The FBAR (the Foreign Bank Account Report) comes from a different law than the federal income tax. The income tax sits in Title 26 of the U.S. Code. The FBAR comes from the Bank Secrecy Act, which is Title 31. These two laws are very different, with very different obligations and rights. One of the important differences is the time frame in which the government can assess penalties for not complying.

Who has to file an FBAR?

By its expansive terms, which some would call extraterritorial, the FBAR law applies to U.S. citizens residing outside the U.S. It also applies to most LPRs (lawful permanent residents, or green card holders) residing outside the U.S. Many of these people are unaware the rules reach them.

What is a statute of limitations for these penalties?

A statute of limitations is the time frame in which the government has to assess penalties for not complying with the law. For foreign accounts, these time periods are not the same under Title 31 (the Bank Secrecy Act) as they are under Title 26 (the income tax law). The gap between the two is what makes this area confusing.

Is there a time limit for the IRS to assess income tax if a return was never filed?

No. When a U.S. citizen or LPR residing overseas fails to file an income tax return, the time period for the IRS to make tax assessments never lapses. There is effectively no statute of limitations against the IRS in that situation. The clock to assess does not start until a return is filed.

How long does the government have to assess civil FBAR penalties?

Title 31, the Bank Secrecy Act, is different. It does have a time period that runs against the U.S. federal government, even if the FBAR was never filed. For civil assessments of penalties, that time period is 6 years.

Can someone be criminally liable for not filing an FBAR?

Yes. A U.S. citizen or LPR living overseas could become criminally liable for willfully not filing the FBAR form. Criminal liability carries different legal consequences than a civil penalty. The key word is willfully, which separates a criminal matter from a civil one.

How is the FBAR filed now?

All FBARs must now be filed electronically. The form is not filed with the IRS. It is filed with FinCEN (the Financial Crimes Enforcement Network), on Form 114, Report of Foreign Bank and Financial Accounts, through the BSA E-Filing System website. The electronic Form 114 supersedes TD F 90-22.1, the paper FBAR form used in prior years.

Can the U.S. collect FBAR penalties in the filer’s home country?

Not always. The laws of many countries outside the U.S. often conclude that enforcing these FBAR penalties against a U.S. citizen, inside that person’s home country, violates the laws of that country. Canada is one example. Calgary based tax attorney Roy Berg has written on the question of whether the IRS can collect FBAR penalties under the Canada-US Treaty.

Is there a statute of limitations for criminal FBAR charges?

Yes, there are also statutes of limitations for criminal charges the government brings for FBAR violations. The law gets much more complex here, especially when the taxpayer is residing outside the U.S. In that situation, the time period can be tolled or suspended in favor of the government, which extends the window to bring charges. Jack Townsend has written on the statutes of limitations for FBAR noncompliance related to tax noncompliance.

Understanding State Income Taxes and Global Tax Planning for Expatriates (Part I of II)

Assets and income earned in high tax states such as California and New York, are taxed very differently compared to low-tax states such as Texas, Nevada, Florida or Tennessee. Focusing on “expatriation” (e.g., renouncing USC or abandoning LPR status) of the individual might be misplaced if the person wants to live mostly in the United States. See earlier post, Form 8854 Filing: TIGTA Report Reveals Compliance Gap

Countries From Which Viewers Read Posts – Tax-Expatriation.com – First Week of 2024 (Which Ones are Tax Treaty Countries?) – Applying the “Escape Hatch”

The whole idea of the “escape hatch” for tax treaties is an excellent way of explaining how and when tax treaty law applies in different circumstances. Importantly, the U.S. federal government cannot deny an individual (or presumably a company either) from properly applying the law of a tax treaty – even if they “gave [an] untimely notice of his treaty position “. See further comments at the end of this post and the District Court’s opinion here – Aroeste v United States – Order (Nov 2023). Meanwhile, see below the 22 countries from where global readers viewed Tax-Expatriation.comduring the first full week of 2024.

Below is the list of 22 countries (including the United States) from where readers hailed, who read Tax-Expatriation.comduring the first week of 2024. All, but Brazil, Croatia, Nigeria, the United Arab Emirates, Colombia, Kenya and Bermuda have income tax treaties with the United States.

This means that all other individuals are connected with the following 14 countries that have tax treaties with the United States:

Mexico

India

Canada

United Kingdom

Switzerland

Australia

China

Spain

Turkey

Germany

Japan

Romania

Portugal

Netherlands

Further, all individuals who might have never formally abandoned their lawful permanent residency (“green card”), maybe never filed specific IRS tax forms, and yet reside in one of these fourteen (14) treaty countries could be eligible for the application and the specific benefits of international income tax treaty law. This, along the lines of the decision in Aroeste v United States (Nov. 2023). In addition, there could be other tax treaty benefits applicable to those individuals in these fourteen countries depending upon where are their assets, what type of income they have, where does the income come from, and where do they reside.

The tax treaty rights discussed here are established by law, as elucidated by the Federal District Court in Aroeste v United States (Nov. 2023). The Court determined that the IRS cannot simply assert an individual’s ineligibility for treaty law provisions based solely on the failure to file specific IRS forms within the government-defined “timely” period. The Court emphasized that there is no automatic waiver of treaty benefits as a matter of law, while acknowledging: “. . . Aroeste gave untimely notice of his treaty position. . .” For specific excerpts from the opinion, please refer to the highlighted portions below. To access the complete opinion, please consult Aroeste v United States – Order (Nov 2023).

* * * * * * * * *

B. Whether Aroeste Did Not Waive the Benefits of the Treaty Applicable to Residents of Mexico and Notified the Secretary of Commencement of Such Treatment.

To establish Mexican residency under the Treaty, and thus avoid the reporting requirements of “United States persons,” Aroeste must have filed a timely income tax return as a non-resident (Form 1040NR) with a Form 8833, Treaty-Based Return Position Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2722 Page 8 of 17 9 22-cv-00682-AJB-KSC Disclosure Under Section 6114 or 7701(b). Indeed, Aroeste did not submit Form 8833 to notify the IRS of his desired treaty position for the years 2012 and 2013 until October 12, 2016, when he submitted an amended tax return for both years at issue. (Id.) The Government asserts that because Aroeste did not timely submit these forms, he cannot establish that he notified the IRS of his desire to be treated solely as a resident of Mexico and not waive the benefits of the Treaty. (Id. at 4.) The Government relies upon United States v. Little, 828 Fed. App’x 34 (2d Cir. 2020) (“Little II”), a criminal appeal in which the court held a lawful permanent resident of a foreign country was a “‘resident alien’ or ‘person subject to the jurisdiction of the United States’ with an obligation to file an FBAR.” Id. at 38 (quoting 31 C.F.R. § 1010.350(a), (b)(2)).

In response, Aroeste asserts that while he agrees with the Government that I.R.C. § 6114 requires disclosure of a treaty position, he disagrees as to the consequences for a taxpayer’s failure to timely file the disclosure. (Doc. No. 75-1 at 6.) While the Government asserts the failure to timely file Forms 1040NR and 8833 deprives individuals of the Treaty benefits provided, Aroeste argues instead that I.R.C. § 6712 provides explicit consequences for failure to comply with § 6114. Specifically, § 6712 states that “[i]f a taxpayer fails to meet the requirements of section 6114, there is hereby imposed a penalty equal to $1,000 . . . on each such failure.” I.R.C. § 6712(a). Based on the foregoing, Aroeste argues the taxpayer does not lose the benefits or application of the treaty law.1 (Doc. No. 75-1 at 6.) In United States v. Little, 12-cr-647 (PKC), 2017 WL 1743837, at *5 (S.D. N.Y. 1 Aroeste further asserts that published agency guidance, letter rulings, and technical advice support his position. (Doc. No. 75-1 at 7.) For example, in 2007, an IRS agent sought advice from IRS Counsel asking, “Do we have legal authority to deny a tax treaty because Form 8833 is not attached or the treaty is claimed on the wrong Form (1040EZ or 1040)?” Legal Advice Issued to Program Managers During 2007 Document Number 2007-01188, IRS. IRS Counsel responded, “No, you cannot deny treaty benefits if the taxpayer is entitled to them. You may impose a penalty of $1,000 under section 6712 of the Code on an individual who is obligated to file and does not.” Id. As to this, the Court finds it has no precedential value under I.R.C. § 6110(k)(3), which states that “a written determination may not be used or cited as precedent.” See Amtel, Inc. v. United States, 31 Fed. Cl. 598, 602 (1994) (“The [Internal Revenue] Code specifically precludes [plaintiff] and the court from using or citing a technical advice memorandum as precedent.”) Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2723 Page 9 of 17 10 22-cv-00682-AJB-KSC May 3, 2017) (“Little I”), a criminal case for the plaintiff’s willful failure to file tax returns, the court stated the plaintiff’s same argument “that the failure to take a Treaty position can result only in a financial penalty also lacks merit. 26 U.S.C. § 6712(c) expressly states that ‘[t]he penalty imposed by this section shall be in addition to any other penalty imposed by law.’” (emphasis added).

I have been consulted over the years by other taxpayers which are cited now as published decisions by the government and the Federal District Court (Southern District of California). These cases are referenced and cited in my own most recent case of Aroeste v United States (Nov. 2023).

However, in Little I, the plaintiff never attempted to take a treaty position. Next, in Shnier v. United States, 151 Fed. Cl. 1, 21 (2020), the court denied the plaintiffs’ claims for relief based on tax treaties because they failed to disclose a treaty based position on their tax returns pursuant to I.R.C. § 6114 “and did not attempt to cure this omission in their briefing[.]” Although the plaintiffs in Shnier were naturalized U.S. citizens who attempted to recover their income taxes under I.R.C § 1297, the court’s brief discussion of I.R.C. § 6114 in relation to a treaty-based position is instructive that an untimely notice of a treaty position does not bar the individual from taking such position. Moreover, in Pekar v. C.I.R., 113 T.C. 158 (1999), the court noted that a taxpayer who fails to disclose a treaty-based position as required by § 6114 is subject to the $1,000 penalty, but stated “there is no indication that this failure estops a taxpayer from taking such a position.” Id. at 161 n.5.2 The Court agrees with Aroeste.

Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

* * * * * * * * *

For individuals living in any of these 14 tax treaty countries (or any of the total 67 income tax treaty countries), the key takeaway is that, based on their specific circumstances, they might be eligible to leverage the international tax treaty principles outlined in the Aroeste v United States case (Nov. 2023). The forthcoming post will pose questions for consideration by the potentially millions of individuals affected by these rules of law.

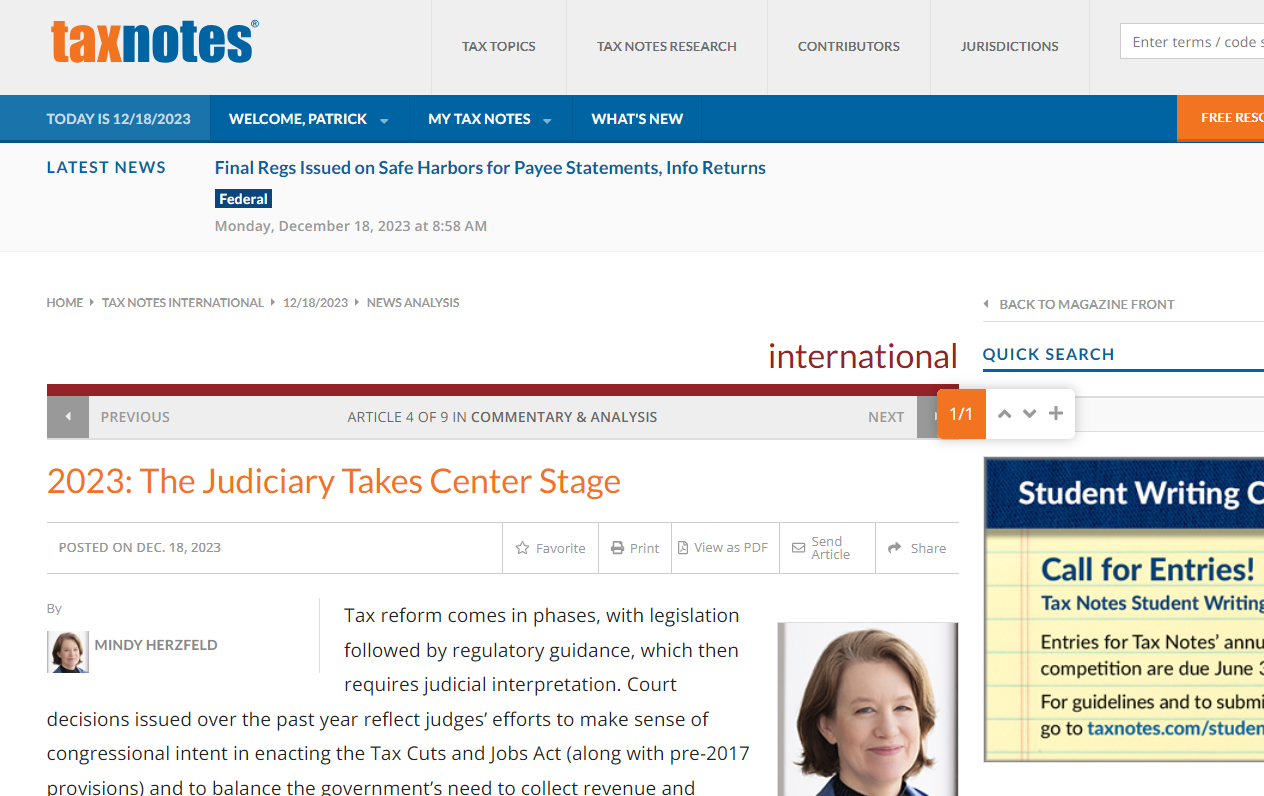

2023: The Judiciary Takes Center Stage; Professor – Mindy Herzfeld’s article in Tax Notes International –

Professor Herzfeld has an excellent article posted the 18th of December 2023. You can access it here with a paid subscription – titled: 2023: The Judiciary Takes Center Stage. She has lots to cover regarding recent international tax law decisions by the U.S. federal courts (United States Tax Court, Federal District Courts & Court of Federal Claims).

She covers Christensen v. United States, which is another tax treaty case regarding the ability to take a foreign tax credit against the Section 1411 tax on net investment income; authored by Judge Marion Blank Horn of the Court of Federal Claims. Judge Horn is no stranger to important international tax issues. She authored the 2002 decision of Estate of Jack vs. United States regarding “domicile” for U.S. estate tax purposes and the impact of the Canadian decedent’s visa status. More recently the Estate of Margaret J. Jones vs. the United States (2022) was a lengthy case of Judge Horn’s denying the Estate a refund. This Estate of Margaret J. Jones is also Canadian citizen (decedent) case; but addressed a very different issue – re: the 5% “miscellaneous offshore penalty” she paid that is identified by the IRS’ rules they created in the “Streamlined Domestic Offshore Procedures” instructions (it is not a treaty case).

TCJA, U.S. Trade or Business – SCOTUS & Moore

The Professor also addresses Moore v. United States (which she has written about before) and Altria Group Inc. v. United States and the subpart F rules under the TCJA.

The recent U.S. Tax Court (USTC) case of YA Global Investments LP v. Commissioner, is discussed by Professor Herzfeld regarding U.S. trade or business activities. Of course, another key USTC case regarding Section 6038 penalties is reviewed which has been appealed by the government – Farhy v. Commissioner. See, Six Weeks, Three International Information Reporting Decisions –

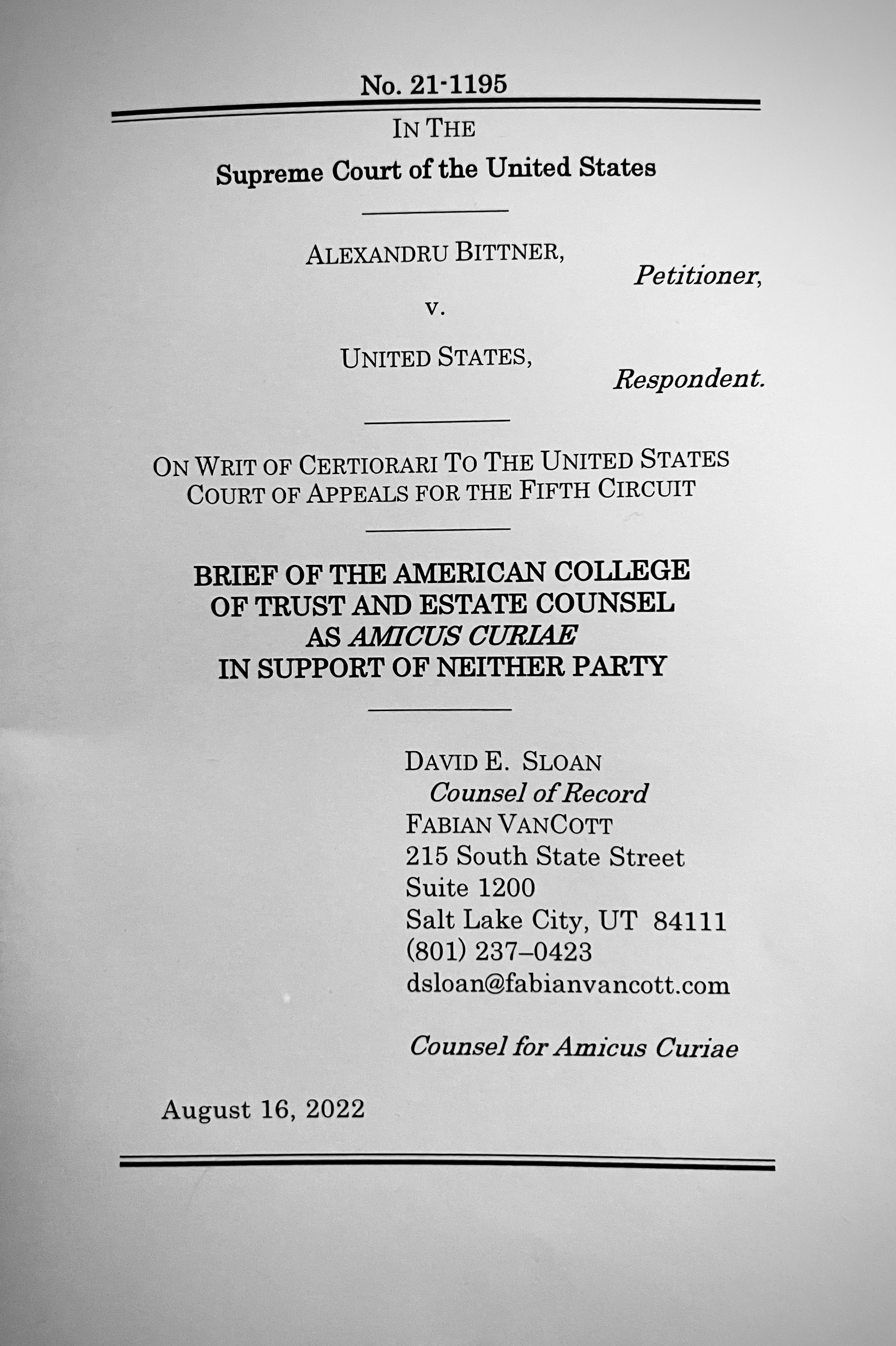

The SCOTUS decision near and dear to my heart (as I personally worked on the ACTEC amicus brief) of Bittner v. United States, is also reviewed briefly by Professor Herzfeld. In that case the SCOTUS held penalties are limited to $10,000 per year for a non-willful violation of the statute (not $2.72 million as the government asserted based upon each account).

She reviews some important transfer pricing cases Coca-Cola Co. v. Commissionerand 3M Co. v. Commissioner.

Do read Professor Herzfeld’s article when you get a chance. More details about her background and how to follow her is set out below:

Mindy Herzfeld is professor of tax practice at University of Florida Levin College of Law, counsel at Potomac Law Group, and a contributor to Tax Notes International. Follow Mindy Herzfeld (@InternationlTax) on X, formerly known as Twitter.

Never in my 30 year career practicing international tax law have I seen the judiciary so active in international tax matters – particularly when you take into consideration various SCOTUS cases.

Why Sir Paul McCartney would have to give up his Knighthood – if he were to become a U.S. Citizen?

Successful athletes, singers, writers, actors, artists and other talented individuals from outside the United States rarely consider becoming a U.S. citizen unless they plan on living permanently in the U.S. for the rest of their lives. The reason can often be found in how the U.S. federal tax regime (particularly estate and gift taxes) can apply on their worldwide assets and worldwide income. These talented individuals typically generate income from around the world, most every major country and therefore will have business and investment interests around the world.

A non-citizen artist or entertainer can usually enter into the U.S. for performances and employment opportunities on a range of visa options. For instance, many of these individuals can typically get an O-1 visa, because of their extraordinary abilities.

The petitioner must provide evidence demonstrating your extraordinary ability in the sciences, arts, business, education, or athletics, or extraordinary achievement in the motion picture industry.

Back to British knighthoods and damehoods. British nationals can receive these honors from the British Crown, as did Paul McCartney from the Queen in 1997. Individuals who are British nationals and citizens of commonwealth countries (e.g., Canada, Australia and New Zealand) are eligible for these UK Honors. However, it appears that U.S. citizens (who are not also nationals of the UK or a commonwealth country), will not be eligible for these formal UK honors. There are many honorary UK honors granted to various U.S. citizens over the last several decades, including –

Why Most LPRs Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets (Part I)

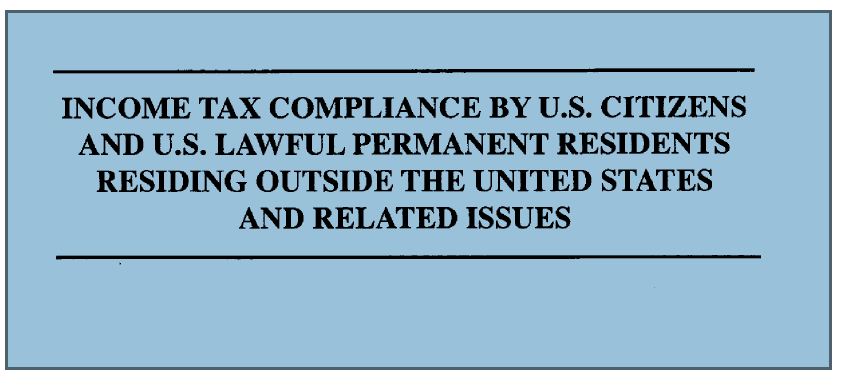

1998 Report from Department of Treasury to Chairman of House Committee on Ways and Means

Whether you have a “foreign bank account” for instance, is not intuitive, if you reside principally in a country outside the U.S. In other words, the accounts one may have in their country of tax residency (e.g., Germany, Canada, U.K., India, the U.S., Denmark, Mexico, etc.) will not seem like a “foreign bank account” at all. Rather, it is an account in a financial institution in their country of residency, i.e. a “domestic account.” Similarly, a U.S. bank account for an LPR residing outside the U.S. will intuitively seem like a “foreign bank account.” This is just one counter-intuitive example. Others will be explored in subsequent posts – e.g., “foreign corporations” and “foreign partnerships” among others.

There is a particularly formal way of abandoning LPR status, which is by filing Form I-407, Record of Abandonment of Lawful Permanent Resident. The very instructions to the form imply that it is not the only way to abandon – as the form ” . . . is designed to provide a simple procedure to record an individual’s abandonment . . . “

To complicate the law further, Treasury regulations provide for the so-called “green card test” – but do not contemplate the application of an income tax treaty for which we have nearly 70 with various countries:

(1) Green card test. An alien is a resident alien with respect to a calendar year if the individual is a lawful permanent resident at any time during the calendar year. A lawful permanent resident is an individual who has been lawfully granted the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws. Resident status is deemed to continue unless it is rescinded or administratively or judicially determined to have been abandoned.

Treas. Reg. § 301.7701(b)-1(b).

To review the nearly 70 income tax treaties with different countries, they can be reviewed on the IRS website – United States Income Tax Treaties – A to Z – The application of these treaties to LPRs will be explored in later posts. Incidentally, no where on the actual “green card” is there express reference to tax obligations as exists on the back page of a U.S. passport.

I will leave you with an excerpt from the 1998 report referred to above starting on page 14:

” . . . Other factors also operate to limit both compliance measurement and improvement. Because the United States asserts taxing jurisdiction over those with little or no connection to the United States other than citizenship or status as a lawful permanent resident, in many cases overseas U.S.taxpayers are difficult to trace or contact. Moreover, even when valid tax assessments can be made against overseas taxpayers, IRS has limited enforcement recourse if the taxpayer’s assets are physically located outside of the United States. In addition, persons may be unaware of their status as U.S. taxpayers with an obligation to file a U.S. tax return. As described in Section II.B, supra, IRS has undertaken various taxpayer education initiatives to increase awareness of filing and payment obligations. In some cases, however,education may not be sufficient. For example, an individual who was born outside the United States and has never even visited the country may, nevertheless, be a U.S. citizen by reason of his parents’ U.S. citizenship. Such a person may not even know that he is a U.S. citizen and thus likely will not know of his obligation to file a U.S. tax return. Similarly, the United States imposes tax on greencard holders who no longer reside in the United States but who have not surrendered their greencards. Although the immigration laws may no longer recognize the validity of the green card if the holder attempted to reenter the country, and the individual may no longer consider himself entitled to lawful permanent resident status, the individual [generally] remains subject to U.S. tax under the Code.[emphasis added along with clarifying language in brackets]

Importantly, no where throughout all of this extensive 1998 report is there even a mention of the foreign bank account reporting obligations. Imagine, the Treasury never once in their report explained how and to what extent FBAR reporting applied to these taxpayers – even-though the ” . . . report responds to section 513 of the Health Insurance Portability and Accountability Act, Pub. L. 104-191, which directs the Secretary of the Treasury to prepare a report that describes income tax compliance by U.S. citizens and lawful permanent residents residing outside the United States . . . “

The “965 Hammer” (aka the “Transition” or “Repatriation” Tax) for USCs Residing Overseas

Small businesses around the world commonly operate through companies established in their country of operation. According to the U.S. Tax Foundation, with admittedly outdated information from the year 2014, there were 1.7 million traditional C corporations, compared to 7.4 million partnerships and S corporations; even more sole proprietorships operating in the U.S.

I could not find similar data for other countries around the world, which is where Section 965 takes us.

USCs who live outside the U.S. and operate a business through a corporate entity in their country of residence (e.g., Canada, Mexico, UK, France, South Africa, Japan, Brazil, Hong Kong, Sweden, etc.) can be shocked when they learn how the new tax provision of IRC Section 965 works.

Hence, new IRC Section 965 imposes a one-time mandatory repatriation tax on accumulated earnings and profits of foreign corporations. The tax is paid by the U.S. shareholder. This makes policy sense, if the goal is to tax U.S. based taxpayers, especially mega companies with billions or 100s of millions of dollars of offshore un-taxed cash. In the past, much of these offshore profits could avoid U.S. taxation indefinitely as long as they were not actually repatriated in the form of dividends to the U.S. shareholder(s).

However, most people at the time were not expecting that this same repatriation tax would befall USCs living overseas arising from their local business operations.

Probably Congress and the Administration did not contemplate the fallout to these USC taxpayers. They were focusing on a different group of taxpayer. Nevertheless, Section 965 imposes immediate U.S. individual taxation on the “phantom income” (i.e., when no dividends are distributed to the USC shareholder) of the USC shareholder.

The next few posts will be dedicated to trying to explain in plain English how the “965 Hammer” (as I am affectionately calling it) applies to USCs residing in their home country with a business or investment assets held in a corporation.

The due date under the statute for paying this 965 tax has “come and past”; however, the IRS has granted certain extensions of time. These will be discussed in subsequent posts.

Importantly, a timely election under Section 965(h)(1) must be made by the due date (including extensions) for filing the return for the relevant year. For USCs residing outside the U.S., that due date was June 15th, 2018 and hopefully all USCs filed an automatic extension (IRS Form 4868) by that date, which would extend your due date to October 15, 2018 and the time to file the 965(h)(1) election.

. . . However, the IRS has determined that, if an individual’s net tax liability under section 965 in the individual’s 2017 taxable year is less than $1 million, the individual makes a timely election under section 965(h), and the individual did not pay the full amount of the first installment by the due date under section 965(h)(2), the failure to make the payment will not result in an acceleration event under section 965(h)(3) so long as the individual pays the full amount of the first installment (and its second installment) by the due date for its 2018 return (determined without regard to extensions). . .

A USC’s extensions and elections are very important here. A later post will explain how a USC residing outside the U.S. can obtain an additional extension at the discretion of the IRS. This can extend the due date of the 2017 income tax returns (IRS Form 1040) from the extended October 15th date to a further extended date of December 15th, 2018; for which the 965 election must be correctly made by the USC individual shareholder of a non-U.S. corporation.

A “Resident” is a “Resident” is a “Resident” – or Not?

Who is a “resident”? What is a “resident”? This sounds like such a basic question. It is not so simple for tax purposes; nor for other provisions of the law.

There is the colloquial meaning of resident. For instance, if Mr. Smith says, “I have been a resident of Montana on my ranch for 30 years”; to what does he refer? What if Mr. Smith has a house in California (which he has owned for 15 years) and another ranch in Alberta, Canada that he has owned for 45 years. Is he also a “resident” of Canada and California?

What if he is not a U.S. citizen but holds a particular type of visa, such as lawful permanent residency (an immigrant visa)? What if he has a non-immigrant visa, such as an E-2 visa? What if he only spends 4 months a year on his ranch in Montana, of where is he a “resident”?

Is he a “resident” in some or all of these scenarios? Why is this important in the context of “U.S. expatriation taxation”?

There are three sources of federal law where it becomes very important, which will be discussed in later posts:

In addition, various states, such as California, Texas and Washington D.C. (actually not a state; but all places I happen to be licensed to practice law) have their own definitions of who are “residents” for income tax and other purposes.

Subsequent posts will discuss the importance of understanding who is a “resident” and the implications under these various laws.

Laymen regularly have an idea of where they are “resident” – but that idea is often very different from definitions of “resident” under federal Titles 31, 26 and 8 and state laws (e.g., Texas, D.C., Florida, California, New York, etc.).

Mr. Dewees gets Smacked! U.S. District Court Upholds Multiple $10,000 Penalties (US$120,000 – NO Forms 5471) for USC Residing in Canada

United States Citizens (“USCs”) and lawful permanent residents (“LPRs”) residing overseas should read the story of Mr. Dewees to learn what could happen if they go into the offshore voluntary disclosure program (“OVDP”); when he appears to have been a “good faith” taxpayer. The IRS issued a press release in March 2018 – IRS to end offshore voluntary disclosure program; Taxpayers with undisclosed foreign assets urged to come forward now The IRS explained that it will close the program next month on September 28, 2018. Take the story of the Dewees into consideration before rushing into the OVDP.

This is not a new case, as the U.S. District Court for the District of Columbia issued its opinion a year ago – Dewees v. United States, 2017 U.S. Dist. LEXIS 124989 (D.C. D.C. 2017). However, it is an important case if anyone is confused about whether they should go into the OVDP. See the story of the Dewees.

He also did not initially pay information reporting penalties assessed by the IRS regarding his Canadian company. He resided in Canada where is business and company was located. The Court noted that he “. . . voluntarily disclosed [to the IRS] his failure to file the required informational returns . . . ” The Dewees were “rewarded” by their good faith efforts by the IRS which then turned around and ” . . . assessed a statutory penalty of $120,000, $10,000 for each year of non-compliance . . . “

The Canadian revenue authority would not refund his Canadian tax refund until the IRS penalty was paid in full. He eventually paid $120,000 of information penalties and brought a suit for refund in U.S. District Court.

The U.S. District Court first explained the obligations of USCs residing overseas with –

The Court then dismissed the suit for refund on the grounds that Mr. Dewees failed to state a viable claim and the Court therefore lacked jurisdiction to hear his claims (which were “excessive fines”, “equal protection” and “due process” claims).

Here, the USC residing in Canada was apparently well intended, since the District Court said that Mr. “Dewees learned that he had failed to comply with these requirements . . . ” In another part of the opinion, the Court uses the word “neglected” to file information returns for over a decade.

“Learned” and “neglected” certainly does not sound intentional, which is probably why the IRS did not attempt to pursue Title 31 willfulness FBAR penalties.

The USC entered the OVDP on the advice of a tax specialist and then withdrew after the IRS was proposing to assess an “OVDP in-lieu of penalty” of US$185,862.

The IRS ultimately did not pursue any FBAR penalties in this case, not even the annual $10,000 per year penalty for failure to file the FBAR form.

The U.S.-Canada income tax treaty has a special “assistance in collection” provision, which provides in part as follows –

Article XXVI A Assistance in Collection 1. The Contracting States [referring to the U.S. and Canada] undertake to lend assistance to each other in the collection of taxes referred to in paragraph 9, together with interest, costs, additions to such taxes and civil penalties, referred to in this Article as a “revenue claim”.

I explained in an earlier post, how the “Revenue Rule” was a common law concept that generally prohibited the U.S. government from assisting in the collection of taxes of another country. Hence, the U.S. Treasury renegotiated the treaties with five countries (including Canada) that now have a specific treaty provision such as XXVI A above:

As a result of these cases and the Revenue Rule, the U.S. and Canada modified their income tax treaty to (at least in theory) allow for the international enforcement of taxes. The U.S. now has five income treaties with “mutual assistance” provisions: Canada, Sweden, France, Denmark, and the Netherlands (with a clause in the newly negotiated, but yet to go into force, Swiss treaty).

In the Dewees case, we learned that the assistance in collection provision is not merely a theoretical tool that can be used in collecting taxes. The actions of both the Canadian (CRA) and U.S. governments (IRS and District Court Judge), made the provision effective. The US$120,000 penalty, that has nothing to do with any U.S. taxes, was collected by the IRS.

Questions to ponder in this case:

Would the USC have been better off, by getting proper advice as to how to file on a going forward basis?

Why did the USC ever go into the OVDP program in the first place under these facts?

In this case, the program did not exist at the time the taxpayers went into the OVDP in 2009.

Why did Dewees not simply consider (assuming he had good faith facts) filing amended tax returns to include late filed IRS Form 5471 forms?

Why did the IRS aggressively pursue these $120,000 in information penalties (presumably because he opted out of the OVDP program and they like to make examples out of those taxpayers that leave the program)?

Would and will the IRS assess more $10,000 per year penalties for additional companies for a good faith failure to file IRS Form 5471 forms? In other words, what if the Dewees had four Canadian companies, would the IRS have assessed US$480,000 (US$10,000 per year X 4 – per company – X 12 – the number of years the form was not filed)?

Will the IRS have success with any other country that does not have a similar tax treaty provision on the collection of taxes as the unique U.S.-Canada provision?

What about Sweden, France, Denmark, and the Netherlands with specific provisions in the U.S. income tax treaties? See a discussion of the U.S. District Court case in Georgia involving a Danish citizen, Torben Dileng v. Commissioner as discussed by Keith Fogg in the Procedurally Taxing Blog –

Will the aggressive actions of the IRS in this Dewee case to collect penalties backfire? Will USCs residing overseas be less likely to go into specific IRS programs for fear of being smacked down to the tune of US$120,000 (plus legal fees and costs) for merely neglecting to file information returns when no U.S. taxes are even owing?

United States citizens leaving after presidential elections?

The popular press has reported that the Canadian immigration service website crashed shortly after the results of the election. See Fox News, Nov. 9, 2016, Canadian immigration website crashes during election

It will be interesting to see if there will be a surge in United States citizens, not just the accidental American living outside the U.S., who will be inclined to renounce citizenship? These are not easy or legally simple steps, as various posts in this website explain. At a minimum, the individual must have citizenship in at least one other country, so as not to be left stateless.

It could be very difficult to mathematically determine whether this comes to pass, simply since the data provided for all names of individuals, does not include where they reside currently and for how long, inside or outside of the United States.

Of course, some may desire to move and live outside United States, without actually remounting their United States citizenship.

h on September 28, 2018. Take the story of the Dewees into consideration before rushing into the OVDP.

h on September 28, 2018. Take the story of the Dewees into consideration before rushing into the OVDP. Section 6038 to file

Section 6038 to file

this website explain. At a minimum, the individual must have citizenship in at least one other country, so as not to be left stateless.

this website explain. At a minimum, the individual must have citizenship in at least one other country, so as not to be left stateless.