Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

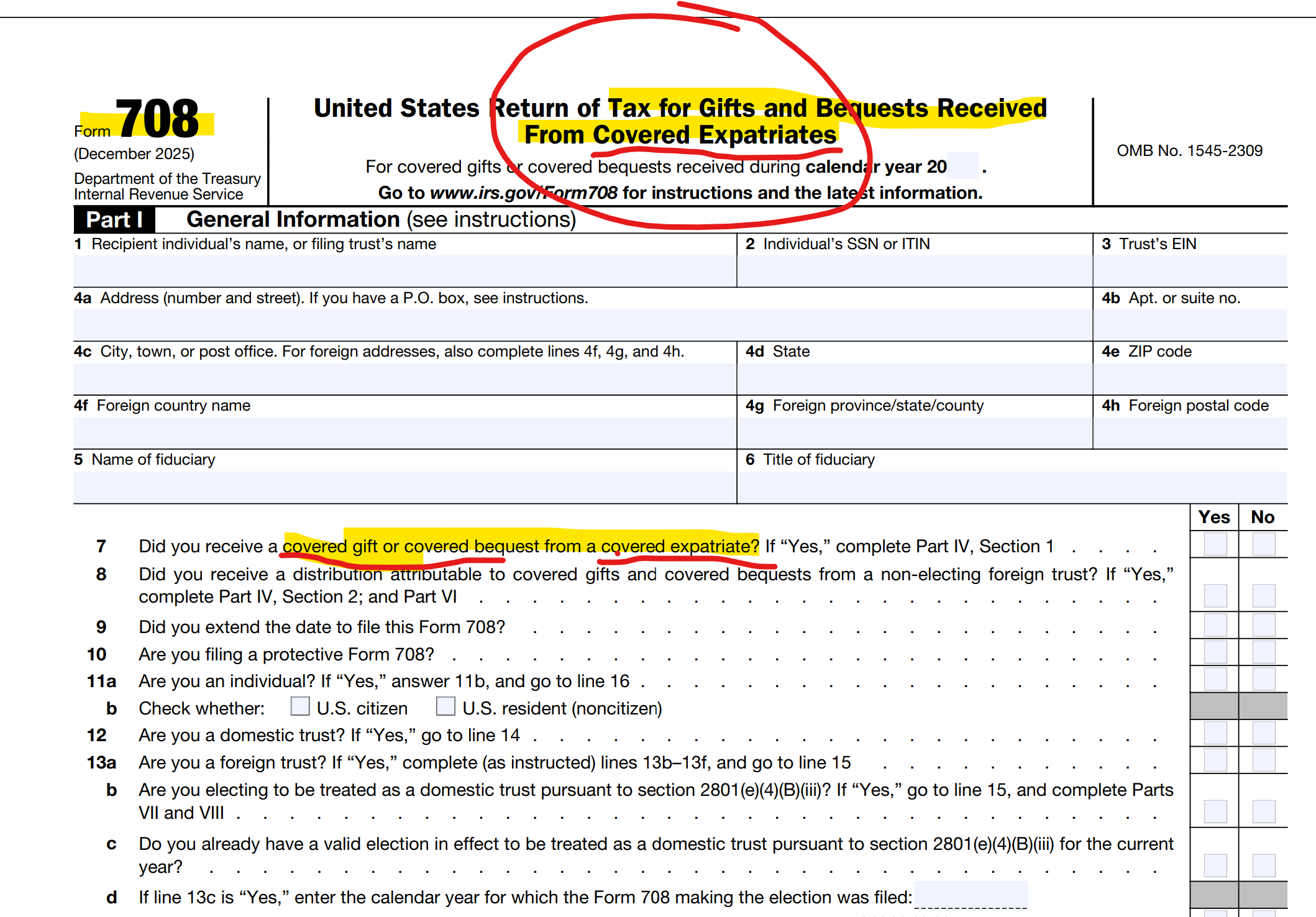

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

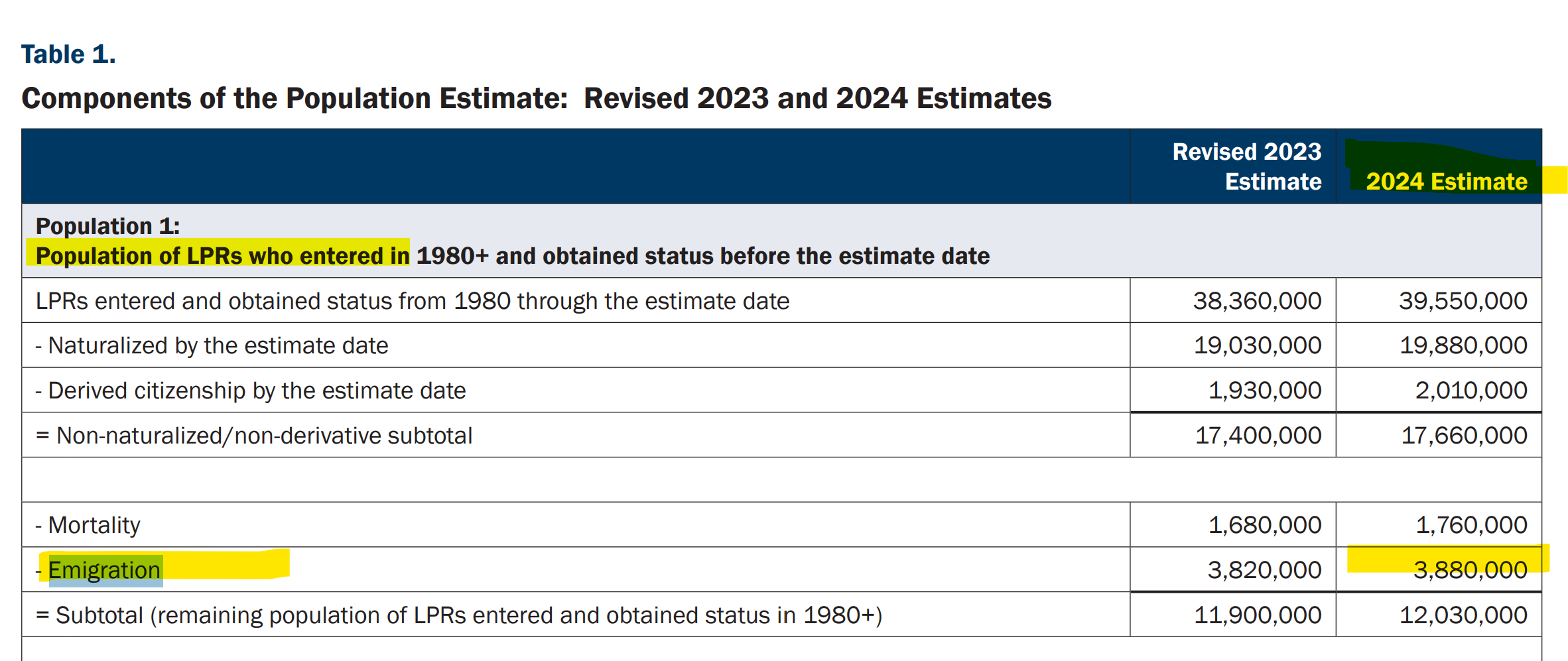

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

There have been numerous articles being written about the key case of the author (Patrick W. Martin) who has represented Mr. and Mrs. Aroeste for nearly 8 years.

Last week (Nov. 20, 2023), Judge Battaglia in the Southern District of California (San Diego) ruled in favor of our client Mr. Alberto Aroeste regarding the application of the U.S.-Mexico Tax Treaty. The DOJ, Tax Division arguments on behalf of the Internal Revenue Service in the case (and their Motion for Summary Judgment – MSJ) were largely rejected by the Court.

A thorough read of the Order from the Court is recommended to understand the substantial legal findings and legal analysis made by the Court relevant to those who possess a “green card” referred to as “lawfully admitted for permanent residence” in Title 8, § 1101(a)(13) [Immigration and Nationality Act]. Key to this case, Title 26, § 7701(b)(6) [Federal Tax Code] then rather contorts the concept by saying an individual is a “lawful permanent resident” in accordance with immigration laws; but then goes on to put conditions on who apparently is a “lawful permanent resident” for federal tax purposes. While immigration law requires the individual be ” . . . accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed”; the tax definition seems to ignore that status (i.e., has it changed and is the personal no longer accorded the privilege of residing permanently in the U.S.?).

The Board of Immigration Appeals (the “Board”), has long recognized that an alien’s status may change by operation of law, such that an alien may abandon his LPR status without a finding of removability (or, formerly, deportability or excludability) after a formal adjudicatory process. See United States v. Yakou, 428 F.3d 241, 247 (D.C. Cir. 2005); at 247-51 (discussing case law regarding abandonment and holding that an alien may abandon LPR status without formal administrative action); see also Matter of Quijencio, 15 I. & N. Dec. 95 (B.I.A. 1974); Matter of Kane, 15 I. & N. Dec. 258 (B.I.A. 1975); Matter of Muller, 16 I. & N. Dec. 637 (B.I.A. 1978); Matter of Abdoulin, 17 I. & N. Dec. 458, 460 (B.I.A. 1980); Matter of Huang, 19 I. & N. Dec. 749 (B.I.A. 1988).

The Court did not need to get into the nuances of immigration law to rule against the government in this case.

Some of the substantial takeaways from the decision are:

Waiver of the Tax Treaty: The government cannot assert an individual waived the treaty law because she initially filed the wrong IRS forms (1040) instead of the non-resident form (1040NR) and IRS Form 8833.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

Aroeste v United States – Order 20 Nov 2023 (p. 17)

Expatriation Tax form – IRS Form 8854: Validity and its Failure to Comply with the Administrative Procedure Act (“APA”)

C. Whether Aroeste Was Required to File Form 8854 The Government next argues that even if the IRS had accepted Aroeste’s amended returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009-85. (Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both amended forms. (Id.) Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does

not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Aroeste v United States – Order 20 Nov 2023 (p. 11)

Tax Treaty Law Applies – Article 4 Regarding Tax Residency

Various detailed analysis and discussions from the Court –

Aroeste v United States – Order 20 Nov 2023 (p. 11-14)

The Preamble to the FBAR Regulations is Not the Law –

. . . the Government points to the preamble to the 31 C.F.R. Part 1010 regulations, providing that “[a] legal permanent resident who elects under a tax treaty to be treated as a non-resident for tax purposes must still file the FBAR.” Amendment to the Bank Secrecy Act Regulations—Reports of Foreign Financial Accounts, 76 Fed. Reg. 10234-01 (Feb. 24, 2011). The Court finds this unavailing. The Government’s argument does not refute the plain language of the FBAR regulations, which explicitly invoke provisions of Title 26, including the provision that requires consideration of an individual’s status under an applicable tax treaty for the purpose of determining whether an individual is a “United States person” subject to FBAR filing. Specifically, Title 31 C.F.R. § 1010.350, which governs reporting of FBARs, subsection (b)(2) states that a “resident of the United States is an individual who is a resident alien under 26 U.S.C. 7701(b) and the regulations thereunder . . . .” The Government fails to cite to any case law or statue indicating otherwise, and the Court finds none. As such, because the Court finds the Treaty applicable to Aroeste, then the residence provisions of the Treaty, or the “tie breaker rules” dictates whether Aroeste may be treated as a nonresident alien.

Aroeste v United States – Order 20 Nov 2023 (p. 14)

This is the third court case (the other two were in U.S. Tax Court) I have had over the last several years where the IRS tried to assess substantial penalties and taxes against LPRs who resided substantially outside the United States. The other two cases were conceded by the IRS prior to going to trial. One case had over US$40M at stake as assessed by the IRS. This case, in federal district court, was pushed all the way to this favorable (to Mr. Aroeste and those around the world in similar circumstances) outcome by the government. We were successful with all of these non-U.S. citizen cases (two brothers from Mexico and an individual from Germany).

On Monday 11 Sept 2023, Robert Goulder wrote a detailed article about the implications of what he calls “The Green Card From Hell”! His article can be reviewed in its entirety through the subscription service provided by Tax Notes International – FBAR Madness: We Need to Chat About Aroeste.

Goulder made some key observations that are worth repeating for anyone who has been a green card holder for basically more than seven years. That can trigger the “expatriation” tax provisions – the focus of this blog.

The facts of the case of Mr. Alberto Aroeste are covered extensively and accurately in Goulder’s article.

He noted:

This week’s article concentrates on the novel FBAR issue that will be decided in Aroeste v. United States, an illegal exaction suit before the U.S. District Court for the Southern District of California.7 The case has garnered attention for good reason. It pushes back against the government’s dubious policy of requiring individuals treated as nonresidents under a U.S. tax treaty to provide FBAR filings. Let’s note the futility of the financial information which the government seeks from these folks. It concurrently exempts treaty nonresidents from the need to file IRS Form 8938 (“Statement of Specified Foreign Financial Assets”), the tax code’s counterpart to the FBAR.8 It remains problematic that the government should demand reporting from treaty nonresidents as if they were residents.9

The one issue not explained well relates to how and when lawful permanent residency (i.e. a “green card”) under Title 8 is even valid in the first place. Goulder’s article explains some of the rights of lawful permanent residency status, but also addresses some key areas of the immigration law the same as most tax law experts cover a different area of the law. See, SCOTUS’ observations of the law in this context: Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

For instance, Goulder claims green card holders cannot be deported as long as the immigration status remains valid. True – but what is not explained is how easy it is to cease to have a valid one in the first place. What he doesn’t explain is how and when an individual can “abandon” or “relinquish” the status as a green card holder (as a matter of law) by not residing permanently in the United States. See, Fundamentals of Immigration Law, written by Charles A. Wiegand, III, Former Immigration Judge, Oakdale, Louisiana. The law is complex as described by Wiegand.

Goulder does not seem to find the government’s arguments persuasive (“ain’t buying it“!):

For Aroeste, there seems to be little doubt his closer personal and economic ties are with Mexico. The IRS knows this. An analysis conducted by an IRS agent concluded that he spent no more than 67 days in the United States during 2012 and 57 days in the United States in 2013, with three-quarters of the remaining time spent in Mexico.

Goulder –

The IRS doesn’t care where Aroeste had closer personal and economic ties. That’s because it doesn’t care about the tiebreaker. As the government sees it, the treaty is a distraction that has no meaningful role to play in this litigation. The plaintiff’s immigration status is conclusive, end of story. His green card settles the matter, such that all further inquiries are superfluous and should cease.

Id.

What bothers me about that argument is how the government’s position selectively wishes away the existence of the U.S. tax treaty network — but only for application of the FBAR regime. The Mexico treaty would still mean something in another context, but not on the pivotal issue of Aroeste’s status as a U.S. person for FBAR purposes. Sorry, I ain’t buying it.

Id.

The government argues the treaty is only relevant for income and excise tax purposes, and what we have here are penalties based on violations of the Bank Secrecy Act — not the Internal Revenue Code. As the government sees it, no plaintiff can successfully challenge penalties authorized by Title 31 with legal remedies based on Title 26. I’m still not buying it.

Id, Goulder

I would recommend you take a read through his article that also addresses a discussion on how the government prefers to keep internal memoranda from the eyes of the public. He discusses at some length – Tax Analysts and Coastal States. How the Court in Aroeste took an approach different from the D.C. Circuit in articulating 9th Circuit law regarding attorney client privileged documents in the possession of the government.

The world is starting to wake up to better understand how the U.S. Treasury negotiated so-called “bilateral” FATCA Intergovernmental Agreements (“IGAs”) with some 113 countries around the world. The list of all countries can be found here at the Treasury website – Foreign Account Tax Compliance Act (FATCA)

Not all of these countries have actually signed the IGAs. Many of them have what the U.S. Treasury calls an “agreement in substance.”

How does this impact USCs and LPRs residing outside the U.S.? Many ways.

First, extensive information is being collected by foreign financial institutions (FFIs – non-U.S. financial institutions) throughout the world to identify “U.S. Persons” and “Substantial U.S. Owners.” The IGAs use the term “Specified U.S. Person” with respect to what are defined as “U.S. Reportable Accounts.” See as an example, the Treasury FATCA IGA with Colombia, which is largely identical in form to almost all other IGAs.

Second, many FFIs have adopted a policy to no longer accept or retain U.S. accounts, due to the cost of compliance associated with U.S. citizens and lawful permanent residents. Also, many FFIs simply want to avoid the risk of being penalized heavily by the U.S. federal government for having U.S. taxpayers and being charged with some type of wrongdoing; namely aiding and abetting U.S. taxpayers to evade U.S. tax obligations. See, Jack Townsend’s thoughtful website Federal Tax Crimes that reviews in detail the various cases with foreign banks, with a particular focus on Swiss banks, U.S. DOJ Program for Swiss Banks .

Now to the “dirty little secret” of FATCA IGAs. They are not bilateral in the sense that U.S. banks do not need to provide the same detailed information on their non-U.S. clients (e.g., UK, French, Canadian, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, residents, etc.) as do FFIs regarding “U.S. accounts.” This is no real secret, since a simple reading of the FATCA IGAs will get you to this conclusion by simply understanding the difference between what is defined as a “U.S. Reportable Account” (which is extraordinarily broad) compared to “Country X Reportable Account.” The latter definition, e.g., a Colombian Reportable Account, only obligates U.S. banks to send information of individual residents on U.S. source income under chapter 3 and certain accounts of Colombian entities.

Hence, all non-U.S. source income to a Colombia resident individual is not subject to reporting by the U.S. financial institution. She could have a portfolio of US$150M in non-U.S. mutual funds, ADRs traded on the NYSE and have no reporting of all of her income going back to the Colombian government. Also, stock sales of U.S. corporations (e.g., Apple, Ford or Microsoft) is not treated as “U.S. source income” defined under chapter 3. Plus, a Colombian resident who has an offshore corporation (e.g., a BVI company) that owns the investments, NO reporting is required of the U.S. financial institution; even if the entire US$150M portfolio were invested in U.S. stocks, U.S. treasuries, and other American made financial investments.

Contrast that with what is defined as a “U.S. Reportable Account” that would include a U.S. Person that is a “Controlling Person” of a “Non-U.S. Entity.” Take the same example in reverse; a Colombian bank must identify all of its clients with Non-U.S. Entities (undertake an expensive due diligence process) to then identify whether such entities (e.g., a BVI company) has a “Specified U.S. Person”. Plus, it does not matter if the income is from Colombian sources or non-Colombian sources. Income is income and must be reported by the FFI.

Accordingly, Banks around the world in at least 113 countries (e.g., UK, French, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, Cayman, Singapore, Guatemala, Hong Kong, etc.) are required to drill down and collect detailed information on beneficial owners of basically all companies, trusts and other legal entities. This work is required, so as to identify who are “U.S. persons” to identify “substantial U.S. owners” as that term is defined in the FATCA regulations. The IGAs call these essentially “U.S. Reportable Accounts.” In the case of FFIs, U.S. taxpayers cannot hide behind offshore opaque legal entities (e.g., which would generally be illegal for USCs to form and hold assets in a foreign corporation and not report the assets, activities and earnings of the foreign corporation, which would generally be a CFC or possibly a PFIC). See prior post: March 30, 2015, The Problem with PFICs! “Avoid PFICs Like the Plague”

The FATCA IGAs, require these FFIs to provide extensive information on all income on these “U.S. Reportable Account” to the IRS, either directly or indirectly through their own governments.

In contrast, individuals resident in any foreign country (e.g., UK, French, Mexican, Chinese, Dutch, Spanish, Colombian, Brazilian, Belgium, Guatemala, Luxembourg, etc.) can generally hold their ownership interests of U.S. investment assets in U.S. banks and financial institutions through opaque legal structures and hide behind the entity without worrying that a U.S. financial institution has any duty to identify and disclose who are the beneficial owners to the tax authorities of those residents. See Colombian individual scenario above with a BVI company.

Why did the Treasury purposefully create this limited reporting obligations for U.S. financial institutions while creating extensive and detailed reporting obligations for FFIs?

Why are U.S. financial institutions not required under FATCA IGAs to identify the beneficial owners of opaque legal structures to report the income and gains to foreign tax authorities?

Why are U.S. financial institutions not required under FATCA IGAs to identify the and report non-U.S. source income in their U.S. accounts?

Why has the U.S. refused to participate in the OECD common reporting standards?

United States Citizens (“USCs”) and lawful permanent residents (“LPRs”) who live largely outside the U.S. must generally be aware of U.S. federal tax laws and how they apply to them. USCs and LPRs “expats” (living outside the U.S.) are of course constantly being required to understand U.S. tax law and comply with its provisions.

Recently, the U.S. Treasury proposed new regulations requiring certain foreign owned single member U.S. limited liability companies and grantor trusts to report information.

The preamble to the proposed regulations (which are titled – Treatment of Certain Domestic Entities Disregarded as Separate From Their Owners as Corporations for Purposes of Section 6038A) note that:

Some disregarded entities are not obligated to file a return or obtain an employer identification number (“EIN”). In the absence of a return filing obligation (and associated record maintenance requirements) or the identification of a responsible party as required in applying for an EIN, it is difficult for the United States to carry out the obligations it has undertaken in its tax treaties, tax information exchange agreements and similar international agreements to provide other jurisdictions with relevant information on U.S. entities with owners that are tax resident in the partner jurisdiction or otherwise have a tax nexus with respect to the partner jurisdiction. . . . a disregarded entity is not subject to a separate income or information return filing requirement. Its owner is treated as owning directly the entity’s assets and liabilities, and the information available with respect to the disregarded entity depends on the owner’s own return filings, if any are required.

For those LPRs residing outside the U.S. who are not U.S. taxpayers by virtue of an applicable income tax treaty (i.e., by application of the treaty tie-breaker rules, typically Article 4), it appears these newly proposed regulations could be applicable to their single member LLCs or grantor trusts. USCs will not be effected, since the proposed regulations impose this reporting requirement when there is “(2) One foreign person [who] has direct or indirect sole ownership of the entity.” A USC cannot be a “foreign person”; which is not a defined term in the current statute or regulation. A “United States person” is a defined term and so is a “nonresident alien”; but not a “foreign person.”

Curiously, the Treasury is using IRC Section 6038A as the authority to issue such regulations. That statute only references “a corporation” which is a technically defined term under IRC Section 7701(a)(3), (a)(4) and (a)(30)(C). Section 6038A makes no reference to a”disregarded entity” a “grantor trust” or any other company or entity that are not “corporations.” Therefore, it is difficult to imagine how the Treasury has the statutory authority to issue this proposed regulation without legislative authority?

There are many misunderstandings of how the law works when someone renounces U.S. citizenship. The author regularly hears a range of myths that will befall an “Accidental American” when and if, they renounce. These “myths” include the following:

Myth 1: There is a 10 year period of U.S. income taxation after renouncing citizenship.

Fact: The old tax law from 1996 and the modifications in 2004 had a 10 year period of taxation concept after “expatriation.” There is no longer such a 10 year period of taxation for those persons who renounce on or after June 17, 2008.

Myth 2: Former U.S. citizens will not be allowed to enter into the U.S.; i.e., will be barred from re-entry at a point of entry by a U.S. immigration officer.

Fact: Former U.S. citizens are generally entitled to any visa status, the same as any other non-U.S. citizen. There is not a single case where a former U.S. citizen was barred re-entry to the U.S., due to tax motivated purposes.

Myth 3 : Former U.S. citizens will not be allowed to ever re-obtain citizenship.

Fact: Former U.S. citizens are generally entitled to U.S. citizen status, the same as any other non-U.S. citizen. Importantly, U.S. citizenship may simply not be available to any particular non-U.S. citizen, depending upon the particular circumstances.

Myth 4: U.S. citizens do not need to renounce their U.S. citizenship if they live in a country with an income tax treaty with the U.S.; since the tie breaker rules of residency will keep them from being U.S. income tax residents.

Fact: U.S. citizens cannot escape worldwide taxation, both income and gift/estate taxes, by living outside the U.S., since all U.S. bilateral income tax treaties and estate and gift tax treaties have a “savings clause” allowing the U.S. government to impose taxation on U.S. citizens notwithstanding the treaty.[1] This is how the U.S. tax net works on worldwide assets and income.

There are many more myths which will be discussed in a later post.

[1] See footnote no. 14 of Crow v. Commissioner, 85 T.C. 376 (1985):

14/ . . . The Treasury Department’s explanation of the Maltese treaty . . . :

“Paragraph (3) contains the traditional ‘saving clause’ under which each Contracting State reserves the right to tax its residents, as determined under Article 4 (Fiscal Residence), and its citizens as if the Treaty had not come into effect. [Department of Treasury, Technical Explanation of the Agreement Between the United States of America and the Republic of Malta with Respect to Taxes on Income 2 (Published in Treasury Department Press Release R 367 on Sept. 24, 1981), 1984-2 C.B. 366.]” This interpretation is consistent with the typical interpretations accompanying recent treaties containing general savings clauses.

The willfulness question is important, when the USC or LPR decides what steps they need to take regarding the filing of U.S. income tax returns.

A LPR residing predominantly in a country with a US. income tax treaty (of which there are 68) may be in the best position to “clean up” their U.S. tax filing and return positions. Specifically their facts might allow them to file as a non-resident under the “tie-breaker provisions” – typically Article 4); and indeed such filings might be applicable for several prior years.

The issue of “expatriation” becomes front and center for the LPR who notifies the IRS that he or she is not a resident of the U.S, pursuant to an applicable income tax treaty and files the treaty position accordingly.

Specifically, the statutory language of IRC Section 7701(b)(6) has three tests for when the individual is no longer a LPR for federal tax purposes:

The individual is treated as a resident of a foreign country under the provisions of a tax treaty;

The individual does not waive the benefits of the treaty, and

Notifies the Secretary of the commencement of such treatment.

If the LPR has had that status for the requisite number of 8 years or more, to be treated as a “long term resident”, he or she would generally be subject to the “exit tax” of Sections 877 and 877A (plus a tax to any future U.S. persons who receive gifts or inheritances from such former LPR). See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

If the LPR has not been “non-willful” (double negative intended) by not filing U.S. income tax returns, interesting legal questions are raised as to the consequences to the LPR.

In addition, the IRS “streamlined” procedure announced on June 18th, 2014, has specific requirements obligating the taxpayer to certify “non-willful” behavior.

Various consequences of signing these certifications under penalty of perjury, will be discussed in later posts.

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below.

Please first read Part I of this series: Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI, which outlines some of the foundational questions every green card holder should consider before addressing the additional issues questions below. Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

The list of all countries can be found here at the Treasury website – Foreign Account Tax Compliance Act (FATCA)

The list of all countries can be found here at the Treasury website – Foreign Account Tax Compliance Act (FATCA) government for having U.S. taxpayers and being charged with some type of wrongdoing; namely aiding and abetting U.S. taxpayers to evade U.S. tax obligations. See, Jack Townsend’s thoughtful website Federal Tax Crimes that reviews in detail the various cases with foreign banks, with a particular focus on Swiss banks, U.S. DOJ Program for Swiss Banks .

government for having U.S. taxpayers and being charged with some type of wrongdoing; namely aiding and abetting U.S. taxpayers to evade U.S. tax obligations. See, Jack Townsend’s thoughtful website Federal Tax Crimes that reviews in detail the various cases with foreign banks, with a particular focus on Swiss banks, U.S. DOJ Program for Swiss Banks .

See prior post: March 30, 2015, The Problem with PFICs! “Avoid PFICs Like the Plague”

See prior post: March 30, 2015, The Problem with PFICs! “Avoid PFICs Like the Plague”