Does IRS Notice 2009-85 regarding expatriation have the “force of law”?

The above statement may sound quite provocative, until one explores in more detail some of the basic principles identified by the U.S. Supreme Court.

IRS Notice 2009-85 is the guidance issued by the IRS after Section 877A was adopted in 2008 and attempts to address a number of issues regarding the mark to market rules. This IRS Notice is a type of so-called “IRB” guidance (Internal Revenue Bulletin). Other IRS guidance that falls into this “IRB” guidance category includes revenue rulings and revenue procedures.

Two key Supreme Court cases, Mayo Clinic and Home Concrete and the 3rd Circuit Cohen decision, among many others, help articulate when such IRS authority is valid, and when it can be successfully challenged by taxpayers. A thoughtful law review article by Kristin Hickman, Unpacking the Force of Law, articulates in much detail the law in this regard and when IRS guidance, specifically including IRS Notices are subject to other U.S. laws, including the Administrative Procedures Act (“APA”).

Below is a list of some of the provisions of IRS Notice 2009-85 that seem to fall outside the language of the statute:

What are the consequences if a former USC or LPR does not comply with one or more of the above requirements that are only set forth in a Notice and not the statute?

Can the IRS make a determination that the taxpayer is a “covered expatriate”, even if they otherwise do not meet the asset or tax liability thresholds?

There is no “timely filed” requirement in the statute or even an inference in it, as to the time and effective nature of notifying the IRS?

Can the IRS successfully argue that the certification requirement of Section 877(a)(2)(C) has not been satisfied and the individual is a “covered expatriate” if IRS Form 8854 is not “timely filed” as defined by the IRS in the Notice?

Must a taxpayer necessarily agree to “such other treatment as the Secretary determines” appropriate, even if such determination is contrary to the terms of an applicable income tax treaty? Can the Secretary unilaterally override the terms of an income tax treaty negotiated between two countries?

These and other questions remain as a result of IRS Notice 2009-85.

???????????????? ?Please click here to view the above in Chinese.?

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

Probably the most misunderstood concept in the U.S. tax expatriation law provisions is Section 877(a)(2)(C) for several reasons.

1. People of modest means with modest to little income and little to no assets can fall into this category.

2. Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45

3. Lawful permanent residents (“LPRs”) can inadvertently fall into this category without doing anything, other than living principally in a country outside the U.S., which has a U.S. income tax treaty. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9. At the end of this post is a list of the countries with U.S. income tax treaties.

4. Few individuals understand exactly what must be included and reported in IRS Form 8854 to be able to satisfy the certification requirement above. For more details, see What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

The relevant provisions of Section 877(a)(2)(C) are highlighted below:

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Failure to certify truthfully about compliance with U.S. tax law for 5 years, as set forth above in the statute, means the individual necessarily will be a “covered expatriate.” Does this mean that if a U.S. citizen who renounces citizenship or a LPR who abandons their green card, will necessarily be a “covered expatriate” if they fail to follow IRS Notice 2009-45 “Guidance for Expatriates Under Section 877A”?

What steps will the IRS take if someone intentionally does not comply with the certification requirement? Will they become a target of a criminal investigation, and under what circumstances? What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

There are many pending and open questions not answered by current law, as the U.S. Treasury has yet to publish regulations under Section 877A, 877 or 2801.

APPENDIX – Countries with Income Tax Treaties with the United States

What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Below is a fairly detailed summary of the type of tax crimes that are commonly investigated by IRS Criminal Investigation (“CI”) agents.

As has already been noted, TaxAnalysts reporter Jaime Arora reported in the 3 March 2014, Worldwide Tax Daily certain comments made by Mr. Jeffrey Cooper, who is the deputy director of the IRS Criminal Investigation division’s international operations. It was reported that IRS CI is looking into why people are making the choice to shed their U.S. citizenship; whether it is related to any particular laws. Cooper was quoted at the Federal Bar Association’s Section on Taxation’s 38th Annual Tax Law Conference held on February 28, 2014.

TaxAnalysts journalist Arora quoted Cooper as identifying why people are making the choice and “If we find something, we do; if not, we just move on,” he said.

It is common policy for the IRS CI not to provide information on how they commence taxpayer investigations, including how they obtain U.S. citizenship renunciation referrals or documents. There could be a number of ways these investigations are commenced. It may be as simple as taking the list from the Quarterly Publication of Individuals, Who Have Chosen to Expatriate – Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G and start reviewing their tax return files (IRS Forms 1040, 8854, etc.) along with FBAR filings.

IRS CI tax investigations generally focus on false documents or false statements, evasion of taxation, aiding and abetting of the above along with other related tax and Bank secrecy (Title 31) crimes.

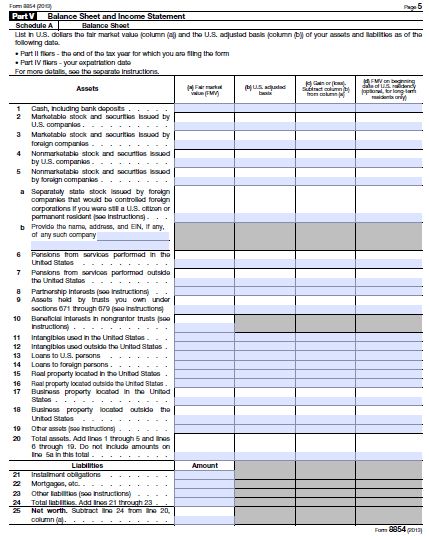

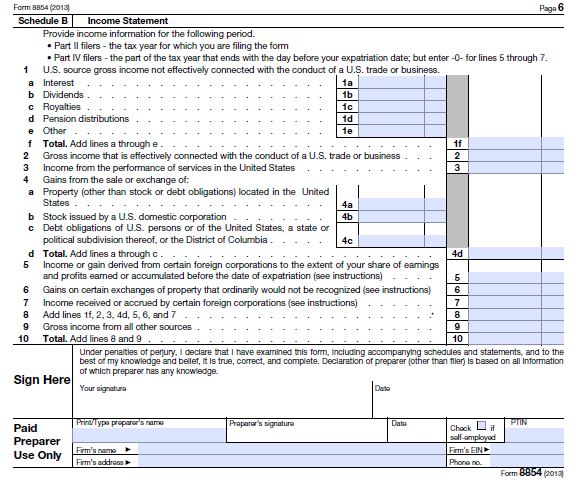

The tax reporting process for expatriates is extensive, including the basic requirement of signing IRS Form 8854 under penalty of perjury, which provides as follows on the last page of the form:

There are a host of reporting requirements and factual information that must be provided under Sections 877 and 877A, for all persons (including those with little to no assets), specifically including filing IRS Form 8854 which asks for a “boat load” of asset, income, liability and tax information. A former U.S. citizen or LPR always needs to be careful that the information provided is true, accurate and complete. See Part V of the form.

A summary of these crimes is set out below:

1. Criminal Offenses under Title 26 (Federal Tax Law)

a. Tax Evasion (IRC Section 7201)

b. Filing a False Return or Other Document – Perjury (IRC Section 7206(1) )

(i) Aiding or assisting in the perpetration of a false or fraudulent document (26 U.S.C. § 7206(2))

(ii) Removal or concealment with intent to defraud, commonly related to untaxed liquor (26 U.S.C. § 7206(4))

(iii) Compromises and closing agreements involving fraud or concealment (26 U.S.C. § 7206(5))

c. Failure to File Return, Supply Information, or Pay Tax – (IRC § 7203 – Misdemeanor – up to 12 months imprisonment)

d. Fraudulent Returns, Statements, or Other Documents (IRC § 7207)

e. “Structuring” Transactions to Evade Cash Reporting (IRC § 6050I)

In addition to these tax specific crimes, other key crimes commonly used by IRS CI agents in tax cases, particularly international cases, include:

2. Tax Related Criminal Offenses under Titles 18 and 31 (Not Tax Law Specific)

a. Conspiracy (Section 371 of Title 18)

(i) Elements of the Offense

(ii) Penalties and Statute of Limitations

b. False Statements (Title 18 U.S.C. § 1001)

(i) Penalties and Statute of Limitations

c. Perjury

d. Mail fraud

e. Principals and those Who Aid and Abet (Title 18)

f. Accessory After the Fact

Finally, it is worth noting that the government regularly collects information from internet resources, such as blogs and e-mails as they build a case for criminal prosecution. A former head of the Tax Division at the U.S. Department of Justice once told me that “e-mails and internet communications was God’s gift to prosecutors”.

???????????????? ?Please click here to view the above in Chinese.?

What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

Many lay p ersons are stumped as they try to understand the tax consequences of Sections 877 and 877A. The language in the drafting of the statutes is not so clear. Be careful to understate the meaning and how the IRS interprets the law.

ersons are stumped as they try to understand the tax consequences of Sections 877 and 877A. The language in the drafting of the statutes is not so clear. Be careful to understate the meaning and how the IRS interprets the law.

One of the greatest risks for anyone who wants to self-diagnose their path towards becoming a former U.S. citizen, is Section 877(a)(2)(C). To be blunt, anyone who renounces their citizenship at the Embassy or Consulate will find that process relatively easy. However, no one at the U.S. Department of State will provide tax advice or try to interpret the meaning of Section 877(a)(2)(C). Indeed, the Foreign Affairs Manual used to read to the person taking the oath, simply provides the standard overview language of “special tax consequences” arising form the renunciation.

Even the most economically modest individual, with little assets or income, can fall into this trap for the unwary – Section 877(a)(2)(C). The statute is spelled out below –

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

The provision is clear that anyone who does not satisfy it, will be a “covered expatriate” and hence subject to the taxation and reporting requirements under Sections 877 and 877A and 2801.

This is worth understanding well, before rushing off to take the oath at the U.S. Embassy or the U.S. Consulate.