the IRS to access these records.

The IRS Can Make an Assessment of Taxes and Penalties and Ask Questions Later

Taxpayers have a distinct disadvantage under the law vis-à-vis the IRS, since the law creates a “presumption of correctness” in favor of the IRS determination of taxes owing by any particular taxpayer.

This concept is decades old and is found in U.S. Supreme Court precedence at least as far back as 1933, where the Court in Welch v. Helvering (290 U.S. 111 (1933)) explained:

The Commissioner of Internal Revenue resorted to that standard in assessing the petitioner’s income, and found that the payments in controversy came closer to capital outlays than to ordinary and necessary expenses in the operation of a business. His ruling has the support of a presumption of correctness, and the petitioner has the burden of proving it to be wrong. Wickwire v. Reinecke,275 U. S. 101; Jones v. Commissioner, 38 F.2d 550, 552. [emphasis added]

This continues to be the law to this day.

What this means for taxpayers, particularly United States citizens and lawful permanent residents (“LPRs”) who reside outside the U.S., is that the IRS will often make erroneous tax determinations; yet the calculation of the amount of tax owing is presumptively correct.

The individual has the burden of proving the government wrong.

As an international tax practitioner, I have seen some of the most farfetched tax assessments by the IRS in the international context. If the IRS uses bad or incomplete information and then produces a tax assessment result, it is like the old computer saying; “junk in junk out.”

The IRS almost always, by definition, has incomplete information for taxpayers residing overseas. For that reason, it is not uncommon for them to make statutory notices of deficiency that are not supported by the law or the facts. See, the IRS explanation of a Notice of Deficiency CP3219N (“90-day letter”) proposing a tax assessment. Understanding Your CP3219N Notice

This power of the IRS under the law, is also compounded by the ability of the IRS to file a “substitiute return” for those USCS and LPRs residing overseas. See a prior post from November 2014, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas.

U.S. Department of State, Starts Communicating with U.S. Citizens Overseas Regarding Tax Obligations with the IRS

The IRS is in charge of U.S. federal tax administration. It’s mission statement is set out below and is very different from the mission of the U.S. Department of State:

The IRS Mission

Provide America’s taxpayers top quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

This mission statement describes our role and the public’s expectation about how we should perform that role.

- In the United States, the Congress passes tax laws and requires taxpayers to comply.

- The taxpayer’s role is to understand and meet his or her tax obligations.

- The IRS role is to help the large majority of compliant taxpayers with the tax law, while ensuring that the minority who are unwilling to comply pay their fair share.

The U.S. Department of State is in charge of something very different from taxes and tax policy. Below is its Mission Statement –

Department Mission Statement

The Department’s mission is to shape and sustain a peaceful, prosperous, just, and democratic world and foster conditions for stability and progress for the benefit of the American people and people everywhere. This mission is shared with the USAID, ensuring we have a common path forward in partnership as we invest in the shared security and prosperity that will ultimately better prepare us for the challenges of tomorrow.

–From the FY 2014 Agency Financial Report,

released November 2014

In my career of more than 25 years as a tax professional, working in the international tax area, I have never before seen communications sent by the U.S. Department of State, directly discussing U.S. federal tax obligations.

However, there have been many changes in the last few years in how aggressive the IRS (and Tax Division, Department of Justice) has become in enforcing U.S. tax laws overseas. See, Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

This seems to be part of a bigger trend of the IRS to use other governmental agencies and their resources in identifying and locating U.S. taxpayers and their assets overseas.

One recent development is the communication sent by the U.S. Department of State via e-mail to U.S. citizens residing overseas. The following is the complete text of the tax compliance communication sent by the U.S. Department of State, which ends with a reference: “I Haven’t Filed All My Tax Returns, What Can I Do?.” It then references the IRS offshore programs (which includes the OVDP, which in my view, should be reserved for only those U.S. taxpayers who have criminal tax liability – see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior):

Dear U.S. citizens,

The Internal Revenue Service (IRS) has provided the following guidance for U.S. citizens abroad preparing for the 2015 tax filing season. This IRS guidance is posted under Federal Benefits and Obligations on travel.state.gov. U.S. embassies and consulates cannot mail tax returns on behalf of U.S. taxpayers living abroad.

