Bittner

Quaint?: U.S. Treasury 1998 Report: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues (Part I of Part II)

This is a classic report that now reads quaintly.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

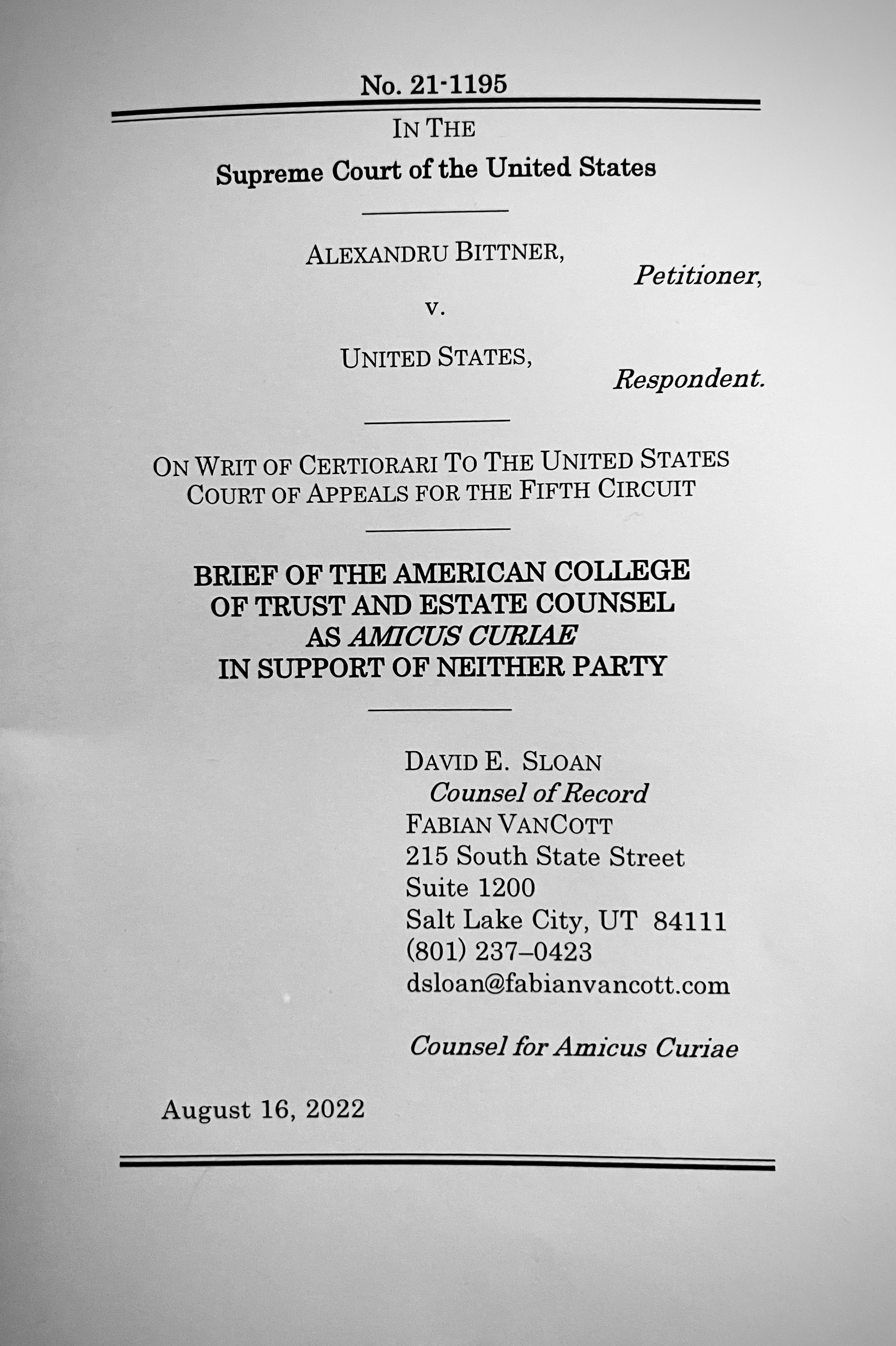

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties in United States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

More comments to come – in Part II.

