International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

EB-5 Visa – a common Path to a “Green Card” and then USC

Pathways to United States Citizenship – (USC): Focus on the EB-5

Every individual who ultimately becomes a naturalized U.S. citizen must first qualify for lawful permanent resident (“LPR”) status unless a narrow statutory exception applies. Although public attention frequently focuses on the EB-5 immigrant investor program, with the idea they are those with greater assets and income (contemplating taxes) EB-5 investors represent only a very small percentage of all individuals who become lawful permanent residents. Understanding the relative size of each immigration pathway is essential because every pathway ultimately raises many of the same U.S. tax issues—including worldwide income taxation, estate and gift taxation, and the tax consequences of later abandoning lawful permanent resident status or renouncing U.S. citizenship.

The EB-5 visa has been a fixture of U.S. law since the early 1990s. It was not until 2009 that a substantial number of EB-5 visas were issued in a given year, 4,218 to be exact. Statistically, the total EB-5 visa leading to LPR status is a fraction of the other categories as explained here. For an excellent overview of the law and categories, see the CRS report- Permanent Legal Immigration to the United States: Policy Overview (Updated November 4, 2024)

EB-5 Visa – to a “Green Card” then to United States Citizenship – (USC)

From the laws inception in 1992 through FY2004, there were only 6,024 EB-5 visas issued during that 12 year period. That is an annual average of only approximately 500 persons. See, the GAO Report on Immigrant Investors. As the program grew in popularity so too did the location of investors from around the world. It was not until 2009 when the total number of investors started growing substantially. Most significantly in 2009 when 4218 EB5 visas were issued, still less than 1/2 of the 10,000 allocated annually by the statute.

These numbers kept going at an annual pace especially starting in 2012, when 6,764 EB-5 visas were issued and then around 10K+/- annually for the last dozen years or so, up until the years that were impacted by a change in the law and a bit by COVID (2020 and 2021).

Chinese Investors Have Dominated the total Group of EB-5 Investors

The country-of-origin analysis is important because practitioners frequently advise clients from these jurisdictions regarding immigration planning, cross-border tax planning, and eventual expatriation planning with consequences in those countries.

I have compiled the total list of countries from which EB-5 visa investors came from as summarized in the Country of Origin global graphic for FYE 2024. There are over 100 countries from which these investors came from, but again, China is the dominant country, followed by Vietnam, India, Taiwan and then South Korea as the countries with the greatest number of investors. South Africa comes next, followed by Brazil and then Mexico, but each with less than 200 total investors, each country as follows:

China

9547

Vietnam

1533

India

1428

Taiwan

513

Korea, South

325

South Africa

158

Brazil

157

Mexico

128

Hong Kong S.A.R.

116

Venezuela

97

Canada

81

Great Britain & N. Ireland

63

Russia

58

Nigeria

52

Turkey

44

Colombia

44

France

38

United Arab Emirates

30

Germany

29

Japan

25

Singapore

23

Kazakhstan

21

Peru

20

Ukraine

17

Sweden

15

Argentina

15

Egypt

14

The importance of this analysis is to help individuals (and their advisors) who fit into these categories, e.g., who have a pathway to a green card and then on to become a naturalized U.S. citizen, understand the potential “tax expatriation” consequences of their decisions over the long-run.

What are the U.S. “tax expatriation” consequences to individuals who go down these pathways, including to their dependent children, or spouses or any future beneficiaries who are “United States person”?

What are the tax expatriation consequences if the individual later decides they do not want to be a green card holder or a U.S. citizen and later wishes to abandon their lawful permanent residency status or formally renounce their U.S. citizenship?

These and many other questions should be considered, especially for long-term family planning. Not just for the investor, but for their children and spouse, who may be eligible for the visa that can lead to LPR status and eventually to USC. Facilitating younger children (under 21 years of age) is a common driver for EB-5 investors for families who want the United States to be a pathway for their children’s’ future.

