Month: July 2014

Li Lianjie – Famous Former U.S. Citizens – Born in Beijing, China (“Jet Li”)

The Chinese actor Li Lianjie, who is better known by his stage name Jet Li, was born in Beijing. He was born in 1963 and his father died when he was just 2 years old and he “. . . was from a very poor family and . . . didn’t have enough money for a good school, so sports-school was good . . . ”

He was born in 1963 and his father died when he was just 2 years old and he “. . . was from a very poor family and . . . didn’t have enough money for a good school, so sports-school was good . . . ”

He is a huge star in China and throughout Asia and became famous in Hollywood.

As a teenager he became a master at Wushu, the full-contact sport from Chinese martial arts. His martial arts fame led to acting, first in China and also in the United States. His film debut Shaolin Temple (1982), helped make him a star.

He apparently became a naturalized citizen of the United States while working in Hollywood.

He apparently has also become a naturalized citizen of Singapore.

He is often highlighted by government officials of China as a model citizen and success story.

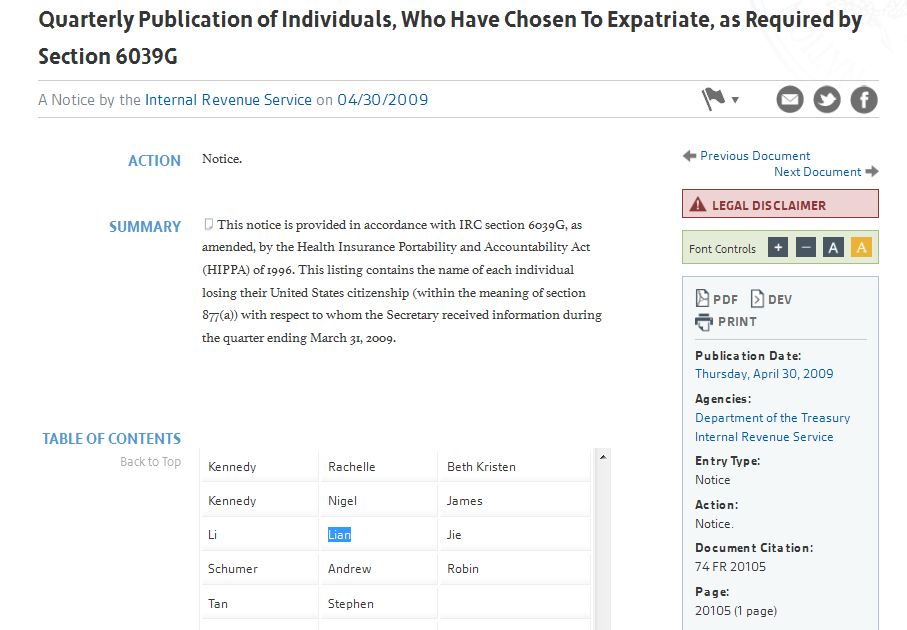

By the year 2009 he renounced his U.S. citizenship as listed in the U.S. federal government’s “Quarterly Publications of Individuals, Who Have Chosen to Expatriate, as Required by Section 6039G“

See here the list for the first quarter of 2009, where Li Lianjie is in the 2009 first quarter list of expatriates.

Presumably, Jet Li solicited timely and filed for a Certificate of Loss of Nationality (“CLN”) timely so he was not subject to the rules of 7701(a)(50) that went into effect in 2008 – See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

Finally, the certification requirement that is available to those individuals who are born with dual national citizenship to avoid “covered expatriate” status, was presumably not available for Li Lianjie, since he was not born a U.S. citizen. Presumably, he could not satisfy each of the requirements of IRC Section 877A(g)(1)(B).

Part II: U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Pasquantino – Wire Fraud and Mail Fraud

Please see my prior post for important background and an introduction to the “Revenue Rule”, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

The 9th Circuit Her Majesty case and the Canadian Supreme Court Harden case were both discussed. Both cases are older (1997 and 1963, respectively) and both directly address the old English common law “Revenue Rule” which stands for the proposition as explained by the Canadian Supreme Court citing to another case that:

“. . . there is a well-recognized rule, which has been enforced for at least 200 years or thereabouts, under which these courts will not collect the taxes of foreign States for the benefit of the sovereigns of those foreign States; and this is one of those actions which these courts will not entertain.”n3 [1928] Ch. 877 at 884.