2023: The Judiciary Takes Center Stage; Professor – Mindy Herzfeld’s article in Tax Notes International –

Professor Herzfeld has an excellent article posted the 18th of December 2023. You can access it here with a paid subscription – titled: 2023: The Judiciary Takes Center Stage. She has lots to cover regarding recent international tax law decisions by the U.S. federal courts (United States Tax Court, Federal District Courts & Court of Federal Claims).

- Tax Treaties

Professor Mindy Herzfeld discusses our recent case Aroeste v United States – Order (Nov 2023), which I have discussed at some length in recent posts. See, Federal District Court Rules in Favor of Mexican Citizen – Aroeste vs. United States (LPR) – Tax Treaty Applies: Government’s Motion for Summary Judgment is Denied. It was a pleasure for me to represent Mr. Aroeste over several years and see the favorable outcome of the federal district court that obligates the government to respect the terms of substantive tax treaty law.

She covers Christensen v. United States, which is another tax treaty case regarding the ability to take a foreign tax credit against the Section 1411 tax on net investment income; authored by Judge Marion Blank Horn of the Court of Federal Claims. Judge Horn is no stranger to important international tax issues. She authored the 2002 decision of Estate of Jack vs. United States regarding “domicile” for U.S. estate tax purposes and the impact of the Canadian decedent’s visa status. More recently the Estate of Margaret J. Jones vs. the United States (2022) was a lengthy case of Judge Horn’s denying the Estate a refund. This Estate of Margaret J. Jones is also Canadian citizen (decedent) case; but addressed a very different issue – re: the 5% “miscellaneous offshore penalty” she paid that is identified by the IRS’ rules they created in the “Streamlined Domestic Offshore Procedures” instructions (it is not a treaty case).

- TCJA, U.S. Trade or Business – SCOTUS & Moore

The Professor also addresses Moore v. United States (which she has written about before) and Altria Group Inc. v. United States and the subpart F rules under the TCJA.

The recent U.S. Tax Court (USTC) case of YA Global Investments LP v. Commissioner, is discussed by Professor Herzfeld regarding U.S. trade or business activities. Of course, another key USTC case regarding Section 6038 penalties is reviewed which has been appealed by the government – Farhy v. Commissioner. See, Six Weeks, Three International Information Reporting Decisions –

The SCOTUS decision near and dear to my heart (as I personally worked on the ACTEC amicus brief) of Bittner v. United States, is also reviewed briefly by Professor Herzfeld. In that case the SCOTUS held penalties are limited to $10,000 per year for a non-willful violation of the statute (not $2.72 million as the government asserted based upon each account).

She reviews some important transfer pricing cases Coca-Cola Co. v. Commissioner and 3M Co. v. Commissioner.

Do read Professor Herzfeld’s article when you get a chance. More details about her background and how to follow her is set out below:

Mindy Herzfeld is professor of tax practice at University of Florida Levin College of Law, counsel at Potomac Law Group, and a contributor to Tax Notes International. Follow Mindy Herzfeld (@InternationlTax) on X, formerly known as Twitter.

Never in my 30 year career practicing international tax law have I seen the judiciary so active in international tax matters – particularly when you take into consideration various SCOTUS cases.

Federal Court Determines IRS “Guidance for Expatriates Under Section 877A” – IRS Notice 2009-85: “Is Not Binding Authority”

The Federal District Court made numerous key legal findings in its Order on November 20, 2023; in Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. One of the more significant findings was that IRS Notice 2009-85 is not binding authority. This blog is dedicated to tax expatriation related matters under U.S. law.

- IRS Notice 2009-85 is Not Binding Authority per the Court

See, Federal District Court Rules in Favor of Mexican Citizen – Aroeste vs. United States (LPR) – Tax Treaty Applies: Government’s Motion for Summary Judgment is Denied. Please read through the case in detail.

The author along with his Chamberlain Hrdlicka, Attorneys at Law colleagues have been representing Mr. Aroeste throughout this District Court case. The author of tax-

expatriation.com has represented him for several years throughout the IRS audits and the on-going U.S. Tax Court cases along with his wife.

While many may consider this case to be a Title 31/FBAR case (which it is), it has greater ramifications under the tax expatriation laws in the author’s view. The finding by this Court regarding IRS Notice 2009-85 is significant with far reaching implications. The IRS Notice 2009-85 is broad in its scope and is more than 60 pages in length. It notes that, “Section 877A(i) provides that the Secretary shall prescribe such regulations as may be necessary or appropriate to carry out the purposes of section 877A.” (p.4)

- No Treasury Regulations Ever Issued – After 15 Years of IRS Notice 2009-85

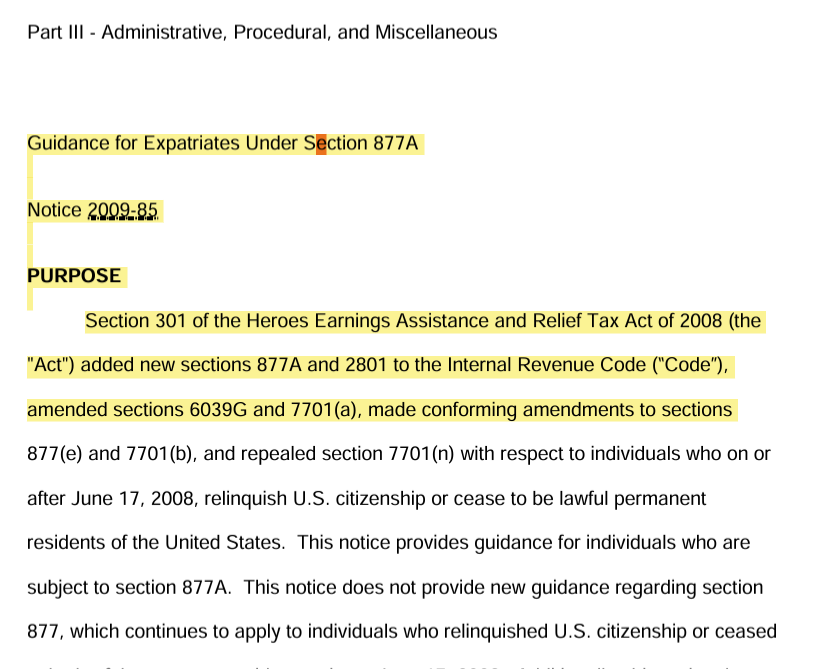

The Treasury Department never issued regulations under 877A, which is now 15 years old. The notice provides the historical background as follows:

Notice 2009-85 PURPOSE Section 301 of the Heroes Earnings Assistance and Relief Tax Act of 2008 (the “Act”) added new sections 877A and 2801 to the Internal Revenue Code (“Code”), amended sections 6039G and 7701(a), made conforming amendments to sections 877(e) and 7701(b), and repealed section 7701(n) with respect to individuals who on or after June 17, 2008, relinquish U.S. citizenship or cease to be lawful permanent residents of the United States. This notice provides guidance for individuals who are subject to section 877A.

IRS Notice 2009-85., p. 1.

The Court in Aroeste concluded that Mr. Aroeste ceased to be a lawful permanent resident.

Specifically, the Court finds Aroeste . . . ceased to be treated as a lawful permanent resident of the United States because he commenced to be treated as a resident of Mexico under the Treaty, did not waive the benefits of such Treaty, and notified the Secretary of the commencement of such treatment.

Aroeste v. United States, p. 17.

- Case Law from – Aroeste v. United States_- Clarifies Key Concepts in the Law

Many practitioners have questioned the accuracy and validity of many of the conclusions asserted in the 2009 notice; such as the timing of when someone becomes a “covered expatriate”. How and why they become a “covered expatriate” by the concepts introduced in the 2009 notice. The multiple examples presented, reflecting various tax outcomes according to the IRS, were never commented on by the public.

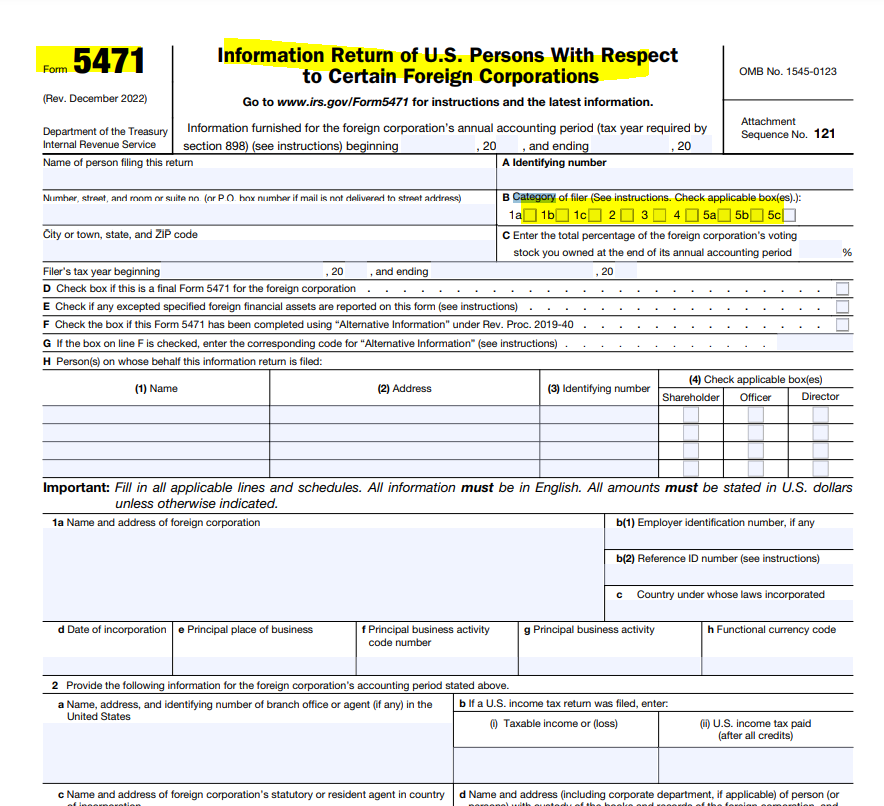

Another question many have raised is the effectiveness of IRS Form 8854? Throughout the notice, the IRS uses the word “must” some 88 times regarding the individual who ceased to be a U.S. citizen or a “lawful permanent resident” (or in some instances references to third parties). Does the IRS imply that if any of these “must”/conditions imposed under the notice are not satisfied, the individual is necessarily a “covered expatriate” with the adverse tax consequences that might follow?

Are their other adverse tax consequences that might follow? For instance, can the IRS repeatedly assert international information penalties regarding the individual’s

- companies in her own country,

- beneficiary rights of a trust or an estate in her own country, or

- other investment assets or financial accounts in her country of residence that might be deemed a “specified foreign financial asset” if the individual is a United States person”?

Can the IRS in perpetuity assert such information penalties regarding other code sections such as 6038D, 6038, 6039F, 6048, etc.? See, Three Precedent Setting Cases in International Information Reporting (“IIR”) in 6 Weeks: * Aroeste, * Bittner, and * Farhy: all Interconnected via Title 26, Title 31 and U.S. Income Tax Treaties

For instance, the 2009 notice provides that a “covered expatriate” must file a “dual status return” and file a Form 1040NR with a 1040 attached as a schedule for the “year of expatriation”. See, IRS Notice 2009-85, p. 49.

The IRS goes on to say in that notice that individuals “must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation.” Id., p. 50. The government asserts that if this condition is not satisfied, the individual will necessarily be treated as ” . . . covered expatriates within the meaning of section 877A(g) whether or not they also meet the tax liability test or the net worth test.“

These would be pretty damning consequences to an individual, if they otherwise met the statutory test of certifying compliance with the tax laws for the preceding five years.

Importantly, the Court in Aroeste v. United States concluded as a matter of law that 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). It concluded Mr. Aroeste did not need to file Form 8854 with his amended returns. He had filed Form 8833 – treaty based reporting.

The court cited to ” . . . Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.”

None of these comments represent legal advice. Complex laws applied to specific facts require a legal expert to opine on the consequences and recommended courses of action. It is worth noting that individuals who have a “green card” and who have not previously articulated the application of a U.S. income tax treaty, should consider taking proactive steps to protect their rights under the law. Also, United States citizens who formally renounced their citizenship, who may never have taken specific tax reporting positions should consider taking proactive steps to help avoid the risk the IRS might assert substantial penalties or conclude the individual became a “covered expatriate”.

Tax Notes International: Article by Robert Goulder: FBAR Madness: We need to Chat About Aroeste

On Monday 11 Sept 2023, Robert Goulder wrote a detailed article about the implications of what he calls “The Green Card From Hell”! His article can be reviewed in its entirety through the subscription service provided by Tax Notes International – FBAR Madness: We Need to Chat About Aroeste.

Goulder made some key observations that are worth repeating for anyone who has been a green card holder for basically more than seven years. That can trigger the “expatriation” tax provisions – the focus of this blog.

The facts of the case of Mr. Alberto Aroeste are covered extensively and accurately in Goulder’s article.

He noted:

This week’s article concentrates on the novel FBAR issue that will be decided in Aroeste v. United States, an illegal exaction suit before the U.S. District Court for the Southern District of California.7 The case has garnered attention for good reason. It pushes back against the government’s dubious policy of requiring individuals treated as nonresidents under a U.S. tax treaty to provide FBAR filings. Let’s note the futility of the financial information which the government seeks from these folks. It concurrently exempts treaty nonresidents from the need to file IRS Form 8938 (“Statement of Specified Foreign Financial Assets”), the tax code’s counterpart to the FBAR.8 It remains problematic that the government should demand reporting from treaty nonresidents as if they were residents.9

Goulder – FBAR Madness: We Need to Chat About Aroeste.

The one issue not explained well relates to how and when lawful permanent residency (i.e. a “green card”) under Title 8 is even valid in the first place. Goulder’s article explains some of the rights of lawful permanent residency status, but also addresses some key areas of the immigration law the same as most tax law experts cover a different area of the law. See, SCOTUS’ observations of the law in this context: Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

For instance, Goulder claims green card holders cannot be deported as long as the immigration status remains valid. True – but what is not explained is how easy it is to cease to have a valid one in the first place. What he doesn’t explain is how and when an individual can “abandon” or “relinquish” the status as a green card holder (as a matter of law) by not residing permanently in the United States. See, Fundamentals of Immigration Law, written by Charles A. Wiegand, III, Former Immigration Judge, Oakdale, Louisiana. The law is complex as described by Wiegand.

Goulder does not seem to find the government’s arguments persuasive (“ain’t buying it“!):

For Aroeste, there seems to be little doubt his closer personal and economic ties are with Mexico. The IRS knows this. An analysis conducted by an IRS agent concluded that he spent no more than 67 days in the United States during 2012 and 57 days in the United States in 2013, with three-quarters of the remaining time spent in Mexico.

Goulder –

The IRS doesn’t care where Aroeste had closer personal and economic ties. That’s because it doesn’t care about the tiebreaker. As the government sees it, the treaty is a distraction that has no meaningful role to play in this litigation. The plaintiff’s immigration status is conclusive, end of story. His green card settles the matter, such that all further inquiries are superfluous and should cease.

Id.

What bothers me about that argument is how the government’s position selectively wishes away the existence of the U.S. tax treaty network — but only for application of the FBAR regime. The Mexico treaty would still mean something in another context, but not on the pivotal issue of Aroeste’s status as a U.S. person for FBAR purposes. Sorry, I ain’t buying it.

Id.

The government argues the treaty is only relevant for income and excise tax purposes, and what we have here are penalties based on violations of the Bank Secrecy Act — not the Internal Revenue Code. As the government sees it, no plaintiff can successfully challenge penalties authorized by Title 31 with legal remedies based on Title 26. I’m still not buying it.

Id, Goulder

I would recommend you take a read through his article that also addresses a discussion on how the government prefers to keep internal memoranda from the eyes of the public. He discusses at some length – Tax Analysts and Coastal States. How the Court in Aroeste took an approach different from the D.C. Circuit in articulating 9th Circuit law regarding attorney client privileged documents in the possession of the government.

Three Precedent Setting Cases in International Information Reporting (“IIR”) in 6 Weeks: * Aroeste, * Bittner, and * Farhy: all Interconnected via Title 26, Title 31 and U.S. Income Tax Treaties

In just over six weeks, there have been three key judicial precedents favorable to international individuals. These cases have helped clarify the requirements of individuals and the limitations on the powers of the IRS in assessing IIR penalties. Please see the full article on tax notes. These IIR decisions relate to:

- Title 31 penalties for Foreign Bank Account Reports (“FBARs”),

- Title 26 IIR penalties specific to reporting of ownership interests in foreign companies [and “reportable events” with foreign trusts[1]], and

- How these two federal statutory regimes of Title 31 and 26 crossover into international law as set forth in U.S. income tax treaties negotiated with different countries around the world.

Each of these three cases are interconnected and have significant impact to individuals with global lives, global assets, multi-national family members and those who have businesses or accounts in different parts of the world.

- Aroeste v. United States

First, on February 13th, 2023, the Southern District of California District Court (the “District Court”) made a key determination in a Joint Discovery Motion decision in Aroeste.[2] The District Court concluded in Aroeste that the IRS/DOJ[3] could not ignore the U.S.-Mexico income tax treaty (“Treaty”) and its application to a Mexican national who has resided almost all of his life in Mexico City and has maintained a “green card” for immigration purposes in the United States. It is a non-willful FBAR case. The District Court applied the interconnected statutes and regulations of Titles 31 and 26 to help determine who qualifies as a “United States person”; specifically with reference to international law and obligations set forth in the Treaty. The key question in that case that remains to be answered is who (specifically Mr. Aroeste and by extension to a pool of millions of green card individuals residing outside the United States who are not citizens[4]) must file FBARs?

Second, on February 28th, 2023, the Supreme Court of the United States (“SCOTUS”) resolved in Bittner[5], that the applicable non-willful FBAR penalty is not measured by every foreign account of the individual as the Service has argued for years. That case also dealt with non-willful filing of FBARs and the SCOTUS concluded the IRS cannot impose penalties of $10,000 on each and every account held; but rather the penalty is “per report” that was not correctly filed. Hence, the total maximum penalty per year is $10,000. A maximum penalty of $50,000 (x5 years) applied per the SCOTUS versus the IRS determined amount of US$2.7M+.

- Farhy v. Commissioner

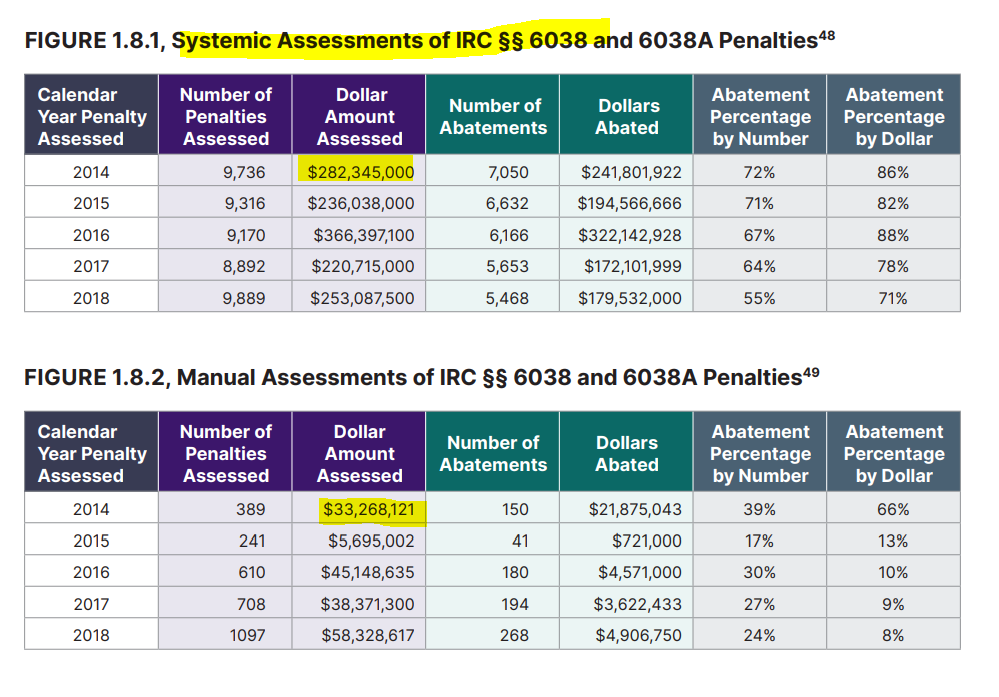

Lastly, on April 3rd, 2023, the United States Tax Court (the “Tax Court”) issued a decision in Farhy,[6] stating that the IRS does not have statutory authority to assess IIR penalties under section 6038(b). The IIR that is required by this statute is IRS Form 5471, which includes multiple filing categories. This has far reaching implications about how the government will be able to collect the IIR penalties the Service administratively determines are owed.[7] The Taxpayer Advocate previously issued a report on point titled: The IRS’s Assessment of International Penalties Under IRC §§ 6038 and 6038A Is Not Supported by Statute, and Systemic Assessments Burden Both Taxpayers and the IRS[8] In that report, the Taxpayer Advocate identified more than $310M of penalties just for the tax year 2014 the IRS “assessed” under Sections 6038 and 6038A.[9] We now know these “assessments” were invalid.

[1] See, footnote 19 regarding United States Tax Court’s Order in the case of Alberto Aroeste & Estela Aroeste vs. Commissioner.

[2] No. 22-cv-682-AJB-KSC, 2023 BL 46094 (S.D. Cal. Feb. 13, 2023).

[3] The “IRS” or the “Service” are used as shorthand for the Internal Revenue Service; and the Department of Justice; Tax Division is referred to as the “DOJ.”

[4] See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year and 4.8 million are estimated to have died and/or emigrated. The authors have extrapolated from these estimates in the report to conclude that more than 3 million of these individuals have emigrated and left the United States. The millions of individuals do not reside in the U.S. of which Mr. Aroeste is one of these individuals; although a tax treaty must exist in the country of residence for the analysis of the District Court in Aroeste v. United States to be applicable.

[5] No. 31—1195 (U.S. Feb. 28, 2023); 598 U. S. ____ (2023); The majority opinion by Justice Gorsuch cited to the ACTEC amicus brief (where Patrick W. Martin, the author of tax-expatriation.com and a fellow of ACTEC worked on the drafting of the brief) and concluded:

“Best read, the BSA treats the failure to file a legally compliant report as one violation carrying a maximum penalty of $10,000, not a cascade of such penalties calculated on a per-account basis.” The ACTEC brief was cited by the majority opinion- “ We see evidence, too, that the point of these reports is to supply the government with information potentially relevant to various kinds of investigations, criminal and civil alike. But what we do not see is any indication that Congress sought to maximize penalties for every nonwillful mistake (whether a late filing, a transposed account number, or an out-of-date bank address). See Brief for American College of Trust and Estate Counsel as Amicus Curiae 5–7.”

[6] 160 T.C. No 6 (April 3, 2023).

[7] See, Patrick W. Martin, Megan L. Brackney, Robert Horowitz, and Javier Diaz de Leon Galarza: Problems Facing Taxpayers with Foreign Information Return Penalties, November 12, 2020.

[8] See, Annual Report to Congress 2020 (pp 119-131), citing – Robert Horwitz, Can the IRS Assess or Collect Foreign Information Reporting Penalties? TAX NOTES TODAY (Jan. 31, 2019) 301-305; Erin Collins and Garrett Hahn, Foreign Information Reporting Penalties: Assessable or Not? TAX NOTES TODAY (July 9, 2018) 211-213 and 2 Frank Agostino and Phillip Colasanto, The IRS’s Illegal Assessment of International Penalties, TAX NOTES TODAY (Apr. 8, 2019) 261-269.

[9] Id., See, Figures 1.8.1, Systemic Assessments of IRC §§ 6038 and 6038A Penalties & 8.2, Manual Assessments of IRC §§ 6038 and 6038A Penalties.