1. Who Must File?

All U.S. citizens and resident aliens must file a U.S. individual income tax return, even if they permanently live outside the United States and may not owe any tax because of income exclusion or tax credit.

2. When is the 2014 Federal Tax Return Due?

Due date for Form 1040: April 15, 2015

Extensions:

- An automatic extension to June 15, 2015, is granted for taxpayers living outside the United States and Puerto Rico. No form is required; write “Taxpayer Resident Abroad” at the top of your tax return.

- Caution: This extension applies only for filing your tax return, not for payment. If you owe any taxes, you’re required to pay by April 15, 2015. Interest and penalties will generally be applied if payment is made after this date.

- To request an additional extension to October 15, 2015, use Form 4868.

- Caution: This extension applies only for filing your tax return, not for payment. If you owe any taxes, you’re required to pay by April 15, 2015. Interest and penalties will generally be applied if payment make after this date.

- Other extensions may be available on IRS.gov.

3. Can I Mail My Return and Payment?

You can mail your tax return and payment using the postal service or approved private delivery services. A list of approved delivery services is available on IRS.gov. If you mail a return from outside the United States, the date of filing is the postmark date. However, if you mail a payment, separately or with your return, your payment is not considered received until the date of actual receipt.

4. Can I Electronically File My Return?

You can prepare and e-file your income tax return, in many cases for free. Participating software companies make their products available through the IRS. E-File options are listed on IRS.gov.

5. What Forms May I Need?

- 1040, U.S Individual Income Tax Return

- Instructions to Form 1040

- 1116, Foreign Tax Credit

- 2013 Instructions to Form 1116 – 2014 instructions will be available soon, please check on http://www.irs.gov

- 2350, Application for Extension of Time to File U.S. Income Tax Return (for U.S. citizens and residents abroad)

- 2350 in Spanish

- 2555, Foreign Earned Income Exclusion

- Instructions to Form 2555

- 2555-EZ, Foreign Earned Income Exclusion

- Instructions to Form 2555-EZ

- 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return

- 4868 in Spanish

- 8802, Application for United States Residency Certificate

- Instructions to Form 8802

- 8938, Statement of Specified Foreign Financial Assets

- Instructions to Form 8938

- 14653, Certification by U.S. Person Residing Outside of the United States for Streamlined Foreign Offshore Procedures

6. How Do I Pay My Taxes?

You must pay your taxes in U.S. dollars.

- Direct pay. You can pay online with a direct transfer from your U.S. bank account using Direct Pay, the Electronic Federal Tax Payment System, or by a U.S. debit or credit card. You can also pay by phone using the Electronic Federal Tax Payment System or by a U.S. debit or credit card.

- Foreign wire transfers. If you have a U.S. bank account, you can use the Electronic Federal Tax Payment System. If you do not have a U.S. bank account, ask whether your financial institution has a U.S. affiliate that can help you make same-day wire transfers.

- Foreign electronic payments. International taxpayers who do not have a U.S. bank account may transfer funds from their foreign bank account directly to the IRS for payment of their tax liabilities.

7. Other Reporting?

You also may have to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR), by June 30, 2015.

8. Does the IRS Provide Help in Other Languages?

The IRS provides tax information in Chinese, Korean, Russian, Spanish, and Vietnamese. Go to http://www.irs.gov and use the drop down box under “Languages” on the upper right corner to select your language.

9. Where Can I Get Help?

Contact the International Taxpayer Service Call Center by phone or fax. The International Call Center is open Monday through Friday, from 6:00 a.m. to 11:00 p.m. (Eastern Time).

Tel: 267-941-1000 (not toll-free)

Fax: 267-941-1055

You may also contact the IRS office in London, Paris, or Frankfurt. For addresses and telephone numbers, contact my local office internationally.

10. I Received a Notice from the IRS, What Do I Do?

If you receive a notice from the IRS and need to contact the IRS, call the number listed on the notice or the International Taxpayer Service Call Center (see above).

11. Where Can I Get More Information?

For information on the IRS website about international taxpayers, see this page.