More recently in 2005 in Pasquantino, the U.S. Supreme Court reaffirmed the “Revenue Rule” with the following statement: “The revenue rule, . . . [u]nder that rule, the courts of one sovereign will not enforce the tax judgments or unadjudicated tax claims of another sovereign.”

However, the Supreme Court in Pasquantino found that a federal “wire fraud” charge (described below) can be used by U.S. prosecutors to pursue criminal tax fraud in another country, under the laws of that other country, when invoking the U.S. wire fraud statute.

In the case of Pasquantino the U.S. prosecutors used Canadian tax evasion related to the smuggling of liquor into Canada as the basis for bringing a U.S. federal wire fraud charge. The individuals used telephone calls to place the liquor purchases from a discount liquor store in the U.S. The telephone calls were the basis of the wire fraud claim; since Canadian excise taxes were not paid upon the importation of the liquor from the U.S.

The U.S. Attorneys Criminal Resource Manual describes ” . . . wire fraud under Section 1343 directly parallel those of the mail fraud statute, but require the use of an interstate telephone call or electronic communication made in furtherance of the scheme. United States v. Briscoe, 65 F.3d 576, 583 (7th Cir. 1995) (citing United States v. Ames Sintering Co., 927 F.2d 232, 234 (6th Cir. 1990) (per curiam)); United States v. Frey, 42 F.3d 795, 797 (3d Cir. 1994) (wire fraud is identical to mail fraud statute except that it speaks of communications transmitted by wire) . . . “

The same manual defines mail fraud: “There are two elements in mail fraud: (1) having devised or intending to devise a scheme to defraud (or to perform specified fraudulent acts), and (2) use of the mail for the purpose of executing, or attempting to execute, the scheme (or specified fraudulent acts).” Schmuck v. United States, 489 U.S. 705, 721 n. 10 (1989); see also Pereira v. United States, 347 U.S. 1, 8 (1954) (“The elements of the offense of mail fraud under . . . § 1341 are (1) a scheme to defraud, and (2) the mailing of a letter, etc., for the purpose of executing the scheme.”) . . .”

A simple example of “mail fraud” is putting in the mail a false U.S. federal tax return. Sending false returns electronically to the IRS could fall within the ambit of a “wire fraud” claim. Making telephone calls, or sending e-mails, between states also is used regularly for wire fraud claims. For an example of how wire fraud and mail fraud charges are brought in tax cases, see the U.S. Attorney’s press release of tax evasion against Congressman Grimm.

The Tax Lawyer published a thoughtful article on the topic in VOL. 59, NO. 2 WINTER 2006, ALL HANDS ON DECK: RESCUING THE REVENUE RULE FROM THE SUPREME COURT’S DECISION IN PASQUANTINO

Imagine that you walk into work tomorrow and find a criminal indictment sitting on your desk. The indictment alleges that recent actions by your company violated the wire fraud statute and that you, as the CEO, are criminally liable.1 According to the government, your company used the U.S. telephone wire system to place calls between New York and California for the purpose of defrauding the Chinese government of property. Specifically, the Government contends that your company defrauded China by not paying taxes due under a Chinese revenue law. While this hypothetical may seem absurd at first, the Supreme Court’s recent decision in Pasquantino v. United States makes this very situation all too realistic.2

At the end of the day, it seems this case stands for the proposition that the U.S. government can indeed use U.S. laws, to at least indirectly enforce the tax laws of another country. The dissenting opinion in this 5-4 decision, written by Justice Ginsburg at 375 noted that (“Canadian courts are best positioned to decide ‘whether, and to what extent, the defendants have defrauded the governments of Canada and Ontario out of tax revenues owed pursuant to their own, sovereign, excise laws.’”) (quoting United States v. Pasquantino, 336 F.3d 321, 343 (4th Cir. 2003).

The direct enforcement by the U.S. government of U.S. tax judgments overseas will usually be very difficult, specifically to collect overseas assets to pay the taxes. However, the point of Pasquantino is that the government has yet another tool to bear against U.S. persons, at least in certain circumstances, that may help them effectively (and indirectly) bring legal actions against them in the U.S. to effectively enforce tax claims arising from transactions overseas. This can be a very powerful tool for the government.

Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0: Including “Streamlined” Rules that are a Game Changer Thursday, July 17, 2014, 12 noon – 1:30 p.m. (PST)

The State Bar of California – Taxation Section

Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0: Including “Streamlined” Rules that are a Game Changer

Thursday, July 17, 2014, 12 noon – 1:30 p.m. (PST)

Speakers:

• Patrick W. Martin of (Procopio et al San Diego – ), who is the tax team leader of the firm’s tax practice and specializes in international tax matters, with a strong focus on international tax compliance

• Mark E. Matthews of (Caplan & Drysdale in DC – ) focuses his practice on criminal tax enforcement, broad-based civil tax compliance and was Chief of the IRS Criminal Investigation Division, the agency’s investigative and law enforcement arm.

This program offers 1.5 hours participatory MCLE credit, 1.5 legal specialization credit in the area of Taxation Law and .5 hour credit in Legal Ethics. You must register in advance in order to participate.

Just days ago (June 2014), the IRS significantly revamped the “offshore voluntary disclosure program” (“OVDP”) that has existed since 2009. The new terms of the OVDP have now completely changed the “rules of the road” about how and when taxpayers can or should participate in such program. In addition, the so-called “streamlined” process has been changed in virtually all respects.

Learn – when should a taxpayer be considering the 2014 OVDP? When should a taxpayer not participate in the 2014 OVDP? When is an individual eligible? Learn important differences under the 2014 OVDP for those who reside in the U.S. versus U.S. citizens and lawful permanent residents who reside outside the U.S.

Understand the legal ramifications for those who sign certifications under penalties of perjury.

Understand the legal risks for financial, tax and legal advisers.

These changes create numerous legal risks for the unwary and for the financial, tax and legal advisers.

Find out how you can best assist your clients and minimize their legal risks, while simultaneously complying with the labyrinth of rules imposed by the Internal Revenue Service, including modifications to their own terms. This Webinar is appropriate for tax lawyers, non-tax lawyers (such as trusts and estate lawyers and business lawyers), certified public accountants, bankers, trust officers, trustees, enrolled agents and others who have clients who have assets located outside the U.S.

A detailed highlight of the new rules of circular 230 and their application in light of these changes to the OVDP will be discussed, along with other important ethical considerations and practice pointers.

Understand the legal ramifications of U.S. taxpayers who sign certifications under penalties of perjury, specifically including those required by the OVDP. How will United States citizens and lawful permanent residents (“LPR”) who are residing outside the United States view these rules? What are the pitfalls of the revisions in this program? How does the recent jury verdict in the willfulness FBAR 50% penalty case (with 150% penalty found by the jury) in Zwerner affect decisions of taxpayers and their advisers?

This webinar is taught by experienced tax lawyers, all former employees of the IRS, including a former Chief of the IRS Criminal Investigation Division, including experts who specialize in international tax related matters and advising those with worldwide assets; multi-national families and U.S. citizens and LPRs residing outside the U.S.

Extensive written materials will be provided that analyze the law, consider various legal implications of the 2014 OVDP. The course will specifically focus on current trends and developments of the IRS and Tax Division/Justice Department and current civil and criminal cases moving forward.

Plus, understand the basics of FATCA (the Foreign Account Tax Compliance Act) now in effect for 2014 and how this affects this arena of practice and international tax compliance. Specifically understand the role of FATCA under the new IRS modifications to the OVDP and why it is more important than ever.

Finally, some key income tax concepts of residency and international information reporting requirements under Title 26 and Title 31 will be briefly analyzed in the context of the 2014 OVDP.

Moderator: Eric D. Swenson of (Procopio et al San Diego – http://www.procopio.com/attorneys/eric-d-swenson) is a tax attorney with multiple years at Chief Counsel in the IRS and handles complex tax controversy and defense cases against the IRS and State taxing authorities.

Speakers:

• Patrick W. Martin of (Procopio et al San Diego – http://www.procopio.com/attorneys/patrick-w–martin), who is the tax team leader of the firm’s tax practice and specializes in international tax matters, with a strong focus on international tax compliance

• Mark E. Matthews of (Caplan & Drysdale in DC – http://www.capdale.com/mmatthews) focuses his practice on criminal tax enforcement, broad-based civil tax compliance and was Chief of the IRS Criminal Investigation Division, the agency’s investigative and law enforcement arm.

To register, see Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0 or go to http://www.calbar.org/online-cle and select Taxation or Webinars.

