iga

Foreign Government Receives a “FATCA Christmas Gift” from IRS: 1 Gigabyte of U.S. Financial Information

The last post discussed how the director of the Mexican tax administration was critical of the U.S. federal government for not providing FATCA information on U.S. financial accounts. See, Foreign Government Criticizes U.S. Government for  NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts, dated December 14, 2015.

The automatic exchange of bank and financial information is driven by the U.S. Treasury driven Intergovernmental Agreement (IGA).

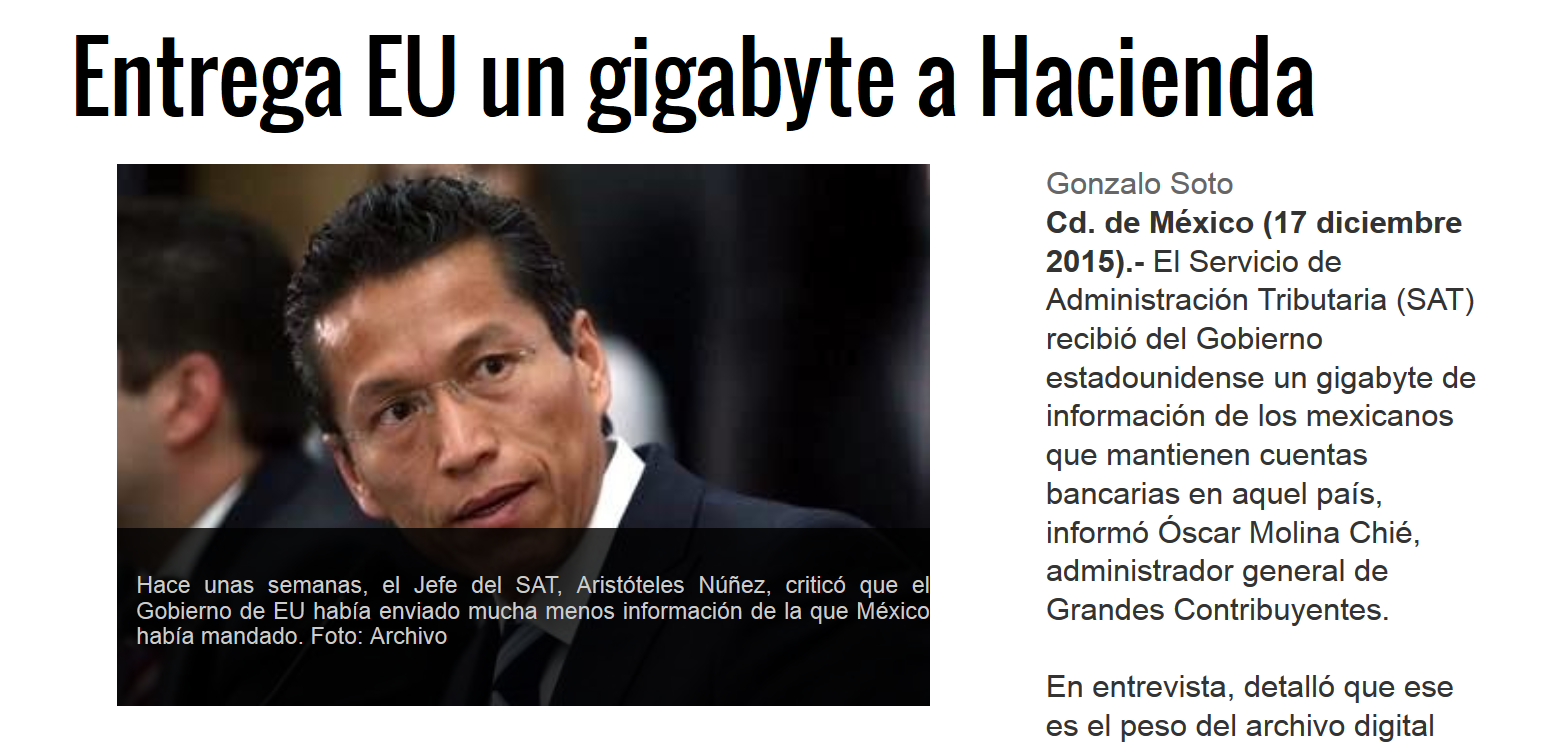

As a follow-up, the Mexican newspaper Reforma reported on the 17th of December that the U.S. just provided Mexico’s treasury with a gigabyte of Mexican taxpayer information regarding U.S. financial and bank accounts. See, Entrega EU un gigabyte a Hacienda, dated Dec 17, 2015.

This news comes on the heals of the earlier criticism by the Commissioner of the Mexican IRS (SAT – Servicio de  Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez. The Reforma article quotes Óscar Molina Chié (who is in charge of the large taxpayers division at SAT) generously regarding how and what information was provided by the U.S. federal government.

Finally, the article emphasized that Mexico has sent the IRS information regarding Mexican bank accounts of U.S. citizens.

The question is how much Mexican bank and financial information has actually been provided by SAT of the hundreds of thousands (if not more than 1 million) dual national taxpayers, who are citizens of both Mexico and the U.S.? See, Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand, dated January 28, 2015.

Foreign Government Criticizes U.S. Government for NOT Providing FATCA IGA Information on Their Taxpayers with U.S. Accounts

This news is ironic. The U.S. government has chastised various banks and governments around the world since 2009 for not providing financial information on U.S citizens (USCs) and other U.S. taxpayers regarding their foreign bank and financial accounts. See, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior, posted Sept 8, 2014.

Now, it is foreign governments’ turn, to criticize the U.S. Treasury and IRS for not keeping up with its promises to provide U.S. financial and bank information on taxpayers of their countries pursuant to all of the FATCA Intergovernmental Government Agreements (IGAs) that were pushed so hard by U.S. Treasury. See, FATCA IGA with Hong Kong Signed: U.S. Citizens and Lawful Permanent Residents Residing in or Around Hong Kong Need to Know, posted on Nov. 17, 2014.

The Commissioner of the Mexican IRS (SAT – Servicio de Administración Tributaria (SAT)), Mr. Aristóteles Núñez Sánchez just announced that the U.S. government is not holding up its side of the bargain under the U.S.-Mexico IGA. See, the Dec. 12, 2015 article en the national Mexican newspaper, El Universal, EU incumple entrega de informacion: SAT: Mexico ha hecho su parte, asegura Aristóteles Núñez

The article, which is in Spanish, explains that Mexico has complied with its obligations under the IGA by providing detailed information about U.S. taxpayers with accounts in Mexican financial institutions to the U.S. government. However, the U.S. government has not complied with its side of the bargain. The news report says no specific details were provided by Mr. Núñez about what type of information was provided.

FATCA Driven (Even More . . . ) – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information (Part III)

Information and more information is the mantra of revised IRS Forms as a result of FATCA. See, FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

U.S. citizens residing outside the U.S. along with lawful permanent residents (“LPRs”) are not the only persons who need to understand the IRS forms referenced above. Indeed, all entities and institutions, whether they are small privately held companies or large and traditional financial institutions are required to complete and have signed a range of IRS forms.

persons who need to understand the IRS forms referenced above. Indeed, all entities and institutions, whether they are small privately held companies or large and traditional financial institutions are required to complete and have signed a range of IRS forms.

The forms can be either the actual IRS form, or a satisfactory substitute form. Many individuals are of the erroneous view that if they are not financial institutions, they do not need to concern themselves with these classifications.

Unfortunately, that is not the case. Also, these classification rules apply to the surprise of many, if there are (or are not) U.S. persons involved.

In addition to a basic understanding of U.S. laws, it is also crucial that the parties see if their country has entered into an IGA. For instance, if we examine the tiny little country of Liechtenstein which has a relatively large financial sector, it is necessary to first classify the type of entity.

For instance, if it is a Liechtenstein Stiftung, it will probably (but not necessary) be a trust and not a corporation. See the IRS Memorandum from 2009 that provides that a Liechtenstein Stiftung will be classified as a trust, if its primary purpose is to protect or conserve the property transferred to the Stiftung for the Stiftung’s beneficiaries and is usually not established primarily for actively carrying on business activities.[1]

[1] See Memorandum Number: AM2009-012, dated October 16, 2009, issued by the Office of Chief Counsel, Internal Revenue Service.

Next, in this example, with a Liechtenstein Stiftung, the country of Liechtenstein has entered into an Intergovernmental Agreement (“IGA”).

Hence, the terms of the IGA are most important. Under the IGA, as is the case generally for FATCA, the entity has to be either an Foreign Financial Institution (“FFI” or “FI”) or a Non-Financial Foreign Entity (“NFFE”).

1) Definition of Financial Institution (“FI”)

A financial institution is any entity that:

- Accepts deposits in the ordinary course of a banking or similar business (“Depository Institution”);[1]

- Holds, as a substantial portion of its business financial assets for the benefit of one or more other persons (“Custodial Institution”);[2]

- Is an investment entity; or

- Is an specified insurance company or holding company that is a member of an expanded group;[3]

[1] See Article 1(i), IGA.

[2] See Article 1(h), IGA.

[3] See Article 1(k), IGA.

Generally a private Liechtenstein Stiftung would not satisfy any of these requirements (although it could conceivably be the case that one could be an “investment entity”). Hence, it would generally be an NFFE and not an FI.

NFFEs can be passive or active. The kind of compliance obligations varies depending on the type of NFFE (passive or active).

- Passive NFFEs

A passive NFFE is an NFFE which is not an active NFFE or a withholding foreign partnership or withholding foreign trust.[1]

There are several criteria under which a NFFE can be classified as an active NFFE. The following explain the most relevant criteria.

- Active NFFEs

Among the criteria that the IGA establishes, under which a NFFE can be considered as an Active NFFE, are the following:

1) If less than 50% of the NFFE’s gross income is passive income and less than 50% of the assets held by the NFFE are assets that produce or are held for the production of passive income during the preceding calendar year. A

2) Substantially all of the activities of the NFFE consist of holding (in whole or in part) the outstanding stock of, or providing financing and businesses other than the business of a Financial Institution.

Sometimes trusts or Stiftungs will also participate in or hold interests in companies, some of which may engage in active trades or businesses or simply hold passive investments. On the contrary, the companies/subsidiaries only hold other assets from which they derived passive income (e.g., dividends, interests, rents, royalties, etc.).[2]

This will determine if a Stiftung will be classified as a Passive NFFE or not under FATCA regulations and the IGA.

[1] It also can make a difference if the trust (or Stiftung in this example) is a so-called “withholding” foreign trust; which generally requires an agreement with the IRS.

[2] Treas. Reg. § 1.1472-1.

Not surprisingly, the above analysis is complex, because the rules are complex. Accordingly, it has been the author’s experience, that many institutions around the world which request one or more of the above IRS Forms have great difficulty in even implementing these rules. Most of their employees seem to have little understanding of what is a very complex area of law, even when their resident country has issued extensive regulations or guidance about how the terms of the IGA are to be implemented.