Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

This is Part II, a follow-on discussion of older U.S. case law and IRS rulings that address how and when individuals are subject to U.S. taxation before and after they assert they are no longer U.S. citizens.

I might point out that I am of the belief that we humans always like to hear the news we want to hear; and/or interpret it in the way we find most beneficial to us. Who doesn’t like good news versus bad news? Whether we (laypeople and tax lawyers alike) interpret Section 877A(g)(4) in any particular way; it is of no real consequence when it is the IRS that will enforce the law and ultimately the Department of Justice, Tax Division who will handle any such case interpreting this provision before a U.S. District Court or the Court of Federal Claims. For those who have not litigated before these Courts and seen how aggressive are the government lawyers in advocating for the government, the following discussion will hopefully be illustrative.

See, Part I: Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4)), dated October 16, 2015.

The question is what is the correct date of “relinquishment of citizenship” as defined in the statute; IRC Section 877A(g)(4)? Many argue the law cannot be applied retroactively?

However, the specific case discussed here, did just that; applied the law retroactively to determine U.S. citizenship status of an individual and corresponding tax obligations. This was also in a time of a much simpler tax code with (i) no international information reporting requirements (e.g., IRS Forms 8938, 8858, 5471, 8865, 3520, 3520-A, 926, 8621, etc.), (ii) no Title 31 “FBAR” reporting requirements and (iii) no constant drumbeat by the IRS of international taxpayers and enforcement. See, recent announcement by IRS on Oct. 16, 2015 (one day after tax returns were required to be filed by many) Offshore Compliance Programs Generate $8 Billion; IRS Urges People to Take Advantage of Voluntary Disclosure Programs. However, for cautionary posts on the IRS OVDP and the deceptive numbers published (e.g., “$8 Billion”), see How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Of course, the answer to this question helps determine if and when will the individual be subject to the federal tax laws of the U.S. on their worldwide income and global assets. In the case of Ms. Lucienne D’Hotelle (an interesting 1977 appellate opinion from the firs circuit) she had spent little time in the U.S. and had sent a letter in her native language French to the U.S. Department of State, which stated “I have never considered myself to be a citizen of the United States.” This is not unlike many individuals around the world today; at least as of late – in the era of FATCA, who assert they are not a U.S. citizen because they “relinquish[ed] it by the performance of certain expatriating acts with the required “intent” to give up the US citizenship” and did not notify the U.S. federal government.

The Court nevertheless found Ms. Lucienne D’Hotelle retroactively subject to U.S. income taxation on her non-U.S. source income (up until she received a certificate of loss of nationality from the Department of State); for specific years even when the immigration law provisions of the day said she was no longer a U.S. citizen during that same retroactive period.

There have been many contemporary commentators who argue an individual does not need to (i) have, (ii) do, or (iii) receive any of the following, and yet still should be able to successfully argue they have shed themselves of U.S. citizenship and hence the obligations of U.S. taxation and reporting on their worldwide income and global assets –

(i) receive a U.S. federal government issued document (e.g., a certificate of loss of nationality “CLN” per 877A(g)(4)(C)),

(ii) receive a cancelation of a naturalized citizen’s certificate of naturalization by a U.S. court (per 877A(g)(4)(D)),

(iii) provide a signed statement of voluntary relinquishment from the individual to the U.S. Department of State (per 877A(g)(4)(B)), or

(iv) provide proof of an in person renunciation before a diplomatic or consular officer of the U.S. (per paragraph (5) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481(a)(5)), in accordance with 877A(g)(4)(C)).

Some older tax cases that interpreted similar concepts are worthy of consideration. They will certainly be in any brief of the attorneys for the U.S. Department of Justice, Tax Division and/or Chief Counsel lawyers for the IRS in any case where the individual challenges that none of the above items are required in their particular case to avoid U.S. taxation and reporting requirements.

The D’Hotelle case is illustrative of the efforts taken by the Department of Justice, Tax Division in collecting U.S. income tax on a naturalized citizen. You will notice they did not take a sympathetic approach to her case. Ms. Lucienne D’Hotelle was born in France in 1909 and died in 1968 in France, yet the U.S. government continued to pursue collection of U.S. income taxation on her foreign source income from the Dominican Republic, France and apparently Puerto Rico even after her death during a period of time when she used a U.S. passport. Lucienne D’Hotelle de Benitez Rexach, 558 F.2d 37 (1st Cir.1977). She, not unlike many individuals today, claimed she was not a U.S. citizen – or at least stated “I have never considered myself to be a citizen of the United States.”

Some of the particularly interesting facts relevant to Ms. D’Hotelle, a naturalized citizen, which are relevant to the question of U.S. taxation of citizens, were set forth in the appellate court’s decision as follows:

Lucienne D’Hotelle was born in France in 1909. She became Lucienne D’Hotelle de Benitez Rexach upon her marriage to Felix in San Juan, Puerto Rico in 1928. She was naturalized as a United States citizen on December 7, 1942. The couple spent some time in the Dominican Republic, where Felix engaged in harbor construction projects. Lucienne established a residence in her native France on November 10, 1946 and remained a resident until May 20, 1952. During that time s 404(b) of the Nationality Act of 1940 provided that naturalized citizens who returned to their country of birth and resided there for three years lost their American citizenship. On November 10, 1947, after Lucienne had been in France for one year, the American Embassy in Paris issued her a United States passport valid through November 9, 1949. Soon after its expiration Lucienne applied in Puerto Rico for a renewal. By this time she had resided in France for three years.

* * *

On May 20, 1952, the Vice-Consul there signed a Certificate of Loss of Nationality, citing Lucienne’s continuous residence in France as having automatically divested her of citizenship under s 404(b). Her passport . . . was confiscated, cancelled and never returned to her. The State Department approved the certificate on December 23, 1952. Lucienne made no attempt to regain her American citizenship; neither did she affirmatively renounce it.

* * *

Predictably, the United States eventually sought to tax Lucienne for her half of that income. Whether by accident or design, the government’s efforts began in earnest shortly after the Supreme Court invalidated *40 the successor statute to s 404(b). In in Schneider v. Rusk, 377 U.S. 163 (1964), the Court held that the distinction drawn by the statute between naturalized and native-born Americans was so discriminatory as to violate due process. In January 1965, about two months after this suit was filed, the State Department notified Lucienne by letter that her expatriation was void under Schneider and that the State Department considered her a citizen. Lucienne replied that she had accepted her denaturalization without protest and had thereafter considered herself not to be an American citizen.

There are other facts that make clear the government was not fond of her husband, the income that he earned and how he managed his and his wife’s assets during and after her death. The Court also discusses at length the fact that she had used a U.S. passport during the years when she alleges she was not a U.S. citizen. The Court goes on to analyze her U.S. citizenship, and the following discussions are illustrative of the ultimate tax consequences.

LUCIENNE’S CITIZENSHIP

The government contends that Lucienne was still an American citizen from her third anniversary as a French resident until the day the Certificate of Loss of Nationality was issued in Nice. This case presents a curious situation, since usually it is the individual who claims citizenship and the government which denies it. But pocketbook considerations occasionally reverse the roles. United States v. Matheson, 532 F.2d 809 (2nd Cir.), cert. denied 429 U.S. 823, 97 S.Ct. 75, 50 L.Ed.2d 85 (1976). The government’s position is that under either Schneider v. Rusk, supra, or Afroyim v. Rusk, 387 U.S. 253, 87 S.Ct. 1660, 18 L.Ed.2d 757 (1967), the statute by which Lucienne was denaturalized is unconstitutional and its prior effects should be wiped out. Afroyim held that Congress lacks the power to strip persons of citizenship merely *41 because they have voted in a foreign election. The cornerstone of the decision is the proposition that intent to relinquish citizenship is a prerequisite to expatriation.

12 Section 404(b) would have been declared unconstitutional under either Schneider or Afroyim. The statute is practically identical to its successor, which Schneider condemned as discriminatory. Section 404(b) would have been invalid under Afroyim as a congressional attempt to expatriate regardless of intent. Likewise it is clear that the determination of the Vice-Consul and the State Department in 1952 would have been upheld under then prevailing case law, even though Lucienne had manifested no intent to renounce her citizenship. Mackenzie v. Hare, 239 U.S. 299, 36 S.Ct. 106, 60 L.Ed. 297 (1915). Accord, Savorgnan v. United States, 338 U.S. 491, 70 S.Ct. 292, 94 L.Ed. 287 (1950). See also Perez v. Brownell, 356 U.S. 44, 78 S.Ct. 568, 2 L.Ed.2d 603 (1958), overruled, Afroyim v. Rusk, supra.

411 F.Supp. at 1293. However, the district court went too far in viewing the equities as between Lucienne and the government in strict isolation from broad policy considerations which argue for a generally retrospective application of Afroyim and Schneider to the entire class of persons invalidly expatriated. Cf. Linkletter v. Walker, supra. The rights stemming from American citizenship are so important that, absent special circumstances, they must be recognized even for years past. Unless held to have been citizens without interruption, persons wrongfully expatriated as well as their offspring might be permanently and unreasonably barred from important benefits. Application of Afroyim or Schneider is generally appropriate.* * *

During the interval from late 1949 to mid-1952, Lucienne was unaware that she had been automatically denaturalized.

* * *

Fairness dictates that the United States recover income taxes for the period November 10, 1949 to May 20, 1952. Lucienne was privileged to travel on a United States passport; she received the protection of its government.

_

It’s quite interesting that the Court uses and focuses on fairness as to the U.S. government, more than a discussion of “fairness” to the individual. The use of the passport seems to be an integral fact. Here, the Court determined she was retroactively a U.S. citizen and hence subject to taxation on her worldwide income during those crucial periods (1949 through 1952) even though (1) the U.S. Department of State said she was not a U.S. citizen during that time, and (2) she stated “I have never considered myself to be a citizen of the United States.”

_

101112 Although the government has not appealed the decision with respect to taxes from mid-1952 through 1958, the district court was presented with the issue. We wish to explain why the government should be allowed to collect taxes for the two and one-half year interval but not for the subsequent period. The letter from Lucienne to the Department of State official in 1965, which appears in English translation in the record, states that after the Certificate of Loss of Nationality, “I have never considered myself to be a citizen of the United States.” We think that in this case this letter can be construed as an acceptance and voluntary relinquishment of citizenship. We also find that in this particular case estoppel would have been proper against the United States. Although estoppel is rarely a proper defense against the government, there are instances where it would be unconscionable to allow the government to reverse an earlier position. Schuster v. Commissioner of Internal Revenue, 312 F.2d 311, 317 (9th Cir. 1962). This is one of those instances. Lucienne cannot be dunned for taxes to support the United States government during the years in which she was denied its protection. In Peignand v. Immigration and Naturalization Service, 440 F.2d 757 (1st Cir. 1971), this court refused to decide whether estoppel could apply against the government. A decision on the question was unnecessary, since the petitioner had not been led to take a course of action he would not otherwise have taken. Id. at 761. Here, Lucienne severed her ties to this country at the direction of the State Department. The right hand will not be permitted to demand payment for something which the left hand has taken away. However, until her citizenship was snatched from her, Lucienne should have expected to honor her 1952 declaration that she was a taxpayer.

_

Of particular note, the Court highlighted that the Department of State (one hand) cannot take away citizenship, the individual’s passport and issue a certificate of loss of nationality (“CLN”), and the IRS (on the other hand) impose taxation for the time period after the CNL was issued.

–

One point of emphasis by the Court was how U.S. citizenship rights are a highly protected right; as articulated by the U.S. Supreme Court. That high protection granted, serves to aid those individuals who defend against a government arguing they somehow ceased to be a U.S. citizen. Of course, for those trying to escape U.S. taxation, the result is not a desired one “. . . a curious situation, since usually it is the individual who claims citizenship and the government which denies it. . . “

–

C’est la vie Ms. Lucienne D’Hotelle!

Will 2015 Be a Record Year for Citizenship Renunciations?

USCs without a Social Security Number (and a Passport) Cannot Travel to the U.S.

Recent posts have focused on the dilemma facing U.S. citizens (USCs) who have no social security number (“SSN”). See an older post (23 July 2014) – Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

These problems are quickly coming to the surface, now that financial institutions  (“FFIs”) around the world and private companies and trusts (e.g., non-financial foreign entities -NFFEs) must have their owners and clients certify they are not U.S. citizens; OR report the accounts of such U.S. citizens to the IRS under FATCA and the intergovernmental agreements (“IGAs”).

(“FFIs”) around the world and private companies and trusts (e.g., non-financial foreign entities -NFFEs) must have their owners and clients certify they are not U.S. citizens; OR report the accounts of such U.S. citizens to the IRS under FATCA and the intergovernmental agreements (“IGAs”).

See, U.S. Citizens Overseas who Wish to Renounce without a Social Security Number will Necessarily be a “Covered Expatriate”

The intricacies of this problem are highlighted in a technical paper I recently drafted and presented to the U.S. Treasury Department and the Joint Committee of Taxation, among other federal government groups. Some key excerpts of that paper titled URGENT NEED FOR U.S. CITIZENS RESIDING OUTSIDE THE U.S. TO BE ABLE TO OBTAIN A TAXPAYER IDENTIFICATION NUMBER (“TIN”) OTHER THAN A SOCIAL SECURITY NUMBER are set out below in this section:

The U.S. tax law imposing taxation on the worldwide income of USCs[1] residing overseas has created a dilemma that prejudices these USCs without a SSN. This strict SSN/TIN regulatory rule undermines the basic tax administration system and discourages tax compliance for those USCs who never obtained a SSN. This dilemma affects numerous USCs throughout the world, which is now compounded by the certification and reporting requirements of USCs and third parties, such as FFIs and NFFEs[ under the Foreign Account Tax Compliance Act (“FATCA”).

In short, USCs without a SSN, necessarily cannot be in compliance with U.S. federal tax law. As I point out in my paper, such –

“A law that cannot be complied with is surely a bad law, the same as a “ . . .law that cannot be enforced is a bad law.”[a]

[a] See, The Case Against Taxing Citizens, Reuven S. Avi-Yonah (March 31, 2010), University of Michigan School of Law, Law & Economics Working Papers.

The paper referenced above explains how difficult it is for USCs residing overseas to ever obtain a SSN. Specifically, it explains how difficult it is to have an in-person interview at only 18 different locations around the world with a U.S. Department of State employee. See, 12 Year Old (and Older) U.S. Citizens Residing Outside the U.S. Must Have An “In-Person” Interview in a U.S. Embassy or Consulate for SSN Application in 1 of Just 17 Posts Worldwide

As a USC residing somewhere around the world, you might decide to simply spend the time, money and resources to travel internationally to arrive in the U.S. to apply for a SSN directly with the Social Security Administration within the U.S. Unfortunately, any USC is now legally prohibited from traveling in or out of the U.S. without a U.S. passport. There are few exceptions to this general rule, none of which contemplate U.S. federal tax compliance. See, the relevant excerpts from the white paper:

C. Travel to the U.S. is Also Not An Option for a USC without a SSN, Due to 22 CFR § 53.1 Requiring a U.S. Passport

A possible solution to this TIN/SSN dilemma may appear to be a trip to the U.S. by the USC to apply for a SSN in the U.S. Unfortunately, this simply creates another dilemma, since the USC must have a U.S. passport to travel to the U.S. The immigration law regulations 22 CFR § 53.1 require that a U.S. citizen have a U.S. passport to enter or depart the United States. The relevant part of the regulations is § 53.1(a) which provides as follows:

Passport requirement; definitions.

(a) It is unlawful for a citizen of the United States, unless excepted under 22 CFR 53.2,[2] to enter or depart, or attempt to enter or depart, the United States, without a valid U.S. passport.

These regulations were first published in 2006 and unfortunately, simply create another dilemma for the USC residing overseas without a SSN. This additional dilemma is that an application[3] for a U.S. passport requires the individual have a SSN; a vicious circle back to the inability to obtain a SSN.

At the end of the day, the restrictions imposed on USCs make it legally impossible for a USC without a passport to travel to the U.S. (even if they wish they could) to obtain a SSN.

[1] See, IRC § 61 and Treas. Reg. §§ 1.1?1(b) and 1.1?1(a)(1)..

[2] The exceptions set forth in this regulation would not generally be applicable in the case of USCs residing overseas without a SSN.

[3] Application for a U.S. Passport – http://www.state.gov/documents/organization/212239.pdf.

Inflation Adjusted Exclusion Amounts Since Inception of 2008 “Mark to Market” Expatriation Tax Law: Example

The current “expatriation” “exit tax” forces a “covered expatriate” to pay U.S. income taxation on their unrealized gains (the “mark to market” concept) as if they sold their worldwide assets.

An “unrealized gain” is the amount of gain “built into” the property or other investment of the individual, which has yet to be sold or otherwise disposed of by the him or her. For instance, the  diagram below reflects various assets held by a “Covered Expatriate” which includes Mexican real estate with a tax basis of US$200,000 but a current fair market value of US$1.1M. This means the unrealized gain in that Mexican real property is US$900,000 (US$1.1M – US$200K).

diagram below reflects various assets held by a “Covered Expatriate” which includes Mexican real estate with a tax basis of US$200,000 but a current fair market value of US$1.1M. This means the unrealized gain in that Mexican real property is US$900,000 (US$1.1M – US$200K).

Who is a “covered expatriate” is a very important legal analysis that needs to be considered for each U.S. citizen who wishes to renounce or “long-term resident.” See, The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C) (9 March 2014).

Importantly, the law provides for an exclusion from taxation on the former (a) U.S. citizen’s (“USC”) or (b) long-term resident’s unrealized gains. (See, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter? – 19 Aug. 2014). In other words, no U.S. income tax is due and payable by a “covered expatriate” if they did not have assets with unrealize d gains greater than a certain threshold amount.

d gains greater than a certain threshold amount.

That threshold amount has been changing annually, since the initial US$600,000 that was originally adopted into the law in 2008. It is changing due to annual inflation adjustments.

The current 2015 exclusion amount adjusted for inflation is US$690,000. See, The “Phantom” Gain Exclusion from the “Mark to Market” Tax – Increases to US$690,000 for the Year 2015 (15 November 2014).

Hence, in this case, if the only asset owned by the “covered expatriate” (assuming she became one in 2015) was the real estate in the above example with unrealized gain of US$900,000, only US$210,000 would be subject to the “mark to market” tax on expatriation (i.e., the exit tax). This is because $690,000 of the total US$900,000 unrealized gain will be excluded from taxation (US$900K – US$690K).

The Mark to Market tax regime imposes taxation on this amount, even though the real estate is never sold. This means, the “covered expatriate” must come “out of pocket” to find the cash and means necessary to pay the tax imposed under the law.

There is no economic benefit obtained from this annual inflation adjustment if a U.S. citizen or long-term resident waits to become at a later time a covered expatriate; unless they consume, deplete or lose their assets in the interim. But at least, there is an inflation adjustment, so the taxpayer is not subject to an increasing amount of gain subject to tax as time progresses and inflation eats away at the true economic value and economic growth of the individual’s assets.

U.S. Citizens Overseas who Wish to Renounce without a Social Security Number will Necessarily be a “Covered Expatriate”

U.S. Citizens Overseas who Wish to Renounce without a Social Security Number (“SSN”) will Necessarily be a “Covered Expatriate”

- The Dilemma of SSNs, TINs and USCs Residing Overseas

The prior post discussed some of the complications of United States Citizens (“USCs”) who reside outside the U.S. and do not have a social security number (“SSN”) . This dilemma exists, even though USCs are not generally required to file for or  obtain a SSN (e.g., at birth – See, SSA Publication – “Social Security Numbers For Children” page 2, It is not obligatory to file for a SSN at birth. “Must my child have a Social Security number? No. Getting a Social Security number for your newborn is voluntary. But, it is a good idea to get a number when your child is born. . . . ).

obtain a SSN (e.g., at birth – See, SSA Publication – “Social Security Numbers For Children” page 2, It is not obligatory to file for a SSN at birth. “Must my child have a Social Security number? No. Getting a Social Security number for your newborn is voluntary. But, it is a good idea to get a number when your child is born. . . . ).

Indeed, it is the U.S. federal tax law that requires the USC must have a SSN for their taxpayer identification number (“TIN”). I will reference various excerpts from a recent paper I drafted and presented titled URGENT NEED FOR U.S. CITIZENS RESIDING OUTSIDE THE U.S. TO BE ABLE TO OBTAIN A TAXPAYER IDENTIFICATION NUMBER (“TIN”) OTHER THAN A SOCIAL SECURITY NUMBER , including the following:

. . . the IRS’ increased focus on international tax compliance has made clear that USCs residing overseas have U.S. tax return filing obligations, even if they have no assets, no income, or no real personal connections in or with the U.S. See IRS notice from 2011 which addresses numerous aspects of tax compliance for USCs overseas, including various penalties under the law[1]:

. . . U.S. Citizens or Dual Citizens Residing Outside the U.S. . . .

The IRS is aware that some taxpayers who are dual citizens of the United States and a foreign country may have failed to timely file United States federal income tax returns or Reports of Foreign Bank and Financial Accounts (FBARs), despite being required to do so. . . . 2. Penalties imposed for failure to file income tax returns or to pay tax . . . 3. Possible additional penalties that may apply in particular cases . . . 6. Possible penalties for failure to file FBAR . . . 7. New reporting requirement for foreign financial assets . . . [emphases added]

USCs residing overseas are subject to the range of tax penalties that apply to all individual taxpayers (e.g., negligence penalties, failure to file penalties, late payment or failure to pay penalties, etc.).[2] Additionally, USCs residing overseas are subject to other, typically much harsher penalties for not timely filing U.S. federal information returns regarding assets located outside the U.S.[3]; alluded to above in the IRS 2011 notice.[4]

These civil penalties typically are a minimum of US$10,000 per statutory violation. USCs who live outside the U.S. necessarily have assets, such as financial accounts in their country of residence. These Title 26 information reporting requirements[5] are referred to herein as “International Information Returns.”

The IRS will not process federal tax returns and International Information Returns without a valid TIN.[6] Plus, the law does not provide for an exception for USCs overseas who do not file returns, if they do not have a SSN. Late filed, or incomplete International Information Returns and tax returns (e.g., lacking a SSN) will typically subject USCs to these penalties even in those cases when the taxpayer has no federal income tax liability.[7]

[1] See, IRS FS-2011-13, December 2011, updated February, 2014.

[2] See, IRS FS-2011-13 and as a sample of some of the many statutory penalties that could typically apply, IRC §§ 6048, 6652(f), 6677, 6654, 6655, 6698, 6699, 6166, 6653, 6675, 6715, 6715A, 6717, 6718, 6719, 6720A, 6725, et. seq.

[3] See, IRC §§ 6038, 6038B, 6038D, 6039F, 6039G, 6046, 6046A, 6048, et. seq.

[4] See, IRS FS-2011-13, December 2011, updated February, 2014.

[5] See, IRC §§ 6038, 6038B, 6038D, 6039F, 6039G, 6046, 6046A, 6048, et. seq.

[6] See, IRS website, “General ITIN Information” – http://www.irs.gov/Individuals/General-ITIN-Information – “IRS no longer accepts, and will not process, forms showing “SSA”, 205c”, “applied for”, “NRA”,& blanks, etc.”

[7] See, IRC §§ 911 (foreign earned income exclusion) and 901 (foreign tax credit), et. seq. A USC residing overseas may have no actual federal income tax liability (for various reasons), typically due to the foreign earned income exclusion and/or foreign tax credit calculation.