Why These Immigration Pathways Matter from a Tax Perspective

Every pathway leading to lawful permanent resident status almost always subjects the individual to the comprehensive U.S. federal income tax system. Depending upon the individual’s assets, family structure, treaty residence, and future living plans, obtaining a green card will also have significant implications for:

worldwide income taxation;

estate and gift taxation;

foreign trust reporting;

information reporting obligations under various laws;

controlled foreign corporation rules;

PFIC reporting;

exit tax planning; and

long-term succession planning.

Equally important, many lawful permanent residents eventually decide to return permanently to their country of origin or another foreign jurisdiction. Those individuals—and frequently their spouses and dependent children—must carefully consider the tax consequences of formally abandoning lawful permanent resident status or, after naturalization, renouncing U.S. citizenship. The sooner individuals and their advisors realize these consequences, the better they can plan for important life decisions.

Those tax consequences are collectively referred to as the U.S. tax expatriation rules, and they form the principal subject of this website.

The legal pathways towards lawful permanent residency status can be broken down into the following categories and the EB-5 category is a fraction (only about 1%) of the total pool leading to LPR status:

This category includes EB-1 through EB-5 categories that include individuals with extraordinary ability, certain professionals, other skilled workers. The chart I prepared here reflects the total number of EB-5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b).

EB-1, EB-2 and EB-3 represent the greatest group of individuals who obtained LPR status (e.g., approximately 5X, each category compared to the EB-5 category). See Yearbook of Immigration Statistics, Table 6.

For instance, annually the EB-1 through EB-3 categories are processing about 50K per year of each, and the EB-5 category is only 131K over most of its 25 year life (or about 10K per year – for more recent years). Approximately 16% of all green card holders come through these employment based preferences.

Table – Approximate Decade-Average Share by Category, FY2014–FY2023

Category

Approx. Share

Notes

Family-sponsored (total)

~64%

Immediate relatives + family preferences combined

— Immediate relatives

~46%

Spouses ~26%, parents ~14%, children ~6%

— Family preferences (F1–F4)

~18%

Numerically capped at 226,000

Employment-based (EB-1–EB-5)

~16%

Capped at 140,000; breached in COVID years

Refugees & asylees

~12%

Numerically unlimited; ceiling-driven volatility

Diversity

~4%

Statutory ceiling 55,000

All other / special

~4%

SIV, U/T victims, cancellation, registry, etc.

C. Diversity Immigrant Program

The annual diversity lottery, allocated by random selection, to natives of countries with historically low rates of immigration to the United States. See, 8 U.S. Code § 1153(c). The Attorney General plays a key role by statute in this determination. There is a statutory maximum of 55,000 and only represents about 4% of all LPRs compared to the larger pool. This program is on hold as of December 19, 2025 when the USCIS policy memorandum (PM-602-0193) directs officers to place an immediate hold on pending adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

D. Humanitarian and Special Pathways: Refugees/Asylees

Several routes proceed outside the preference system (the three categories above). Refugees and asylees adjust under a specific statutory regime; self-petitioning abused spouses and children proceed under other provisions; victims of qualifying crimes and of trafficking can adjust from U and T nonimmigrant status; and certain children subject to qualifying juvenile-court findings can qualify, among others. There are statutory limits placed on this group.