Part II: IRS Form W8-IMY – FATCA Driven – More on the W-9 and W-8 Alphabet Soup with FATCA: IRS Form W8-IMY

Part II: IRS Form W8-IMY – FATCA Driven – More on the W-9 and W-8 Alphabet Soup of FORMs: IRS Form W-8-IMY

FATCA, “Chapter 4”, withholding started the first week of this month, July 1, 2014. Presumably the amount of FATCA withholding will be nominal, if for no other reason, virtually all of the major world economies are countries that have actually signed an IGA or “reached an agreement [FATCA] in substance”.

See the complete and most recent list of countries who have signed FATCA IGAs or “reached an agreement in substance.” See, Russia Joins the FATCA Group – On the Last Day? Complete List of Countries to Date (Very Few Notable Absences)

As explained in previous posts, the U.S. federal tax authority, the Internal Revenue Service (IRS) has been modifying dramatically the tax forms required to be filled out and filed by both individuals, financial institutions around the world (FFI) and by non-financial foreign entities (NFFE) all due to FATCA. See, specifically the post that focused on new form W8-BEN-E. See, FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

United States Citizens (USCs) and Lawful Permanent Residents (LPRs) who reside outside the U.S. will need to have a general understanding of how these forms are to be completed. This is particularly important, since they are to be signed under “penalty of perjury” as to their accuracy. There will be a host of institutions that will be requesting USCs and LPRs residing overseas to complete these forms, including their banks, investment and brokerage houses, investment funds, private companies, mutual funds, etc. in their home country of residence or any other country outside the U.S.

What information and how it needs to be provided, depends upon whether the USC or LPR is being asked to sign as an individual. If that is the case see, FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

If the account with the financial institution is not an individual account, a W8-BEN-E or W8-IMY will typically be required to be completed by the entity, when the USC or LPR has an ownership interest in the entity (e.g., corporation, partnership or trust). Specifically when a USC or LPR is a “substantial U.S. owner” as defined by the statute and FATCA regulations. In short, a “substantial U.S. owner” is a “U.S. person” (which always includes USCs and sometimes includes LPRs) with more than a 10% interest by vote or value in a foreign corporation, partnership or trust.

There is no 10% ownership threshold for “foreign investment vehicles” (as defined in IRC Sections 1473(2)(B) and 1471(d)(5)(C)) such as investment funds, private equity funds, private companies, etc. where itis engaged (or holding itself out as being engaged) primarily in the business of investing, reinvesting, or trading in securities, partnership interests, commodities, or any interest (including a futures or forward contract or option) in such securities, partnership interests, or commodities.

As you can see, this is a very broad definition that does not require any ownership threshold to cause reporting; a .00001% ownership interest in a “foreign investment vehicle” will give rise to a “U.S. owner” and hence subject to FATCA reporting.

This post and follow-up posts focuses on a few key aspects of the Form W-8IMY.

Incorporated into this post are key pages, showing the different categories that a partnership or a trust (or other “flow through” entity) will be required to complete when representing their status to different third parties, including foreign financial institutions.

Normally, the individual USC or LPR will not need to complete the W-8IMY (but certainly may be required if they are the managing partner of a partnership, trustee of a trust, or fall into other categories identified in the law). It will be the trust or partnership itself that will be collecting information about its U.S. owners (e.g., through an IRS Form W-9). The trust or partnership itself, will then be reporting this information to the foreign financial institution that will then report to the IRS (or to their own country who will then report to the IRS if there is an IGA in place).

U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

Maybe its a natural response for USCs and LPRs living overseas to ask: “What is the chance I will get audited by the IRS?” Sometimes, those individuals who either have less good faith (or are simply ignorant about how U.S. tax law functions) will also ask: “How will the U.S. government ever know of my assets or income in my home country?”

A follow-up question is how does the U.S. federal government enforce tax obligations overseas? This question often comes, of course, from individuals who reside in different countries outside the U.S. and typically have most (if not all) of their assets located in their country of residence.

A USC or LPR residing in Costa Rica, for instance, might have almost all of his business assets in Costa Rica and maybe financial investment assets in nearby regions such as Panama. Similarly, a Chinese born dual national USC may have companies and business assets in both mainland China and Hong Kong. If neither of these individuals have assets in the U.S., how can the U.S. federal government enforce tax liens, levies and the like against these individuals?

investment assets in nearby regions such as Panama. Similarly, a Chinese born dual national USC may have companies and business assets in both mainland China and Hong Kong. If neither of these individuals have assets in the U.S., how can the U.S. federal government enforce tax liens, levies and the like against these individuals?

These questions are getting asked more and more now that FATCA has gone into force and financial information around the world is being collected regarding USC accounts in virtually all countries and financial institutions. See, FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

An excellent layman’s term summary of FATCA can be located on HSBC’s website here.

This overseas asset and income information will eventually be delivered, pursuant to the FATCA rules, to the U.S. Internal Revenue Service (IRS – revenue authority).

Hence, the collection of information under FATCA will be extensive. This, at least in part, answers the question of: “How will they ever know of my assets or income in my home country?” Admittedly, the complete answer to this question is far more complicated, when one considers the intricacies of FATCA and its regulations and other guidance from the IRS/Treasury.

However, that is a different question, than how that financial and income information will be used by the IRS to (a) make tax assessments, (b) assess and collect foreign bank account report (FBAR) penalties (See, Section 16 of the IRM), and (c) generally enforce and collect such tax assessments and penalties against USCs and LPRs residing outside the U.S.

1. INFORMATION – The collection of asset and financial information under FATCA has a very “long arm” around the world. Indeed, the image of the Uncle Sam octopus published in the June 28, 2014 article in the The Economist entitled Taxing America’s diaspora: FATCA’s flaws captures well the idea of the reach of FATCA.

2. INFORMATION VS COLLECTION – However, enforcing tax assessments and penalties and collecting against assets located outside the U.S. is a very different legal question, without such a “long arm”; simply because the reach and jurisdiction of U.S. law is necessarily limited and regularly in conflict with local laws of different countries.

To say it another way, Uncle Sam can indeed enforce the collection of financial and asset information under FATCA, due to the economic costs and ramifications to financial institutions and their investors if they did not comply with the automatic information exchange. However, Uncle Same cannot simply enforce the collection of U.S. taxes and penalties through the worldwide financial institutional network, the same way it can in the U.S.

The U.S. has broad lien, levy and seizure powers under U.S. tax law. The IRS can simply seize assets from U.S. bank accounts without going to a judge or court for final (or jeopardy) tax assessments provided they comply with various provisions of the law. This is not a typical concept in the law for other creditors (other than the IRS) who must generally first take steps through the courts to get some type of judicial action (e.g., a court order) before simply seizing and taking assets from an individual.

The IRS’s broad lien and levy powers against assets, however, has significant limitations overseas. See the 1998 Treasury Report – Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs, I hav e worked with IRS Revenue Officers who specialize in international collection matters who argue and assert they can merely exercise this lien and levy power overseas against foreign financial institutions. However, this is where the power of the IRS comes to a screeching halt (or at least a major slowdown); when the collection of overseas assets is at stake.

e worked with IRS Revenue Officers who specialize in international collection matters who argue and assert they can merely exercise this lien and levy power overseas against foreign financial institutions. However, this is where the power of the IRS comes to a screeching halt (or at least a major slowdown); when the collection of overseas assets is at stake.

The IRS is not without remedies to collect foreign assets, but it is not a simple process; if it can be done at all in any particular circumstance.

The IRS has no specific enforcement provisions negotiated in international treaties that will necessarily enable them to enforce and collect U.S. income taxes overseas with foreign government assistance. The cornerstone 9th Circuit case of Her Majesty held in 1979 that the Canadian tax authorities could not enforce a tax judgment against U.S. taxpayers within the U.S. –

The basic facts were these, as reported in the case:

British Columbia then served a “Notice of Intention to Enforce Payment” on the defendants in the United States, and filed a certificate of assessment in the Vancouver Registry of the Supreme Court of British Columbia. This certificate was for $195,929.50 (a penalty and interest were included), and under the laws of British Columbia its filing gave it the same effect as a judgment of the court. British Columbia then instituted the present action in the United States. It was dismissed because the court below concluded that the Oregon courts would follow the “revenue rule.” Stated simply, the revenue rule merely provides that the courts of one jurisdiction do not recognize the revenue laws of another jurisdiction.1

The U.S. 9th Circuit Court went on to say:

Although the Supreme Court has never had occasion to address the question of whether the revenue rule would prevent a foreign country from enforcing its tax judgment in the courts of the United States, the indications are strong that the Court would reach the same result as we reach in the present case. Both the majority and the dissenting opinion in Banco Nacional de Cuba v. Sabbatino, 376 U.S. 398, 84 S.Ct. 923, 11 L.Ed.2d 804 (1964), discussed the rule in a spirit which indicates a continued recognition of the revenue rule in the international sphere.10

This Majesty case specifically cited a Canadian Supreme Court case (Harden) which also applied the revenue rule in not enforcing a tax judgement in the U.S. courts for taxes against a Canadian resident:

Reciprocity would itself be a sufficient basis for denying British Columbia’s claim. The courts of British Columbia, relying upon the revenue rule, have refused to recognize the judgment of a United States court for taxes. United States v. Harden, 1963 Canada Law Reports 366 (Sup.Ct. of Canada, 1963, Affirming Court of Appeal for British Columbia).12

CONCLUSION: The revenue rule has been with us for centuries and as such has become firmly embedded in the law. There were sound reasons which supported its original adoption, and there remain sound reasons supporting its continued validity. When and if the rule is changed, it is a more proper function of the policy-making branches of our government to make such a change.

As a result of these cases and the Revenue Rule, the U.S. and Canada modified their income tax treaty to (at least in theory) allow for the international enforcement of taxes. The U.S. now has five income treaties with “mutual assistance” provisions: Canada, Sweden, France, Denmark, and the Netherlands (with a clause in the newly negotiated, but yet to go into force, Swiss treaty).

The U.S. tax and international tax world has changed dramatically since 1979 and the 9th Circuit case of Her Majesty particularly with the advent of FATCA. Nevertheless, there are serious legal limitations imposed on t he IRS in collecting assets for U.S. tax liabilities and penalties owed by USCs and LPRs residing overseas. Indeed, this is surely one of the principle reasons the IRS revised OVDP terms in June 2014 impose a 0% penalty against USCs and LPRs who participate in the so-called “streamlined process”. See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas.

he IRS in collecting assets for U.S. tax liabilities and penalties owed by USCs and LPRs residing overseas. Indeed, this is surely one of the principle reasons the IRS revised OVDP terms in June 2014 impose a 0% penalty against USCs and LPRs who participate in the so-called “streamlined process”. See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas.

The follow-on post will discuss the very limited provisions that have been recently negotiated with these five different countries and explain in more detail the limits on the U.S. federal government on the collection of taxes. It will also discuss the important differences of civil U.S. international tax enforcement/collection versus criminal tax enforcement; which are two very different beasts.

Finally, a dedicated post on the topic will discuss the steps the U.S. federal government is taking through the Department of Homeland Security and a database of information (TECS) to track and monitor people and their assets. The government describes TECS as follows: “The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. It contains information about individuals and businesses suspected of, or involved in, violations of federal law.”

More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. – -(What if there are No Records?)

The statutory rules of PFICs are set forth in 26 U.S. Code § 1297 – Passive foreign investment company. The U.S. Treasury and IRS also published new regulations in January 2014 on PFICs.

For an overview, see “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

United States Citizens living overseas, whether or not they are “Accidental Americans”, as well as lawful permanent  residents (LPRs) living outside the U.S. generally have the burden of proof under U.S. tax law to show they complied with U.S. law. Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

residents (LPRs) living outside the U.S. generally have the burden of proof under U.S. tax law to show they complied with U.S. law. Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

This presumption of correctness was confirmed by the U.S. Supreme Court and therefore imposes the burden on the taxpayer of proving that the assessment made by the IRS is erroneous. During my career, I have seen plenty of erroneous assessments made by the IRS, and an increasing number of assessments made against taxpayers residing in countries throughout the world, be it France, Australia, Canada, Russia, Germany, Mexico, Thailand, Japan, Hong Kong, etc.

Why is this presumption of correctness relevant, when PFICs are explained and discussed here? The law of PFICs is complex, to the point that very few IRS revenue agents really have any detailed understanding of how PFICs work, when they apply and how taxpayers are to report their investments in PFICs. Very few U.S. tax practitioners understand PFICs.

Accordingly, I regularly see errors made by the IRS in proposed tax assessments, including PFIC calculations. Unfortunately for the individual taxpayer, they must prove the IRS is wrong in its tax assessment.

PFICs create a real burden on individual taxpayers who have shares in a PFIC in different locations around the world, since it is rare that foreign companies, investment funds, mutual funds and the like ever provide any detailed accounting of (a) asset, or (b) income information (per U.S. tax rules) that are required to be reported by PFIC investors who are USCs or LPRs.

Unlike a controlled foreign corporation (CFC), a PFIC has no ownership threshold. If a USC owns just 1,000 shares/units out of 20M issued shares in a foreign mutual fund, the U.S. citizen will nevertheless need to report this 1,000 share/unit interest (even though this is only 0.0005% of the fund) on his or her individual income tax return if the foreign mutual fund meets – the income test or asset test. Virtually all mutual and investments funds will satisfy these tests, since by definition the funds are making investments in other companies or other passive income items, such as bonds, stocks, futures, ETFs, etc.

The income test is met when at least 75% of the income is passive income as defined under the law. The asset test is satisfied when at least 50% of the foreign corporation’s average assets produce such passive income.

The practical problem arises when the individual taxpayer needs information from the fund (or other foreign entity) that reflects information such as –

- the pro-rata share of the “ordinary” earnings (in the example above, just 1,000 share/20M shares – 0.0005% of the fund);

- the pro-rata share of the “net capital gain”;

- the total cash or property distributed;

- the total cash or property “deemed” distributed (which means there was actually no distribution – but the law “deems” there to have been a distribution); and

- many other complex calculations that require basic information to be provided by the PFIC in the first place.

What foreign fund or investment company around the world (located in whatever country – catering to customers commonly in their own country) even tracks or accounts for income and gains for U.S. tax law purposes; i.e. “ordinary” earnings versus “capital gains” – specifically including the netting of “capital gains” and “capital losses” as required by U.S. law? I certainly do not see such accounting records provided in the marketplace of investment funds, hedge funds and companies that cater to persons residing outside the U.S.

Most foreign companies around the world (unless they are controlled and managed by USCs who are aware of these U.S. tax obligations) never maintain such accounting records or the detailed information necessary to even provide it to their USC or LPR investors. Hence, USCs/LPR investors may never be able to accurate make these PFIC calculations.

Also, the ownership of shares/units of the fund might always be changing throughout the year. In other words, even if the “ordinary income” and “net capital gain” is available for a particular fund/PFIC, the total number of outstanding shares/units has to be stable or known for the USC or LPR to calculate their pro-rata share. In the above example, if there are 20M outstanding shares/units at the beginning of the year, but by the end of the year there are 22M outstanding shares/units, how is the USC or LPR investor ever going to be able to calculate their pro-rata share, assuming they have the “ordinary” earnings and “capital gains” amounts for the entire calendar year? Its not simply the “ordinary” earnings and “capital gains” multiplied by 0.0005%.

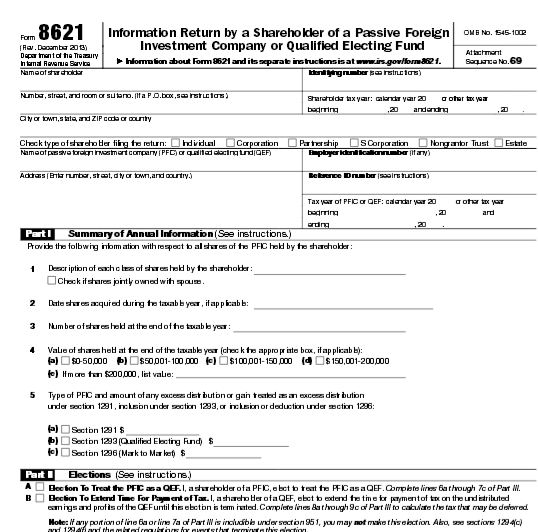

The only “good news” in this explanation of PFICs, is that there is not an automatic US$10,000 penalty for failure to file their investments in a PFIC on IRS Form 8621, Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund.

This is a departure from the normal rule of a minimum US$10,000 penalty for failure to file information returns regarding international (i.e., non-U.S. assets and investments). See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms.

All of these tax compliance rules begs a very important question for a USC who is considering renouncing their U.S. citizenship. The issue arises if they have had investments in PFICs during the last five years. If the USC has not been complying with IRC Section 1297 regarding PFICs, how can the taxpayer ever certify under penalty of perjury ” . . . that he has met the requirements of this title for the 5 preceding taxable years. . . [for purposes of Section 877(a)(2)(C)]”?

More details about PFICs to come in later posts.

Russia Joins the FATCA Group – On the Last Day? Complete List of Countries to Date (Very Few Notable Absences)

According to The Moscow Times, Putin Signs Last-Minute Law to Satisfy FATCA

With China and Russia as prior major holdouts, the recent news from both countries probably assures the long-term success of FATCA.

There are very few notable “hold-outs” on FATCA IGAs. The following list reflects those countries of note (from my perspective) who have not signed or “reached an agreement in substance”:

Kenya

Nigeria

Egypt

Pakistan

Bahrain

Philippines

Malaysia

Guatemala

Uruguay

El Salvador

Nicaragua

Ecuador

Argentina

Venezuela

Lots of other countries with less commercial and financial ties to the U.S., did not – including – countries such as Kazakhstan, Uzbekistan and Cambodia.

There are currently 90 countries identified by the U.S. Treasury as having an IGA or “reaching an agreement in substance” as follows (note there are fewer signed IGAs than unsigned):

Countries that have signed agreements:

Model 1 IGA

1) Australia (4-28-2014)

2) Belgium (4-23-2014)

3) Canada (2-5-2014)

4) Cayman Islands (11-29-2013)

5) Costa Rica (11-26-2013)

6) Denmark (11-19-2012)

7) Estonia (4-11-2014)

8) Finland (3-5-2014)

9) France (11-14-2013)

10) Germany (5-31-2013)

11) Gibraltar (5-8-2014)

12) Guernsey (12-13-2013)

13) Hungary (2-4-2014)

14) Honduras (3-31-2014)

15) Ireland (1-23-2013)

16) Isle of Man (12-13-2013)

17) Italy (1-10-2014)

18) Jamaica (5-1-2014)

19) Jersey (12-13-2013)

20) Latvia (6-27-2014)

21) Liechtenstein (5-19-2014)

22) Luxembourg (3-28-2014)

23) Malta (12-16-2013)

24) Mauritius (12-27-2013)

25) Mexico (4-9-2014)

26) Netherlands (12-18-2013)

27) New Zealand (6-12-2014)

28) Norway (4-15-2013)

29) South Africa (6-9-2014)

30) Spain (5-14-2013)

31) Slovenia (6-2-2014)

32) United Kingdom (9-12-2012)

Model 2 IGA (signed agreements)

33) Austria (4-29-2014)

34) Bermuda (12-19-2013)

35) Chile (3-5-2014)

36) Japan (6-11-2013)

37) Switzerland (2-14-2013)

And those countries which are deemed to have “reached agreement in substance” –

Model 1 IGA

38) Algeria (6-30-2014)

39) Antigua and Barbuda (6-3-2014)

40) Azerbaijan (5-16-2014)

41) Bahamas (4-17-2014)

42) Barbados (5-27-2014)

43) Belarus (6-6-2014)

44) Brazil (4-2-2014)

45) British Virgin Islands (4-2-2014)

46) Bulgaria (4-23-2014)

47) China (6-26-2014)

48) Colombia (4-23-2014)

49) Croatia (4-2-2014)

50) Curaçao (4-30-2014)

51) Czech Republic (4-2-2014)

52) Cyprus (4-22-2014)

53) Dominica (6-19-2014)

54) Dominican Republic (6-30-2014)

55) Georgia (6-12-201)

56) Greenland (6-29-2014)

57) Grenada (6-16-2014)

58) Guyana (6-24-2014)

59) India (4-11-2014)

60) Indonesia (5-4-2014)

61) Israel (4-28-2014)

62) Kosovo (4-2-2014)

63) Kuwait (5-1-2014)

64) Lithuania (4-2-2014)

65) Panama (5-1-2014)

66) Peru (5-1-2014)

67) Poland (4-2-2014)

68) Portugal (4-2-2014)

69) Qatar (4-2-2014)

70) Romania (4-2-2014)

71) St. Kitts and Nevis (6-4-2014)

72) St. Lucia (6-12-2014)

73) St. Vincent and the Grenadines (6-2-2014)

74) Saudi Arabia (6-24-2014)

75) Seychelles (5-28-2014)

76) Singapore (5-5-2014)

77) Slovak Republic (4-11-2014)

78) South Korea (4-2-2014)

79) Sweden (4-24-2014)

80) Thailand (6-24-2014)

81) Turkey (6-3-2014)

82) Turkmenistan (6-3-2014)

83) Turks and Caicos Islands (5-12-2014)

84) Ukraine (6-26-2014)

85) United Arab Emirates (5-21-2014)

Model 2 IGA

86) Armenia (5-8-2014)

87) Hong Kong (5-9-2014)

88) Moldova (6-30-2014)

89) Paraguay (6-6-2014)

90) Taiwan (6-23-2014)*

- ← Previous

- 1

- 2