For general information about international taxpayers, see Publication 54, “Taxation of U.S. Citizens and Residents Abroad.”

For information on the Affordable Care Act and taxpayers outside the United States, see Publication 5187, “Health Care Law.”

12. I Haven’t Filed All My Tax Returns, What Can I Do?

If you have not filed all the returns required of you and want to catch up on your filing obligations, see this announcement: IRS makes changes to offshore-programs.

Does the U.S. Government Assume U.S. Citizens Having Assets Outside the U.S. are Hiding Assets from the IRS?

Does the IRS Assume U.S. Citizens Having Assets Outside the U.S. are Tax Cheats?

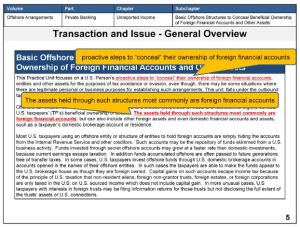

This rhetorical question is asked for a simple reason. In IRS training materials, which are part of the basic core training provided to IRS agents investigating individuals with assets outside the U.S. and international matters and transactions, the IRS makes the following bold statement:

“Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .  “

“

A slide from these IRS training materials has this statement along with tax evasion activities that IRS agents are to be on the look out. Certainly, the identification of illegitimate tax evasion activities is appropriate for tax authorities, but such a bold statement ignores the larger reality of the international business world.

Unfortunately, such a bold statement by the IRS does not reflect the reality of millions of U.S. citizens and lawful permanent residents residing outside the U.S.; or indeed maybe millions more who live in the U.S. and have offshore business and investment activities.

For additional background of the estimated millions of USCs residing outside the U.S., see an earlier post: Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

The world is a very global and international marketplace with international commercial activities undertaken throughout at a scale that rivals the volume of international business just a few years ago. The IRS seems to ignore this important consideration, which is supported by the Department of  Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

According to the federal government itself in reports prepared by the Department of Commerce – Bureau of Economic Analysis, these international transactions continue to grow robustly in the year 2014.

Therefore, a more balanced understanding and view of how, when and where international business is conducted by U.S. citizens around the world should help IRS agents when they conduct tax audits and not assume – erroneously that – “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . .”

“Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –

There have been a series of previous posts that discussed the IRS and other government agencies ability to track taxpayers and their assets outside the U.S.

See for instance, the following posts: Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

and Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

Interestingly, the release of IRS internal training manuals and materials (which were obtained through a Freedom of Information Act – FOIA – request) and includes the Power Point slide in this post, describes the TECs database and how it can be used by IRS agents regarding foreign assets and individuals as follows:

The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. TECS contains historical travel information such as records of commercial airline flights, border crossings, and specific dates that individuals have traveled to and from the United States.

All this information could provide you with potential leads to pursue.

For example, the discovery of where the taxpayer may hold assets or accounts or where the taxpayer conducts business. It may also assist in determining taxpayer’s residency and the credibility of taxpayer testimony. TECS may have gaps in the information captured, caution is advised. For example, it might contain incomplete information about border crossings, private plane and private boat information. It does not contain enough stand alone data to determine residency. It should be used together with other sources of information.

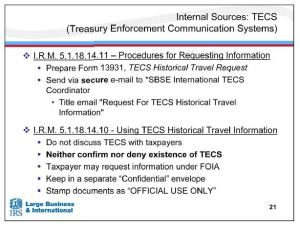

In addition, the IRS training materials demonstrates the secrecy of the TECs database and what steps the IRS tells their agents to take regarding the TECs database. The following excerpt directly from the IRS “Matrix Application Training International Individual Compliance: Basic Structures Part II: Pre-Audit, Investigative Techniques & Statutes”

• IRM 5.1.18.14.10 – Covers using TECS Historical Travel Information

First and foremost, do not discuss the existence of TECS with the taxpayers. We must neither confirm nor deny the existence of TECS data.

Part I: How the IRS “Non-Filer Program” Affects USCs and LPRs Residing Outside the U.S.

U.S. citizens who have spent most all of their lives outside the U.S. are often times shocked to learn about the scope of the U.S. citizenship based taxation system. In recent years, due to the aggressive pursuit of the IRS and Tax Division of the Department of Justice, there has become a keen focus on assets and accounts located outside the U.S.

Most recently in August of this year, the IRS has articulated its position for U.S. citizens and lawful permanent residents residing outside the U.S. in a document titled – “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers”

For a brief chronology of the actions taken by the IRS and DOJ and the U.S. Congress in the offshore world during the last few years see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

See, also IRS Audit Techniques – Expatriation, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The program is detailed in the Internal Revenue Manual, set out below. A follow-up post will discuss some uniquely complex issues affecting U.S. citizens and lawful permanent residents who reside outside the U.S.

Read the Q&A format here.

How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The U.S. federal government has extensive “legal tools” at their disposal to help enforce the U.S. tax law overseas. There are limits, both in practice and legally, of how they can effectively use those legal tools against USCs and LPRs residing outside the U.S. See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

Although U.S. citizenship taxation has been the law in the U.S. since the Civil War, it has been a “de facto” residency based taxation system for the last 100 years, since the U.S. government did not have the means to collect information to identify assets, income and USC and LPR taxpayers outside the U.S. Plus, based upon my experience, few USCs who lived almost all of their lives outside the U.S. had any idea of their obligation to file U.S. federal income tax returns, as U.S. “tax residents.” IRS Form 1040.

This has changed with technology, the integrated worldwide financial system and FATCA which is now bringing a massive amount of financial data and information to the IRS. See, Part 3 – Unintended Consequences of FATCA: Will Taxpayer (Individual’s) Personal Financial Data at IRS get “Snowdened”?

The IRS has a powerful tool to assess taxes against any taxpayer who does not file U.S. income tax returns, specifically including USCs and LPRs residing outside the U.S. This tool is known as the “Substitute Return” and is explained well in a New York Times Article from Feb. 2012, If You Don’t File, Beware the Ghost Return

The IRS provides a snippet of information below in their website:

Substitute Return

If you fail to file, we may file a substitute return for you. This return might not give you credit for deductions and exemptions you may be entitled to receive. We will send you a Notice of Deficiency CP3219N (90-day letter) proposing a tax assessment. You will have 90 days to file your past due tax return or file a petition in Tax Court. If you do neither, we will proceed with our proposed assessment. If you have received notice CP3219N you can not request an extension to file.

If any of the income listed is incorrect, you may do the following:

- Contact us at 1-866-681-4271 to let us know.

- Contact the payer (source) of the income to request a corrected Form W-2 or 1099.

- Attach the corrected forms when you send us your completed tax returns.

If the IRS files a substitute return, it is still in your best interest to file your own tax return to take advantage of any exemptions, credits and deductions you are entitled to receive. The IRS will generally adjust your account to reflect the correct figures.

The Internal Revenue Manual explains the Substitute Return and the so-called Automated Substitute for Return (ASFR) Program.

Based upon my experience, a Substitute Return for a non-resident taxpayer is necessarily terribly wrong and incorrect. This is because it is typically based upon only a small sliver of information; typically some item of income. It does not include a complete picture of the taxpayer. There are never expense items that are available for a deduction, nor foreign taxes reflected available for a foreign tax credit, etc. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

I have never seen a Substitute Return which includes a foreign earned income exclusion calculation for the benefit of the individual. See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed

I suspect that once the IRS collects information under FATCA (starting this year 2014) on the non-U.S. accounts and investments of millions of U.S. citizens and lawful permanent residents, they will begin to issue Substitute Returns in mass. This will cause an entire “parade of horribles” such as the following:

- The foreign addresses will often be incorrect or the regular mail service will simply not be able to effectively deliver the IRS correspondence to the non-U.S. address;

- There will be mismatching of taxpayer identification numbers;

- The IRS will mix up financial information, assets and accounts among Individuals with the same names (e.g., Juan Perez Gonzalez or Mary Johnson) who are living overseas, particularly since there is no global taxpayer identification number system, which will distort terribly the tax assessments the IRS makes;

- The information and reports created by the IRS will be entirely in English, and then sent overseas to countries where English is not a first language and where the taxpayer may have little to no command over the English language;

- Incorrect currency calculations, since most of the time the USC or LPR residing overseas will have their accounts in currencies other than U.S. dollars;

Finally, the last major disadvantage of the USC or LPR overseas in these cases, is that the law creates a “presumption of correctness” in favor of the IRS and their determinations (at least in the civil law context – which is where this part of the tax administration lies). See an earlier post:

Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

This presumption of correctness was confirmed by the U.S. Supreme Court and therefore imposes the burden on the taxpayer of proving that the assessment made by the IRS is erroneous.

See and eariler post, More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

See, U.S. Supreme Court decision, Welch v. Helvering, 290 U.S. 111 (1933), stating that the Commissioner’s “ . . .

At the end of the day, the USC or LPR residing overseas is at a terrible disadvantage as they need to identify U.S. tax law principles applicable to their case (which almost always means they need to hire a U.S. tax professional and incur those costs) and respond within a very short window of time to the IRS. They also have to prove the IRS was wrong in its determinations made in the Substitute Return.

How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

The separation of powers is often on full display when there are key Congressional hearings focused on the work (or lack thereof) undertaken by the key executive branch agencies responsible for tax enforcement:

1. Treasury/IRS, and

2. Justice Department.

There is an important reason why every day taxpayers should be interested in these hearings; particularly those who are considering renouncing United States Citizenship.

The actions and reactions of the IRS and Justice Department are often in response to Congressional hearings. This is very much the case with individual taxpayers with assets throughout the world.

A brief timeline of various hearings, and actions taken by the IRS and Justice Department (largely in response to such criticism) can be followed to demonstrate the influence of these hearings:

U.S. Senate Permanent Subcommittee on Investigations, published their report on August 1, 2006, entitled Tax Haven Abuses: The Enablers, The Tools & Secrecy.

Little direct action was taken by the IRS or Justice Department in this year. It was the year 2008, where the direct hearings lead to more direct action taken.

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on July 16, 2008, entitled Tax Haven Banks and U.S. Tax Compliance –

November 2008, a U.S. federal grand jury indicted the Chairman and CEO of UBS Global Wealth Management and Business Banking.

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on March 4, 2009 Tax Haven Banks and U. S. Tax Compliance – Obtaining the Names of U.S. Clients with Swiss Accounts

UBS agrees in February 2009 to pay a US$780M fine to the U.S. government and enter into a deferred prosecution agreement on charges of conspiring to defraud the United States by impeding the Internal Revenue Service.

IRS Implements first Offshore Voluntary Disclosure Program (“OVDP”) on March 26, 2009

Numerous taxpayers and several Swiss bankers were indicted and/or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

Congress passes and the President signs into law, the Foreign Account Tax Compliance Act (“FATCA”) in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act.

IRS Implements its second Offshore Voluntary Disclosure Initiative (“OVDI”) in 2011.

Numerous taxpayers and several Swiss financial advisors were indicted; and a HSBC Indian client was also indicted or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

IRS creates an open ended OVDP program in 2012 that continues; with modifications made in 2014.

Several taxpayers were indicted; including those implicating an Israeli bank for various tax crimes charges. . See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains commitments from various countries to sign various FATCA, intergovernmental Agreements (“IGAs”) for automatic exchange of financial information; France, Germany, Italy, Spain, United Kingdom, Denmark and Mexico.

In January 2013, the U.S. Attorney’s Office in the Southern District of New York secured the guilty plea of Wegelin Bank, the oldest private bank in Switzerland and the first foreign bank to plead guilty to felony tax charges.

In August, 2013, the United States and Switzerland Issue Joint Statement Regarding Tax Evasion Investigations and ability of Swiss banks to enter into deferred prosecution agreements.

Several taxpayers were indicted and advisors; including multiple financial institutions outside of Switzerland for various tax crimes charges. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains more commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information;.

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on February 26, 2014 Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

See prior post, Hearings – Permanent Subcommittee on Investigations – re: Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts – February 26, 2014

Posted on February 26, 2014 Updated on March 2, 2014

IRS announces on June 18, 2014, IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance

See, “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The Treasury Department obtains numerous commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information. See, HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

Will the IRS treat a USC or LPR residing outside the U.S. who purposefully refuses to file U.S. income tax returns and information returns the same as “tax protesters”?

What is a “tax protester”? What is the significance for USCs and LPRs residing overseas?

What if the U.S. tax and its applicability to USCs and LPRs living overseas, specifically including the tax on expatriation seems unfair, unjust, overreaching, burdensome, etc.? Is that a legal basis for defying the law’s application and reach?

The author has consistency argued, that from a tax policy perspective, U.S. citizenship based taxation of worldwide income for those who live outside the U.S. needs to be repealed as it is unique in the world, dates to the 19th Century Civil War and is inappropriate for the global world we live in. See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

“Tax protesters” and their frivolous arguments generally assert, somehow the U.S. federal tax laws are against the U.S. Constitution; i.e., unconstitutional. The U.S. Supreme Court has already ruled that U.S. citizenship based taxation is indeed Constitutional when it upheld as Constitutional the concept of citizenship based taxation in 1924 in Cook v. Tait. In that case, the U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife. See, Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50)

These Constitutional arguments are not looked well upon by any branch of the U.S. federal government. The IRS and Tax Division of the Department of Justice regularly prosecute these cases. The Courts regularly uphold the government’s position; and the Congress has passed increasingly harsh penalties, including as late as in 2007 (See IRC section 6702 – Frivolous Tax Submissions).

The term “tax protester” became somewhat taboo after Congress passed a law designed at protecting taxpayer’s rights. The current, more politically correct terminology comes from the National Tax Defier Initiative, also known as the “TAXDEF Initiative” which was launched by the Tax Division of the DOJ.

In short, the Courts, specifically including the U.S. Supreme Court have consistently rejected a range of arguments that the tax law is unconstitutional. Those individuals who advance such arguments, which have consistently been upheld as frivolous legal arguments, are commonly referred to as “tax defiers” or “tax protesters.”

A classic quote from the 7th Circuit is apropos – Coleman v. Commissioner, 791 F.2d 68, 69 (7th Cir. 1986) –

- Some people believe with great fervor preposterous things that just happen to coincide with their self-interest. “Tax protesters” have convinced themselves that wages are not income, that only gold is money, that the Sixteenth Amendment is unconstitutional, and so on. These beliefs all lead—so tax protesters think—to the elimination of their obligation to pay taxes.

Hoards of taxpayers have been found liable for civil penalties, civil fraud penalties and criminal liability (in the most egregious of cases – with prison sentences) over the years as they have asserted a range of arguments found to be frivolous.

Will the IRS or the Tax Division of the DOJ take a similar position against UCS or LPRs who have resided overseas who argue the U.S. tax law should not apply to them? See an earlier post, Tracking U.S. Citizens and LPRs in and Out of the Country – Tracking Taxpayers (Entry/Exit System)

Who in the government will test the limits of enforcement overseas? Will the long-arm of the U.S. federal government, and its enforcement, grow even longer? Will information collected by the IRS via FATCA enable the government to compile and pursue such cases? See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

Read Wikipedia for a colorful overview of – Tax protester history in the United States

Tracking U.S. Citizens and LPRs in and Out of the Country – Tracking Taxpayers (Entry/Exit System)

The U.S. federal government, led by the Department of Homeland Security (“DHS”) has taken great efforts and incurred great cost to develop technology and systems to track individuals as they come into the U.S. There are also programs afoot, specifically the Entry/Exit system with Canada, that helps track individuals as they leave the U.S. For more details, see the Wilson Center and its review of the Entry-Exit Systems in North America.

This tracking is very specific and part of the TECS database that is operated and managed by the DHS. The TECS database has been discussed in prior posts, including Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

See also, an earlier post that discusses the TECS database and its usage by the Internal Revenue Service in U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

This topic will become even more relevant starting in 2015 as the IRS collects financial and account information via FATCA of USCs and LPRs residing in various countries throughout the world.

A series of posts dedicated to this topic will be made, including by guest immigration lawyers, discussing various legal implications of the tracking of U.S. citizens and LPRs.