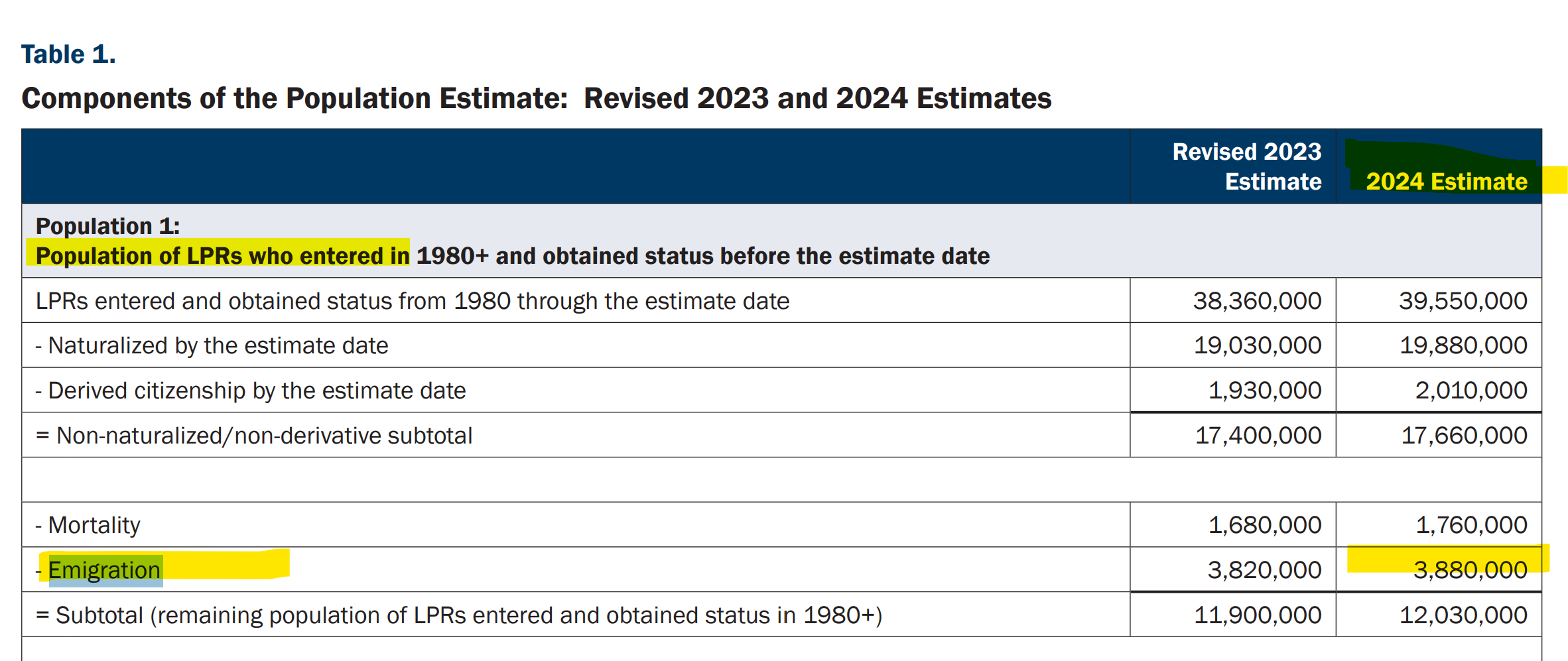

Whatever category one uses for LPR status, there will be important U.S. federal tax consequences to them and typically their family members. That’s the large part of the focus on this forum where the author has written about the subject of how it all ties to “tax expatriation”. As previously reported, there are 3.88 million “LPR” individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. See, Table 1 of the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

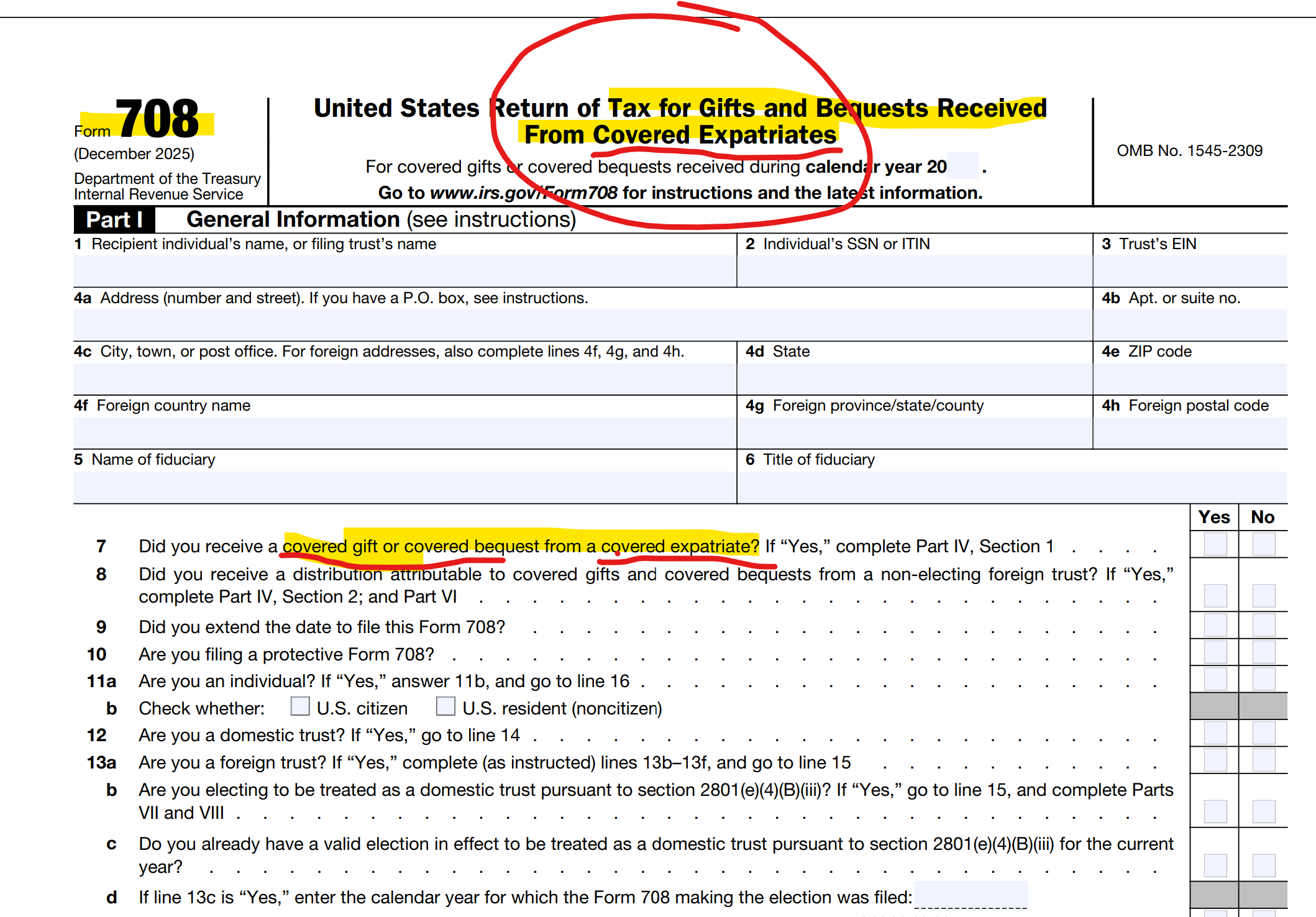

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

These regulations are extensive and provide an explanation of the purpose of these rules.

II. Purpose of Foreign Gift and Trust Provisions

During the mid- to late-1990s, abusive tax schemes, including offshore schemes involving foreign trusts, reemerged in the United States after reaching their last peak in the 1980s. GAO, Efforts to Identify and Combat Abusive Tax Schemes Have increased, but challenges remain, GAO–02–733 (Washington, DC: May 22, 2002). In these schemes, foreign trusts were used to transfer large amounts of assets abroad, where it was much more difficult for the IRS to identify whether U.S. persons owned a trust.

interest in such trusts, and whether such persons were reporting and paying the required taxes on their income from such trusts. Many of the foreign trusts were established in tax haven jurisdictions with bank secrecy laws. Before the 1996 Act amended sections 6048 and 6677, there was no Form 3520-A), which was limited to five percent of the transfer or corpus of the trust, as applicable, not to exceed $1,000. In light of this, it was difficult for the IRS to obtain information about income earned by U.S.-owned foreign trusts and distributions to U.S. beneficiaries from foreign trusts, and Sections 6048 and 6677 were generally ineffective in ensuring that U.S. persons provided this information. information. The result was “rampant tax evasion.” 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan). Requirement for U.S. Persons to Report Distributions from Foreign Trusts and the Penalty for Failure to Report Transfers to a Foreign Trust or an Annual Foreign Trust Information Statement (in Federal Register/Vol. 89, No. 90/Wednesday, May 8 of 2024/Proposed Rules and 141 Cong. Rec. S13859 (daily edition of September 19, 1995) (comments by Senator Moynihan).

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

Three Precedent Setting Cases in International Information Reporting (“IIR”) in 6 Weeks: * Aroeste, * Bittner, and * Farhy: all Interconnected via Title 26, Title 31 and U.S. Income Tax Treaties

In just over six weeks, there have been three key judicial precedents favorable to international individuals. These cases have helped clarify the requirements of individuals and the limitations on the powers of the IRS in assessing IIR penalties. Please see the full article on tax notes. These IIR decisions relate to:

Title 31 penalties for Foreign Bank Account Reports (“FBARs”),

How these two federal statutory regimes of Title 31 and 26 crossover into international law as set forth in U.S. income tax treaties negotiated with different countries around the world.

Each of these three cases are interconnected and have significant impact to individuals with global lives, global assets, multi-national family members and those who have businesses or accounts in different parts of the world.

Aroeste v. United States

First, on February 13th, 2023, the Southern District of California District Court (the “District Court”) made a key determination in a Joint Discovery Motion decision in Aroeste.[2] The District Court concluded in Aroeste that the IRS/DOJ[3] could not ignore the U.S.-Mexico income tax treaty (“Treaty”) and its application to a Mexican national who has resided almost all of his life in Mexico City and has maintained a “green card” for immigration purposes in the United States. It is a non-willful FBAR case. The District Court applied the interconnected statutes and regulations of Titles 31 and 26 to help determine who qualifies as a “United States person”; specifically with reference to international law and obligations set forth in the Treaty. The key question in that case that remains to be answered is who (specifically Mr. Aroeste and by extension to a pool of millions of green card individuals residing outside the United States who are not citizens[4]) must file FBARs?

Second, on February 28th, 2023, the Supreme Court of the United States (“SCOTUS”) resolved in Bittner[5], that the applicable non-willful FBAR penalty is not measured by every foreign account of the individual as the Service has argued for years. That case also dealt with non-willful filing of FBARs and the SCOTUS concluded the IRS cannot impose penalties of $10,000 on each and every account held; but rather the penalty is “per report” that was not correctly filed. Hence, the total maximum penalty per year is $10,000. A maximum penalty of $50,000 (x5 years) applied per the SCOTUS versus the IRS determined amount of US$2.7M+.

