We ended the last post (I of VI) on this topic by referencing a crucial article I authored and published more than a decade ago in the International Tax Journal– titled Oops.. .Did I Expatriate and Never Know It – (2014)

- Key Background on LPRs and “Oops . . . Did I Expatriate”?

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below.

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below.

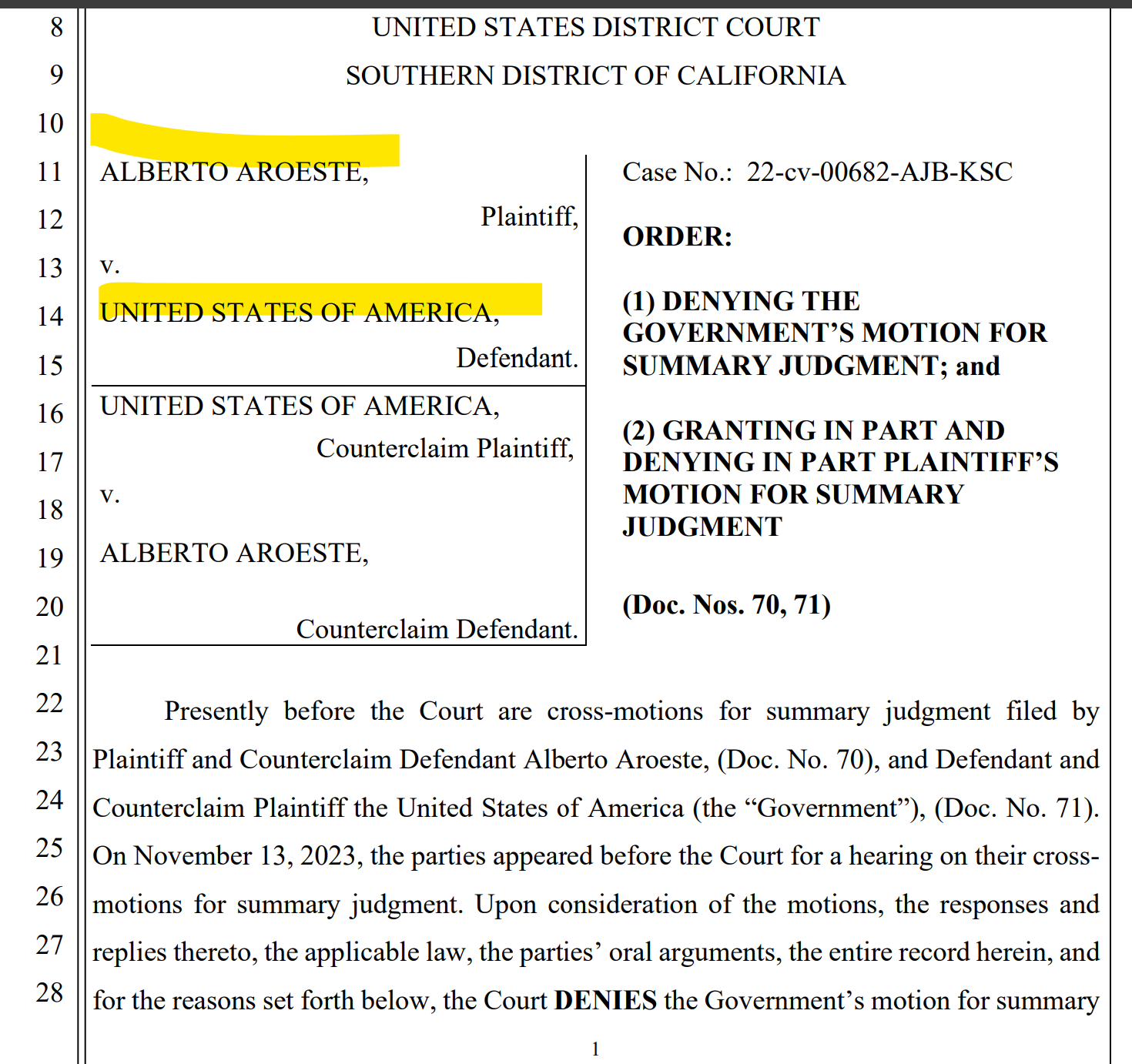

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

- Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Please read an earlier post from yours truly (About the Author: Patrick W. Martin), more than a decade ago –“Covered Expatriate” Status is a “Scarlet Letter”— which discusses the severe and often misunderstood consequences of covered expatriate status.

In addition, see another earlier post I authored explaining why covered expatriate status matters even for individuals with modest or limited assets: Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

- Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroeste decision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

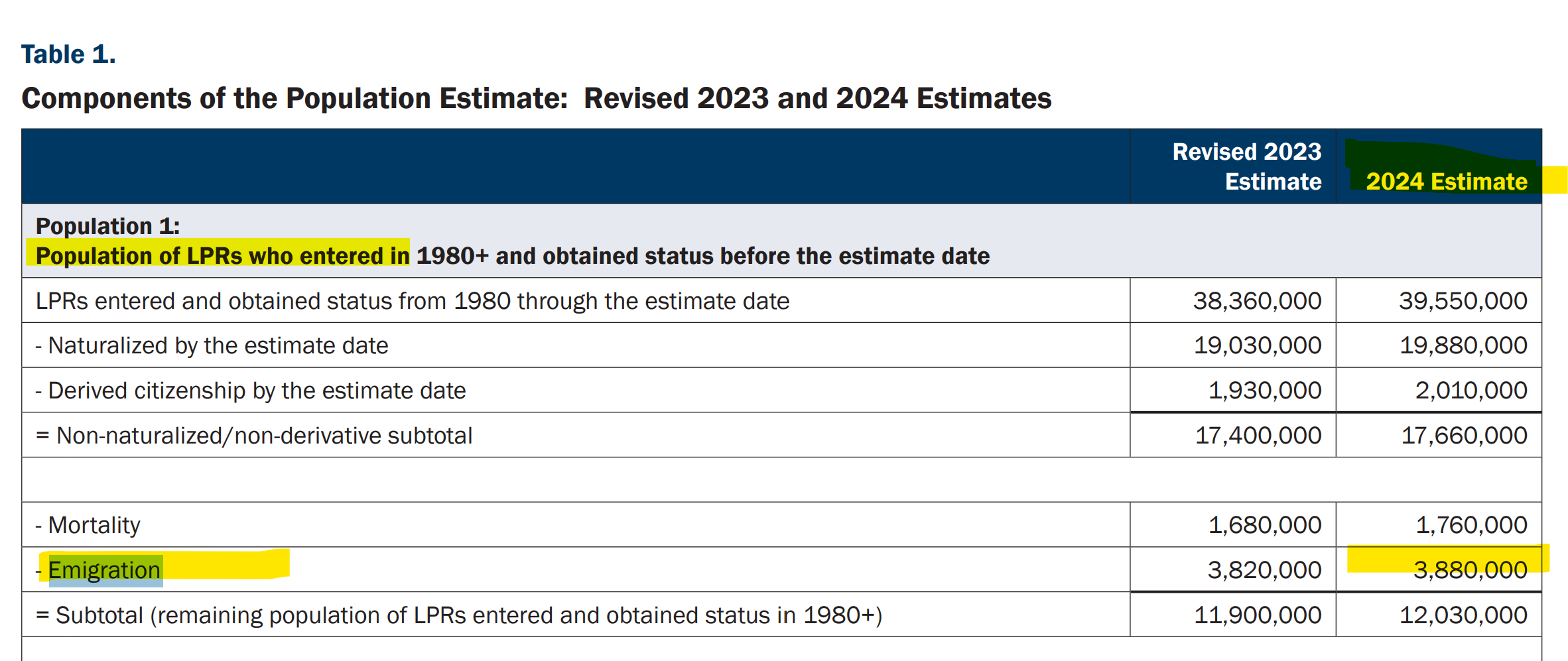

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023; see Table 1 in the report.

In order to understand what issues anyone with a green card has (especially when living outside the U.S.), some key questions should be asked:

- Gifts and inheritances after I leave (what U.S. taxes)

-

- If I become a covered expatriate, can I still give money to my children who live in the U.S. without U.S. taxes?

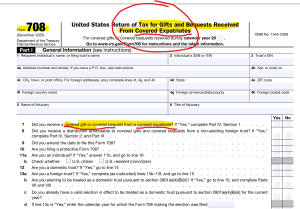

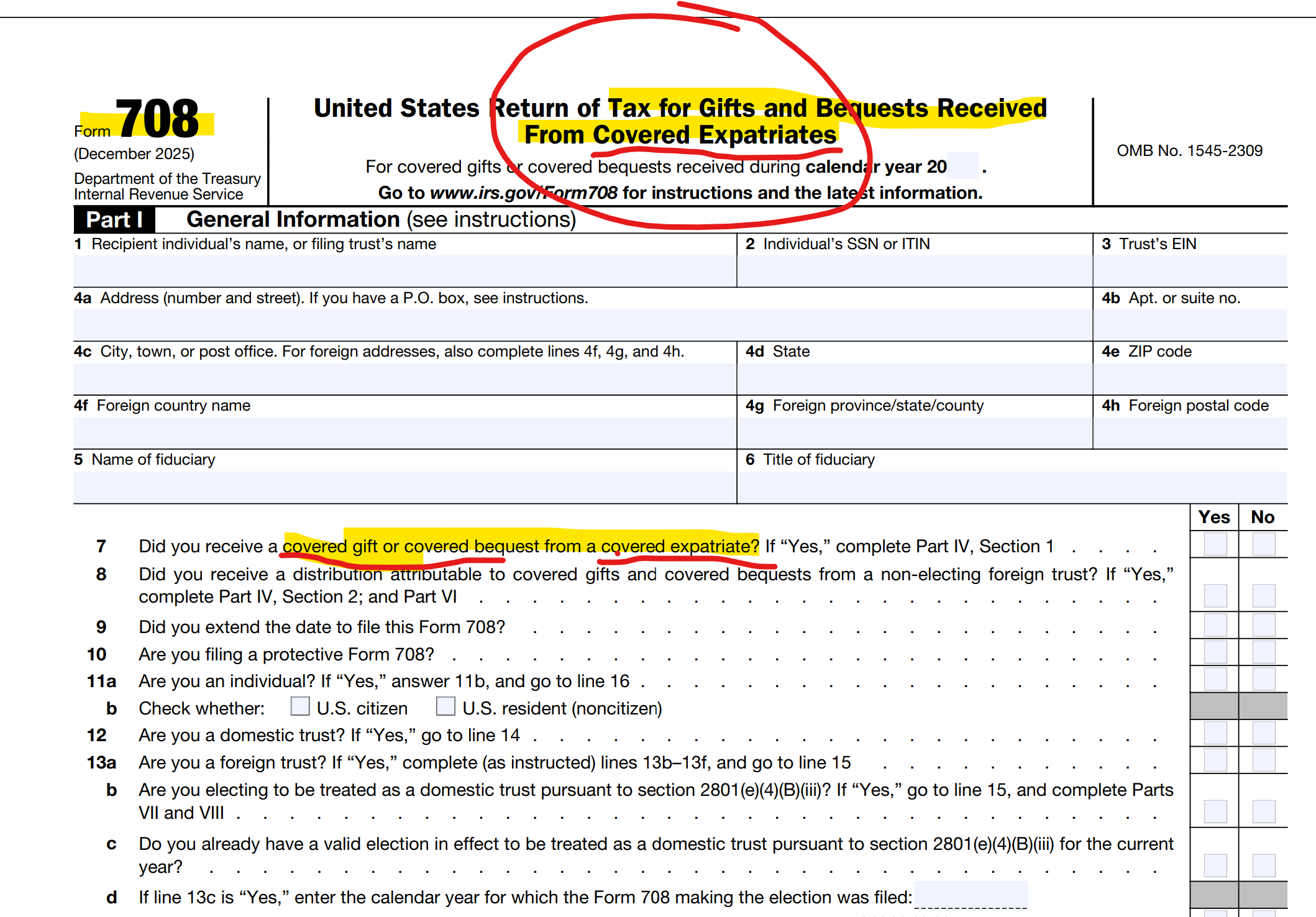

- When do I or my family members need to File IRS Form 708, United States Return of Tax for Gifts and Bequests Received From Covered Expatriates

- Worldwide income while I still have the green card

-

- Does the U.S. tax the salary I earn in my home country?

-

- What is the foreign earned income exclusion, and do I qualify?

- Must I file an IRS Form 8854, Initial and Annual Expatriation Statement

(and what are the legal implications of such filings)? - What if I do not file IRS Form 8854, Initial and Annual Expatriation Statement?

- Am I still a U.S. taxpayer?

-

- If I never told USCIS I left, does the IRS still consider me a U.S. tax resident?

-

- Can I be a U.S. tax resident and a tax resident of my home country at the same time?

-

- What is a “tax treaty tie-breaker” and how does it help or hurt me?

- Aroeste v. United States — what does it mean for me? –

- Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)

-

- If I use the treaty to be a non-resident, am I giving up my green card automatically?

-

- Can I be a non-resident for income tax under the treaty but still be considered a “U.S. person” for other rules like FBAR?

- Do all forms I file with the U.S. federal government (IRS, USCIS, ICE and others) subject me to claims of signing under penalty of perjury?

Stay tuned . . . . . . . . . for III of VI