What is the statute of limitations on an IRS tax audit?

The statute of limitations is the time frame in which the government has to conduct an audit against a US taxpayer. Once that time frame lapses, the IRS cannot commence tax audits or assess taxes or tax penalties against a US citizen (USC) or lawful permanent resident (LPR, a green card holder) living overseas. In other words, the limitations period sets a fixed window, and after it closes the taxpayer generally has protection from new audits and assessments for that year.

In what situations is there no statute of limitations for a US citizen or green card holder abroad?

There are basically three ways a US citizen or green card holder living outside the US will have no protection of a statute of limitations against the IRS. In these scenarios the limitations period stays open, so there is no closing date on the government’s ability to audit or assess. The three basic scenarios are:

The USC or LPR does not file a US income tax return (IRC Section 6501(c)(3)).

There is fraud on the part of the taxpayer (IRC Sections 6501(c)(1), (c)(2)).

The USC or LPR fails to report certain foreign transactions (IRC Section 6501(c)(8)).

What happens to the statute of limitations if you do not file a US income tax return?

If a US citizen or green card holder does not file a US income tax return, there is no statute of limitations for that year under IRC Section 6501(c)(3). Because the limitations clock generally starts when a return is filed, no return means the period never begins to run. The IRS may therefore audit or assess for that year without a fixed cutoff.

How does tax fraud affect the statute of limitations?

Where there is fraud on the part of the taxpayer, there is no statute of limitations under IRC Sections 6501(c)(1) and (c)(2). An example is a taxpayer who intentionally does not report income. In that situation the limitations period stays open, so the IRS may pursue an audit or assessment for that year without a closing date.

What happens if you fail to report certain foreign transactions?

If a US citizen or green card holder fails to report certain foreign transactions, there is no statute of limitations under IRC Section 6501(c)(8). This rule was only recently adopted as part of the “HIRE Act,” the same law that created FATCA (the Foreign Account Tax Compliance Act). The limitations period for the year can remain open until the required foreign-transaction reporting is made.

Why file a complete and accurate return even when no tax is owed?

One basic point from the law is that a US citizen or green card holder is almost always better off filing tax returns that are complete and accurate, even when no tax is owing. Filing this way helps assure a fixed time frame during which the US federal government can conduct tax audits and other related tax investigations. Without that fixed window, the limitations period may stay open. Anyone weighing their own situation may want to consult an experienced tax attorney.

Where can you read more about international tax statute of limitations issues?

For an overview of the statute of limitations periods, see the presentation “Starting the Race Against the Tax Authority in the International Tax World – Statute of Limitations & Lack of Filings” by John C. McDougal, Special Trial Attorney at the IRS, and Jon P. Schimmer and Eric D. Swenson of Procopio.

What’s Your Probability of an IRS Tax Audit? Taboo – to say? . . . . shhhhh . . . . “Covered Expatriates”

Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

Mérida – the Place to be in February (19th and 20th)

The implications of the Aroeste v United States – Order (Nov 2023) particularly for millions of taxpayers globally and “U.S.” taxpayers affected by pertinent tax treaty provisions, will be a focal point of discussion at the upcoming international tax conference in February.

The University of San Diego School of Law – Chamberlain International Tax Institute will take place on February 19th and 20th, 2024, at the International Convention Center in Mérida, Yucatán, México. You can register for the conference – HERE –

Among the courses offered, there will be a detailed examination of- Aroeste v. the United States: Limits on Government Authority Re: Tax Treaty Law ++– along with other international tax topics and sessions featuring much Moore:

United States Supreme Court – Tax Decisions & Moore

International Tax Reporting: New Reporting of International Partnerships – K-2s & K-3s

United States-based Cross-Border Real Estate Investments (Advanced)

U.S. Investor Visa Options and Limitations

California, Texas & Florida Probate Proceedings of Cross-Border Estates

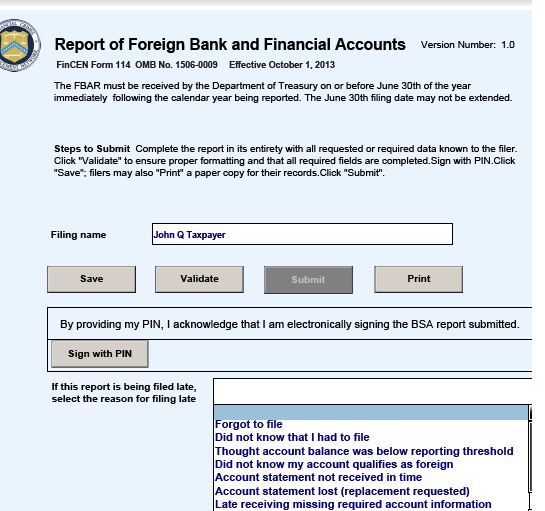

Importantly, the website provides the following comforting statement:

The IRS will not impose a penaltyfor the failure to file the delinquent FBARs if you properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs, and you have not previously been contacted regarding an income tax examination or a request for delinquent returns for the years for which the delinquent FBARs are submitted.

The question is the following:

Is the IRS bound by their own statement on their website as a matter of law?

In other words, can they go ahead and assess FBAR penalties notwithstanding the statement set forth above on their website?

Assuming you do have an FBAR filing requirement, e.g., residing in your country of residence with financial accounts in your own country or in other financial institutions outside the U.S.; can the IRS assess a penalty against you for a delinquently filed FBAR? What if you have properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs?

The answer may surprise you. It will be addressed in a subsequent post.

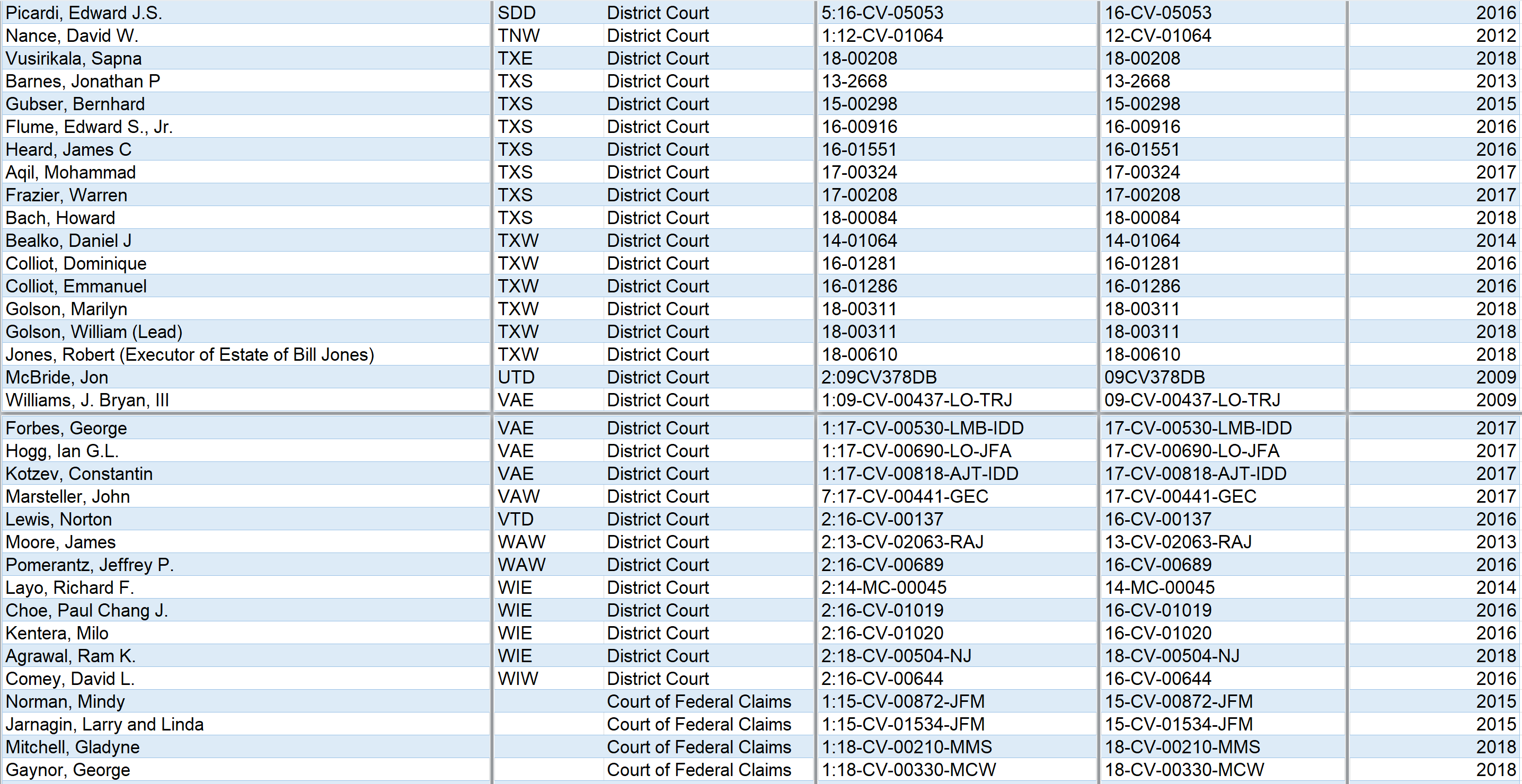

Incidentally, to date, there have been more than 200 FBAR civil penalty cases filed in U.S. federal courts. The Federal District Courts have seen approximately 200+ civil penalty cases and the Court of Federal Claims, much less popular venue, has seen 5 cases thus far.

Part II: “Neither Confirm nor Deny the Existence of the TECs Database”: IRS Using the TECs Database to Track Taxpayers Movements – and Assets

Part II: This is a follow-up to the federal government’s database known as “TECS” (Treasury Enforcement Communication System)that is now operated by the Department of Homeland Security (“DHS”). The IRS uses it to track travel, trips, movement and even asset movements (e.g., wire transfers) by U.S. citizen taxpayers; including those residing outside the U.S.

This previous post described how the U.S. federal government uses the TECS to locate assets and travel patterns of U.S. citizens; specifically outside the U.S. The IRS trains their employees to (1) Not discuss TECS with taxpayers; (2) Neither confirm nor deny existence of TECS; (3) Keep in separate “Confidential” envelope; and (4) Stamp documents as “OFFICIAL USE ONLY”

The image in this post reflects a page from IRS training materials for their employees; e.g., revenue agents (those individuals who audit taxpayers and determine tax deficiencies and the like), revenue officers (those individuals who work on collecting taxes owed or alleged to be owed) and chief counsel attorneys (those individuals who litigate tax cases against taxpayers); among other IRS employees.

Frankly, there is not a lot of detailed law about how and when the IRS can use TECS or other tracking techniques of individuals and their assets. There are no tax cases (at least none that I am aware of) where the Courts have tried to impose limits on the use and methods of the federal government in collecting this type of TECS information. Indeed, there are specific provisions granting broad use of taxpayer information when the government alleges there is a “terrorist incident, threat, or activity” as that term is defined in IRC Section § 6103.

On the other hand, there are important laws about how the IRS cannot generally disclosetaxpayer information. For instance, see the same code section IRC Section § 6103 for wrongful disclosures of taxpayers’ information. That statute makes it a violation (even a criminal violation in certain willful circumstances) to disclose taxpayer information in “most” (or at least many) circumstances. The statute is comprehensive and there is a lot of case law interpreting various provisions. A good overview of the statute can be found in the Criminal Tax Manual for the Department of Justice, Tax Division – Chapter 42.00

A recent case (United States v. Garrity, 2016 U.S. Dist. LEXIS 66372 (D. Conn. 2016), discussed in Jack Townsend’s blog, was one where the IRS had disclosed the name of a deceased taxpayer Paul G. Garrity, Sr. regarding his foreign (non-U.S.) accounts. The disclosure included IRS investigation techniques that were disclosed as part of a FOIA request, which ultimately made it to the public. This was found to be disclosure of return information as defined by IRC Section § 6103. However, the Court there found that there was no violation of the statute by the IRS, as the taxpayer was deceased by the time the claim was brought by the estate. The government made a Title 31 FBAR penalty assessment of over US$1M including interest and penalties that is still pending.

It seems to me that the use of the TECS database by the IRS and Section 6103 are a bit like two heads of a coin. It all deals with taxpayer information and what rights, if any do taxpayers have to protect their personal and financial information – especially where it can (purposefully or inadvertently – e.g., through a data breach/hacking) be released to the public.

There are many unanswered questions as there has been little to no litigation regarding how and when the TECS database can and should be used.

Does the government have any limits on its use?

This ultimately becomes more of a policy discussion about how and to what extent can/should the federal government have and use and collect personal financial and travel information of individuals (particularly for tax purposes)?

The Life Insurance “Gotcha Tax” – IRS Assesses Excise Tax on Normal Life & Other Insurance Policies

The information featured on this blog is designed to orient U.S. citizens (“USCs”) and U.S. lawful permanent residents, i.e., “green card” holders (“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

There are many complex federal tax rules that are often overlooked in the international area. One of those is the excise tax that is payable by the USC or LPR individual, not the non-U.S. insurance company, when premiums are paid to an insurance company. The IRS takes the position that the ” . . . the Service will generally seek payment of the excise tax from the U.S. person making the premium payment . . .” See, IRS Foreign Insurance Excise Tax- Audit Technique Guide.

This is a 1% excise tax on the premiums paid for each life insurance, sickness or accident insurance or contracts. See, IRC Section 4371. If you reside in London and buy life insurance with a UK life insurance carrier (or Paris with a French insurance company, Toronto with a Canadian insurance company, etc.) in your home country, you are probably not thinking that you need to pay Uncle Sam a tax on what you perceive as a “run of the mill” insurance coverage.

Indeed your life insurance company in your country of residence will not be advising that as a USC or LPR, you should be paying Uncle Sam.

If the insurance contract is a casualty policy, the excise tax is 400% greater than the 1% tax on life insurance premiums; i.e., a 4% excise tax. The payment of the tax is made on IRS Form 720, Federal Excise Tax Return.

In my experience, I never find that any individuals who are USCs and LPRs living around the world are aware of this obscure tax. When the tax is not paid the IRS has unlimited time to assess tax and penalties, including late payment penalties, late filing penalties and negligence penalties. Plus, interest that accrues on the unpaid tax and penalties can grow the amounts owing over time. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S., posted March 24, 2014.

The excise tax amount may not seem too significant. However, if it is not timely paid, there will be late payment and late filing penalties (e.g., for failure to file the excise tax return). This 1% or 4% excise tax is on the gross premium payment. This tax amount can certainly add up when insurance premiums are paid annually and over many decades.

Finally, be aware that the IRS is focusing on this excise tax on insurance contracts, at least within its OVDP program where IRS revenue agents are asserting that 25%, 27.5% or 50% of the value of the entire asset (e.g., the cash surrender value of the insurance policy) is subject to the “in lieu of penalty”.

IRS Creates “International Practice Units” for their IRS Revenue Agents in International Tax Matters

The U.S. international tax law has become increasingly complex. I am confident when I say that very few individuals in the world (including IRS revenue agents) understand the complexities of Title 26 and Title 31 as they apply to international matters such as gifts of foreign property, gifts involving U.S. intangible property, gifts to or inheritances from foreign estates with U.S citizens (USCs) or Lawful Permanent Residents (LPRs) beneficiaries, foreign partnerships with USCs, transfers of property to foreign trusts by USCs or LPRs residing outside the U.S., transfers of property to foreign corporations, etc.

Most USCs and LPRs who live in the U.S. certainly know and understand the basics of IRS Form 1040.

The lack of knowledge of these complex laws within the IRS, and the LB&I (Large Business and International group) which specializes in international matters has led to IRS “International Practice Units”. These are designed to allow IRS revenue agents who are not necessarily specialists in the international tax area to review transactions and be prepared to assess taxes and penalties against USCs and LPRs in the international context. The preamble says in part ” . . . Practice Units provide IRS staff with explanations of general international tax concepts as well as information about a specific type of transaction. . . ”

These IRS materials give a good perspective from where the IRS views the world; including the introduction to this particular IRS International Practice Unit where it states: “This Practice Unit focuses on a U.S. Person’s proactive steps to “conceal” their ownership of foreign financial accounts, entities and other assets for the purposes of tax avoidance or evasion, even though, there may be some situations where there are legitimate personal or business purposes for establishing such arrangements. This unit falls under the outbound face of the matrix and thus, will focus on U.S Persons living in the United States . . . Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .” [emphasis added]

This is a breathtaking statement from the IRS internal training manuals that “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .”?

The vast majority of the USCs or LPRs who I see who renounce or abandon their citizenship or LPR status, are living outside the United States and in most cases have spent almost all (if not all) of their lives outside the U.S.

Does the IRS mean that a family living in Switzerland that have dual national family members are “. . . .simply hiding the accounts from the Internal Revenue Service . . . ” if they are using, for instance, a Liechtenstein Stiftung to hold their family assets as part of an estate plan recommended to them by their Swiss legal and tax advisers?

Does the statement that this IRS International Practice Unit focuses on ” . . . U.S Persons living in the United States . . . ” give USCs and LPRs residing outside the U.S. relief from the IRS perspective of USCs simply hiding assets from the Internal Revenue Service? Will IRS revenue agents be sophisticated enough to distinguish between these two different groups; U.S. resident versus non-resident USCs and LPRs? Will the law be applied differently with respect to these resident versus non-resident U.S. taxpayers?

What role will these IRS “International Practice Units” play in forming perceptions and molding ideas of IRS revenue agents who have had little to no life experience in international affairs, multi-national families, global finance and international business operations?

We can call this “forced expatriation”; when the government takes investigative action to deport a lawful permanent resident (“LPR); i.e., cause a forced tax expatriation where an individual files a false return, provides false information or otherwise submits a false document to the government.

The point of this post is to highlight a point previously made:

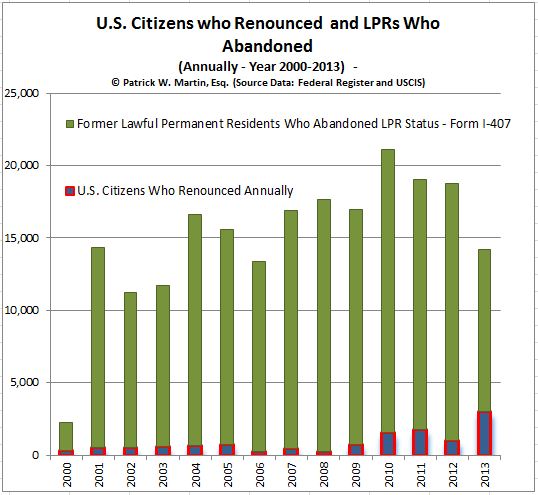

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

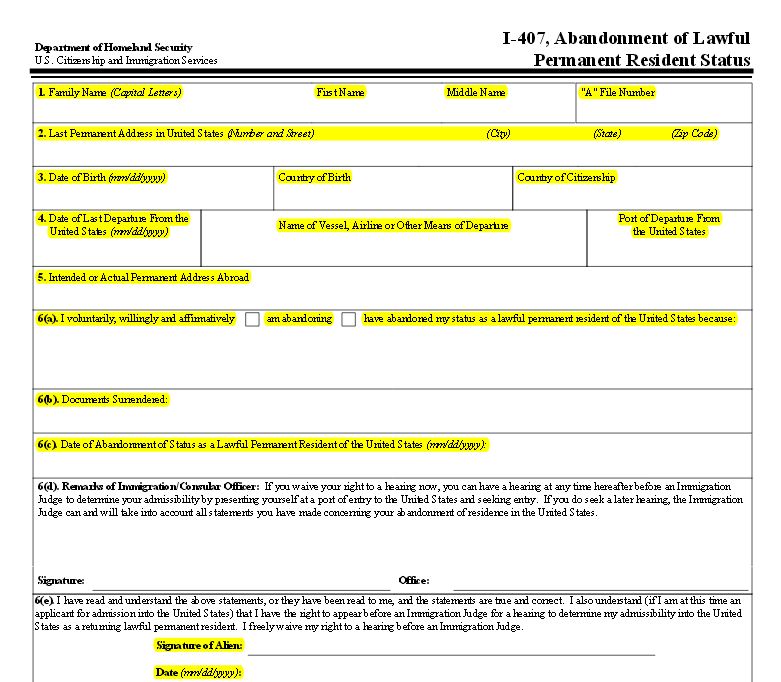

The U.S. Customs and Immigration Service (USCIS) announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement,

Is “It’s Almost Impossible for Me to Get a U.S. Taxpayer Identification Number”; a Defense to Not Filing U.S. Tax Returns?

The U.S. federal government has made the basic task of getting taxpayer identification numbers (“TINs”) very difficult for many individuals. Without a TIN, an individual cannot file tax returns or information reporting returns.

The U.S. tax law imposing taxation on the worldwide income of USCs[1] residing overseas has created a dilemma that prejudices these USCs without a SSN. This strict SSN/TIN regulatory rule undermines the basic tax administration system and discourages tax compliance for those USCs who never obtained a SSN. This dilemma affects numerous USCs throughout the world, which is now compounded by the certification and reporting requirements of USCs and third parties, such as FFIs and NFFEs[2] under the Foreign Account Tax Compliance Act (“FATCA”).

This dilemma is a creature of the Title 26 regulatory law going back to 1974[3] and how the Social Security Administration (“SSA”) imposes strict requirements on the issuance of SSNs to residents overseas.[4] One essential step is that the USC overseas must have an in-person interview, with a designated individual (who are typically U.S. Department of State employees and some designated military personnel). They are located in only a few cities around the world.[5] Some USCs need to travel thousands of miles to merely be able to apply for and obtain a SSN.

[1] See, IRC § 61 and Treas. Reg. §§ 1.1?1(b) and 1.1?1(a)(1).

[2] See, IRC §§ 1471 et. seq. and the regulations thereunder which define “foreign financial institutions” (“FFIs”) and “non-financial foreign entity” (“NFFEs”).

[4] See, 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

[5] Id, page 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

Further posts will discuss a number of the adverse consequences imposed on USCs who do not have a SSN and the severe penalty regime that exists under current law for those unwitting individuals.

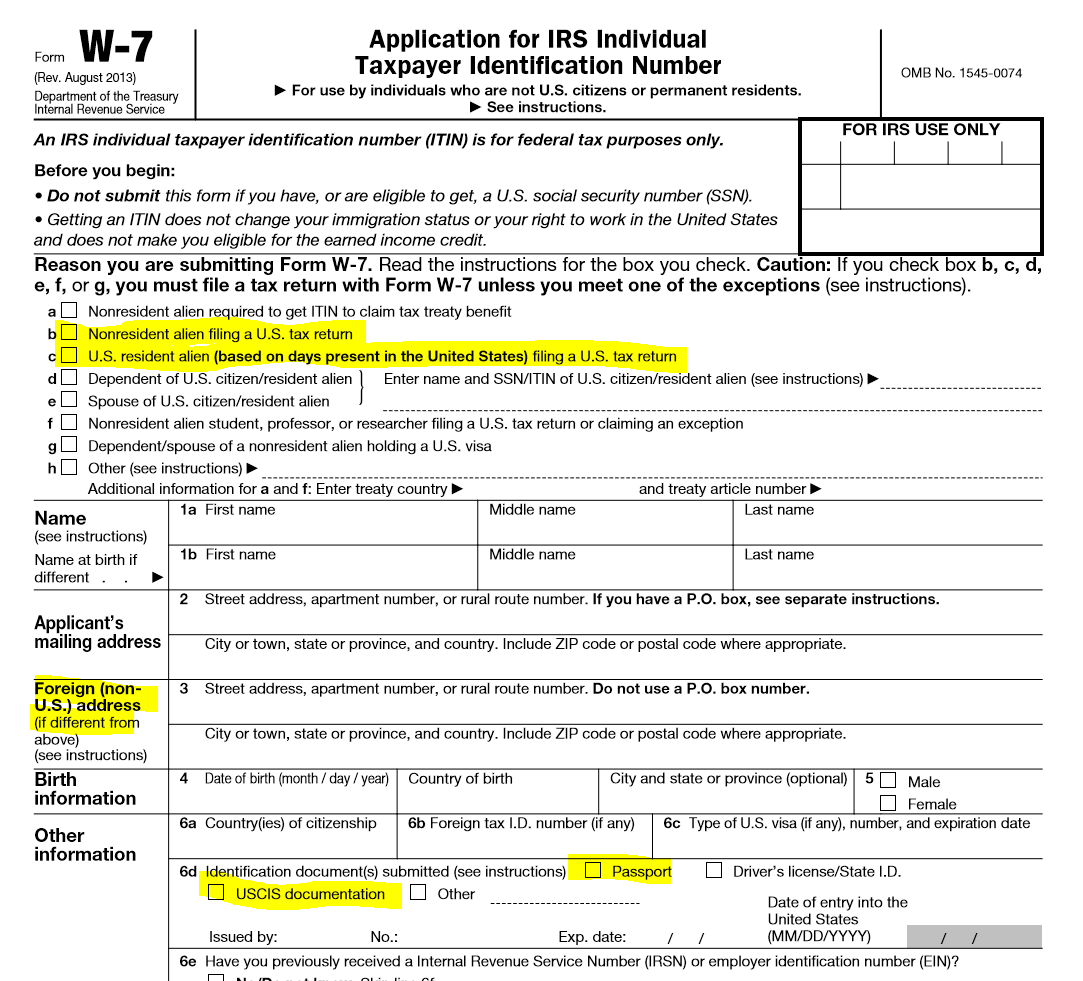

Non-U.S. Citizens and ITINs –

Many individuals who are not USCs nevertheless need to file a tax return and must obtain what is called an individual taxpayer identification number (“ITIN”). See IRS report Obtaining an ITIN from Abroad. An ITIN is applied for by filing an IRS Form W-7, and providing various original documents, principally a passport, directly to the IRS. The process is complex and time consuming. Indeed, the Taxpayer Advocate report included a key summary explanation of the problems associated with obtaining ITINs as follows:

IRS ITIN Policy Changes Make Return Filing Difficult and Frustrating

Recent changes to the IRS’s Individual Taxpayer Identification Number (ITIN) application program are burdening taxpayers and may harm voluntary compliance.

ITINs play an important role in tax administration, as any individual who has a federal tax filing obligation but is not eligible for a Social Security number must apply to the IRS for an ITIN and then use the ITIN on any return, statement, or other document which requires a taxpayer identifying number

Under the new procedures, most applicants must now submit original documentation by mail or travel to Taxpayer Assistance Centers (TACs) to have documents certified, making the application process more difficult

Since December 17, 2003, the IRS has required ITIN applicants with a filing requirement to attach a valid federal tax return with their application (unless they qualify for an exception).

On June 22, 2012, the IRS implemented temporary changes that required all ITIN applicants to submit original documents supporting the information on their applications. Under these procedures, applicants could no longer submit notarized copies and had to send in original documentation, even if a certified acceptance agent (CAA) reviewed and certified the documentation.

On November 29, 2012, the IRS announced revised procedures for the 2013 filing season that require applicants to submit original documentation or copies certified by the issuing agency.

Although the IRS allows CAAs to submit copies of documentation for primary and secondary taxpayers after reviewing original documentation or certified copies, CAAs must still send in original documentation for all dependent applicants.

A limited number of TACs can certify documents for primary, secondary, and dependent taxpayers.

The Revised Procedures Create an Impediment for Taxpayers Required to File Returns.

The recent changes to the ITIN program have made it difficult for taxpayers to file returns.

More on ITINs to follow in later posts.

Legal Defense?

The complexities of obtaining a U.S. TIN begs the question: “Is it a legal defense for a taxpayer to NOT file U.S. tax returns, international information returns, if it is particularly difficult (or nearly impossible in some cases) for that individual to even obtain a TIN?”

Will such a taxpayer have a “reasonable cause” defense to avoid penalties in the case of an audit? These are questions unanswered by any case law to date.

USCs throughout the world are required by FATCA to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . . “

As FATCA requires overseas individuals, including USCs to certify under penalty of perjury their U.S. taxpayer identification number (and if they have none), they necessarily will not be able to comply with this basic reporting requirement.

Will these individuals have a defense under the law for not complying under these circumstances?

Will the government provide relief for these individuals?

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms are set forth here. The new form requires the address overseas of the individual.

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

“mark to market” taxation on their worldwide assets,

40% inheritance tax to U.S. beneficiaries,

40% tax on gifts to U.S. beneficiaries,

etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”

Persons Living Outside the U.S. ***Does it still make sense?

Persons Living Outside the U.S. ***Does it still make sense?

methods of the federal government in collecting this type of TECS information. Indeed, there are specific provisions granting broad use of taxpayer information when the government alleges there is a “terrorist incident, threat, or activity” as that term is defined in

methods of the federal government in collecting this type of TECS information. Indeed, there are specific provisions granting broad use of taxpayer information when the government alleges there is a “terrorist incident, threat, or activity” as that term is defined in  (“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.

(“LPRs”) to important U.S. federal tax consequences to them. It’s primary focus relates to those USCs or LPRs who are contemplating renouncing their citizenship or abandoning their permanent residency status.