The above explains fairly clearly the dilemma facing USCs residing overseas.

The complexity of getting a SSN and the requirements are covered in more detail in the paper. Some key points are:

I. The Social Security Administration Rules Make it Nearly Impossible for Many USCs Overseas to Reasonably Obtain a SSN

The policy and procedures of the SSA regarding issuing SSNs have changed significantly over the years.[1] The Social Security Administration (SSA) provides a detailed chronology of the major changes in policy and procedures  regarding filing for and obtaining a SSN.[2] One of the most significant revisions in the last decade came from The Intelligence Reform and Terrorism Prevention Act of 2004 (P.L. 108-458), which imposes various standards for the verification of documents or records submitted by an individual.

regarding filing for and obtaining a SSN.[2] One of the most significant revisions in the last decade came from The Intelligence Reform and Terrorism Prevention Act of 2004 (P.L. 108-458), which imposes various standards for the verification of documents or records submitted by an individual.

A. Only a Few Countries Around the World have Personnel at U.S. Embassies or Consulate Offices that Can Process SSN Applications – SSA Form SS-5-FS

Applying for SSNs overseas is severely restricted compared to an application in the U.S.

According to the U.S. Department of State, Foreign Affairs Manual (“FAM”), only certain “Claims-Taking Posts” in specific countries “may” include “processing applications for Social Security Numbers.” [3]

These 17 countries (and a city in the case of Jerusalem) with Claims-Taking Posts include:

“Austria, Argentina, Costa Rica, Dominican Republic, France, Germany, Greece, Ireland, Italy, Japan, Jerusalem, Mexico, Norway, Philippines, Poland, Portugal, Spain, and the United Kingdom.”

Noticeably absent are many Western European countries, virtually all of Latin America, virtually all of Asia, virtually all of Eastern Europe, all of the Middle East (except Jerusalem), all of the African continent, all of the Australian continent and surrounding island countries and Russia, among many other significant countries, including OECD member countries.[4]

Nothing in the FAM requires any of these “Claims-Taking Posts” to actually process applications for a SSN. Plus, there are of course hundreds of other countries throughout the world, not listed above, which do not have such a U.S. Department of State Post. For these reasons, USCs in countries such as China must travel to a U.S. Department of State Post (e.g., the Philippines) which is able to process applications for SSNs.

[1] See, SSA website, The Story of the Social Security Number, by Carolyn Puckett, Social Security Bulletin, Vol. 69 NO. 2, 2009 (http://ssa.gov/policy/docs/ssb/v69n2/v69n2p55.html.

[2] See, SSA website, Significant Milestones in Social Security Number Policy. A detailed chronology of the major changes in policy and procedures. http://www.ssa.gov/history/ssn/ssnchron.html.

[3] See 7 FAM 530, page 2 of 64.

[4] In contrast to these 17 countries (and one city – Jerusalem) where a USC residing overseas must travel to apply for a SSN, the Treasury Department has announced it has around 100 countries that have signed, or “have reached agreements in substance” a FATCA IGA. USCs throughout the world are required by the Foreign Account Tax Compliance Act (“FACTA”) to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . .”

- The Necessary “Covered Expatriate Status” of a USC without a SSN

The core point of this post, with the above SSN background, is to explain how a USC without a SSN will necessarily be a “covered expatriate” since they will not be able to truthfully certify they have complied with the federal tax laws (title 26). See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute

As other posts have explained, “covered expatriate” status matters:

See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”! (20 May 2014) and The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” (10 April 2014) and “Covered Expatriate” Status is a “Scarlet Letter” (10 Nov 2014).

If a USC has no SSN, they by definition will never be able to comply with the Certification Requirement of Section 877(a)(2)(C) since they will not be able to comply with IRC § 6109(a) and Treas. Reg. § 301.6109-1. As the SSN/TIN paper explains:

All United States citizens (“USCs”) must have a social security number (“SSN”) under current law as their TIN to file a federal income tax return.[1]

[1] See, IRC § 6109(a) and Treas. Reg. § 301.6109-1.

The IRS will not process federal tax returns and “International Information Returns”, as defined below, without a valid TIN[1]; which currently must be a SSN for a USC.

[1] See, IRS website, – http://www.irs.gov/Individuals/General-ITIN-Information – “IRS no longer accepts, and will not process, forms showing “SSA”, 205c”, “applied for”, “NRA”,& blanks, etc.”

Is “It’s Almost Impossible for Me to Get a U.S. Taxpayer Identification Number”; a Defense to Not Filing U.S. Tax Returns?

The U.S. federal government has made the basic task of getting taxpayer identification numbers (“TINs”) very difficult for many individuals. Without a TIN, an individual cannot file tax returns or information reporting returns.

- U.S. Citizens and SSNs – No Exceptions

U.S. citizens (USCs) residing overseas without a social security number (“SSN”) must use a SSN for their TIN. I presented a recent report to various government officials, including the international tax counsel at the U.S. Treasury Department and the Joint Committee of Taxation, among other groups. Some key excerpts of that paper titled URGENT NEED FOR U.S. CITIZENS RESIDING OUTSIDE THE U.S. TO BE ABLE TO OBTAIN A TAXPAYER IDENTIFICATION NUMBER (“TIN”) OTHER THAN A SOCIAL SECURITY NUMBER are set out below in this section:

The U.S. tax law imposing taxation on the worldwide income of USCs[1] residing overseas has created a dilemma that prejudices these USCs without a SSN. This strict SSN/TIN regulatory rule undermines the basic tax administration system and discourages tax compliance for those USCs who never obtained a SSN. This dilemma affects numerous USCs throughout the world, which is now compounded by the certification and reporting requirements of USCs and third parties, such as FFIs and NFFEs[2] under the Foreign Account Tax Compliance Act (“FATCA”).

This dilemma is a creature of the Title 26 regulatory law going back to 1974[3] and how the Social Security Administration (“SSA”) imposes strict requirements on the issuance of SSNs to residents overseas.[4] One essential step is that the USC overseas must have an in-person interview, with a designated individual (who are typically U.S. Department of State employees and some designated military personnel). They are located in only a few cities around the world.[5] Some USCs need to travel thousands of miles to merely be able to apply for and obtain a SSN.

[1] See, IRC § 61 and Treas. Reg. §§ 1.1?1(b) and 1.1?1(a)(1).

[2] See, IRC §§ 1471 et. seq. and the regulations thereunder which define “foreign financial institutions” (“FFIs”) and “non-financial foreign entity” (“NFFEs”).

[3] See, Treas. Reg. § 301.6109-1(a)(1)(ii)(A).

[4] See, 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

[5] Id, page 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

Further posts will discuss a number of the adverse consequences imposed on USCs who do not have a SSN and the severe penalty regime that exists under current law for those unwitting individuals.

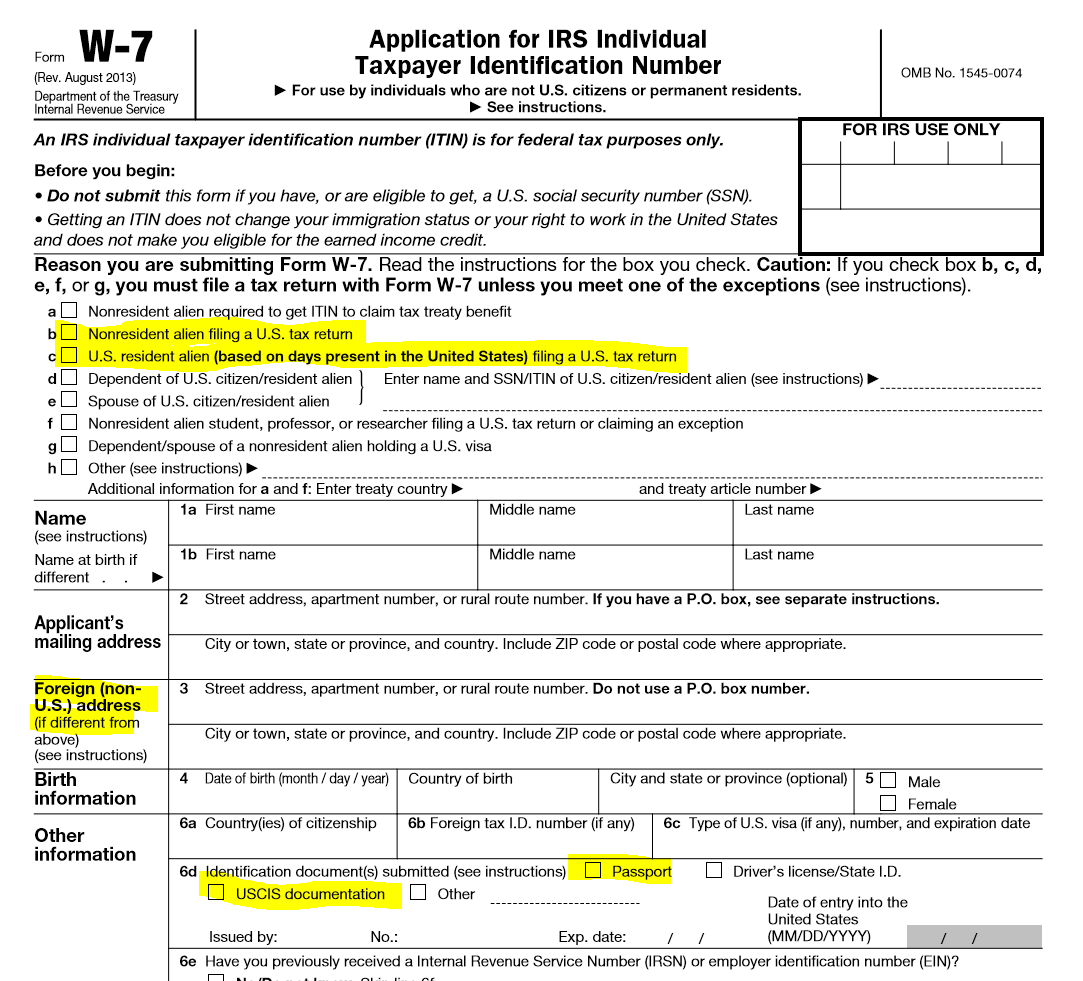

- Non-U.S. Citizens and ITINs –

Many individuals who are not USCs nevertheless need to file a tax return and must obtain what is called an individual taxpayer identification number (“ITIN”). See IRS report Obtaining an ITIN from Abroad. An ITIN is applied for by filing an IRS  Form W-7, and providing various original documents, principally a passport, directly to the IRS. The process is complex and time consuming. Indeed, the Taxpayer Advocate report included a key summary explanation of the problems associated with obtaining ITINs as follows:

Form W-7, and providing various original documents, principally a passport, directly to the IRS. The process is complex and time consuming. Indeed, the Taxpayer Advocate report included a key summary explanation of the problems associated with obtaining ITINs as follows:

- IRS ITIN Policy Changes Make Return Filing Difficult and Frustrating

Recent changes to the IRS’s Individual Taxpayer Identification Number (ITIN) application program are burdening taxpayers and may harm voluntary compliance.

ITINs play an important role in tax administration, as any individual who has a federal tax filing obligation but is not eligible for a Social Security number must apply to the IRS for an ITIN and then use the ITIN on any return, statement, or other document which requires a taxpayer identifying number

Under the new procedures, most applicants must now submit original documentation by mail or travel to Taxpayer Assistance Centers (TACs) to have documents certified, making the application process more difficult

Since December 17, 2003, the IRS has required ITIN applicants with a filing requirement to attach a valid federal tax return with their application (unless they qualify for an exception).

On June 22, 2012, the IRS implemented temporary changes that required all ITIN applicants to submit original documents supporting the information on their applications. Under these procedures, applicants could no longer submit notarized copies and had to send in original documentation, even if a certified acceptance agent (CAA) reviewed and certified the documentation.

On November 29, 2012, the IRS announced revised procedures for the 2013 filing season that require applicants to submit original documentation or copies certified by the issuing agency.

Although the IRS allows CAAs to submit copies of documentation for primary and secondary taxpayers after reviewing original documentation or certified copies, CAAs must still send in original documentation for all dependent applicants.

A limited number of TACs can certify documents for primary, secondary, and dependent taxpayers.

The Revised Procedures Create an Impediment for Taxpayers Required to File Returns.

The recent changes to the ITIN program have made it difficult for taxpayers to file returns.

More on ITINs to follow in later posts.

The complexities of obtaining a U.S. TIN begs the question: “Is it a legal defense for a taxpayer to NOT file U.S. tax returns, international information returns, if it is particularly difficult (or nearly impossible in some cases) for that individual to even obtain a TIN?”

Will such a taxpayer have a “reasonable cause” defense to avoid penalties in the case of an audit? These are questions unanswered by any case law to date.

USCs throughout the world are required by FATCA to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . . “

As FATCA requires overseas individuals, including USCs to certify under penalty of perjury their U.S. taxpayer identification number (and if they have none), they necessarily will not be able to comply with this basic reporting requirement.

Will these individuals have a defense under the law for not complying under these circumstances?

Will the government provide relief for these individuals?

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

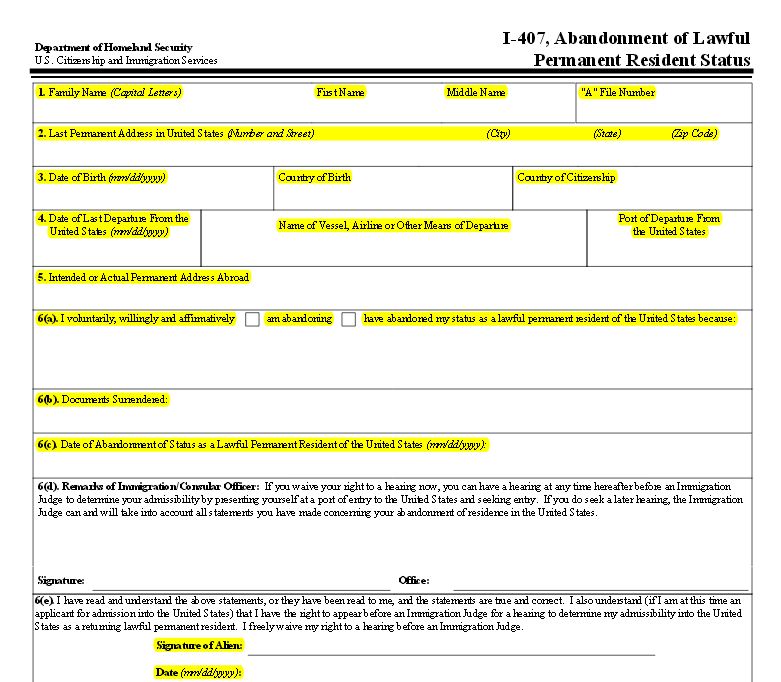

A prior post discussed the newly published USCIS immigration form I-407 for LPRs who must now use it when formally abandoning LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms  are set forth here. The new form requires the address overseas of the individual.

are set forth here. The new form requires the address overseas of the individual.

As readers here know, the names of former U.S. citizens are published quarterly by the U.S. federal government for the world to see. See a prior post, The 2014 Third Quarter Renunciations Is probably the New Norm –

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

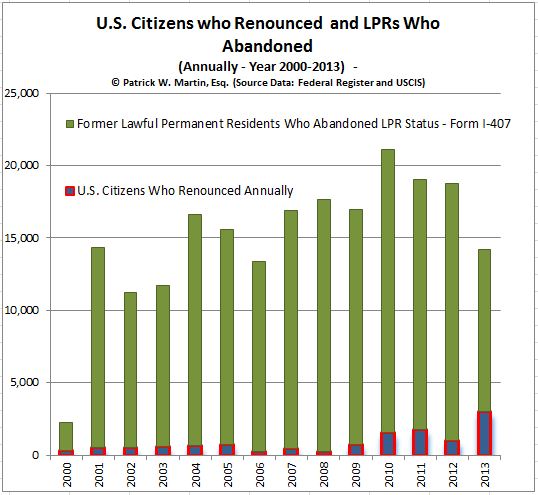

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

- “mark to market” taxation on their worldwide assets,

- 40% inheritance tax to U.S. beneficiaries,

- 40% tax on gifts to U.S. beneficiaries,

- etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”

The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

Categories of records in this system include:

A. The hardcopy paper A-File, which contains the official record material about each individual for whom DHS has created a record under the INA such as: naturalization certificates; various documents and attachments (e.g., birth and marriage certificates); applications and petitions for benefits under the immigration and nationality laws; reports of arrests and investigations; statements; other reports; records of proceedings before or filings made with the U.S. immigration courts and any administrative or federal district court or court of appeal; correspondence; and memoranda. Specific data elements may include:

- Alien Registration Number(s) (A-Numbers);

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

? Document type,

? issuing organization,

? document number, and

? expiration date;

- Military membership;

- Arrival/Departure information (record number, expiration date, class of admission, etc.);

- Federal Bureau of Investigation (FBI) Identification Number;

- Fingerprint Identification Number;

- Immigration enforcement history, including arrests and charges, immigration proceedings and appeals, and dispositions including removals or voluntary departures;

- Immigration status;

- Family history;

- Travel history;

- Education history;

- Employment history;

- Criminal history;

- Professional accreditation information;

- Medical information relevant to an individual’s application for benefits under the INA before DHS or the immigration court, an individual’s removability from and/or admissibility to the United States, or an individual’s competency before the immigration court;

- Specific benefit eligibility information as required by the benefit being sought; and

- Video or transcript of immigration interview

Subsequent posts will discuss how and when the law allows the IRS to access these records.

More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The U.S. Customs and Immigration Service (USCIS) just announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement, which announcment provides in part as follows:

New Version of Form I-407 Now Available

USCIS has published a new edition of USCIS Form I-407, Record of Abandonment of Lawful Permanent Status (OMB No. 1615-0130). You can download the form on our website.

You may begin using the revised Form I-407, Record of Abandonment of Lawful Permanent Resident Status today. The current edition is dated 02/26/2015, and we will not accept previous form editions

The new form has additional information compared to the prior form. Specifically, the Alien Registration Number and USCIS ELIS Account Number is required to be included.

Now, the individual is required to state the reasons for abandoning lawful permanent residency status.

Responses to  each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

One of the important enforcement and practical questions raised, is: Will the IRS be able to better track former “long-term residents” (certain former lawful permanent residents) for purposes of the “expatriation tax” under the new reporting form and system?

As has been explained, if an individual fails to certify under the tax law, they will necessarily be a “covered expatriate”; even if they do not meet the asset or income tax liability thresholds. See a prior post, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute.

The Problem with PFICs! “Avoid PFICs Like the Plague”

There are typically numerous tax issues that USCs and LPRs need to consider prior to renouncing their citizenship; or abandoning th eir lawful permanent residency status.

eir lawful permanent residency status.

One of the most confusing comes from the complex rules of a so-called “PFIC” – the acronym for a “passive foreign investment company.” A prior post in March 2014 discussed the basics of these U.S. tax creatures – “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Most USCs and LPRs with basic mutual fund investments in their country of residence have PFICs and probably don’t even know it.

The IRS and Treasury have recently spent much attention and resources to the regulation of PFICs. In January of 2014, temporary regulations were issued regarding PFICs. See, Regulations §1.1291–0T, et. seq.

One of the many new requirements of these regulations are annual information filing requirements. This means that a U.S. taxpayer (e.g., U.S. citizen or LPR) residing outside the U.S., must file an annual report on IRS Form 8621.

- When Might You have a PFIC?

Taxpayers who have simple passive investments in mutual funds based outside the U.S.. e.g., in their country of residence, almost always have PFICs. There is no percentage ownership threshold in the foreign entity that triggers PFIC tax consequences. An ownership interest of 0.000001% triggers the consequences if either the “income test” or “asset test” are satisfied. Other type of investment funds in the form of a legal entity also typically qualify as a PFIC.

Specifically, a PFIC is a foreign corporation in which a U.S. person has some ownership in (without any percentage threshold requirement) if (i) at least 75% of its gross income is passive income (the “income test”), or (ii) at least 50% of its assets produce passive income (the “asset test”). See IRC § 1297(a).

Also, many retirement funds in various countries (including both private and many government run retirement plans) typically fall into the category of a PFIC. For instance, the Singapore retirement fund system, Central Provident Fund (“CPF”), is actually created by the government, but Singapore taxpayers who are obligated to contribute to the retirement fund will select various mutual funds to invest in through the CPF. Hence, these mutual fund investments are PFICs. See also the technical paper regarding Mexican retirement funds that argues, WHY MEXICAN RETIREMENT FUNDS SHOULD NOT BE SUBJECT TO THE NEW REPORTING REQUIREMENTS UNDER IRC SECTION 1298(f).

- Ugly Tax Consequences of a PFIC

PFICs are taxed to the U.S. taxpayer in a very complicated manner compared to taxation of U.S. based mutual funds or other U.S. based investments. In short, the income earned from PFICs, under the default regime, are taxed at the ordinary income rates, and for past years are typically taxed at the highest marginal ordinary income tax rate is 39.6% (even if the income would otherwise qualify for qualified dividend or long-term capital gains rates – which are taxed at no more than 20%).

There are three alternative regimes for how a U.S. investor is taxed in a PFIC: (i) the “excess distribution” regime (which is the default regime); (ii) the qualified electing fund (“QEF”) regime and (iii) the market-to-market (“MTM”) regime. Each of these regimes will be discussed in later posts.

One key point to know is that most foreign investment funds do not keep records and account for income and expenses in a manner that even allows a U.S. taxpayer to report accurately under the QEF or MTM regime, even if such treatment provides a lower overall U.S. tax.

More on how PFICs are taxed in a later post.

- Even Uglier Tax Reporting – Compliance Consequences of PFICs Driven by FATCA

Finally, the 2010 FATCA legislation has led to the new regulations that now require annual reporting of PFICs. This is done on IRS Form 8621. It is a laborious form and requires extensive and detailed information.

The consequences of not reporting can lead to disastrous tax results. See a prior post from March 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

- Why You Don’t Want to Die with a PFIC or Gift a PFIC Away (even to Your Favorite Charity or Spouse).

Lastly, a later post will explain in more detail why a USC or LPR generally wants to avoid PFICs if at all possible. Many countries require their residents to contribute on a mandatory basis to retirement funds that invest in mutual funds, which may not allow a USC to avoid PFICs. One of the principle reasons to avoid PFICs is the income tax that arises and is owed by the U.S. person, even if he or she tries to give the PFIC away. A gift of a PFIC will typically cause an income tax to the donor in addition to the estate/gift tax rules. This is true for gifts to charity and even to your own spouse.

- Why You Should Avoid PFICs Like the Plague

At the end of the day, the above complications, mean that most USCs and LPRs residing overseas should “avoid PFICs like the plague”.

In the context of USCs who wish to renounce their U.S. citizenship, they will not be able to avoid “covered expatriate” status if they have not complied with these PFIC rules, as they will not be able to “certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The ugly consequences of PFICs can be summarized as follows:

- Higher income tax rate than U.S. based investments on the earnings of the investment, at least under the default method;

- Practically impossible to report the earnings on a more favorable MTM or QEF method;

- Extensive information reporting requirements annually;

- Open ended statute of limitations in favor of the IRS to audit all items on the tax return, for failure to properly file IRS Form 8621;

- Paying a U.S. income tax, even if you gift away the PFIC to charity or to your spouse;

- Trying to even explain effectively the consequences of a PFIC to your tax return preparer; and

- Being subject to the “forever taint” of being a “covered expatriate” for failure to comply with the PFIC rules. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”