Farhy v. Commissioner

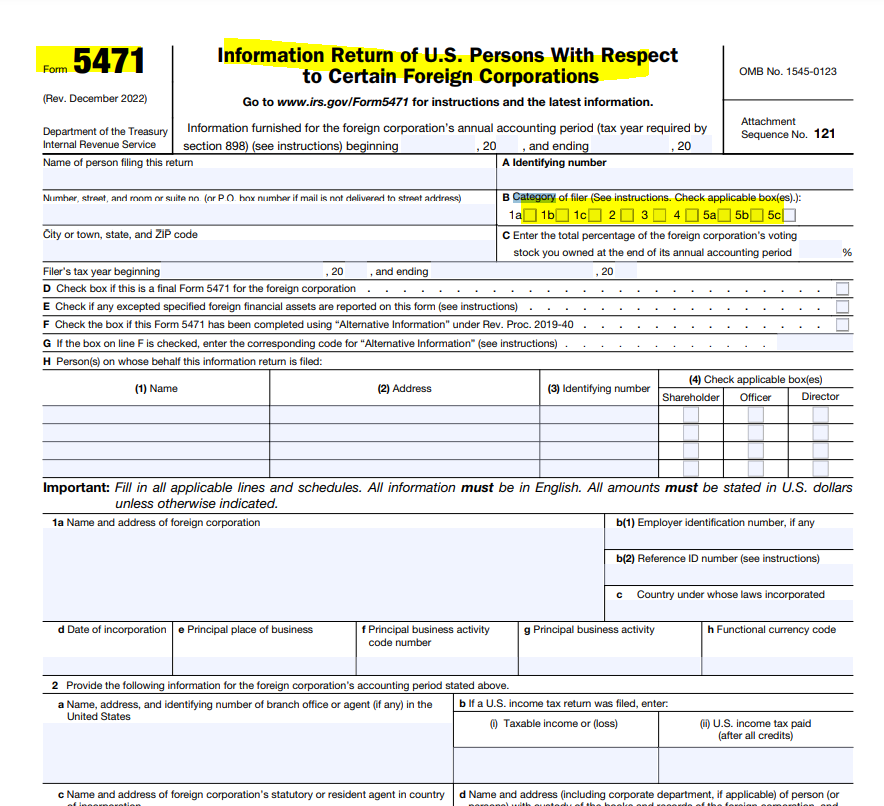

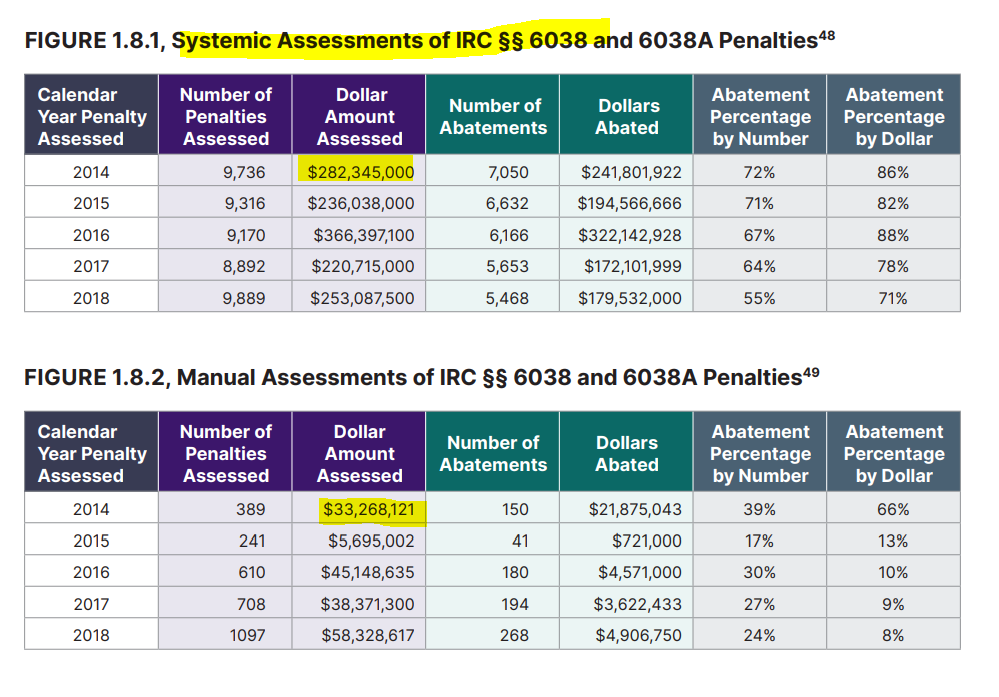

Lastly, on April 3rd, 2023, the United States Tax Court (the “Tax Court”) issued a decision in Farhy,[6] stating that the IRS does not have statutory authority to assess IIR penalties under section 6038(b). The IIR that is required by this statute is IRS Form 5471, which includes multiple filing categories. This has far reaching implications about how the government will be able to collect the IIR penalties the Service administratively determines are owed.[7] The Taxpayer Advocate previously issued a report on point titled: The IRS’s Assessment of International Penalties Under IRC §§ 6038 and 6038A Is Not Supported by Statute, and Systemic Assessments Burden Both Taxpayers and the IRS[8] In that report, the Taxpayer Advocate identified more than $310M of penalties just for the tax year 2014 the IRS “assessed” under Sections 6038 and 6038A.[9] We now know these “assessments” were invalid.

[1] See, footnote 19 regarding United States Tax Court’s Order in the case of Alberto Aroeste & Estela Aroeste vs. Commissioner.

[3] The “IRS” or the “Service” are used as shorthand for the Internal Revenue Service; and the Department of Justice; Tax Division is referred to as the “DOJ.”

[4] See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year and 4.8 million are estimated to have died and/or emigrated. The authors have extrapolated from these estimates in the report to conclude that more than 3 million of these individuals have emigrated and left the United States. The millions of individuals do not reside in the U.S. of which Mr. Aroeste is one of these individuals; although a tax treaty must exist in the country of residence for the analysis of the District Court in Aroeste v. United States to be applicable.

[5] No. 31—1195 (U.S. Feb. 28, 2023); 598 U. S. ____ (2023); The majority opinion by Justice Gorsuch cited to the ACTEC amicus brief (where Patrick W. Martin, the author of tax-expatriation.com and a fellow of ACTEC worked on the drafting of the brief) and concluded:

“Best read, the BSA treats the failure to file a legally compliant report as one violation carrying a maximum penalty of $10,000, not a cascade of such penalties calculated on a per-account basis.” The ACTEC brief was cited by the majority opinion- “ We see evidence, too, that the point of these reports is to supply the government with information potentially relevant to various kinds of investigations, criminal and civil alike. But what we do not see is any indication that Congress sought to maximize penalties for every nonwillful mistake (whether a late filing, a transposed account number, or an out-of-date bank address). See Brief for American College of Trust and Estate Counsel as Amicus Curiae 5–7.”

[7]See, Patrick W. Martin, Megan L. Brackney, Robert Horowitz, and Javier Diaz de Leon Galarza: Problems Facing Taxpayers with Foreign Information Return Penalties, November 12, 2020.

IRS Creates “International Practice Units” for their IRS Revenue Agents in International Tax Matters

The U.S. international tax law has become increasingly complex. I am confident when I say that very few individuals in the world (including IRS revenue agents) understand the complexities of Title 26 and Title 31 as they apply to international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

Most USCs and LPRs who live in the U.S. certainly know and understand the basics of IRS Form 1040.

The lack of knowledge of these complex laws within the IRS, and the LB&I (Large Business and International group) which specializes in international matters has led to IRS “International Practice Units”. These are designed to allow IRS revenue agents who are not necessarily specialists in the international tax area to review transactions and be prepared to assess taxes and penalties against USCs and LPRs in the international context. The preamble says in part ” . . . Practice Units provide IRS staff with explanations of general international tax concepts as well as information about a specific type of transaction. . . ”

These IRS materials give a good perspective from where the IRS views the world; including the introduction to this particular IRS International Practice Unit where it states: “This Practice Unit focuses on a U.S. Person’s proactive steps to “conceal” their ownership of foreign financial accounts, entities and other assets for the purposes of tax avoidance or evasion, even though, there may be some situations where there are legitimate personal or business purposes for establishing such arrangements. This unit falls under the outbound face of the matrix and thus, will focus on U.S Persons living in the United States . . . Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .” [emphasis added]

This is a breathtaking statement from the IRS internal training manuals that “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .”?

The vast majority of the USCs or LPRs who I see who renounce or abandon their citizenship or LPR status, are living outside the United States and in most cases have spent almost all (if not all) of their lives outside the U.S.

Does the IRS mean that a family living in Switzerland that have dual national family members are “. . . .simply hiding the accounts from the Internal Revenue Service . . . ” if they are using, for instance, a Liechtenstein Stiftung to hold their family assets as part of an estate plan recommended to them by their Swiss legal and tax advisers?

Does the statement that this IRS International Practice Unit focuses on ” . . . U.S Persons living in the United States . . . ” give USCs and LPRs residing outside the U.S. relief from the IRS perspective of USCs simply hiding assets from the Internal Revenue Service? Will IRS revenue agents be sophisticated enough to distinguish between these two different groups; U.S. resident versus non-resident USCs and LPRs? Will the law be applied differently with respect to these resident versus non-resident U.S. taxpayers?

What role will these IRS “International Practice Units” play in forming perceptions and molding ideas of IRS revenue agents who have had little to no life experience in international affairs, multi-national families, global finance and international business operations?

which has a chart reflecting the total Chinese investors as a percentage of total – Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

which has a chart reflecting the total Chinese investors as a percentage of total – Part II of Part II: The Gold Card – The U.S. Tax Costs – “It’s like the green card, but better and more sophisticated.”

5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b).

5 visas issued cumulative. This chart reflects the total number of cumulative EB-5 visas that have been issued through the FYE 2024 of approximately 131K. This does not take into consideration how many of these were issued to the principle investor versus spouses and children under twenty-one years of age. See, 8 U.S. Code § 1153(b). adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

adjustment of status, ancillary benefits and associated waiver applications for individuals applying through the Diversity Immigrant Visa program. [1, 2]

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —