International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

Can You Lose Your Green Card Just by Living Outside the United States?

Many green card holders who move abroad assume their permanent resident status is safe as long as they return to the United States occasionally. Under US immigration law, that assumption can be wrong. A green card can be abandoned automatically, without any formal filing, simply by how long you spend outside the United States.

A lawful permanent resident (LPR) can lose permanent resident status through removal (deportation) ordered by an immigration court, or through abandonment. Abandonment can happen formally, by filing Form I-407 (Abandonment of Lawful Permanent Resident Status), or automatically, by operation of law, when an LPR takes an action that constitutes abandonment under immigration law, such as departing the United States for more than a temporary visit abroad. There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

What triggers an automatic abandonment finding?

The Department of Homeland Security (DHS) will make an abandonment finding if an LPR takes a single trip outside the United States lasting more than one year. After a trip of more than one year, the LPR can only challenge the finding in removal proceedings. For a single trip lasting between 6 months and one year, DHS presumes the LPR intended to abandon their permanent resident status, but the LPR may rebut that presumption. Even for shorter trips, DHS may find abandonment if the LPR has spent a significant amount of time outside the United States on multiple trips.

What factors does DHS consider?

DHS and the immigration courts look at: the purpose and duration of the trip abroad; whether there was a specific event after which the LPR planned to return; and the LPR’s family ties, employment, property holdings, and business affiliations in the United States versus the foreign country.

How does filing a tax return as a non-resident affect your status?

Filing a US income tax return as a non-resident alien raises a rebuttable presumption of abandonment of LPR status for immigration purposes.

What can you do if you expect a long absence?

If an LPR knows they will need to spend significant time outside the United States, they should apply for a reentry permit before departing. A reentry permit alone does not guarantee readmission following a long absence, but it is evidence of the intent to return to the United States and maintain permanent resident status.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

How Many Lawful Permanent Residents does the U.S. Receive (Per Year: 1820-2022)

There is an idea that only recently has permanent resident US immigration status into the United States grown substantially. The peak years were in the early 1990s as to absolute numbers. However, the greatest number of permanent residents as a relative percentage of the population was in the early 1900s; by far. See the chart below that I created from DHS immigration statistics data.

There were more LPRs admitted, in absolute terms in 1905 (1,026,499) than in 2022 (1,018,349).

[arm_restrict_content plan=”2,” type=”show”]

In percentage terms the total number of LPRs in 1905 compared to the total population was more than four times (4X) greater than in 2022 when it was (about 3/10th of 1 percent or 0.306%; versus a total population of 333 million) . In 1905 the total population was about 84 million, with newly admitted LPRs representing 1.225 percent of the entire resident population (1.225%; is greater than 4X the 2022 relative percentage).

The “Mark to Market” Tax that did NOT Exist in 1820, 1913, 1966 (Not Until 1996)

The US tax expatriation laws now impose a “mark to market” tax on so-called “long-term residents” who become “covered expatriates.” Such a concept in the tax law never existed in the early part of the 20th century, and indeed only became law in 1996. See an earlier post, The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of US Tax Expatriation law

This so-called Mark to Market tax is based upon a legal fiction, as if the individuals sold their worldwide assets on the “expatriation date.” It applies, even though there’s no current sale of assets, no disposition, transfer, change of ownership, change of title, or other “realization” event. The term “realization” is very significant in US tax law, including as recently discussed by the United States Supreme Court. See below and Moore v. the United States (2024) .

Below is a table of LPRs who were admitted to that status, per year, over the last 200+ years starting in 1820:

Are you or any of your family members one of these millions (more than 88 million) of LPR individuals represented in the above graph over the last 200+ years?

Does TIGTA have the Answer: to the Question – How many former U.S. citizens and long-term lawful permanent residents have filed and should have filed IRS Form 8854?

The short answer to the question above – is NO!

The government does not know how many IRS Forms 8854 should have been filed.

Note the total numbers of 8854 returns filed as reported in Figure 2 of the TIGTA Report were less than 25,000 during a ten year period. This report focuses really only on former U.S. citizens (“USC”) who have renounced their citizenship. Not on lawful permanent residents (“LPRs), which during that same ten year period there were around 200,000 who filed USCIS Form I-407.

* How Many Individuals Should have Filed Form 8854?

How Many LPRs are Living in Tax Treaty Countries like Aroeste (Now including Chile)? What are the Legal-Tax Consequences? (Part I of II)

No, not talking about Texas-Style Chili as reported in the – NYT Cooking Recipe.

Chile, the country in South America and the newest country to have an income tax treaty go into force with the United States. The U.S.-Chile Tax Treaty (in the works for more than a decade) went into force at the end of 2023, on 19 December 2023.

The question is how many “LPRs” are residing in a tax treaty country that are impacted favorably (presumably all of them) by the federal district court decisions we successfully handled against the IRS and DOJ, Tax Division: Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)?

As previously explained, the Aroeste decision will affect potentially millions of “Green Card” holders (a subset of the 3.89M estimated by the government) living outside the U.S. Those who have not formally abandoned their lawful permanent residency status. See, “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – (2020). This “LPR Tax Limbo” is no longer the case after the Aroeste decision.

These individuals who are living in tax treaty countries are not in “LPR Tax Limbo” any more since the Court clarified when the individual is not a United States tax resident. The Court explained, that filing a “late” tax treaty position, does not cause the non-U.S. citizen to have waived the benefits of the income tax treaty. It is the tax treaty with each of the 66 countreis that has the potential of unlocking the “escape hatch” described by the Court.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

The court in Aroeste outlined a 5-step analysis that becomes crucial for the 3.89 million LPRs residing abroad in one of the 66 tax treaty countries, in determining whether they are “United States persons” under the law. This will be covered in Part II.

Millions of LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in November 2023 as of 2014 (until the Chile treaty came into effect). The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importantly, anyone in these circumstances would be remiss, if they did not consider carefully the “mark to market” tax implications to them if they were to become a “covered expatriate” as defined in the law. These “mark to market” tax consequences can have potentially devastating consequences, including to U.S. beneficiaries in the future if not properly planned and considered.

Immigration Forms, I-407; I-485, Application to Register Permanent Residence or Adjust Status & Tax Forms, 1040, 1040NR, 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114, etc. etc. (Part I of III)

The U.S. tax law is complex, including when an individual (i) becomes and (ii) ceases to be, a U.S. income tax resident (USITR). USITR is not a technical term used under the tax law. The U.S. tax and information reporting requirements are very different depending the status of an individual. Anyone who is not a United States citizen, is either a –

“Resident alien“, or a

“Nonresident alien” as the tax law defines both of these categories.

You can’t be both.

“Resident aliens” are generally also “United States persons” (both technical terms in the federal tax law).

“Non-resident aliens” as defined are necessarily not “United States persons.”

Being one versus the other has huge U.S. tax and reporting consequences.

An individual who is a “lawful permanent resident” as referenced in the tax law (Section 7701(b)(6)) cross-references the U.S. immigration law. The first requirement of that statutory tax rule in § 7701(b)(6)(A)) is that “(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws [such status not having changed]. . .[emphasis added]” This means the tax definition is dependent upon the immigration laws, which are found in Title 8, Immigration and Nationality Act. Importantly, the last part of that sentence (i.e., [such status not having changed] is a requirement in the immigration law (Title 8), but does not appear in the tax definition.

The term “lawful permanent resident” cannot be found in Title 8 as a noun or object (i.e., the individual). Instead, the immigration law defines the status of a person in 8 U.S. Code § 1101(a) as follows:- “. . . (20) The term “lawfully admitted for permanent residence” means the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed.“

This analysis is fundamental to be able to determine whether an individual who holds a “green card” in their pocket even has the status of being “lawfully admitted for permanent residence. . . such status not having changed.” It’s a fundamental legal question under immigration law that must be answered first, to then be able to answer the tax question.

Each form an individual files or does not file (e.g., IRS tax form 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114; and immigration forms, e.g., I-485, I-407, etc.) can have a potential impact on the tax residency status of an individual.

The immigration law and when forms, such as Form I-485, Application to Register Permanent Residence or Adjust Status are submitted to the U.S. federal government can have an impact on this determination. The government can use it against the individual as they did unsuccessfully in Aroeste (see below – Pages 9 and 11 of 17); asserting that Mr. Aroeste waived the treaty by not submitting certain forms.

The entire case from the Federal District Court can be read here: Aroeste v. United States, 22-cv-00682-AJB-KSC (20 Nov. 2023):

The tax residency analysis for those who have kept their “green card” in their pocket, can be even more complex as was analyzed by the Court. There are additional provisions of the law that must be considered including old Treasury Regulations that pre-date many provisions of various U.S. income tax treaties.

For instance, each of the following federal tax statutory rules, which will be considered in more detail in later posts (II and III):

Additional posts will review the impact of these provisions in the law and how various immigration forms (including I-485 and I-407, Record of Abandonment of Lawful Permanent Resident Status) and tax forms (including 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858) and FinCEN form 114, can impact the determination of whether someone who has a “green card” in their pocket is or is not a United States person.

What Questions Need to be Asked if You Live (with a “green card”) in one of the 67 Countries – with a U.S. Income Tax Treaty?

Depending upon the factual circumstances of each individual, they may be able to benefit from the international tax treaty law articulated by the U.S. Federal District Court in Aroeste v United States – Order (Nov 2023). Future posts will explore the legal relevance of some of the following questions to consider:

Has the individual filed any U.S. federal income tax returns since leaving the United States?

Was a professional tax return preparer hired or consulted about the filing of a federal income tax return (e.g., a certified public accountant, an enrolled agent, a full time tax return preparer, ta tax attorney, etc.)?

Has the individual been filing IRS Form 1040 Resident Tax Returns in the same way Mr. Aroeste was filing – based upon the advice (that turned out to be erroneous -although given in good faith) from their U.S. tax return preparer?

What steps if any have been taken to notify the U.S. federal government (irrespective of the agency) regarding their physical residency outside the United States?

This information is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

Taxpayer’s Advocate Report – Highlights Massive Gap (?) in U.S. Tax Compliance for Mexican Resident Individuals (Part I of II)

Few people think about how many individuals around the world should or must file U.S. tax returns? When must they file (if ever) when they reside predominantly outside the United States? What are the legal consequences under U.S. law for not filing? This post discusses the discrepancy between the number of individuals who should file tax returns and the actual number of returns filed, particularly focusing on individuals residing in Mexico.

In addition to income tax returns, when are estate or gift tax returns required to be filed under the law of the United States? These comments do not address this question, which will be addressed in a future post.

The 2023 report to Congress by the Taxpayer’s Advocate scratches the surface of this issue in her footnote 41, reported in Most Serious Problem #9. It reads as follows when talking about the number of competent tax return professionals residing outside the United States:

For example, Thailand, a country from which 7,409 individual income tax returns were filed in TY 2021, lists only five preparers, all but one in Bangkok. Mexico, a country from which 10,929 individual income tax returns were filed in TY 2021, lists only 23 preparers. See IRS, Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, https://irs.treasury.gov/rpo/rpo.jsf (last visited Dec. 18, 2023); IRS, CDW, IRTF, TYs 2016-2022 (through Sept. 28, 2023).

Mexico

Lawful Permanent Residency Population in Mexico (Emigrated from the U.S.)

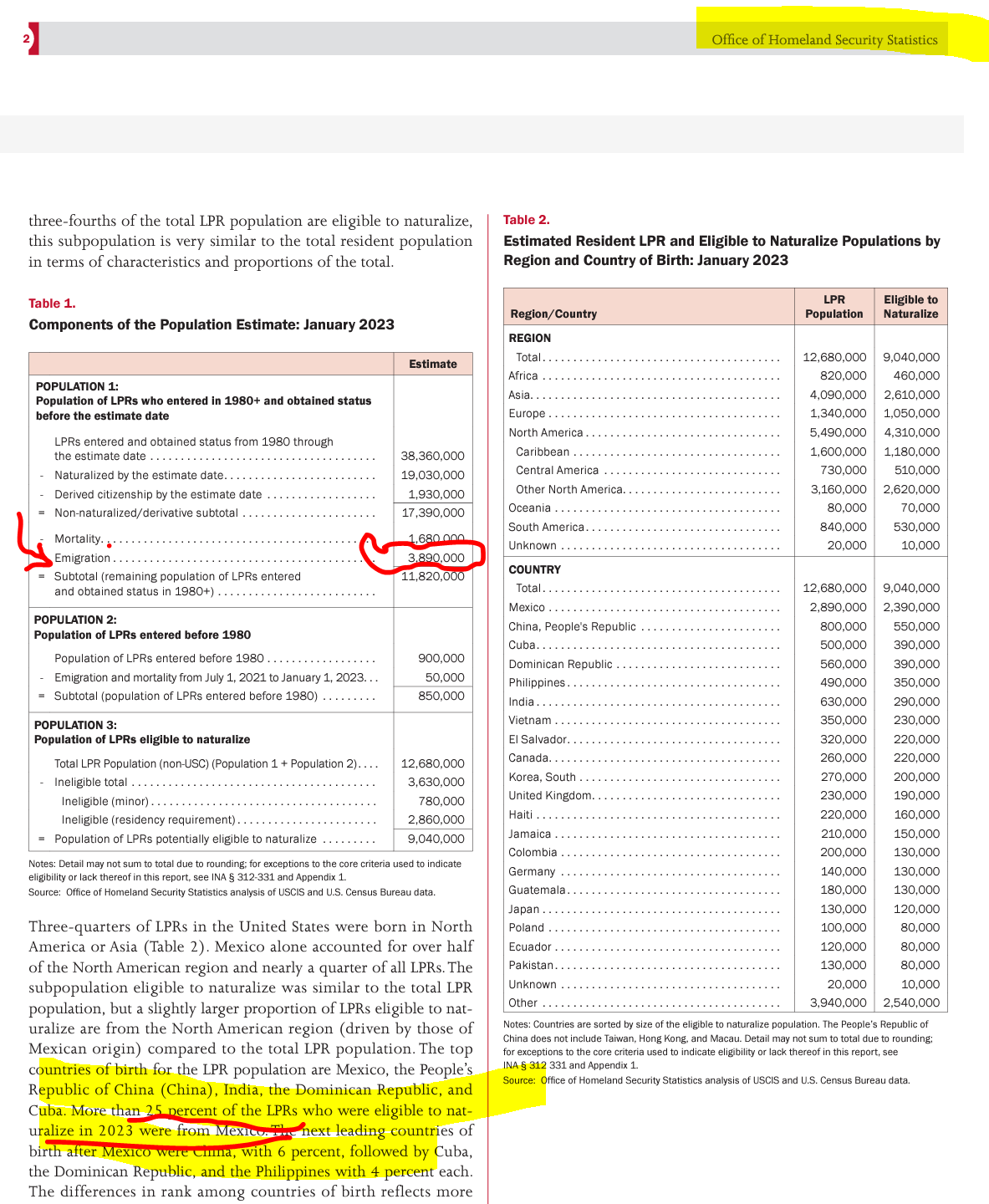

How can Mexico, with nearly 1 million Mexican residents estimated to be living outside the United States without formally abandoning their “lawful permanent residency” status, have only 10,929 tax returns filed from Mexico? The DHS Office of Homeland Security Statistics report estimates approximately 3.89 million LPRs have emigrated and now reside outside the U.S., with a significant portion being Mexican.

Given that around 25% of this group should on their face be United States persons (without applying the law in the U.S.-Mexico tax treaty), it raises questions about why there aren’t more Mexicans filing U.S. tax returns, many more? This does not even consider the U.S. citizen “expat” community who live in Mexico. Maybe a considerable number of the 10,929 tax returns filed from Mexico may actually originate from United States citizens working, residing, or retired in Mexico (so-called “expats”). The number of U.S. expatriates working and living in Mexico is a factor to consider, given the recent reports on thousands of U.S. citizens now working remotely from places such as Mexico City.

U.S. Citizen Population in Mexico

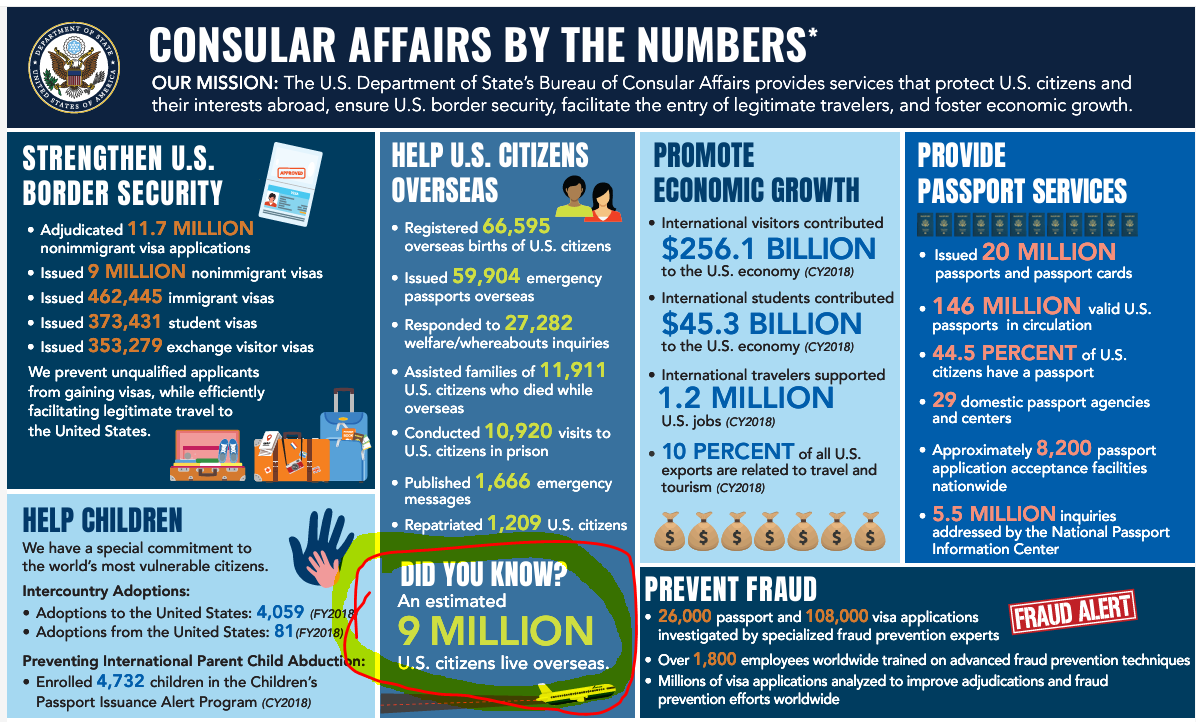

According to the U.S. Department of State, roughly nine million U.S. citizens reside abroad as of 2020. See, Most Serious Problem #9, p. 118 and Consular Affairs by the Numbers:

Given this substantial “expatriate population” (including Mexicans who are dual nationals and would never consider themselves as an “expatriate”; but are more of the “accidental American” type), the discrepancy between reported tax returns and potential filings becomes even more significant. It suggests a considerable underreporting of tax returns among U.S. citizens and LPRs living abroad, specifically in Mexico.

DHS Report: 3.89M Emigrated LPRs — Who Falls Under the Tax Treaty Escape Hatch?

Clear U.S. tax and legal relief now exists for a significant portion of the 3.89 million Lawful Permanent Residents (LPRs) who never formally abandoned their U.S. immigration status. This relief stems from two sources in the law:

(i) Tax treaty laws that apply to individuals residing in one of the 67 income tax treaty countries with the United States, recently including Chile.

(ii) Legal principles, recently confirmed by the Federal Court in Aroeste v. United States, that establish that individuals can apply tax treaty laws (when applicable) even if they missed certain filing deadlines set by the Internal Revenue Service. The Court termed this provision an “escape hatch,” allowing individuals, depending on specific circumstances, to be considered non-residents of the United States (not “United States persons”). This can be true under the relevant treaty, even if they never formally abandoned their LPR status.

The 2023 DHS report estimates that nearly 4 million individuals have emigrated from and left the United States and are now living somewhere around the world. Notably, Mexico constitutes the largest share at about 25% of the total LPR population who have left the United States.

The DHS report allows the reader to extrapolate that around 1 million individuals, similar to Mr. Aroeste, are living in Mexico and did not formally abandon their LPR status by filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

Aroeste v. United States is the third case I’ve litigated, examining whether individuals with a “green card” residing outside the United States in a tax treaty country are considered U.S. income tax residents. The previous two cases (involving Mexican and German citizens) didn’t progress to the oral argument stage; as the government conceded both before trial. See, IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

A FOIA response yielded surprising information; the government records indicate that only 46,364 Forms I-407 were filed from 2013 to 2015.

(Source: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ)

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

What can we glean from the DHS report and the LPR – I-407 information obtained through the FOIA response? There is a substantial gap in the millions; millions of individuals who have physically left the U.S. to reside elsewhere globally, compared to the relatively smaller number of tens of thousands who have officially filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

Conclusion

Importantly, now under the legal principles established in Aroeste v. United States, individuals residing in one of the 67 countries covered by an income tax treaty have specific legal relief from the worldwide reporting of income to the United States government.

The author has extensively discussed the appropriate IRS Form for individuals to sign under penalties of perjury when dealing with their banks and third parties, irrespective of the banks’ location. The choice between IRS Forms W-8 and W-9 hinges on the U.S. income tax residency status of the individual. Forms W-8 and W-9 serve the purpose of conveying the tax residency status of the individual to third parties. The correct (or incorrect form) can have a range of different tax and legal consequences to the individual. A non-resident is generally not subject to income taxation in the United States, except for on limited types of income. In contrast, a resident (for federal income tax purposes) is subject to taxation on their worldwide income. If an income tax resident of the United States falsely certifies their status using Form W-8, severe adverse legal consequences can follow. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

IRS Forms W-8 or W-9 (or Other)?

For U.S. citizens, the process is straightforward—they must sign IRS Form W-9. However, for individuals without U.S. citizenship, the situation becomes more intricate. The following posts delve into critical legal considerations surrounding IRS Form W-8BEN.

These comments provide in-depth insights into the legal consequences of filing and signing specific IRS forms (or their equivalents produced by financial institutions: W-8 vs. W-9). Notably, UBS’s explanation titled “UBS One Source Understanding tax forms—non U.S. taxpayers” sheds light on the efforts foreign financial institutions need to dedicate to assist clients who are not “United States persons” for federal tax purposes, ensuring compliance with U.S. federal tax laws.

Green Card Holders Living Abroad Have Further Analysis to Consider

The complexity heightens for “Green Card” holders living abroad, especially those residing in countries covered by an income tax treaty with the United States. See, Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. Aroeste v United States – Order Nov 2023, emphasizes a 5-step analysis for Green Card holders who have not formally abandoned their status. The ultimate test is whether the individual is entitled to be treated as a resident of a foreign country under a tax treaty.

Aroeste v. United States: Decision’s Impact on LPR Individuals

The decision could potentially affect millions of Green Card holders living outside the U.S. Aroeste Court’s 5-step analysis becomes crucial for the 3+ million LPRs residing abroad, determining whether they qualify as “United States persons” under the law.

LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers around 66 countries. The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan. Some have been cancelled.

Importance of Figuring Out your Residency Status if you Never Formally Abandoned your Green Card and Live in an Income Tax Treaty Country.

The impact of the Aroeste v United States decision presents a dual scenario for individuals who have not formally abandoned their “lawful permanent residency” status. On the positive side, there is an opportunity to inform the Internal Revenue Service (IRS) of their non-resident status by utilizing the applicable income tax treaty. There are specific steps to take as explained by the Court in Aroeste vs. United States. This action can relieve them of U.S. federal income tax filing obligations and Foreign Bank Account Report (FBAR) filing requirements, helping to steer clear of potential penalties and taxes that might otherwise be owed. The Court in Aroeste concluded such late filings could subject the individual ” . . . to penalties pursuant to I.R.C. § 6712(a) equal to $1,000 per failure to timely report his Treaty position. . . “

Potential Downside for “LPRs” Living in an Income Tax Treaty Country.

However, on the flip side, this termination of U.S. income tax residency status may lead to the individual “cease[ing] to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)).” Such a shift can trigger adverse U.S. tax consequences, affecting not only the individual but also extending to children, spouses, family members, and friends who could receive “covered gifts” or “covered bequests.” This classification may result in the individual being deemed a “covered expatriate” under the expatriation tax law, as outlined in IRC 877A(g)(3). See, IRC 877A(g)(3). Potentially severe adverse tax consequences can follow from this edge of the sword. The Court in Aroeste vs. United States did not address these adverse tax consequences as they were not at issue.

This Blog is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Blog.

Although the author has taken great care to make sure that the information contained herein is accurate and useful, it is necessary that you consult an experienced attorney to address any particular situation. Most importantly, if you are contemplating renouncing (or proving relinquishment) of U.S. citizenship or formally abandoning your LPR status, you must get legal advice. This is a very important decision with a range of complex legal consequences.

Dual Nationality has Been Permitted in the U.S.A. since 1967: U.S. Supreme Court Confirmed Constitutional Rights of Citizenship (Afroyim v. Rusk, 387 U.S. 253 (1967))

There is a common myth that still persists about U.S. citizenship. It is often stated (erroneously) that someone becoming a U.S. naturalized citizen must forsake citizenship to another country. Or a U.S. citizen becoming a naturalized citizen of another country must forsake U.S. citizenship. There are good reasons for this “myth.”

First, the federal government used to have a policy that discouraged (if not outright prohibited) nationality in another country while being a U.S. citizen in various circumstances. This despite the language in the 14th Amendment of the Constitution which provides in

relevant part:

“All persons born or naturalized in the United States, and subject to the jurisdiction thereof, are citizens of the United States and of the state wherein they reside. No state shall make or enforce any

law which shall abridge the privileges or immunities of citizens of the United States; nor shall any state deprive any person of life, liberty, or property, without due process of law; nor deny to any person within its jurisdiction the equal protection of the laws.“

Congress then imposed various restrictions on citizens and provided they would lose nationality in various circumstances. Specifically the Nationality Act of 1940 imposed a strict statutory rule that a:

” . . . national of the United States . . . shall lose their nationality by: . . . “(e) Voting in a political election in a foreign state” [since repealed]

Section § 401(e) of the Nationality Act of 1940

The Supreme Court in 1967 found that specific provision as violating the U.S. Constitution. In

that case, Mr. Afroyim was Polish born and become a U.S. naturalized citizen in 1926. The Court concluded he had voted in elections in Israel (after emigrating from the U.S. to Israel in 1950 – without formally renouncing his U.S. citizenship). The opinion of the Court concluded:

We hold that the Fourteenth Amendment was designed to, and does, protect every citizen of this Nation against a congressional forcible destruction of his citizenship, whatever his creed, color, or race. Our holding does no more than to give to this citizen that which is his own, a constitutional right to remain a citizen in a free country unless he voluntarily relinquishes that citizenship.

U.S. Supreme Court in Afroyim (1967)

The decision in Afroyim is in stark contrast to the earlier Supreme Court decision of Perez v. Brownell, 356 U.S. 44 (1958). In the earlier decision SCOTUS cited to the same 1940s Nationality Act – [Section § 401(e) of the Nationality Act of 1940]. The Court explained that the petitioner was born in the U.S. (unlike Afroyim who was born in Poland per the Court); explaining the individual was born in Texas, yet found that he lost his citizenship by voting in political elections in Mexico. The odd notion in Perez is that although he was born in the U.S. the Court referred to him as a “native-born Mexican citizen”. The key facts summarized by that Court were as follows:

Petitioner was born in Texas in 1909. He resided in the United States until 1919 or 1920, when he moved with his parents to Mexico, where he lived, apparently without interruption, until 1943. In 1928 he was informed that he had been born in Texas. At the outbreak of World War II, petitioner

knew of the duty of male United States citizens to register for the draft, but he failed to do so. In 1943 he applied for admission to the United States as an alien railroad laborer, stating that he was a native-born citizen of Mexico, and was granted permission to enter on a temporary basis. He returned to Mexico in 1944 and shortly thereafter applied for and was granted permission, again as a native-born Mexican citizen, to enter the United States temporarily to continue his employment as a railroad laborer. Later in 1944 he returned to Mexico once more. In 1947 petitioner applied for admission to the United States at El Paso, Texas, as a citizen of the United States. At a Board of Special Inquiry hearing (and in his

Mexico

subsequent appeals to the Assistant Commissioner and the Board of Immigration Appeals), he admitted having remained outside of the United States to avoid military service and having voted in political elections in Mexico. He was ordered excluded on the ground that he had expatriated himself; this order was affirmed on appeal. In 1952 petitioner, claiming to be a native-born citizen of Mexico, [356 U.S. 44, 47] was permitted to enter the United States as an alien agricultural laborer. He surrendered in 1953 to immigration authorities in San Francisco as an alien unlawfully in the United States but claimed

the right to remain by virtue of his American citizenship. After a hearing before a Special Inquiry Officer, he was ordered deported as an alien not in possession of a valid immigration visa; this order was affirmed on appeal to the Board of Immigration Appeals.

It does not seem that either Mr. Perez of Mr. Afroyam were much concerned about U.S. federal

tax consequences of their U.S. citizenship. Indeed, Mr. Perez was only a boy of about 10 years old when his parents left Texas to reside in Mexico where he remained for about 23 years before returning to the U.S. Afroyam tried to return to the U.S. apparently after his marriage failed in Israel.

Today, the U.S. Department of State articulates their policy and law of dual nationality for U.S. citizens seeking foreign citizenship. See, U.S. Department of State website:

U.S. law does not impede its citizens’ acquisition of foreign citizenship whether by birth, descent, naturalization or other form of acquisition, by imposing requirements of permission from U.S. courts or any governmental agency. If a foreign country’s law permits parents to apply for citizenship on behalf of minor children, nothing in U.S. law impedes U.S. citizen parents from doing so.

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this

{kind=link}