International Tax · Citizenship Renunciation · LPR Abandonment

International Tax Shareholder

World Cup & Playing in the United States: Green Card Holders, the Treaty Tiebreaker, and the Global Athlete or Entertainer

As the world’s athletes have arrived to perform on U.S. soil, the U.S. tax system is a broad net. The 2026 FIFA World Cup—hosted across the United States, Mexico, and Canada—is a useful occasion to revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

This blog is dedicated to issues of “tax expatriation” which crosses into different professions and global lifestyles. See, for instance the following prior blogs:

There are of course many famous athletes who were not U.S. citizens and then became green card holders and oftentimes then became naturalized U.S. citizens. Since the Knicks just won the NBA championship after 53 years, one of their greatest, Patrick (mi tocayo) Ewing left Jamaica as a boy, became a green card holder and then a naturalized citizen. A 1985 New York Times article, A Favorite Son Goes Home, describes his first return to the island since a boy.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

Athletes and entertainers are specially taxed in the U.S. in the sense they typically receive few benefits from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

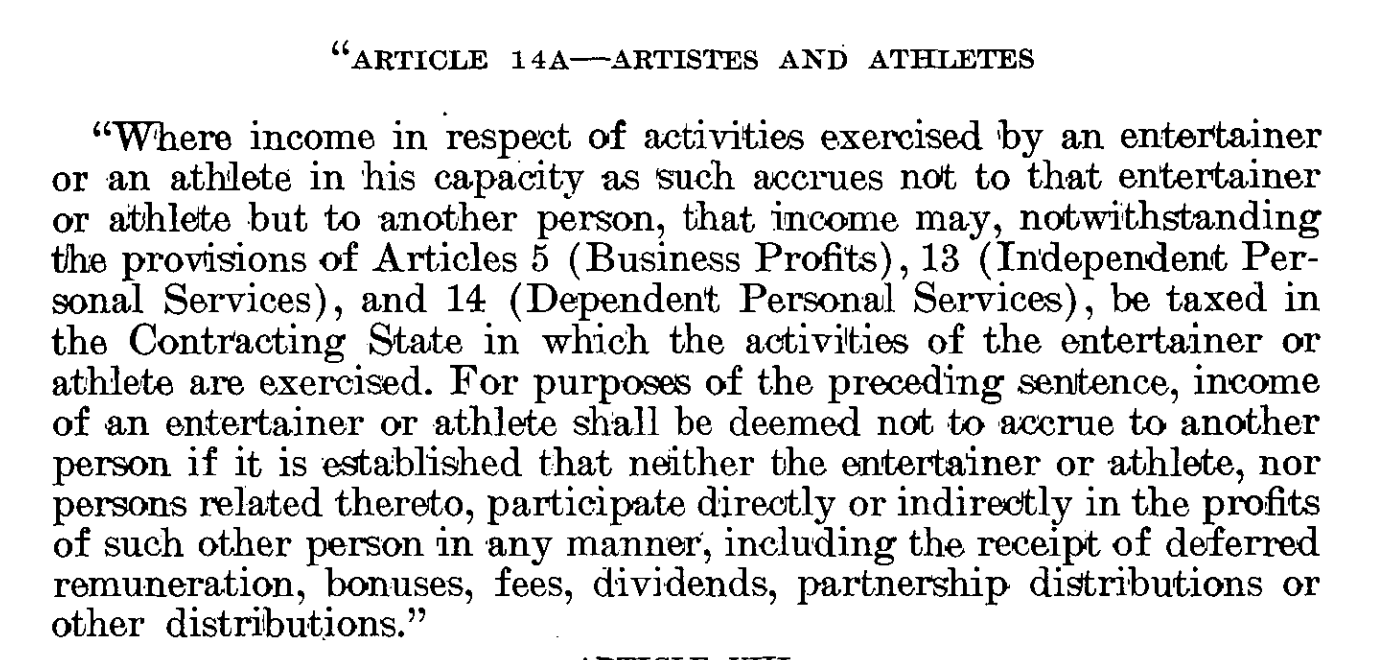

A protocol to the treaty adopted in 1980 has a “new” article 14A specific to artists and athletes as reflected here in its entirety allowing the government to tax athletes and entertainers when they perform in the country (overriding other protective provisions of the treaty – e.g., Business Profits Art. 5, Independent Personal Services Art. 13 and Dependent Personal Services Art. 14):

The IRS also adopted a specific program, called the Central Withholding Agreement (“CWA”) program created by Revenue Procedure 89-47 specific to artists and athletes. I personally think it is a program that is not authorized by the statute and often applied by the IRS in a manner that violates the withholding tax regime we have in Chapter 3 of our statutory tax law, Subtitle A. In practice, third parties are subject to the 30% withholding tax on certain gross proceeds paid to companies other than the artist or athlete, if the athlete or artist doe not participate with the IRS in their CWA.

Mexico

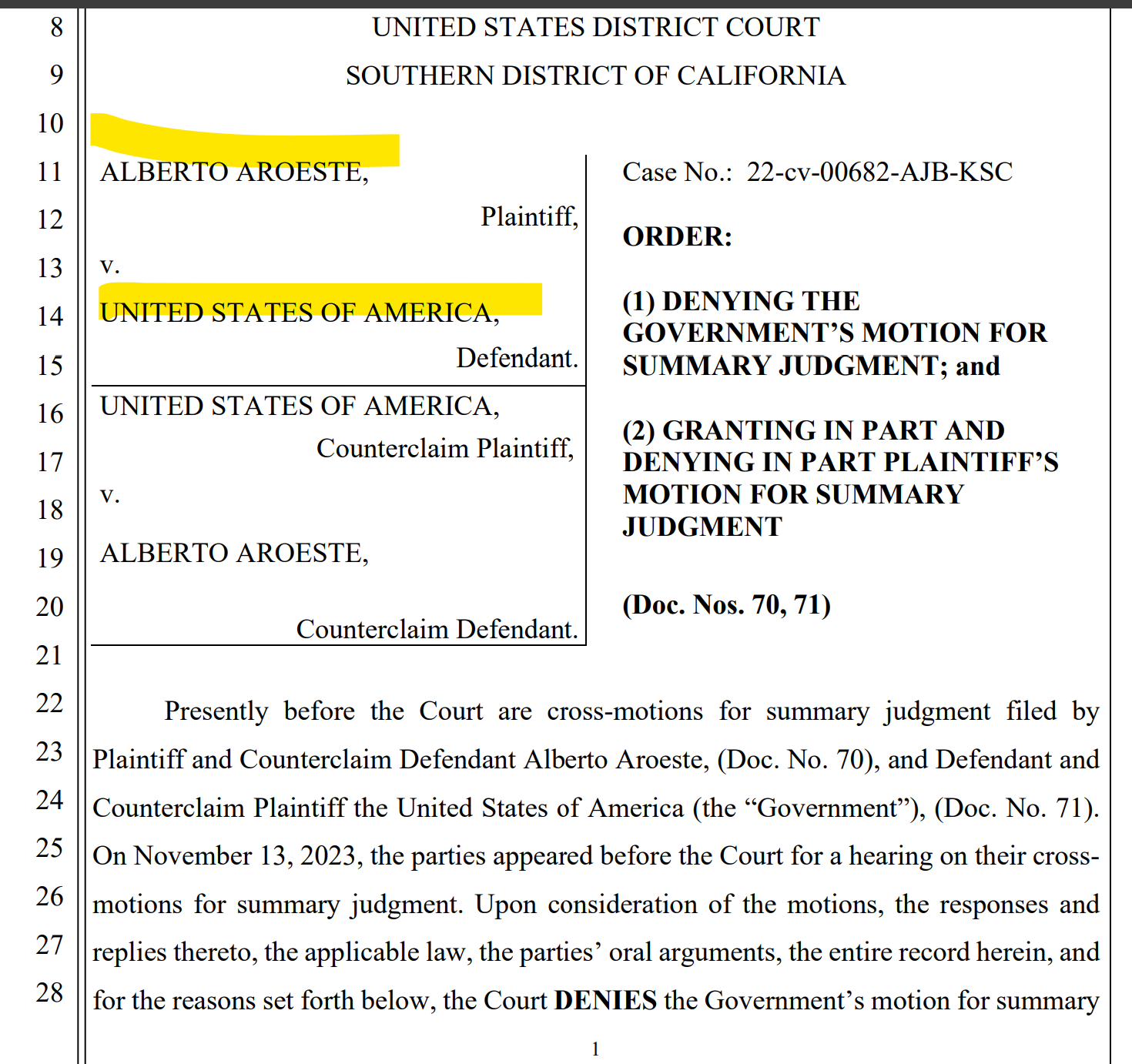

In the case of global soccer players, even one with a “lawful permanent resident” card (i.e., a “green card”) they may be subject to the Chapter 3 withholding tax rules if the athlete is like Mr. Aroeste (Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC)) holding a green card in his pocket, but not a U.S. income tax resident by application of the residency rules set forth in an income tax treaty. Will the soccer player become a “covered expatriate” and not even know it (oops)?! It can get tricky quickly.

Meanwhile, Mexico and the U.S. have both advanced to the knockout round.

Canada plays Switzerland and presumably has a 99% chance of advancing to the Round of 23.

Form W-8 or W-9? Why the Wrong Choice Could Cost Green Card Holders Abroad

The choice between Form W-8 and Form W-9 comes down to one thing: your U.S. tax residency status, not your immigration status. Green card holders living abroad may be able to sign Form W-8 under a U.S. income tax treaty, but picking the wrong form means signing a false statement under penalty of perjury. And claiming treaty benefits carries a risk that many people never see coming. Consulting an experienced attorney before signing anything is essential.

What is the difference between Form W-8 and Form W-9?

Both forms tell your bank or financial institution whether you are a U.S. tax resident or not. Form W-9 is for U.S. residents, who must pay U.S. taxes on income they earn anywhere in the world. Form W-8BEN is for non-residents, who generally only pay U.S. taxes on certain types of income that come from U.S. sources. The form you sign has real legal consequences, not just administrative ones.

What happens if you sign the wrong form?

Signing either form is a certification made under penalties of perjury. If you are a U.S. tax resident and you sign Form W-8, you are making a false statement, and serious legal consequences may follow.

Why is this more complicated for green card holders living abroad?

U.S. citizens always sign Form W-9, with no exceptions. For everyone else, it depends on tax residency status. Green card holders are generally treated as U.S. tax residents even while living in another country, which would normally mean they sign Form W-9. But there is an important exception: if the country where they live has an income tax treaty with the United States, they may be able to claim non-resident status under that treaty and sign Form W-8 instead.

The United States has 58 income tax treaties that together cover 66 countries. That includes the 1973 U.S. and U.S.S.R. income tax treaty, which still applies today to nine former Soviet republics: Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

What did the court decide in Aroeste v. United States, and why does it matter?

Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC) is a federal court decision that established a 5-step analysis for green card holders who have not formally given up their green card but are living abroad. The key question the court addresses is whether a green card holder qualifies to be treated as a resident of a foreign country under an applicable U.S. income tax treaty. This ruling matters for the more than 3 million LPRs who are living outside the United States.

What are the benefits of successfully claiming non-resident status under a treaty?

If a green card holder qualifies as a non-resident under a tax treaty, they may be able to stop filing U.S. federal income tax returns on their worldwide income. They may also no longer be required to file the Foreign Bank Account Report, known as the FBAR, which would help them avoid the significant penalties that come with missing that filing. The court in Aroeste laid out the specific steps required to make this claim correctly.

One important note: if you claim non-resident status under a treaty but fail to report that treaty position to the IRS on time, you face a separate penalty under IRC Section 6712(a) of $1,000 for each failure to timely file. Claiming treaty status correctly and reporting it on time are both required.

What is the risk on the other side?

Claiming treaty-based non-resident status may also legally end your U.S. tax residency. Under IRC Section 7701(b)(6), this shift may cause you to cease to be a lawful permanent resident of the United States. That change may trigger the U.S. expatriation tax rules under IRC Section 877A(g)(3), which could classify you as a covered expatriate. The Aroeste court did not address these consequences because they were not part of that case, but they are real and potentially serious.

What does covered expatriate status mean for your family?

Covered expatriate status does not only affect you. If your family members or friends in the United States later receive gifts or an inheritance from you, they may owe U.S. tax on those transfers under the covered gift and covered bequest rules. This may affect children, spouses, and anyone else who would receive something from you.

Do you need an attorney before making this decision?

The answer depends on which country you live in, which treaty applies, the value of your assets, and your long-term plans. Getting it wrong may trigger exit taxes, affect your family’s inheritance, and have consequences that cannot easily be undone. This post explains the framework but is not a substitute for legal advice specific to your situation.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

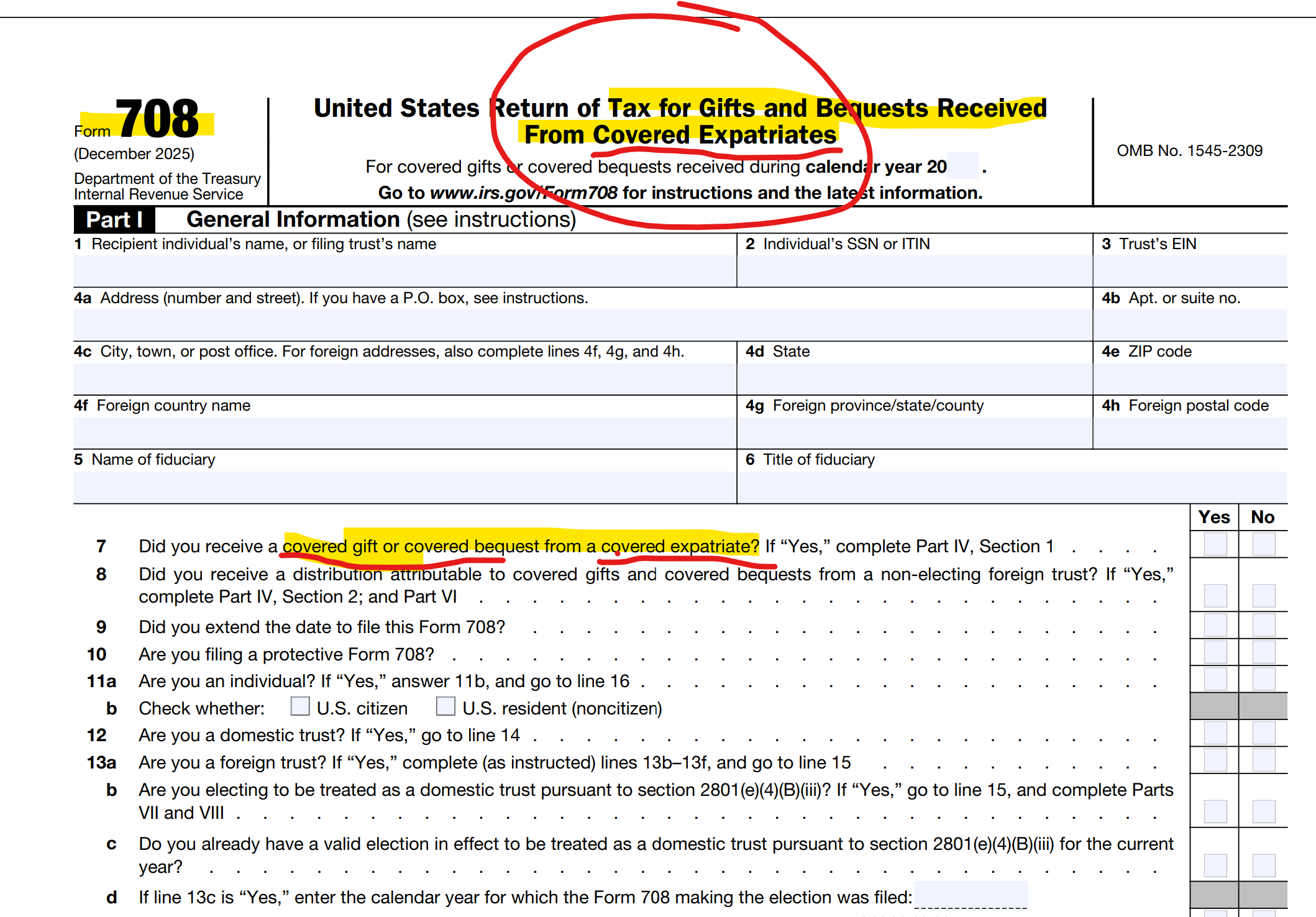

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

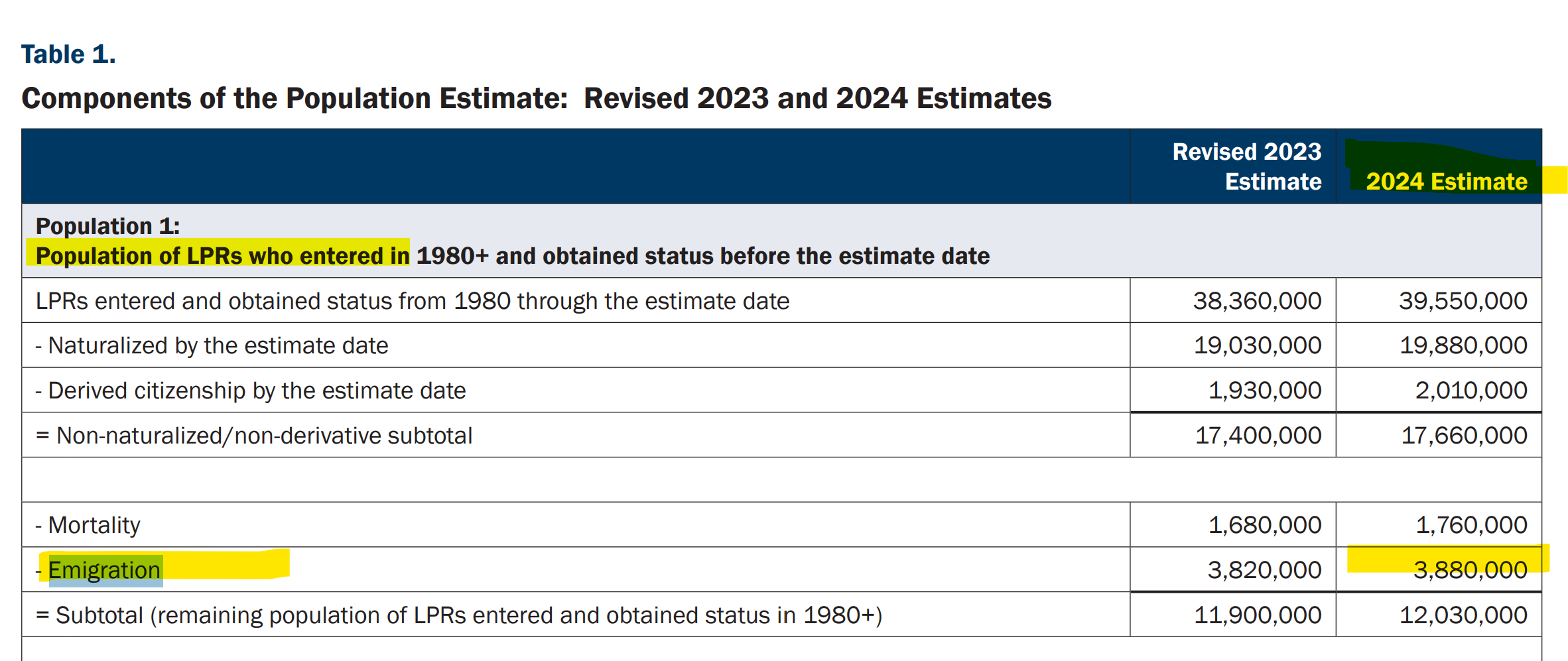

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Part I of Part II: The Gold Card – “It’s like the green card, but better and more sophisticated.”

Will the “gold card” sell to ultra high net worth investors around the world who want U.S. citizenship (“USC”)? What are the tax costs of USC? * About the Author: Patrick W. Martin

President Trump again announced on April 3, aboard Air Force One his plan:

Whether the U.S. adopts a new “Gold Card” “For $5 million [that] we will allow the most successful job-creating people from all over the world to buy a path to U.S. citizenship,” is up to the U.S. government.

Congress can amend Title 8 and include a new “Gold Card” option.

Current law provides the EB-5 visa as one path towards a “green card” that ultimately can lead to U.S. citizenship through naturalization.

President Trump presented at his March 4th speech to a joint session of Congress, explaining the concept: “It’s like the green card, but better and more sophisticated. And these people will have to pay tax in our country.”

Sounds like a panacea to help the U.S. federal deficit problem? If 100,000 of these “Gold Cards” were sold for $5M each, and these funds were paid directly over to the federal government, that would raise $500 billion dollars. If 1 million were sold, that would be $5 trillion dollars to use to pay down the deficit (running annually at far greater than $1 trillion dollars since 2019).

To put that into perspective, the EB-5 visa that also leads to a “green card” that can further lead to U.S. citizenship through naturalization has an annual visa limit of about 10,000. See, USCIS’s article – (16 Aug 2024) – Annual Limit Reached in the EB-5 Unreserved Category There have been multiple years where the annual visa limit was not met. Prior to 2015, the 10,000 visa limit was never met and in several years there were less than 500 EB-5 visas issued annually.

There have been less than 150,000 EB-5 visas issued over the last 35 years since its adoption in 1990. Is it realistic to be able to “sell” even ten thousand $5M gold visas annually, when the “green EB-5 visa” costs $800,000 and has had less than 150,000 issued in nearly 35 years?

Equity Investment for EB-5 visa – $800,000 (Does NOT go to the Government)

The total required equity investment amount for an EB-5 visa in the qualifying project, is only $800,000 (if in a “TEA”). See, EB-5 Immigrant Investor Program, as published by the U.S. Citizenship and Immigration Services (USCIS). See, USCIS’s Chapter 2 – Immigrant Petition Eligibility Requirements. It used to be only $500,000 (1/10th of $5M). A TEA is a targeted employment area (“TEA”) that meets specific requirements under the law. If the capital investment is not in a TEA, the required minimal capital investment amount is $1,050,000 that increases in January 1, 2027 and each 5 years thereafter. Still about 1/5th the cost of a “gold visa”.

U.S. Estate and Gift Tax Consequences for U.S. Citizens and those with a Green Card (“Gold Card”?)

Finally, maybe the biggest impact on who wants an investor visa that leads to U.S. citizenship depends largely upon the U.S. income tax and U.S. estate and gift tax consequences. There are many tax implications. See, my case Aroeste v United States – Order Nov 2023, that was appealed to the 9th Circuit by the Office of Solicitor General (DOJ). U.S. District Court ruled in favor of green card holder.

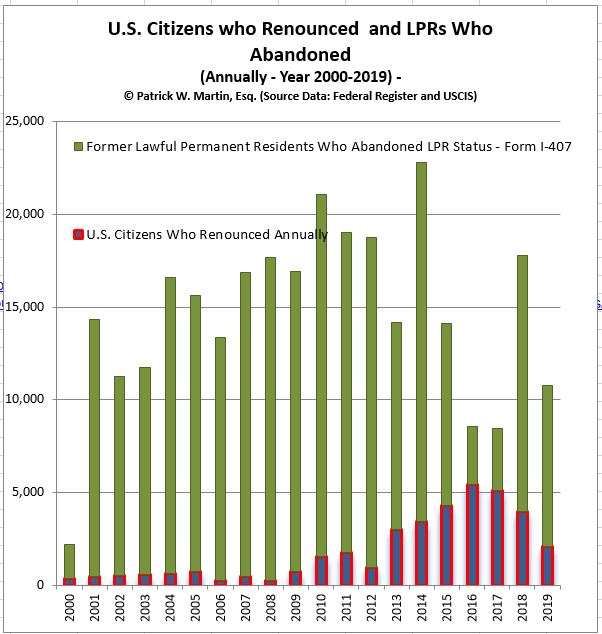

Does TIGTA have the Answer: to the Question – How many former U.S. citizens and long-term lawful permanent residents have filed and should have filed IRS Form 8854?

The short answer to the question above – is NO!

The government does not know how many IRS Forms 8854 should have been filed.

Note the total numbers of 8854 returns filed as reported in Figure 2 of the TIGTA Report were less than 25,000 during a ten year period. This report focuses really only on former U.S. citizens (“USC”) who have renounced their citizenship. Not on lawful permanent residents (“LPRs), which during that same ten year period there were around 200,000 who filed USCIS Form I-407.

* How Many Individuals Should have Filed Form 8854?

Quaint?: U.S. Treasury 1998 Report: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues (Part I of Part II)

This is a classic report that now reads quaintly.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties inUnited States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

How Many LPRs are Living in Tax Treaty Countries like Aroeste (Now including Chile)? What are the Legal-Tax Consequences? (Part I of II)

No, not talking about Texas-Style Chili as reported in the – NYT Cooking Recipe.

Chile, the country in South America and the newest country to have an income tax treaty go into force with the United States. The U.S.-Chile Tax Treaty (in the works for more than a decade) went into force at the end of 2023, on 19 December 2023.

The question is how many “LPRs” are residing in a tax treaty country that are impacted favorably (presumably all of them) by the federal district court decisions we successfully handled against the IRS and DOJ, Tax Division: Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)?

As previously explained, the Aroeste decision will affect potentially millions of “Green Card” holders (a subset of the 3.89M estimated by the government) living outside the U.S. Those who have not formally abandoned their lawful permanent residency status. See, “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – (2020). This “LPR Tax Limbo” is no longer the case after the Aroeste decision.

These individuals who are living in tax treaty countries are not in “LPR Tax Limbo” any more since the Court clarified when the individual is not a United States tax resident. The Court explained, that filing a “late” tax treaty position, does not cause the non-U.S. citizen to have waived the benefits of the income tax treaty. It is the tax treaty with each of the 66 countreis that has the potential of unlocking the “escape hatch” described by the Court.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

The court in Aroeste outlined a 5-step analysis that becomes crucial for the 3.89 million LPRs residing abroad in one of the 66 tax treaty countries, in determining whether they are “United States persons” under the law. This will be covered in Part II.

Millions of LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in November 2023 as of 2014 (until the Chile treaty came into effect). The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importantly, anyone in these circumstances would be remiss, if they did not consider carefully the “mark to market” tax implications to them if they were to become a “covered expatriate” as defined in the law. These “mark to market” tax consequences can have potentially devastating consequences, including to U.S. beneficiaries in the future if not properly planned and considered.

Immigration Forms, I-407; I-485, Application to Register Permanent Residence or Adjust Status & Tax Forms, 1040, 1040NR, 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114, etc. etc. (Part I of III)

The U.S. tax law is complex, including when an individual (i) becomes and (ii) ceases to be, a U.S. income tax resident (USITR). USITR is not a technical term used under the tax law. The U.S. tax and information reporting requirements are very different depending the status of an individual. Anyone who is not a United States citizen, is either a –

“Resident alien“, or a

“Nonresident alien” as the tax law defines both of these categories.

You can’t be both.

“Resident aliens” are generally also “United States persons” (both technical terms in the federal tax law).

“Non-resident aliens” as defined are necessarily not “United States persons.”

Being one versus the other has huge U.S. tax and reporting consequences.

An individual who is a “lawful permanent resident” as referenced in the tax law (Section 7701(b)(6)) cross-references the U.S. immigration law. The first requirement of that statutory tax rule in § 7701(b)(6)(A)) is that “(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws [such status not having changed]. . .[emphasis added]” This means the tax definition is dependent upon the immigration laws, which are found in Title 8, Immigration and Nationality Act. Importantly, the last part of that sentence (i.e., [such status not having changed] is a requirement in the immigration law (Title 8), but does not appear in the tax definition.

The term “lawful permanent resident” cannot be found in Title 8 as a noun or object (i.e., the individual). Instead, the immigration law defines the status of a person in 8 U.S. Code § 1101(a) as follows:- “. . . (20) The term “lawfully admitted for permanent residence” means the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed.“

This analysis is fundamental to be able to determine whether an individual who holds a “green card” in their pocket even has the status of being “lawfully admitted for permanent residence. . . such status not having changed.” It’s a fundamental legal question under immigration law that must be answered first, to then be able to answer the tax question.

Each form an individual files or does not file (e.g., IRS tax form 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114; and immigration forms, e.g., I-485, I-407, etc.) can have a potential impact on the tax residency status of an individual.

The immigration law and when forms, such as Form I-485, Application to Register Permanent Residence or Adjust Status are submitted to the U.S. federal government can have an impact on this determination. The government can use it against the individual as they did unsuccessfully in Aroeste (see below – Pages 9 and 11 of 17); asserting that Mr. Aroeste waived the treaty by not submitting certain forms.

The entire case from the Federal District Court can be read here: Aroeste v. United States, 22-cv-00682-AJB-KSC (20 Nov. 2023):

The tax residency analysis for those who have kept their “green card” in their pocket, can be even more complex as was analyzed by the Court. There are additional provisions of the law that must be considered including old Treasury Regulations that pre-date many provisions of various U.S. income tax treaties.

For instance, each of the following federal tax statutory rules, which will be considered in more detail in later posts (II and III):

Additional posts will review the impact of these provisions in the law and how various immigration forms (including I-485 and I-407, Record of Abandonment of Lawful Permanent Resident Status) and tax forms (including 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858) and FinCEN form 114, can impact the determination of whether someone who has a “green card” in their pocket is or is not a United States person.

revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card? Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute. from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

expatriate” and not even know it (oops)?! It can get tricky quickly.

expatriate” and not even know it (oops)?! It can get tricky quickly.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —